The allure of Texas is undeniable, a vast and diverse state that offers a tapestry of experiences, from the vibrant urban centers of Houston and Dallas to the artistic charm of Austin, the historic depth of San Antonio, and the serene beauty of its Hill Country and Gulf Coast. For many, a visit isn’t enough; the desire to establish a more permanent presence, whether for an extended lifestyle journey, a vacation retreat, or a strategic investment, becomes compelling. This grand state, known for its friendly hospitality, burgeoning economy, and unique cultural identity, attracts travelers, business professionals, and families alike, all seeking to carve out their niche.

Whether you’re dreaming of a sprawling ranch, a chic urban loft, a cozy family home, or a property to capitalize on the state’s thriving tourism industry, the path to ownership in Texas involves a critical financial component often overlooked in the initial excitement: closing costs. These are the fees and expenses, beyond the purchase price, that both buyers and sellers typically incur to finalize a real estate transaction. Understanding “how much are closing costs in Texas?” is not just a matter of financial prudence; it’s an essential step in planning your long-term stay, securing your dream vacation home, or making a sound accommodation investment within this dynamic state. Neglecting to account for these costs can significantly impact your budget, turning a promising adventure into an unexpected financial hurdle.

This guide aims to demystify closing costs in Texas, providing a comprehensive overview that aligns with the considerations of travelers exploring longer stays, lifestyle enhancements, and property investments. We’ll explore the various components that make up these costs, delve into Texas-specific nuances, and offer insights to help you budget effectively, ensuring your journey into Texas real estate is as smooth and predictable as a scenic drive through the Big Bend National Park.

Unpacking Closing Costs: What Are They?

Before diving into the specifics of Texas, it’s crucial to understand the general nature of closing costs. Simply put, these are the administrative and legal fees associated with transferring property ownership from one party to another. They are typically paid at the closing, the final stage of a real estate transaction where documents are signed, and ownership officially changes hands. These costs are separate from your down payment and monthly mortgage payments and can encompass a wide range of services and fees from various parties involved in the transaction.

For anyone considering a move, a long-term stay, or an investment in Texas accommodation – be it a personal residence, a rental property, or even a boutique hotel – understanding these fees is paramount. They represent a significant upfront expense that needs to be factored into your overall financial planning, preventing any unpleasant surprises that could derail your lifestyle aspirations or investment strategies.

The exact amount and types of closing costs can vary widely depending on the location within Texas, the type of property, the complexity of the transaction, and the specific terms of your mortgage loan. However, they generally fall into several main categories:

Lender-Related Fees

When financing a property purchase, your mortgage lender will impose several fees for processing your loan. These are often some of the largest components of closing costs. Examples include:

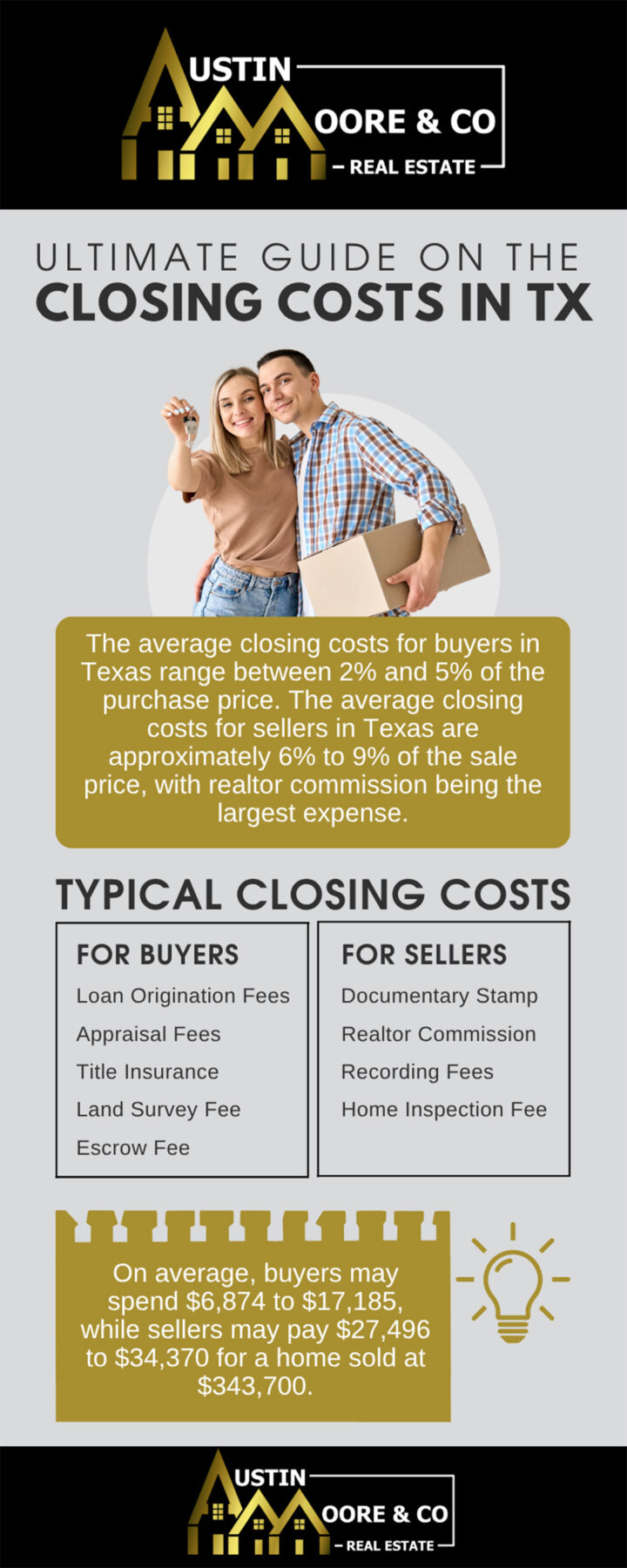

- Loan Origination Fee: A fee charged by the lender for processing your loan application, underwriting the loan, and preparing loan documents. It’s often expressed as a percentage of the loan amount (e.g., 0.5% to 1%).

- Application Fee: Covers the cost of processing your loan application, including credit checks and administrative tasks.

- Underwriting Fee: A fee for evaluating the risk of lending to a borrower.

- Appraisal Fee: Paid to a professional appraiser to determine the market value of the property, which the lender requires to ensure the property is worth the loan amount. This is vital for protecting the lender’s investment and indirectly, yours.

- Credit Report Fee: Covers the cost of obtaining your credit history from credit bureaus.

- Discount Points (Optional): Fees paid to the lender in exchange for a lower interest rate on your mortgage. Each “point” is typically 1% of the loan amount. This is a strategic decision for many, impacting long-term payment plans versus upfront costs.

Third-Party Service Fees

These fees are paid to various professionals and services essential for a smooth transaction but are not directly tied to the lender.

- Title Search and Title Insurance: A title company conducts a search to ensure there are no liens, unpaid taxes, or other encumbrances on the property’s title. Title insurance protects both the lender (lender’s policy) and the buyer (owner’s policy) against future claims that might arise regarding ownership of the property. In Texas, the seller often pays for the owner’s title policy, which is a significant saving for the buyer compared to many other states.

- Escrow Fees / Closing Fees: Paid to the escrow or title company for facilitating the closing process, holding funds, and ensuring all legal requirements are met.

- Survey Fee: In many Texas transactions, a survey is required to verify property lines and ensure there are no encroachments. This is particularly important for larger properties or those with unique boundaries.

- Pest Inspection Fee: Ensures the property is free from termites or other wood-destroying insects.

- Home Inspection Fee: While optional, a professional home inspection is highly recommended to uncover any potential issues with the property’s structure or systems, saving you from costly surprises down the road. This is a critical investment, especially when purchasing a property that might serve as a long-term residence or a future rental.

- Attorney Fees: Though Texas is not an “attorney closing state,” you might choose to hire a real estate attorney to review documents, especially for complex transactions or commercial properties like boutique hotels.

Prepaid Costs and Escrows

These are not strictly “fees” but rather expenses paid at closing that cover future obligations related to homeownership.

- Prepaid Property Taxes: Buyers often need to prepay a portion of their annual property taxes at closing, typically for a few months to a year, to get the escrow account started. Texas has relatively high property taxes compared to other states, making this a significant upfront cost.

- Prepaid Homeowner’s Insurance: Lenders typically require homeowners insurance, and you’ll usually need to pay the first year’s premium upfront at closing. Given Texas’ diverse climate and potential for severe weather, selecting appropriate coverage is crucial.

- Escrow Account Deposits: Many lenders require an escrow account to hold funds for future property tax and homeowner’s insurance payments. A deposit (typically 2-3 months’ worth) is made at closing to fund this account.

Title and Government Fees

These are fees collected by state and local governments for recording the transaction.

- Recording Fees: Paid to the county recorder’s office to officially record the transfer of deed and mortgage documents.

- Transfer Taxes (Not typically in Texas): Unlike many other states, Texas does not have a state or local real estate transfer tax, which is a notable advantage for buyers and sellers here.

Understanding these categories provides a foundational knowledge of what to expect, allowing for more accurate budgeting, whether you’re investing in a property for personal use, a long-term accommodation solution, or to contribute to the thriving tourism sector in Texas.

The Texas Landscape: Average Closing Costs and Factors

Now that we’ve outlined the typical components, let’s focus on the specifics for Texas. While closing costs can range, a general rule of thumb for buyers in Texas is to anticipate paying approximately 2% to 5% of the loan amount (or 1% to 3% of the purchase price, if paying cash or a large down payment) in closing costs. This percentage can fluctuate based on numerous factors, making it essential to obtain a detailed estimate for your specific situation.

A unique aspect of Texas is the customary allocation of certain costs between buyer and seller. As mentioned, sellers often pay for the owner’s title policy, which is a significant expense. However, buyers typically bear the brunt of loan-related fees and other transaction costs.

Geographic Variations within Texas

The vastness of Texas means that closing costs can vary by region and even by specific city. Factors like local recording fees, property tax rates, and market competitiveness can influence the final tally.

- Major Metropolitan Areas: In bustling cities like Houston, Dallas, Austin, and San Antonio, property values tend to be higher, which can lead to higher dollar amounts for fees based on a percentage of the loan or property value. While the percentage might stay relatively consistent, the actual cost will be greater. These areas also often have more competitive service providers, which can sometimes lead to slight variations in fees for appraisals, inspections, and title services.

- Rural Areas and Smaller Cities: In regions like the Rio Grande Valley, El Paso, or smaller communities in the Hill Country or East Texas, property values might be lower, resulting in lower absolute closing cost figures. However, the availability of certain services might be less, or specific local regulations could apply.

- Coastal Regions: Areas along the Gulf Coast may have higher insurance premiums, especially for wind and flood insurance, which would be part of your prepaid costs at closing. This is a crucial consideration for anyone envisioning a beach house or coastal retreat.

Impact of Property Type and Value

The kind of property you’re acquiring significantly impacts closing costs.

- Residential Homes: The most common type of transaction, these costs align with the general percentages mentioned.

- Luxury Properties: Higher purchase prices mean higher loan amounts, resulting in greater dollar values for percentage-based fees (e.g., loan origination, title insurance, appraisal). The complexity of legal documents for high-value properties might also incur slightly higher attorney review fees if sought.

- Investment Properties/Commercial: If you’re buying a multi-unit property, a bed-and-breakfast, or a commercial space for a hotel, the transaction can be more complex. This might involve additional environmental assessments, specialized surveys, and increased legal fees due to the intricate nature of commercial real estate. These investments, while potentially lucrative for tourism and accommodation, come with a higher initial financial hurdle in closing costs.

- Land: Raw land purchases might have fewer inspection-related fees but could involve more extensive survey and environmental study costs.

Loan Type and Lender Influence

The type of mortgage loan you secure also plays a role in your closing costs.

- Conventional Loans: Typically have standard closing costs as outlined.

- FHA/VA Loans: Government-backed loans often have specific rules regarding what fees can be charged and by whom. FHA loans, for instance, include an upfront mortgage insurance premium (UFMIP) that can be financed or paid at closing, adding to the initial cost. VA loans, a fantastic benefit for veterans, typically have a VA funding fee, though some eligible veterans are exempt. These loan types are excellent for individuals looking to establish a new lifestyle in Texas with favorable terms but require careful understanding of their unique fee structures.

- Jumbo Loans: For high-value properties, jumbo loans often have stricter underwriting requirements and might carry slightly higher fees due to their increased risk and complexity.

- Lender-Specific Fees: Different lenders will have varying fee structures for loan origination, processing, and underwriting. Shopping around for lenders can yield not only a better interest rate but also potentially lower closing costs. Always compare the Loan Estimates from multiple lenders carefully.

Understanding these variables is key to accurately predicting your financial outlay. A detailed Loan Estimate, provided by your lender within three business days of applying for a mortgage, will break down all expected closing costs, helping you budget for your Texas property dream.

Beyond the Transaction: Closing Costs in Your Texas Lifestyle & Investment Strategy

For those whose interests extend beyond a transient visit – whether envisioning a permanent move, a seasonal escape, or a strategic investment in the vibrant Texas economy – understanding closing costs is not just a regulatory necessity; it’s a critical component of your broader lifestyle and financial strategy. The decision to buy property here intertwines deeply with how you plan to live, travel, and even contribute to the state’s flourishing tourism and accommodation sectors.

Investing in Texas Real Estate: Vacation Homes & Rental Properties

Texas’ diverse attractions, from the historical Alamo in San Antonio to the live music scene of Austin and the space exploration centers near Houston, make it a prime location for real estate investment, particularly in vacation rentals or longer-term accommodation options.

- Vacation Homes: If you’re acquiring a second home in a popular tourist destination like Fredericksburg in the Hill Country or along the Gulf Coast (e.g., Galveston or South Padre Island), closing costs are an essential part of the initial capital outlay. Factoring these into your budget from the start ensures you have enough reserves not just for the purchase but also for potential renovations or furnishing to make it appealing to future renters. Such an investment can offer both a personal retreat and a revenue stream, enhancing your travel lifestyle.

- Rental Properties: For those looking to capitalize on Texas’ growing population and robust job markets, investing in long-term rental properties in cities like Dallas, Fort Worth, or Plano can be a smart move. Closing costs directly impact your initial return on investment. A lower closing cost means more capital available for property management, maintenance, or further investments, directly affecting the profitability of your accommodation venture.

- Hotels & Guesthouses: For larger-scale investors interested in the hospitality sector, purchasing an existing hotel or developing a new one involves substantial closing costs, often compounded by commercial lending fees, extensive due diligence, and potentially more complex legal structures. These are significant considerations for anyone looking to enter the Texas tourism market as a provider of accommodation.

Relocation and Long-Term Stays: Making Texas Home

For individuals or families making a lifestyle change to Texas, perhaps for a new job, retirement, or simply a desire for a different pace of life, the purchase of a primary residence is a significant step.

- Budgeting for the Move: Beyond the excitement of choosing a neighborhood, envisioning decor, or exploring local attractions, the practical aspect of closing costs demands attention. These costs, along with moving expenses, utility setup fees, and initial furnishing costs, form the complete financial picture of your relocation. Adequate budgeting for closing costs ensures a smoother transition, allowing you to settle into your new Texas life without immediate financial strain.

- Long-Term Accommodation: For those planning extended stays that might eventually lead to permanent residency, comparing the costs of long-term rentals versus purchasing property is crucial. While renting avoids closing costs, it also misses out on equity building. Understanding the total cost of ownership, including closing costs, helps in making an informed decision that aligns with your long-term travel and lifestyle goals.

Budgeting for Your Texas Dream: Tips and Considerations

Effective financial planning is key to navigating closing costs smoothly.

- Get a Detailed Loan Estimate: As mandated by federal law, your lender must provide a Loan Estimate within three business days of receiving your loan application. This document details all estimated closing costs, allowing you to compare offers from different lenders.

- Shop Around for Service Providers: While some fees are fixed, you often have the option to choose your title company, home inspector, and survey company. Comparing quotes can save you hundreds, if not thousands, of dollars.

- Negotiate with the Seller: In a buyer’s market, or depending on the specifics of your offer, you might be able to negotiate for the seller to pay some of your closing costs or offer seller credits. This can be a significant help, especially for first-time homebuyers or those operating on a tighter budget.

- Factor into Your Overall Budget: Do not consider closing costs as an afterthought. Include them in your initial property search budget alongside your down payment. This holistic approach ensures you have a realistic understanding of the total funds required to acquire your piece of Texas.

- Understand Prepaid Expenses: Remember that some closing costs are prepaid expenses for future liabilities like property taxes and homeowner’s insurance. While they are paid upfront, they cover services you will use, making them distinct from pure transaction fees.

Ultimately, whether you’re drawn to Texas for its dynamic cities like Austin or Corpus Christi, its serene landscapes, or its promising economic climate, acquiring property is a significant commitment. By thoroughly understanding “how much are closing costs in Texas,” you empower yourself to make informed decisions that support your travel, accommodation, and lifestyle aspirations. This preparedness ensures your venture into Texas real estate is a rewarding chapter in your life’s journey, setting the stage for countless unforgettable experiences in the Lone Star State.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.