For many individuals approaching their golden years, the question of where to retire is often as much about lifestyle and climate as it is about financial prudence. Among the myriad factors influencing this monumental decision, taxation, particularly on retirement income like Social Security, stands out as a critical concern. Prospective retirees, from those dreaming of sun-drenched beaches to vibrant cityscapes, frequently cast their gaze towards the Golden State, California. Renowned for its unparalleled beauty, diverse cultural experiences, and an array of world-famous landmarks and attractions, California presents an alluring prospect for retirement. However, the state’s reputation for a high cost of living often leads to apprehension regarding its tax policies. So, let’s address the burning question directly: Is Social Security income taxed in California?

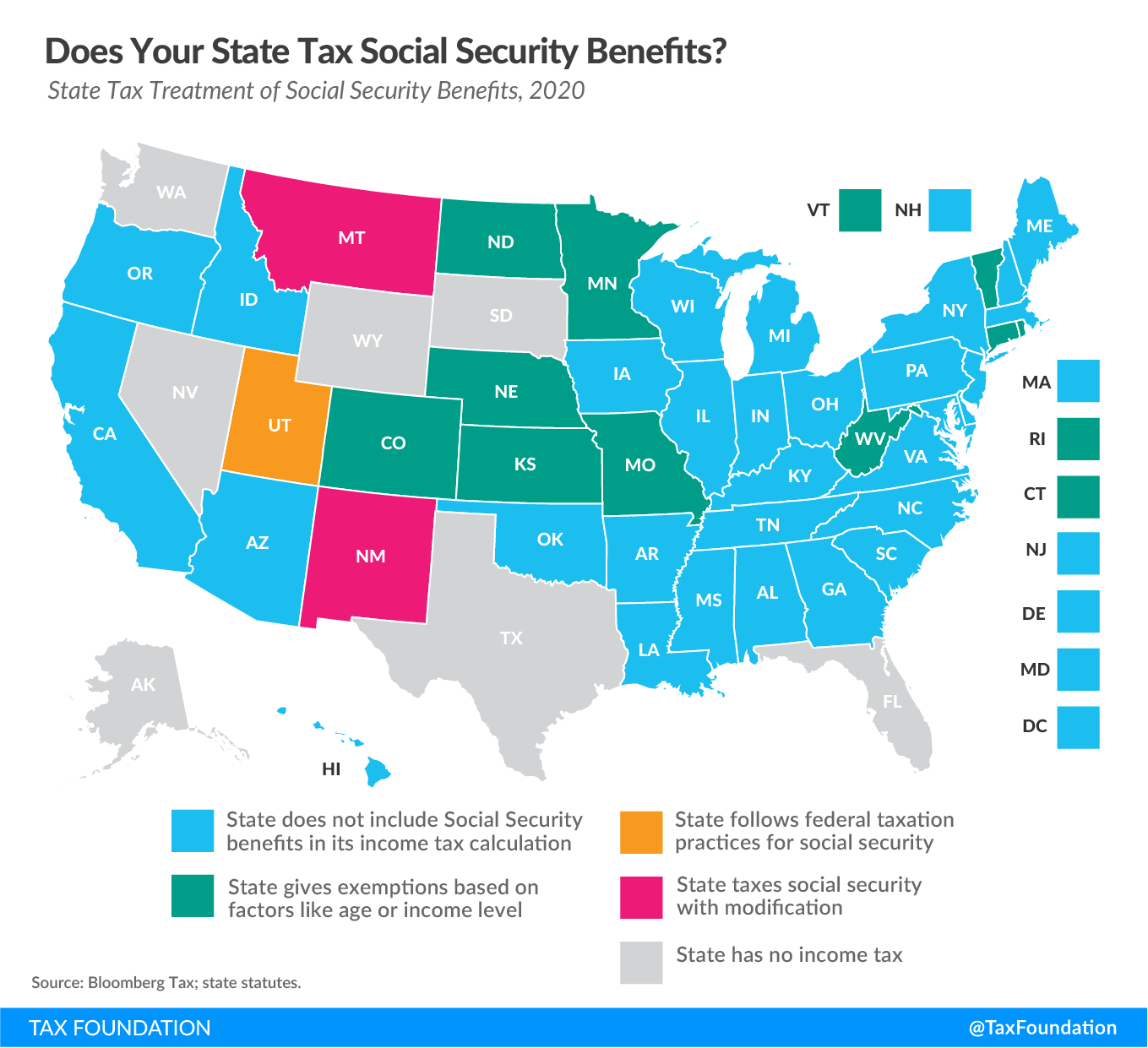

The short, reassuring answer for those considering a life of leisure, exploration, or simply serene relaxation in California is no. The State of California does not impose a state income tax on Social Security benefits. This makes it one of the many states that offer this particular financial advantage to its retired residents. For anyone planning their retirement lifestyle, whether it involves luxury travel through Napa Valley or budget travel exploring the vibrant neighborhoods of Los Angeles, understanding this specific tax relief is a significant piece of the financial puzzle.

The Golden State’s Golden Rule: Social Security Benefits Untaxed

California’s stance on Social Security benefits is a significant draw for retirees from across the United States and beyond. While other forms of income may be subject to state taxation, your monthly Social Security check is explicitly exempt from California state income taxes. This policy stands in stark contrast to a handful of other states that do tax these benefits, providing a clear financial advantage for those who choose to call the Golden State home during their retirement years.

No State Income Tax on Your Benefits – A Welcome Relief for Many

For a state often associated with higher taxes and a premium cost of living, this particular exemption provides a welcome financial buffer. It means that the full amount of your Social Security benefits, as determined by the federal government, will arrive in your bank account without any deductions from the State of California. This can significantly impact a retiree’s monthly budget, freeing up funds for everything from exploring California’s myriad destinations to enjoying its world-class food scene, or simply ensuring a more comfortable accommodation situation, whether it’s a cozy apartment or a luxurious resort suite.

This tax-free status on Social Security benefits helps preserve capital that can be allocated to enriching one’s retirement experiences. Imagine using those extra funds for a stay at a boutique hotel in San Francisco or perhaps a guided tour of Yosemite National Park. The possibilities for travel and leisure within California are endless, and not having your Social Security benefits diminished by state taxes allows for greater flexibility in pursuing these enriching endeavors.

What Qualifies as “Social Security Benefits”?

When we discuss Social Security benefits, we are generally referring to the retirement, disability, and survivor benefits administered by the Social Security Administration. These are the payments that the State of California exempts from its income tax. It’s important to differentiate these from other forms of retirement income, such as private pensions or distributions from 401(k)s and IRAs, which are typically subject to California’s income tax, a topic we will delve into further.

Understanding the Federal Angle: Provisional Income and Your Social Security

While California provides a state-level tax exemption, it’s crucial for retirees to remember that Social Security benefits can still be subject to federal income tax. This is a common area of confusion, as the federal government has its own rules for taxing these benefits, which are independent of state regulations.

How Federal Taxes Still Apply: Provisional Income Calculation

The federal taxation of Social Security benefits depends on what the IRS refers to as your “provisional income.” This calculation includes your adjusted gross income (AGI), any tax-exempt interest (like from municipal bonds), and 50% of your Social Security benefits. Based on certain thresholds for this provisional income, a portion of your Social Security benefits (up to 85%) may become taxable at the federal level.

For single filers, if your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If your provisional income exceeds $34,000, up to 85% of your benefits may be subject to federal tax. For those filing jointly, the thresholds are between $32,000 and $44,000 for 50% taxation, and above $44,000 for up to 85% taxation. These federal guidelines are universal across all states, including California. Therefore, even if you reside in a state that doesn’t tax Social Security, you might still owe federal taxes on a portion of your benefits.

Planning Ahead: Managing Your Taxable Income

Understanding this federal component is vital for comprehensive retirement planning. Retirees in California should consider strategies to manage their provisional income to potentially reduce their federal tax liability on Social Security. This could involve careful planning of withdrawals from traditional IRAs or 401(k)s, managing capital gains, or investing in tax-advantaged accounts. Consulting with a financial advisor is always recommended to tailor a strategy that aligns with your specific financial situation and retirement goals, whether those goals involve extended stays in a Palm Springs resort or regular visits to iconic landmarks like the Golden Gate Bridge.

Beyond Social Security: Navigating California’s Broader Tax Landscape

While the exemption of Social Security benefits from state income tax is certainly a positive for retirees in California, it’s important to consider the broader tax environment. California has a progressive state income tax system, high sales taxes, and generally high property taxes, all of which can significantly impact the overall cost of living and retirement lifestyle.

Other Retirement Income: Pensions, 401(k)s, and IRAs

Unlike Social Security, other forms of retirement income are subject to California’s state income tax. This includes distributions from private and public pensions, as well as withdrawals from traditional 401(k)s and IRAs. California’s income tax rates are among the highest in the nation, ranging from 1% to 13.3% depending on your income bracket. For retirees with substantial retirement savings, this can translate into a significant tax bill. Careful financial planning, including considering Roth conversions or other tax-efficient withdrawal strategies, becomes paramount to preserve your retirement nest egg while enjoying all that California has to offer, from the pristine beaches of San Diego to the bustling metropolis of Los Angeles.

Property Taxes: A Major Consideration for Homeowners and Accommodation Seekers

Property taxes are another substantial financial consideration for anyone looking to retire in California, especially those planning to purchase a home or invest in long-term accommodation options. While the base property tax rate in California is capped at 1% of the assessed value (thanks to Proposition 13), local bonds and special assessments can increase the effective rate. Given California’s high real estate values, especially in desirable areas like coastal towns or regions close to major cities such as San Francisco and San Diego, annual property tax bills can be considerable. This is an important factor for prospective homeowners to weigh against the benefit of untaxed Social Security. Those opting for rental accommodation or extended stays in hotels and resorts will find these costs indirectly factored into their rental prices or booking fees.

Sales Tax and Lifestyle Spending: Impact on Tourism and Daily Life

California has one of the highest statewide sales tax rates in the United States, currently at 7.25%, with local district taxes often pushing the combined rate significantly higher, reaching over 10% in some areas. This affects virtually all purchases, from groceries and clothing to dining out and buying tickets for attractions. For retirees who plan to take advantage of California’s vibrant tourism scene, enjoy its diverse food culture, or simply manage daily expenses, the sales tax can add up. Whether you’re purchasing souvenirs in Hollywood, dining at a gourmet restaurant, or simply stocking up on supplies for your RV travel, the sales tax is an unavoidable part of the financial landscape.

Capital Gains and Other Investments

California treats capital gains as ordinary income, meaning they are taxed at your regular state income tax rate, which can be as high as 13.3%. This is a critical consideration for retirees who plan to sell assets, real estate, or have significant investment portfolios generating taxable gains. Understanding how these gains are taxed is essential for strategic financial planning, especially for those who might be funding their luxury travel or investing in various properties.

Why Retirees Still Flock to California: More Than Just Taxes

Despite the often-cited high cost of living and certain tax burdens, California continues to be an incredibly popular choice for retirees. The allure extends far beyond financial considerations, drawing individuals with its unique blend of natural beauty, cultural richness, and endless lifestyle opportunities.

Unparalleled Lifestyle and Diverse Destinations

California’s diverse geography offers something for everyone. From the sunny beaches of the Pacific Ocean to the majestic mountains of the Sierra Nevada, the tranquil deserts of Death Valley to the verdant vineyards of Napa Valley, the state is a playground for travel and exploration. Retirees can enjoy a mild climate year-round in many regions, fostering an active lifestyle that includes hiking, golfing, surfing, or simply enjoying scenic drives along Big Sur. The state boasts world-class attractions like Disneyland, vibrant arts scenes in San Francisco and Los Angeles, and a rich local culture in every corner. This incredible variety of destinations and experiences often outweighs the tax implications for those seeking an active and fulfilling retirement.

Access to World-Class Amenities and Healthcare

For many retirees, access to quality healthcare is a top priority. California is home to some of the nation’s leading medical facilities, hospitals, and specialists, offering peace of mind. Beyond healthcare, the state provides an abundance of amenities catering to a comfortable retirement, including diverse dining options, cultural institutions, educational opportunities, and a wide range of accommodation choices, from cozy apartments to sprawling resorts. Many communities offer specialized suites and facilities designed for senior living, complete with various amenities and services, ensuring a high quality of life.

Finding Your Perfect Niche: From Coastal Retreats to Desert Oases

Whether you dream of waking up to ocean breezes, living amidst the energy of a bustling city, or finding tranquility in a desert oasis, California has a perfect niche for every retiree. Regions like Lake Tahoe offer stunning natural beauty and outdoor activities, while areas around Silicon Valley provide access to innovation and urban conveniences. The sheer variety means retirees can choose a location that aligns perfectly with their desired pace of life, preferred climate, and specific interests, ensuring their retirement travel and daily living are as rewarding as possible.

Practical Planning for Your California Retirement Journey

Retiring in California requires meticulous planning, balancing the financial realities with the undeniable lifestyle benefits. Understanding the full picture of taxes, costs, and opportunities is key to a successful transition.

Budgeting for the Golden State: Accommodation, Activities, and Beyond

Given the general high cost of living, careful budgeting is paramount. This includes factoring in housing costs (whether renting an apartment, buying a home, or staying in various hotels or villas for extended periods), transportation, utilities, healthcare, and discretionary spending on travel, dining, and activities. While Social Security benefits are untaxed by the state, the savings may need to be strategically allocated to offset other expenses. Exploring options for budget travel within the state or seeking out more affordable accommodation in less expensive regions can help stretch your retirement dollars further.

Exploring Retirement Communities and Long-Term Stays

California offers numerous retirement communities and options for long-term stays, ranging from active adult communities with extensive amenities to assisted living facilities. Researching these options, including their costs and the services they provide, is an important step. Many hotels and resorts also offer discounted rates for longer stays, which can be an attractive option for those who wish to explore different areas before settling down, or for those who prefer the flexibility of not owning a property. Websites offering booking and comparison services can be invaluable resources for finding suitable and affordable arrangements.

Seeking Professional Financial Advice

Navigating the complexities of retirement finances in a state like California is best done with expert guidance. A qualified financial advisor who specializes in retirement planning and understands California’s tax laws can help you create a robust financial plan, optimize your income streams, and minimize your tax burden. They can offer personalized tips on everything from managing your investments to estate planning, ensuring your retirement journey in the Golden State is as financially secure as it is enjoyable.

In conclusion, for those contemplating a retirement filled with the distinctive charm and vibrant lifestyle of California, the answer to whether Social Security benefits are taxed at the state level is a definitive “no.” This significant advantage provides a compelling reason for many to choose the Golden State as their retirement haven. However, it is imperative to consider the broader financial landscape, including federal taxes on Social Security, California’s income tax on other retirement income, and its relatively high property and sales taxes. By understanding these nuances and engaging in thorough financial planning, retirees can effectively balance their financial realities with their aspirations for an enriching and fulfilling retirement amidst California’s iconic landmarks and endless destinations.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.