Understanding California’s tax landscape is crucial for both residents and visitors, especially when it comes to purchases made outside the state for use within its borders. While sales tax is a familiar concept, the use tax in California operates as a complementary levy, ensuring that tax is collected on tangible personal property purchased elsewhere but brought into California for consumption or use. This mechanism aims to create a level playing field, preventing individuals and businesses from avoiding California taxes simply by purchasing goods online or in neighboring states. Navigating this tax can seem complex, but by breaking down its intricacies, it becomes manageable for anyone engaging in commerce that touches the Golden State.

The Core Concept of California Use Tax

At its heart, California’s use tax is designed to capture tax revenue on items that would otherwise be subject to sales tax if purchased within the state. It’s not an additional tax on top of sales tax, but rather an alternative. If sales tax was already paid to another state at a rate equal to or greater than California’s combined state and local rate, then no use tax is due. The principle is simple: pay tax once on the purchase of goods for use in California.

Understanding the “Use” in Use Tax

The term “use” in “use tax” is broad and encompasses more than just physical consumption. In the context of California, “use” includes:

- Consumption: The act of using up or expending a tangible item.

- Storage: Keeping an item within the state, even if it’s not actively being used.

- Other Use: Any form of appropriation or exercise of dominion and control over an item within California, short of selling it in the regular course of business.

This expansive definition means that even if an item is purchased online from a seller outside of California, and no sales tax is collected at the time of purchase, the buyer is still obligated to report and pay the use tax to the state when that item is brought into or used in California. This applies to a wide range of items, from electronics and furniture purchased from out-of-state retailers to vehicles, boats, and aircraft imported into the state.

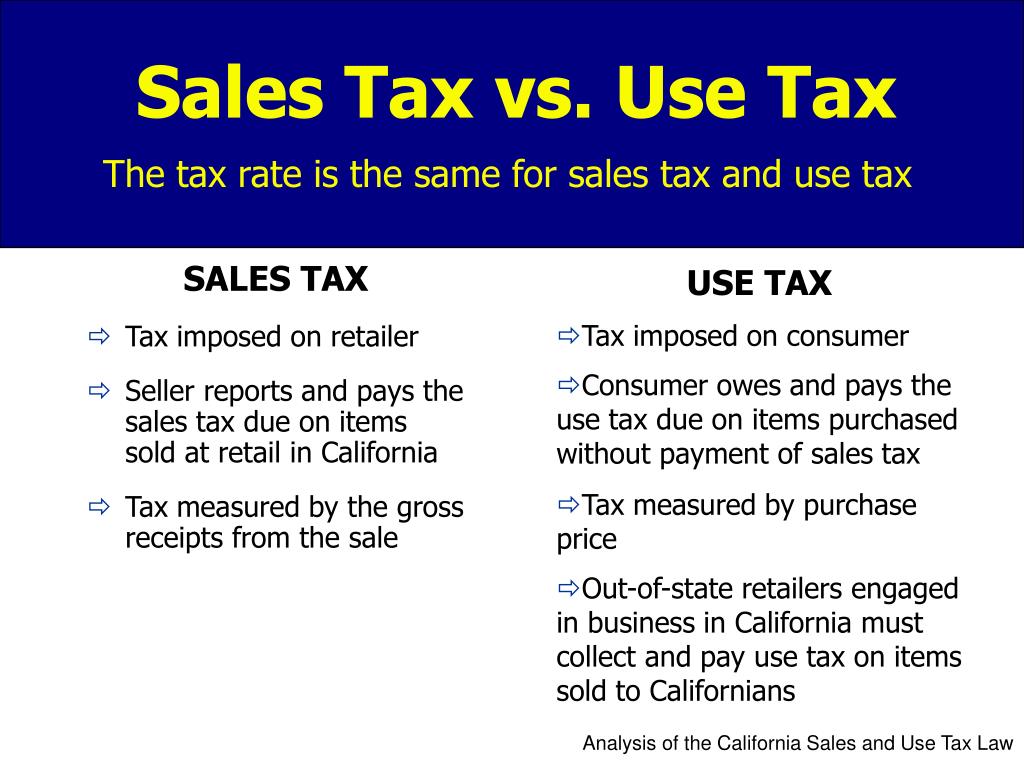

The Distinction from Sales Tax

It is vital to differentiate use tax from sales tax. Sales tax is levied at the point of sale by a retailer to a consumer within California. The retailer is responsible for collecting this tax from the buyer and remitting it to the state. Use tax, on the other hand, is a tax imposed on the consumer for the privilege of using, storing, or consuming tangible personal property in California that was purchased outside the state without paying the requisite California sales tax. The responsibility for remitting use tax generally falls directly on the individual or business making the purchase.

When is Use Tax Applicable in California?

California use tax is applicable in several common scenarios, particularly with the rise of e-commerce and cross-border shopping. The key factor is whether the item was purchased outside California and then brought into the state for use, storage, or consumption, and whether California sales tax was paid at the point of purchase.

Purchases from Out-of-State Retailers

One of the most frequent triggers for California use tax is purchasing goods from out-of-state retailers, especially those that do not have a physical presence in California and therefore do not collect California sales tax at the time of sale. This often includes online retailers, catalog sales, and even purchases made while traveling in other states.

- Online Shopping: When you order items from websites and the seller does not charge California sales tax, you are generally required to pay use tax on those items when they arrive in California. This is because California considers the use of the item within its borders to be taxable, regardless of where it was purchased.

- Catalog and Mail Order: Similar to online purchases, items bought through catalogs or by mail order from out-of-state vendors are subject to use tax if no California sales tax was collected.

- Purchases While Traveling: If you visit another state, such as Oregon (which has no sales tax) or Nevada, and purchase items for personal use back in California, you may owe use tax on those items. The tax is due when the item is brought into California.

Purchases of Specific High-Value Items

Certain categories of purchases, even if made in California, can still involve use tax implications, particularly when the transaction is structured in a way that circumvents sales tax. However, the most common application for use tax relates to items brought into California.

- Vehicles, Boats, and Aircraft: When you purchase a vehicle, boat, or aircraft outside of California and then register or operate it within California, you will typically owe use tax. The California Department of Motor Vehicles (DMV) or similar agencies often collect this tax during the registration process.

- Services: While use tax primarily applies to tangible personal property, certain services that involve the fabrication or incorporation of tangible personal property into a new product can also have use tax implications, particularly if the fabrication occurs out of state.

Exemptions and Credits

It’s important to note that not all out-of-state purchases are subject to use tax. California provides certain exemptions and credits to avoid double taxation.

- Sales Tax Paid to Other States: If you purchased an item in another state and paid sales tax to that state, and the rate of that tax was equal to or greater than the California combined state and local rate applicable to that item, then no use tax is due in California. For example, if you bought a product in Texas and paid the Texas state sales tax, you would generally receive a credit for the Texas tax paid against any California use tax liability.

- Exemptions for Specific Items: Certain items might be exempt from sales and use tax in California, regardless of where they are purchased. These exemptions typically apply to necessities or items deemed beneficial for public policy, such as certain food products or medical devices.

Calculating and Paying California Use Tax

Calculating and remitting use tax in California is a responsibility that falls on the individual or business. While it might seem daunting, the process is designed to be integrated into existing tax reporting mechanisms.

Determining the Applicable Rate

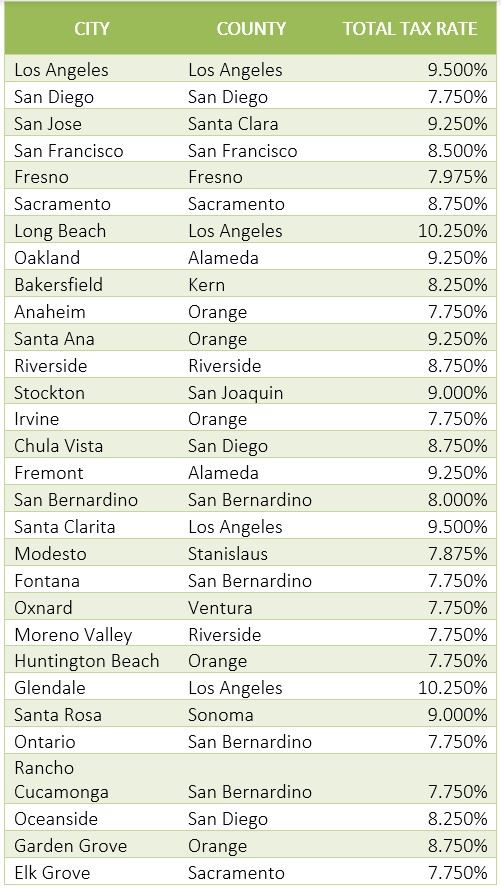

The use tax rate in California is the same as the combined state and local sales tax rate for the location in California where the item is first used, stored, or consumed. This rate varies by county and even by city, due to the addition of local district taxes. The California Department of Tax and Fee Administration (CDTFA) provides resources to help taxpayers determine the correct rate based on their specific location. For instance, a purchase used in Los Angeles County will be subject to the use tax rate specific to that county, which might differ from San Diego County.

Reporting Use Tax

The primary method for reporting and paying use tax is through your California income tax return or your seller’s permit tax returns.

- Individuals: If you are an individual consumer who has purchased taxable items out-of-state for use in California without paying sales tax, you will typically report and pay the use tax when you file your annual California income tax return (Form 540). The Franchise Tax Board (FTB) administers income tax, and the use tax is collected as part of that process.

- Businesses: Businesses that hold a seller’s permit are required to report and pay use tax on their regular CDTFA sales and use tax returns. This ensures that purchases made by the business for its own use, storage, or consumption within California, for which California sales tax was not paid, are accounted for. This includes items purchased for use in operations at facilities like a warehouse in Oakland or an office in San Francisco.

Record Keeping

Maintaining thorough records of out-of-state purchases is essential. This includes receipts, invoices, and any documentation showing sales tax paid to another state. These records serve as proof of payment and help substantiate any claims for credits or exemptions when reporting your use tax liability. For business operations, meticulous record-keeping is not only crucial for tax compliance but also for inventory management and operational efficiency.

Navigating Common Use Tax Scenarios and Avoiding Pitfalls

Understanding the practical implications of California use tax can help individuals and businesses avoid unintentional non-compliance. Being aware of common scenarios and potential pitfalls is key to responsible tax stewardship.

Online Purchases and Remote Sellers

The rise of e-commerce has made remote sellers a significant area of focus for use tax collection. While many large online retailers now collect California sales tax due to economic nexus laws, smaller online businesses or those operating from states without sales tax may still not collect it.

- Understanding “Economic Nexus”: California, like many states, has enacted economic nexus laws that require out-of-state sellers to register and collect California sales and use tax if their sales into the state exceed certain thresholds (e.g., $100,000 in gross sales or 200 separate transactions). This has increased the number of online transactions where sales tax is collected at checkout.

- Personal Use Items: For items intended for personal use, such as clothing, electronics, or home furnishings purchased from online retailers that do not collect sales tax, the individual consumer is responsible for paying the use tax. This might involve a small, individual payment or reporting it on your income tax return.

Use Tax on Tangible Personal Property Leased or Rented

The concept of use tax extends beyond outright purchases to include certain leases or rentals of tangible personal property. If you lease or rent tangible personal property from an out-of-state lessor and use that property in California, and no California sales tax was paid on the lease payments, you may owe use tax. This can apply to equipment rentals for events in Anaheim or machinery for temporary construction projects.

The “Drop Shipment” Scenario

A “drop shipment” occurs when a retailer takes an order from a customer but arranges for a third-party supplier to ship the goods directly to the customer. If the retailer is out-of-state and does not have a physical presence in California, they may not collect California sales tax. However, if the supplier is within California or has a nexus, the supplier might be required to collect and remit sales tax. If neither party collects the tax, the consumer is still responsible for the use tax when the item is used in California.

Penalties for Non-Compliance

The CDTFA enforces use tax compliance. Failure to report and pay use tax can result in significant penalties, interest, and back taxes. The state is increasingly sophisticated in identifying non-compliance, particularly with large purchases or through data matching with other agencies. It is always best to proactively comply with use tax obligations rather than face potential enforcement actions. This is especially true for businesses operating in California, where non-compliance can have severe financial and reputational consequences.

By understanding the nuances of California’s use tax, individuals and businesses can ensure they are meeting their obligations and contributing to the state’s revenue, which in turn supports public services and infrastructure throughout California, from the bustling streets of Los Angeles to the scenic coasts of Big Sur.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.