Florida, often lauded as the Sunshine State, beckons millions with its pristine beaches, vibrant cities, and world-class attractions. From the enchanting theme parks of Orlando to the Art Deco splendor of Miami’s South Beach and the tranquil beauty of the Everglades National Park, it’s a destination that promises unforgettable travel experiences and a desirable lifestyle for residents. Whether you’re planning a luxurious family vacation at Walt Disney World, an adventure at Universal Studios Florida, or considering a long-term stay in a charming coastal town, understanding the local nuances is key to a smooth journey. One often-overlooked aspect that can significantly impact both visitors and residents is the surprisingly high cost of car insurance. For many, the hefty premiums come as a shock, prompting the question: why is car insurance so expensive in Florida?

This comprehensive guide delves into the multifaceted reasons behind Florida’s elevated insurance rates, exploring how they intertwine with the state’s unique demographics, environmental challenges, legal framework, and thriving tourism industry. For anyone looking to explore the picturesque roads of Key West, navigate the bustling highways of Tampa, or simply enjoy the freedom of driving across this diverse state, comprehending these factors is essential for budgeting, planning, and ensuring peace of mind.

The Unparalleled Dynamics of Florida’s Roads: Population, Tourism, and Traffic

Florida’s allure as a top travel destination and a preferred place to live is a double-edged sword when it comes to car insurance. The state is experiencing rapid population growth, drawing new residents from across the globe seeking its warm climate, diverse culture, and economic opportunities. This influx of permanent residents, combined with an unparalleled volume of tourists, creates a unique and often challenging driving environment that directly impacts insurance premiums.

A Confluence of Drivers: Residents, Snowbirds, and Vacationers

Imagine the roads of Orlando during peak season, teeming with rental cars navigating unfamiliar routes to Magic Kingdom or Epcot. Or the vibrant streets of Miami where locals, international visitors, and seasonal “snowbirds” from colder climates all share the asphalt. This constant churn of drivers, many of whom are not accustomed to Florida’s specific traffic laws, driving styles, or congested urban areas, naturally leads to a higher propensity for accidents.

The sheer volume of vehicles on the road, particularly in popular tourist hubs and major metropolitan areas like Jacksonville, Tampa, and Fort Lauderdale, contributes to increased accident frequency. More cars on the road mean more opportunities for collisions, fender-benders, and other incidents that trigger insurance claims. When insurance companies observe a higher frequency of claims in a particular region, they adjust their rates upward to offset their increased risk exposure. This is a fundamental principle of insurance pricing: higher risk equates to higher premiums.

Moreover, the presence of many drivers who are unfamiliar with local roads or are simply distracted by vacation planning (or post-vacation relaxation) adds another layer of risk. Tourists often rely on GPS systems, which can sometimes lead to sudden lane changes or missed turns, further contributing to traffic unpredictability. For residents, this means their daily commute, whether to work or to enjoy local attractions, takes place in a consistently high-risk environment. This translates to higher personal car insurance costs, even for those with impeccable driving records. When planning accommodation, understanding the accessibility by car and the driving environment around popular resorts like Margaritaville Resort Orlando becomes important.

The Impact of Rental Vehicles and Uninsured Motorists

Florida’s thriving tourism sector, while a boon for the economy, also introduces a significant number of rental cars onto the roads. While rental car companies typically provide basic insurance, it’s often minimal, and many tourists opt for supplementary coverage, sometimes through their credit cards or independent travel insurance. However, the sheer volume of these vehicles, coupled with drivers who may be less cautious with a car that isn’t their own, can still contribute to higher accident rates.

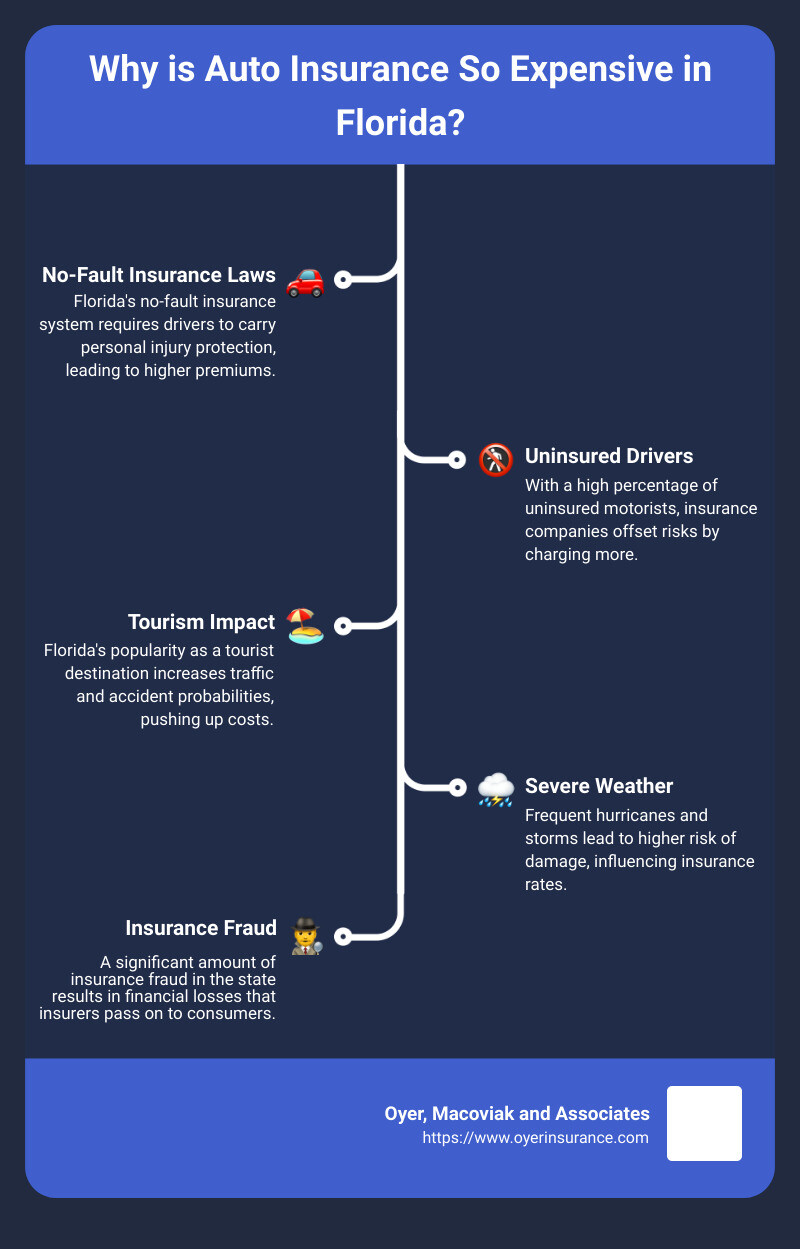

Beyond tourists, Florida unfortunately grapples with one of the highest rates of uninsured motorists in the United States. This is a substantial factor driving up costs for everyone else. When an insured driver is involved in an accident with an uninsured motorist, their own insurance company often has to bear the costs of repairs and medical bills, either through uninsured motorist coverage (which is highly recommended in Florida) or through collision and personal injury protection (PIP) coverage. To compensate for the financial burden imposed by uninsured drivers, insurance companies spread this risk across their policyholders by increasing premiums across the board. This collective burden is a direct result of a significant portion of the driving population opting out of required coverage, a risk that insurance companies must account for in their pricing models.

The Environmental and Legal Landscape: Hurricanes, Fraud, and No-Fault Laws

Beyond the human element, Florida’s natural environment and specific legal framework play colossal roles in shaping its car insurance landscape. From the ever-present threat of hurricanes to the complexities of its no-fault system and the unfortunate prevalence of fraud, these factors create a challenging environment for insurers, directly translating to higher costs for consumers.

Hurricane Alley: The Cost of Catastrophic Weather

Florida is famously situated in “Hurricane Alley,” making it highly susceptible to tropical storms and hurricanes. While homeowners insurance bears the brunt of most hurricane-related damage, car insurance is also significantly impacted. High winds can cause trees and debris to fall on vehicles, storm surges and heavy rainfall lead to widespread flooding, and post-storm conditions often result in accidents due to downed power lines, damaged roads, and debris.

Events like Hurricane Andrew in 1992, and more recent powerful storms affecting areas from Pensacola on the Gulf Coast to Daytona Beach on the Atlantic Coast, demonstrate the immense scale of vehicle damage that can occur. These catastrophic weather events lead to a surge in comprehensive and collision claims, forcing insurance companies to pay out billions. To prepare for and mitigate future losses from such predictable but devastating events, insurers factor the high risk of natural disasters into their premium calculations for all policyholders across the state. Even if your car is safely parked in a garage at a luxury resort like The Breakers Palm Beach, the overall state risk still contributes to your premium.

Flooding is a particularly insidious problem. While not all drivers opt for comprehensive coverage, which typically covers flood damage to vehicles, those who do rely heavily on it. Many parts of Florida, especially low-lying coastal areas and regions near large bodies of water like Lake Okeechobee, are prone to flooding even from typical rainstorms, let alone hurricanes. The extensive damage caused by water intrusion – to engines, electronics, and interiors – often renders vehicles total losses, leading to substantial payouts by insurance providers. The sheer frequency and intensity of these events make them a major actuarial consideration.

The No-Fault System and the Pervasiveness of Insurance Fraud

Florida operates under a “no-fault” car insurance system, meaning that after an accident, each driver’s own insurance company pays for their medical expenses and lost wages, regardless of who was at fault. This system is primarily driven by Personal Injury Protection (PIP) coverage, which is mandatory for all drivers. While designed to streamline claims and reduce litigation, the no-fault system has, paradoxically, contributed to higher costs.

The requirement for PIP coverage (currently $10,000 in medical benefits) means that even minor accidents can quickly exhaust this limit, leading to further claims under other parts of the policy or even lawsuits. This system, unfortunately, has also become a magnet for insurance fraud. Florida consistently ranks among the top states for fraudulent auto insurance claims. This includes staged accidents, exaggerated injury claims, and unethical medical billing practices by clinics and chiropractors who exploit the PIP system.

These fraudulent activities inflate the cost of claims for legitimate accidents, as insurers must allocate resources to investigate suspicious claims and often end up paying for services that were unnecessary or never rendered. The cost of combating fraud, coupled with the payouts on fraudulent claims, is ultimately passed on to honest policyholders through higher premiums. For a state that thrives on tourism, with visitors often renting cars to visit attractions like Kennedy Space Center Visitor Complex or the beaches of Sarasota, this underlying fraudulent activity adds a hidden cost to the entire driving ecosystem.

High Medical and Repair Costs

Beyond the legal structure, the actual costs associated with medical care and vehicle repairs in Florida are substantial. The state has a high cost of living in many areas, particularly in metropolitan centers like Miami-Dade County, Broward County, and Palm Beach County. This translates directly into higher labor costs for auto repair shops and higher charges for medical services.

Modern vehicles are also equipped with increasingly sophisticated technology, such as sensors, cameras, and complex electronic systems. Even a minor fender-bender can damage these components, leading to significantly higher repair bills than in the past. Replacing a bumper with integrated sensors is far more expensive than replacing a simple chrome bumper from decades ago. These advanced safety features, while beneficial, drive up the cost of collision claims. Similarly, medical treatments, rehabilitation, and even emergency services in Florida come with high price tags, especially in areas with a strong tourism infrastructure where services cater to a diverse and often international clientele. These elevated expenses are directly reflected in the payouts insurance companies make, which then influence future premium calculations.

The Ripple Effect on Florida Lifestyle and Travel

For both residents and visitors, the high cost of car insurance in Florida isn’t just a financial footnote; it’s a significant factor shaping lifestyle choices, travel planning, and the overall economic landscape. Understanding this ripple effect is crucial for anyone considering a move to the Sunshine State or simply planning their next Florida getaway.

Planning Your Florida Vacation: Rental Car Insurance Considerations

Tourists flock to Florida for its diverse attractions, from the thrilling rides at Busch Gardens Tampa Bay to the serene shores of Siesta Key Beach. Most rely on rental cars to explore, as public transportation options can be limited outside of major city centers. The cost of rental car insurance, whether purchased directly from the rental company, through an independent insurer, or via credit card benefits, is directly influenced by Florida’s overall high insurance risk profile.

Visitors often find themselves adding significant daily charges for rental car coverage, which can quickly inflate the total cost of a trip. This decision-making process can be complex: relying solely on personal auto insurance (if it extends to rentals) or credit card benefits might seem cost-effective, but understanding the limitations of such coverage in Florida’s unique no-fault system is vital. For example, if your personal policy doesn’t cover PIP in Florida, you could be exposed. Travel guides often advise travelers to budget for this additional expense, just as they would for theme park tickets or resort fees at hotels like Loews Portofino Bay Hotel. The implication is that even transient visitors are indirectly paying for the state’s high insurance costs.

Relocation Costs and Daily Commutes for Residents

For individuals and families considering a move to Florida, perhaps to a vibrant city like St. Petersburg or a family-friendly suburb of Orlando, the cost of car insurance is a critical budgeting factor. What might have been an affordable premium in another state can skyrocket upon moving to Florida, catching many new residents off guard. This significant increase impacts the overall cost of living and can influence housing decisions, especially for those considering commuting between different areas.

The daily commute for residents, whether for work or leisure activities like visiting Disney Springs or Universal CityWalk, is inherently more expensive due to these high premiums. It’s not just about gas prices; the cost of keeping a vehicle legally on the road is a substantial recurring expense. For families planning trips to Animal Kingdom or Hollywood Studios, or those exploring the natural wonders of Dry Tortugas National Park, the cumulative effect of high insurance premiums can limit disposable income for other experiences. This financial burden can particularly affect budget travelers or those seeking a more economical lifestyle, making meticulous financial planning essential.

Strategies for Navigating Florida’s High Insurance Costs

While the factors contributing to expensive car insurance in Florida are numerous and deeply entrenched, drivers are not entirely powerless. There are proactive steps both residents and long-term visitors can take to mitigate these costs and ensure they are getting the best possible value for their coverage.

Smart Driving and Policy Choices

The most direct way to keep insurance costs down is to maintain a clean driving record. Avoiding accidents and traffic violations, particularly in heavily congested areas like Tampa or Miami, directly impacts your premiums. Insurers reward safe drivers with lower rates. Additionally, choosing a vehicle that is less expensive to insure can make a significant difference. Cars with high safety ratings, lower repair costs, and less likelihood of theft (a problem in certain urban centers) often qualify for lower premiums.

When selecting coverage, it’s crucial to understand Florida’s specific requirements, especially the mandatory PIP. While basic liability and PIP are required, carefully consider additional coverages like Uninsured/Underinsured Motorist (UM/UIM) protection. Given the high rate of uninsured drivers in the state, UM/UIM can be an invaluable safeguard against significant out-of-pocket expenses if you’re hit by a driver without sufficient coverage. Adjusting deductibles can also impact premiums; a higher deductible means lower monthly payments but a larger out-of-pocket expense if you file a claim.

Exploring Discounts and Providers

Comparison shopping is paramount in Florida’s competitive insurance market. Rates can vary significantly between different providers for the exact same coverage. Obtain quotes from multiple insurance companies, including national carriers and regional specialists, to find the most competitive pricing. Don’t be afraid to leverage independent insurance agents who can shop around on your behalf.

Furthermore, inquire about all available discounts. Common discounts include:

- Multi-policy discounts: Bundling car insurance with homeowners, renters, or even travel insurance (if offered by the same provider).

- Good driver discounts: For drivers with a clean record over a specified period.

- Safe driver programs: Telematics programs that monitor driving habits via an app or device.

- Good student discounts: For younger drivers who maintain good academic standing.

- Vehicle safety feature discounts: For cars equipped with advanced safety features like anti-lock brakes, airbags, and anti-theft systems.

- Defensive driving course discounts: Completing an approved defensive driving course can sometimes lead to a reduction in premiums.

- Senior discounts: Some companies offer discounts for older drivers, particularly those who take refresher courses.

- Payment method discounts: For paying premiums in full or signing up for automatic payments.

Even small discounts can add up, making a noticeable difference in your overall cost. If you’re staying at a reputable hotel like Ritz-Carlton Sarasota or Kimpton Epic Hotel and need rental insurance, check if your existing provider offers specific vacation or temporary coverage options that align with these discounts.

In conclusion, the high cost of car insurance in Florida is a complex issue driven by a unique convergence of factors: a dense and transient population, the ever-present threat of natural disasters, a challenging legal framework ripe for fraud, and the generally high cost of medical and auto repairs. While these elements contribute to an expensive driving environment, both residents and visitors can navigate these costs effectively by understanding the underlying causes and actively seeking out smart coverage options and available discounts. By doing so, you can ensure that your journey through the Sunshine State remains as enjoyable and financially manageable as possible, allowing you to focus on the unforgettable travel, tourism, and lifestyle experiences that Florida so generously offers.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.