California has long been synonymous with sunshine, innovation, and an unparalleled lifestyle. From the pristine beaches of Southern California to the majestic redwoods of the north, and from the vibrant urban centers like Los Angeles and San Francisco to the serene vineyards of Napa Valley, the Golden State offers a diverse tapestry of experiences that draw millions of visitors and residents alike. Many dream of retiring in this idyllic setting, picturing leisurely days exploring Yosemite National Park, strolling along the Santa Barbara coastline, or enjoying the cultural richness of San Diego. However, before packing your bags and booking that long-term stay in a luxury resort overlooking the Pacific, a crucial question often arises for those planning their finances: Does California tax pensions?

The answer, like much of California’s appeal, is nuanced and requires a deeper dive into the state’s tax policies. While the allure of the climate, the vibrant culture, and world-class attractions from Disneyland to the Golden Gate Bridge are undeniable, understanding the financial implications, especially for retirees, is paramount for a smooth transition and a comfortable lifestyle. This guide will clarify California’s stance on taxing retirement income, explore other pertinent taxes, and provide a broader perspective on financial planning for those considering making the Golden State their home, whether for a temporary escape or a permanent relocation.

Unpacking California’s Retirement Income Tax Policies

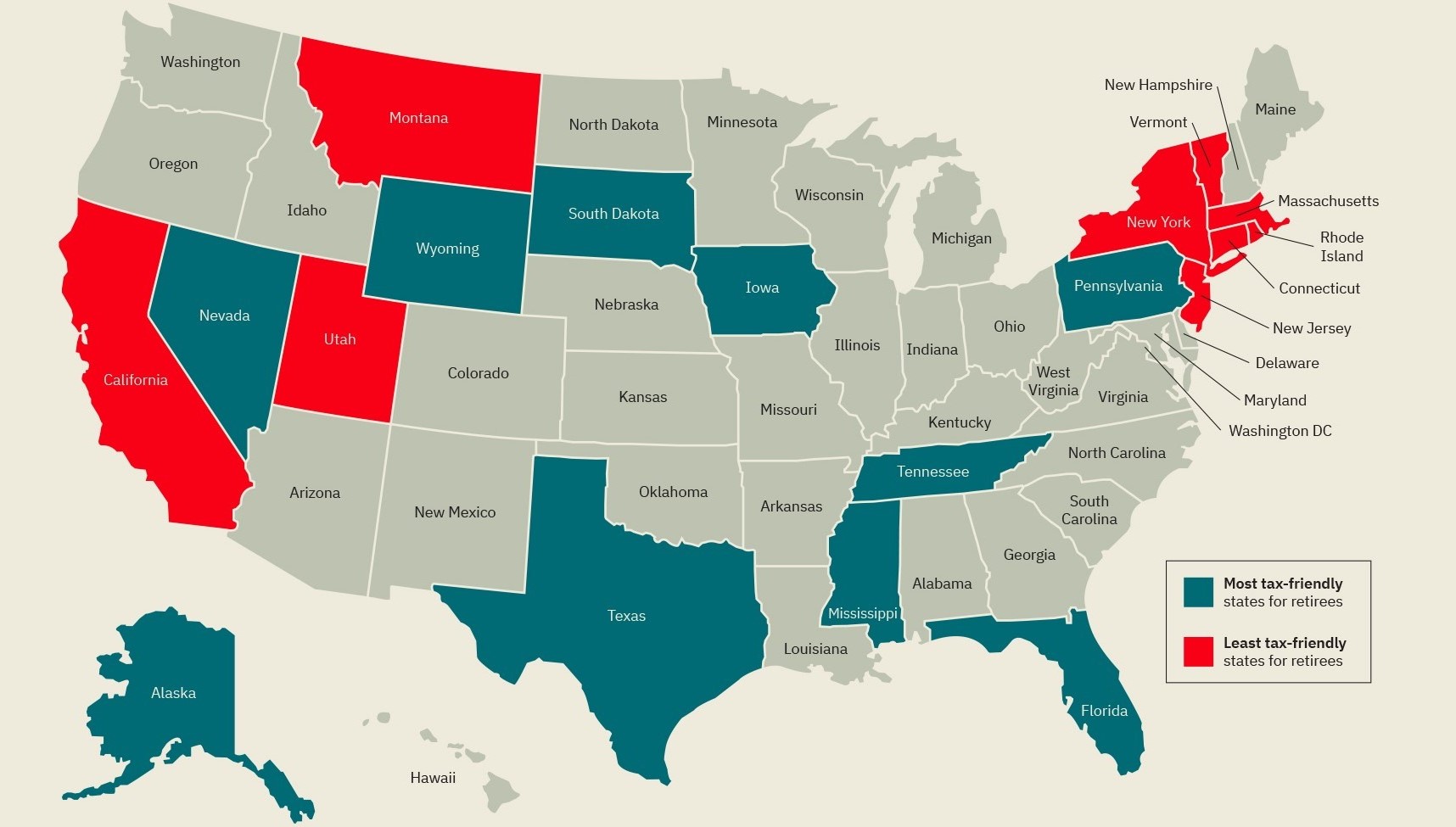

When considering retirement destinations, tax burdens are often a significant factor. Some states are known for being particularly tax-friendly for retirees, often exempting various forms of retirement income. California, however, operates under a different philosophy regarding much of that income.

The General Rule: Pensions and Distributions Are Taxable

Unlike a number of states that offer broad exemptions for retirement income, California generally does not exempt most types of retirement income from state income tax. This is a critical point for anyone receiving regular pension payments or drawing from retirement accounts. This broad taxation applies to a wide array of income sources that many retirees depend on:

- Private Employer Pensions: If you receive a pension from a private company or organization, these payments are typically subject to California state income tax.

- State and Local Government Pensions: Pensions from non-California state and local government employers are also generally taxable. For pensions received from the California Public Employees’ Retirement System (CalPERS) or the California State Teachers’ Retirement System (CalSTRS), these benefits are also included in taxable income for state purposes.

- 401(k) and IRA Distributions: Income distributed from traditional 401(k)s, 403(b)s, and Individual Retirement Accounts (IRAs) is subject to California income tax, just as it would be for federal income tax purposes. This means that as you withdraw funds from these accounts in retirement, those withdrawals will be added to your taxable income.

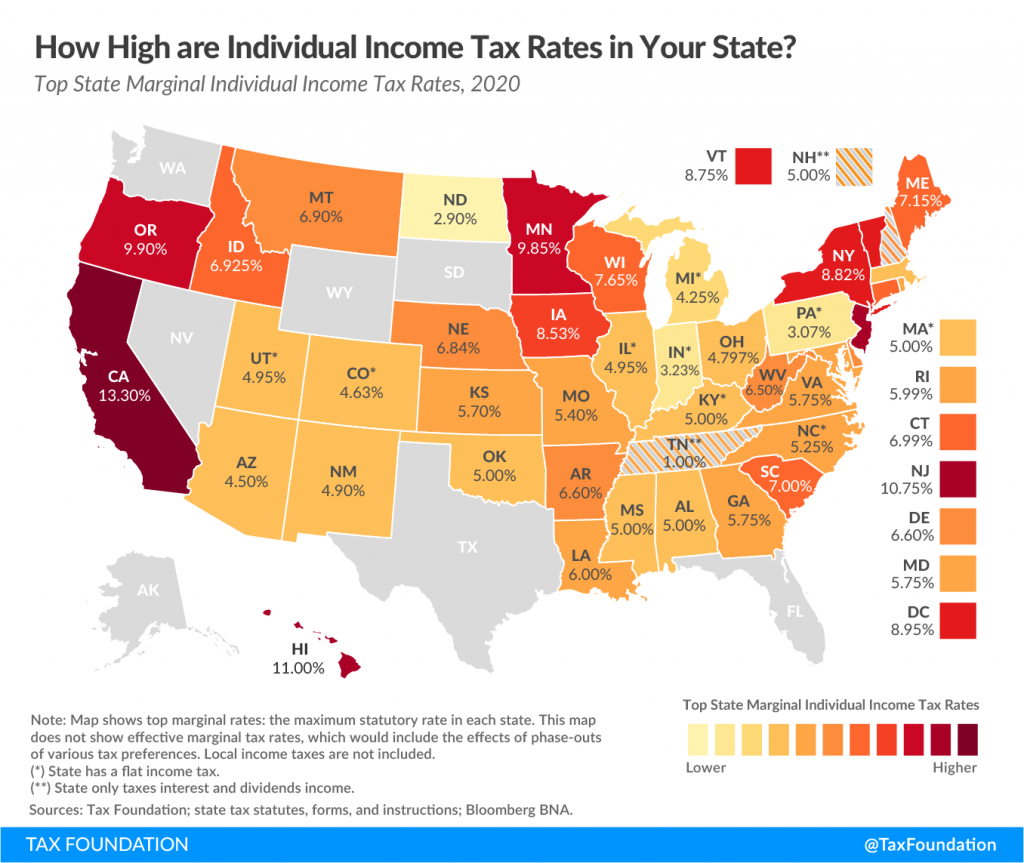

California’s income tax system is progressive. This means that the more income you earn, the higher percentage you pay in state income tax. Rates in California are among the highest in the nation, ranging from 1% to 12.3%. For very high earners, specifically those with incomes over $1 million, an additional 1% mental health services tax applies. This progressive structure means that those with substantial pension income or large withdrawals from retirement accounts could find themselves in higher tax brackets, impacting their overall retirement budget.

For individuals exploring accommodation options, whether it’s a villa in Palm Springs for a long-term winter stay or a quaint apartment in Carmel-by-the-Sea, understanding how your pension income is taxed is crucial for budgeting. A higher tax liability might influence the type of accommodation you can afford or the frequency of your travels to California’s many enticing destinations.

Key Exemptions: Social Security and Railroad Retirement Benefits

While California broadly taxes many forms of retirement income, there are two significant and welcome exceptions that provide some relief for retirees:

- Social Security Benefits: A major advantage for retirees in California is that Social Security benefits are entirely exempt from state income tax. This means that no matter your income level or the amount of Social Security you receive, California will not levy a state income tax on those specific funds. This exemption can be a considerable financial cushion, especially for those whose Social Security represents a significant portion of their retirement income.

- Railroad Retirement Benefits: Similar to Social Security benefits, income received from the Railroad Retirement system is also exempt from California state income tax. This provides a similar advantage for retirees who have qualified for and receive these specific benefits.

These exemptions are important considerations when planning your retirement budget in California. For those heavily reliant on Social Security or Railroad Retirement, the effective state tax burden on their overall retirement income might be significantly lower than someone primarily drawing from private pensions or large IRA accounts. This distinction underscores the importance of a personalized financial assessment before committing to a California retirement, whether it involves settling down in Sacramento or enjoying the vibrant lifestyle of Monterey.

Beyond Retirement Income: Other Taxes Affecting California Living

While income tax on pensions is a primary concern, a holistic view of California’s tax environment requires an examination of other significant levies. These taxes can greatly influence the overall cost of living and, consequently, your travel and accommodation choices within the state.

Navigating California’s Property Tax Landscape

For anyone considering purchasing a home, whether a primary residence or a vacation property for occasional visits, understanding California’s property tax system is essential. Property taxes are based on the assessed value of the property, and while the state boasts some of the highest home values in the nation, its unique system, primarily governed by Proposition 13, offers some protections.

- Proposition 13’s Impact: Enacted in 1978, Proposition 13 limits the base property tax rate to 1% of the property’s assessed value. Crucially, it also caps the annual increase in assessed value to a maximum of 2% per year, unless there is a change of ownership. This means that property owners who have owned their homes for many years often pay significantly less in property taxes than those who have recently purchased comparable properties, due to their lower assessed value.

- Local Add-ons: Beyond the 1% base rate, property tax bills include additional levies for local bonded indebtedness (for schools, infrastructure projects, etc.) and special assessments (e.g., for specific local services). These add-ons can vary significantly by county and city, meaning property tax rates can range from roughly 1.1% to 1.5% or more of the assessed value, depending on the specific location within California.

The impact of property taxes on living in California cannot be overstated. High property values, particularly in desirable areas like Malibu or near landmarks such as Hollywood, translate to substantial property tax bills, even with Proposition 13’s protections for long-term owners. For new buyers, particularly those moving from out of state, the annual property tax payment can be a significant budget item, rivaling or even exceeding other monthly expenses. This could influence decisions on whether to rent an apartment, buy a modest home, or invest in a more expansive property suitable for hosting family visits and exploring local tourism.

Understanding Sales Tax: What You’ll Pay for Goods

Sales tax is another everyday expense that can add up over time. California has one of the highest statewide sales tax rates in the United States.

- Statewide Rate: The base statewide sales tax rate is 7.25%.

- Local Additions: On top of the statewide rate, local jurisdictions (cities and counties) can impose additional sales taxes. This means that the combined sales tax rate can climb considerably, reaching up to 10.75% in some areas. For instance, dining out at a restaurant in San Francisco or shopping for souvenirs in Santa Monica could incur a higher sales tax rate than purchasing items in a less densely populated region.

This tax applies to most tangible goods purchased, from groceries (excluding certain staple food items) to clothing, electronics, and even vehicle purchases. It generally does not apply to services, which is a common distinction in sales tax laws. For visitors or new residents, the cumulative effect of these sales taxes on daily purchases, especially when furnishing a new home or indulging in local shopping experiences, is an important financial consideration. It impacts the perceived value of everything from a stay at a boutique hotel in Laguna Beach (through the cost of goods purchased during the trip) to the overall budget for exploring California’s diverse attractions.

Estate Tax: A State-Level Relief

For those concerned about wealth transfer, California offers a notable advantage:

- No State-Level Estate or Inheritance Tax: California does not levy a state-level estate tax or an inheritance tax. This is a significant relief for individuals planning their legacy, as it means that their heirs will not face an additional state tax burden on inherited assets beyond what might be applicable at the federal level.

While federal estate tax rules still apply to very large estates, the absence of a state-specific estate or inheritance tax is a positive aspect for residents of California. This factor can influence decisions regarding where to establish a permanent residence, particularly for individuals with substantial assets, as it ensures that more of their wealth can be passed on to their beneficiaries without state intervention.

Financial Planning and Lifestyle in the Golden State

Considering the diverse tax landscape, prospective retirees and residents must carefully weigh the financial implications against the myriad lifestyle benefits that California offers. It’s a state that promises unparalleled experiences, from the cultural vibrancy of Hollywood and Griffith Observatory to the natural beauty of Big Sur and Lake Tahoe.

Weighing the Cost of Living Against California’s Allure

The cost of living in California is notoriously high, significantly influenced by housing costs, but also by the various taxes discussed. For retirees, this means that their pension and retirement income, even if substantial, might not stretch as far as it would in other states.

- Housing and Accommodation: Whether you’re looking for a short-term apartment rental in San Diego or dreaming of a permanent home in Palo Alto, housing costs will likely be your largest expense. High property values translate into high rents and high purchase prices. This reality impacts everything from the size of the home you can afford to the neighborhoods you might consider. For travelers, this means budgeting carefully for hotel stays or exploring alternative accommodation options like vacation rentals or more budget-friendly hotels in less central locations.

- Everyday Expenses: Beyond housing, the higher sales tax, alongside generally higher prices for goods and services in many parts of the state, contributes to a higher overall cost of living. Even simple pleasures like dining out in Sausalito or enjoying local attractions can carry a higher price tag.

- The Lifestyle Factor: Despite the financial considerations, millions choose California for its unparalleled lifestyle. The diverse geography allows for skiing in the morning and surfing in the afternoon. The state is a hub for arts, culture, and culinary excellence. It offers endless opportunities for exploration, from historic landmarks like Alcatraz Island to scenic drives along Highway 1. For many, these lifestyle benefits and experiences outweigh the higher costs and tax burdens. The ability to travel easily to world-class destinations, enjoy year-round outdoor activities, and immerse oneself in rich cultural experiences defines the lifestyle that attracts so many to the Golden State.

Making Informed Decisions for Your California Dream

Ultimately, deciding whether California is the right place for your retirement or long-term stay involves a careful balance of financial realities and lifestyle aspirations.

- Personalized Financial Assessment: Given the complexity of California’s tax system, especially concerning retirement income, a crucial step is to consult with a qualified tax professional or financial advisor who specializes in California tax law. They can provide personalized advice based on your specific income sources, assets, and financial goals. This expert guidance can help you understand your potential tax liability and strategize ways to mitigate it within legal means.

- Budgeting for the Golden State: Create a detailed budget that accounts for all potential expenses, including income taxes on your pensions and retirement distributions, property taxes, sales tax on purchases, and the generally higher cost of living. Factor in your desired lifestyle, whether it involves frequent luxury travel, dining at acclaimed restaurants, or simply enjoying the natural beauty of the state.

- Exploring Different Regions: California is a vast state, and the cost of living and specific tax rates (like local sales tax and property tax add-ons) can vary significantly from one region to another. Areas like San Luis Obispo or the Central Valley might offer a more budget-friendly lifestyle compared to the major metropolitan areas. Researching various cities and counties to find a location that aligns with both your financial plan and your lifestyle preferences is highly recommended.

In conclusion, while California generally taxes most pension income and retirement account distributions, it does offer significant exemptions for Social Security and Railroad Retirement benefits, and boasts no state-level estate tax. The high cost of living, driven by housing and sales tax, is a trade-off for the state’s unparalleled beauty, vibrant culture, and endless opportunities for travel and adventure. With careful planning and professional advice, your dream of a California retirement can certainly become a reality, allowing you to fully embrace the lifestyle of the Golden State.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.