For many, the mention of “taxes” conjures images of complex spreadsheets and dreaded annual filings. However, understanding specific tax structures, particularly capital gains tax in a vibrant state like California, is more than just a fiscal obligation; it’s a critical component of strategic financial planning. Whether you’re a seasoned investor, a prospective homeowner, or someone dreaming of funding their next grand adventure with smart asset management, comprehending capital gains tax is essential. For those deeply engaged with the world of travel, luxury accommodation, and lifestyle investments — the very heart of what Life Out of the Box champions — these tax implications can directly influence decisions about buying a vacation home, investing in a hotel development, or simply budgeting for your next global escapade.

California, often referred to as the Golden State, is renowned for its diverse economy, breathtaking landscapes, and an unparalleled lifestyle that attracts people from across the globe. From the sun-drenched beaches of San Diego to the tech hubs of Silicon Valley and the artistic allure of Los Angeles, it’s a state of immense opportunity. This very vibrancy, however, often comes with a higher cost of living and, consequently, a unique tax environment. Capital gains tax is a significant part of this landscape, impacting anyone who sells an asset for more than its purchase price. This article will demystify capital gains tax in California, exploring its nuances, its impact on your financial and travel goals, and strategies to navigate it effectively, all while keeping your wanderlust in mind.

Understanding Capital Gains: A Traveler’s Perspective on Investment

Before diving into the specifics of California’s tax rates, it’s crucial to grasp the fundamental concept of capital gains. From the perspective of a traveler or lifestyle enthusiast, your assets aren’t just figures on a balance sheet; they represent potential. They could be the equity in a charming bed-and-breakfast you owned in Napa Valley, the shares you held in a burgeoning boutique hotel chain like Standard Hotels, or even a beloved vacation property in Palm Springs. When you sell these assets for a profit, that profit is generally considered a capital gain, and it’s subject to taxation.

What Exactly Are Capital Gains?

At its core, a capital gain is the profit you make from selling a capital asset. Capital assets encompass a wide range of items, including:

- Real Estate: This is perhaps the most common and impactful for travelers and those interested in accommodation. This includes your primary residence, vacation homes, rental properties, or commercial real estate like a storefront in San Francisco or a resort in Lake Tahoe.

- Stocks and Bonds: Investments in publicly traded companies, mutual funds, and other financial instruments. Imagine selling shares of Marriott International after they’ve significantly appreciated.

- Collectibles: Art, antiques, precious metals, and other valuable items.

- Certain Business Assets: Depending on their nature and how they’re used.

The calculation is straightforward: Selling Price – Original Purchase Price – Selling Expenses (like realtor fees or renovation costs that add to the property’s basis) = Capital Gain (or Loss). For instance, if you bought a condo in Santa Monica for $800,000, invested $50,000 in renovations, and then sold it for $1,000,000, your capital gain would be $150,000. This gain then becomes part of your taxable income.

Short-Term vs. Long-Term Gains: The Time Horizon of Your Investments

The duration for which you hold an asset before selling it is a critical factor in determining how your capital gains will be taxed, both at the federal and state levels. This distinction is paramount for strategic investors, especially those eyeing properties or ventures with varying time horizons.

- Short-Term Capital Gains: These are profits from assets held for one year or less. From a tax perspective, short-term capital gains are treated just like ordinary income. This means they are taxed at your regular income tax rate, which can be significantly higher, especially for high-income earners in California. For someone looking to “flip” a property quickly or make rapid trades in hospitality stocks, understanding this immediate impact is vital.

- Long-Term Capital Gains: These are profits from assets held for more than one year. Long-term capital gains generally enjoy preferential tax treatment, meaning they are taxed at lower rates than ordinary income. This encourages long-term investment and stability, a common strategy for those building wealth through real estate, retirement accounts, or substantial stakes in tourism-related businesses.

For many seeking financial independence to fuel a lifestyle of travel and exploration, cultivating long-term capital gains is often the more tax-efficient path. Whether it’s patiently waiting for a luxury villa in Malibu to appreciate or holding onto shares of a robust airline like United Airlines, the long-term approach often yields greater after-tax profits, leaving more funds for booking that dream suite at the Four Seasons Resort Hualalai or exploring the ancient wonders of Rome.

Navigating California’s Capital Gains Tax Landscape

California stands out with its robust economy and unique tax policies. For capital gains, understanding the interplay between federal and state taxes is crucial, as both levy their own claims on your profits. This dual taxation system requires careful consideration, especially for those who manage significant asset portfolios or invest in high-value properties within the state.

The Golden State’s Unique Tax Structure

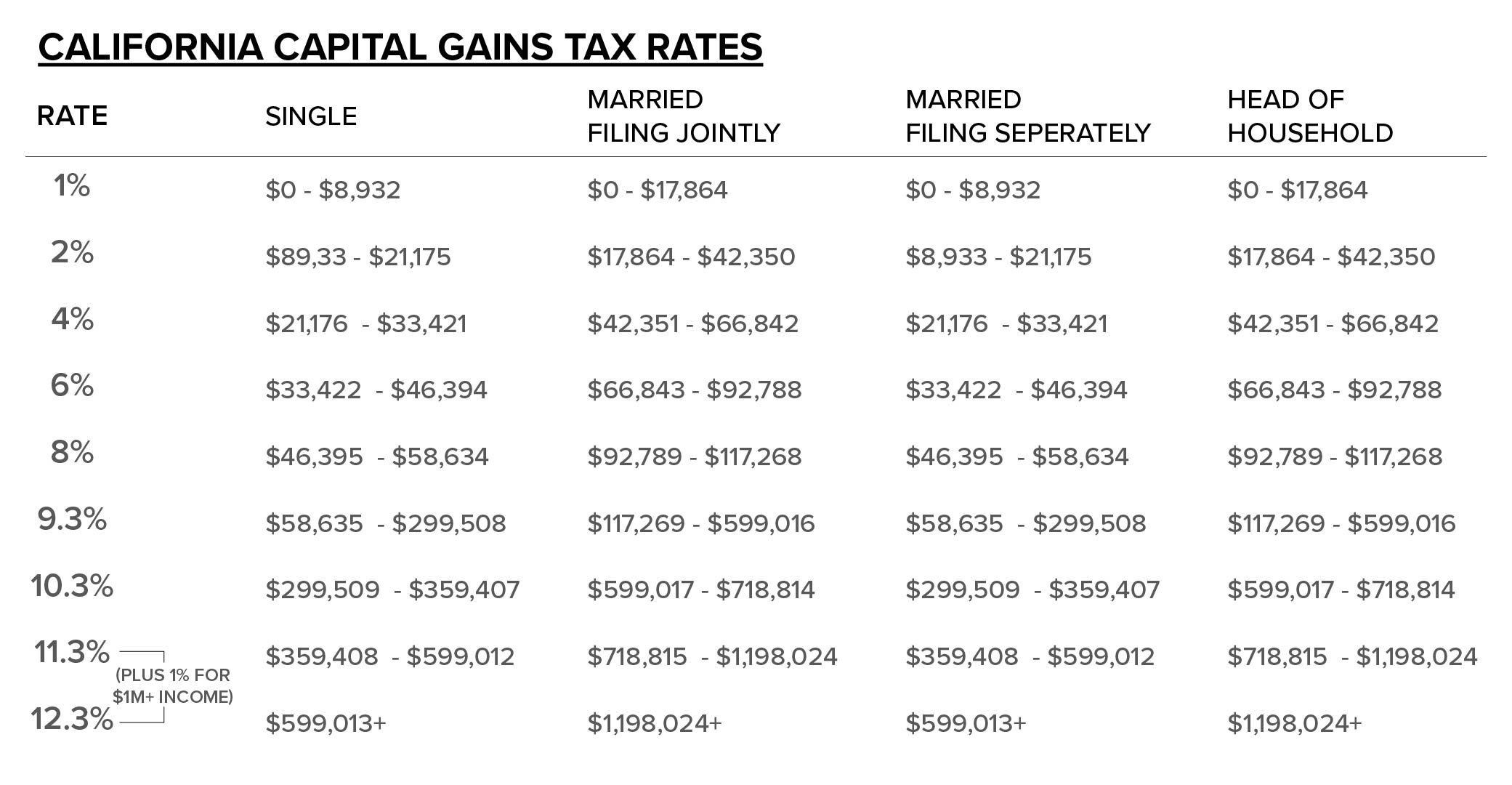

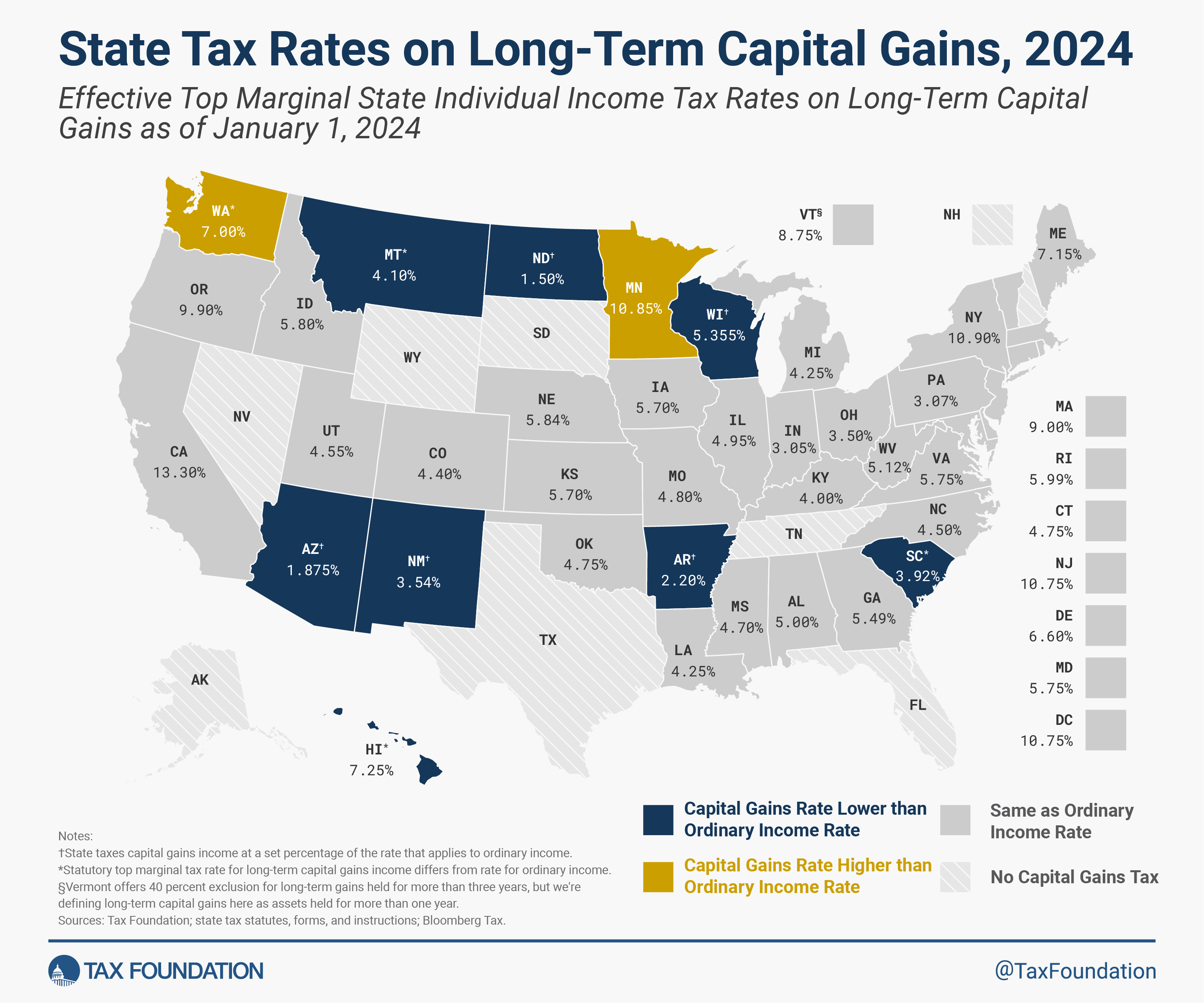

One of the most important things to understand about capital gains tax in California is that there is no separate, fixed capital gains tax rate at the state level. Instead, capital gains are treated as ordinary income and are added to your other income (wages, business profits, etc.). This means they are subject to California’s progressive income tax rates, which can be among the highest in the United States.

California’s marginal income tax rates can range from 1% to 12.3% for most taxpayers, with an additional 1% surcharge for high-income earners (those with taxable income over $1 million), bringing the top marginal rate to 13.3%. This means that if you’re in the highest income bracket in California and realize a significant capital gain, a substantial portion of that gain could be owed to the state.

For instance, if you sell an investment property in San Jose for a $500,000 long-term capital gain, and your total income for the year (including this gain) places you in the 12.3% bracket, you would owe approximately $61,500 to California on just that capital gain, in addition to your federal obligations. This emphasizes why careful planning is not just advisable but essential for residents and investors in the state. This can significantly impact the net proceeds available for your next travel adventure or investment in a luxury accommodation in Mexico.

Federal Implications: A Dual Responsibility

While California’s rates are significant, you also have to consider federal capital gains tax. The United States federal government has separate capital gains tax rates, which do differentiate between short-term and long-term gains.

- Federal Short-Term Capital Gains: As mentioned, these are taxed at your ordinary federal income tax rates, which can range from 10% to 37%.

- Federal Long-Term Capital Gains: These benefit from preferential rates, typically 0%, 15%, or 20%, depending on your overall taxable income. Most taxpayers fall into the 15% bracket, while high-income earners face the 20% rate.

- Net Investment Income Tax (NIIT): For higher-income individuals, an additional 3.8% Net Investment Income Tax may apply to certain investment income, including capital gains. This means a top federal long-term capital gains rate could effectively be 23.8% (20% + 3.8%).

Combining federal and state taxes, the total capital gains tax burden for a high-income earner in California can be substantial. For example, if you’re in the highest federal (20% + 3.8% NIIT) and California (13.3%) brackets, your combined top marginal rate on long-term capital gains could approach 37.1% (23.8% + 13.3%). This joint obligation underscores the importance of strategic tax planning and potentially seeking advice from a qualified financial professional to optimize your asset sales, whether they fund your retirement or your dream vacation to Paris.

Capital Gains and Your Travel & Accommodation Investments

For those with a passion for travel and an eye for lucrative investments in the hospitality sector, capital gains tax isn’t just an abstract concept; it’s a very real factor influencing purchasing, selling, and portfolio management decisions. How you navigate these taxes can significantly impact the funds available for exploring new destinations, staying in luxurious resorts, or even investing in your next travel-related venture.

Selling Your Vacation Home or Investment Property

Many travelers dream of owning a slice of paradise—a charming villa in Tuscany, a beachfront condo in Maui, or a cozy cabin near Yosemite National Park. In California, investing in second homes or rental properties is a popular way to generate income and build wealth. However, when it comes time to sell these properties, capital gains tax becomes a central consideration.

Unlike a primary residence, which may qualify for significant capital gains exclusion ($250,000 for single filers, $500,000 for married filing jointly, if you’ve lived there for at least two out of the last five years), vacation homes and investment properties do not typically benefit from this exclusion. This means that the full amount of your capital gain (after subtracting your basis and selling expenses) will be subject to both federal and California capital gains taxes.

Consider an investor who purchased a vacation rental in Big Sur a decade ago for $1 million, spending $100,000 on upgrades and renovations, and now sells it for $2 million. Their capital gain would be $900,000. This substantial gain would be fully taxed, potentially reducing their net profit by hundreds of thousands of dollars. Understanding this upfront can help you set realistic profit expectations and plan your next move, whether it’s buying another property or funding a sabbatical year abroad.

Investing in Hospitality: Hotels, Resorts, and Tourism Ventures

Beyond personal property, capital gains tax also impacts investments in the broader hospitality and tourism industry. This could include:

- Shares in publicly traded hotel companies: Brands like Hilton Hotels & Resorts or Hyatt Hotels are common investment vehicles. Selling these shares for a profit, especially after long-term holding, will incur capital gains.

- Direct investment in boutique hotels or resorts: Participating in a syndication or partnership that owns a unique property, perhaps a luxury resort in Cabo San Lucas or a glamping site near Joshua Tree National Park. When these assets are sold, or your stake is bought out, capital gains will apply.

- Tourism-related businesses: This might involve owning a stake in an experiential travel company, a local tour operator in San Luis Obispo, or a digital platform connecting travelers with unique accommodations.

For these types of investments, the principles of short-term vs. long-term gains apply. Savvy investors often prioritize long-term holdings to benefit from the lower federal capital gains rates. This strategic patience can yield significantly more capital to reinvest in the industry, expand a portfolio of unique stays, or simply provide a more robust travel fund for future explorations to places like Tokyo or London.

Planning Your Next Adventure: How Tax Savings Can Fund Your Lifestyle

Ultimately, for many readers of Life Out of the Box, financial planning isn’t just about accumulating wealth; it’s about leveraging that wealth to create a desired lifestyle, often centered around travel, unique experiences, and comfortable accommodations. Understanding and minimizing your capital gains tax burden directly translates into more disposable income for these pursuits.

Imagine selling an asset with a $100,000 capital gain. If you haven’t planned effectively, a combined federal and California tax rate of, say, 35% means $35,000 goes to taxes. That’s a substantial sum that could have funded:

- A two-week luxury cruise through the Mediterranean Sea.

- A year of monthly weekend getaways to charming California wine country hotels.

- A significant portion of a down payment on a new fractional ownership property in a sought-after destination like Aspen.

- An extended stay at a Ritz-Carlton property while exploring a new city.

By strategically planning your asset sales, utilizing available deductions and deferrals, and understanding the timing of your gains, you can optimize your after-tax profit. This not only bolsters your investment portfolio but also directly enhances your ability to indulge in the travel and lifestyle experiences you cherish, making the world more accessible and your adventures more luxurious.

Strategies to Minimize Your Capital Gains Tax Burden

Given the significant impact capital gains tax can have, especially in California, employing strategic tax planning is paramount. Smart approaches can help you retain more of your hard-earned profits, allowing you to reinvest, save, or spend more on your passion for travel and unique accommodations.

Leveraging Tax-Advantaged Accounts and Deductions

One of the foundational strategies involves utilizing accounts designed to offer tax benefits:

- Retirement Accounts (IRAs, 401(k)s): Investments held within tax-advantaged retirement accounts grow tax-deferred or, in the case of Roth accounts, tax-free. When you sell assets within these accounts, you generally don’t pay capital gains tax until withdrawal (for traditional accounts) or not at all (for Roth accounts, assuming qualified withdrawals). This is an excellent way to grow your wealth for future travel during retirement, knowing the gains aren’t immediately eroded by taxes.

- Tax-Loss Harvesting: If you have investments that have declined in value (capital losses), you can sell them to offset capital gains. If your losses exceed your gains, you can deduct up to $3,000 of the net loss against your ordinary income each year, carrying forward any remaining losses to future years. This is a powerful tool to reduce your overall taxable income and, by extension, your capital gains liability. Imagine using losses from a less-than-stellar stock investment to offset gains from a profitable sale of shares in a successful hotel chain like MGM Resorts International.

- Qualified Opportunity Funds (QOFs): These funds allow investors to defer or even reduce capital gains taxes by reinvesting those gains into designated “Opportunity Zones”—economically distressed communities. While not suitable for everyone, investing in a QOF could potentially provide significant tax benefits while supporting development in areas that might also benefit from tourism growth, perhaps a nascent tourism district in Oakland or Fresno.

The 1031 Exchange: A Game Changer for Real Estate Investors

For those deeply invested in real estate, particularly income-producing properties like vacation rentals, commercial buildings, or hotels, the 1031 Exchange (also known as a like-kind exchange) is an incredibly powerful tool. This provision of the tax code allows investors to defer capital gains taxes when they sell one investment property and reinvest the proceeds into another “like-kind” property within specific timelines.

Here’s how it works: Instead of recognizing a capital gain when you sell a property, you can defer the tax by purchasing another qualifying property. This means you can keep more of your money working for you, growing your real estate portfolio faster without the immediate tax hit. For a real estate enthusiast looking to upgrade from a small rental property in Sacramento to a larger boutique hotel development near Pebble Beach, a 1031 Exchange can be transformative, allowing them to funnel all their equity into the new venture.

There are strict rules and timelines for 1031 Exchanges, including identifying replacement properties within 45 days of selling the original and closing on the new property within 180 days. Working with a qualified intermediary is essential to ensure compliance. This strategy is particularly appealing for those who view real estate as a primary means of building wealth for a travel-rich lifestyle, enabling continuous reinvestment and compounding returns.

Opportunity Zones: Investing in Community and Enjoying Tax Benefits

As mentioned briefly, Opportunity Zones, established by the Tax Cuts and Jobs Act of 2017, offer another unique avenue for capital gains deferral and potential reduction. By investing capital gains into a Qualified Opportunity Fund (QOF) that then invests in businesses or properties located within designated Opportunity Zones, investors can:

- Defer Capital Gains: The original capital gains invested into a QOF can be deferred until the earlier of the date on which the investment in the QOF is sold or exchanged, or December 31, 2026.

- Reduce Capital Gains: If the investment in the QOF is held for at least five years, the basis of the original capital gain is increased by 10%. If held for seven years, it increases by another 5% (total 15%).

- Eliminate Capital Gains on QOF Investment: If the investment in the QOF is held for at least 10 years, any capital gains from the appreciation of the QOF investment itself are tax-free.

For a traveler with an investment mindset, this could mean investing in a new hotel construction in a revitalized urban area of San Bernardino, a new experiential tourism business in a rural California county, or a mixed-use development that includes short-term rental units. Beyond the financial benefits, this strategy offers the potential to contribute to community development, aligning investment with social impact, all while managing your tax liability.

Conclusion: Making Informed Decisions for Your Financial Journey and Wanderlust

Understanding “How Much Is Capital Gains Tax In California?” extends far beyond merely calculating a percentage. It’s about recognizing the intricate connections between your financial decisions, your investment portfolio, and your aspirational lifestyle. For those who curate their lives around travel, unique accommodations, and enriching experiences, every dollar saved on taxes is a dollar liberated to explore a new destination, upgrade to a dream suite, or invest in another venture that fuels their passion.

California’s unique tax structure, combining federal capital gains rates with its own progressive income tax on these gains, presents both challenges and opportunities. Whether you’re selling a cherished vacation home, cashing out on a savvy stock investment in the hospitality sector, or strategically leveraging real estate through a 1031 Exchange, the timing and method of your asset sales can have profound implications for your net worth and your ability to fund future adventures.

By delving into the distinctions between short-term and long-term gains, understanding the dual tax burden of federal and state rates, and exploring powerful mitigation strategies like tax-advantaged accounts, tax-loss harvesting, 1031 Exchanges, and Opportunity Zone investments, you empower yourself to make more informed and financially savvy decisions.

The journey of life is a grand adventure, and your financial journey should be no different. By mastering the nuances of capital gains tax in California, you’re not just optimizing your tax returns; you’re actively shaping the resources available for your next luxurious escape to the Maldives, your investment in a charming boutique hotel in Charleston, or simply the freedom to live life fully, out of the box, and across the globe. Plan wisely, invest strategically, and let your financial savvy pave the way for unparalleled travel experiences.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.