California, a state renowned for its breathtaking landscapes, from the iconic Golden Gate Bridge in San Francisco to the sun-drenched beaches of Southern California, also faces a significant and growing threat: wildfires. The increasing frequency and intensity of these blazes have made fire insurance not just a recommendation, but a critical necessity for homeowners and businesses across the Golden State. Understanding the costs associated with this vital protection is paramount for residents. This article delves into the factors influencing fire insurance premiums in California, what it typically covers, and strategies for managing these expenses.

Understanding the Factors Driving Fire Insurance Costs

The price of fire insurance in California is not a one-size-fits-all figure. It’s a complex calculation influenced by a multitude of variables, many of which are unique to the state’s geography and climate. Insurers meticulously assess risk, and certain characteristics of a property and its surroundings will significantly impact the premium.

Property-Specific Risk Factors

The most direct influence on your fire insurance premium is the nature of the property itself. The age and construction materials of your home play a crucial role. Older homes, particularly those built with less fire-resistant materials like wood shake roofs or traditional siding, are generally considered higher risk and thus command higher premiums. Newer construction incorporating fire-retardant materials and modern building codes can often lead to lower rates. The presence of features like defensible space – cleared vegetation around a home – is a significant positive factor. Conversely, properties located in densely wooded areas or those with steep slopes, which can exacerbate fire spread, will likely see increased insurance costs. The value of your home, including its replacement cost, also directly affects the premium, as a higher replacement value means a larger potential payout for the insurer in the event of a total loss.

Geographic Location and Wildfire Risk Zones

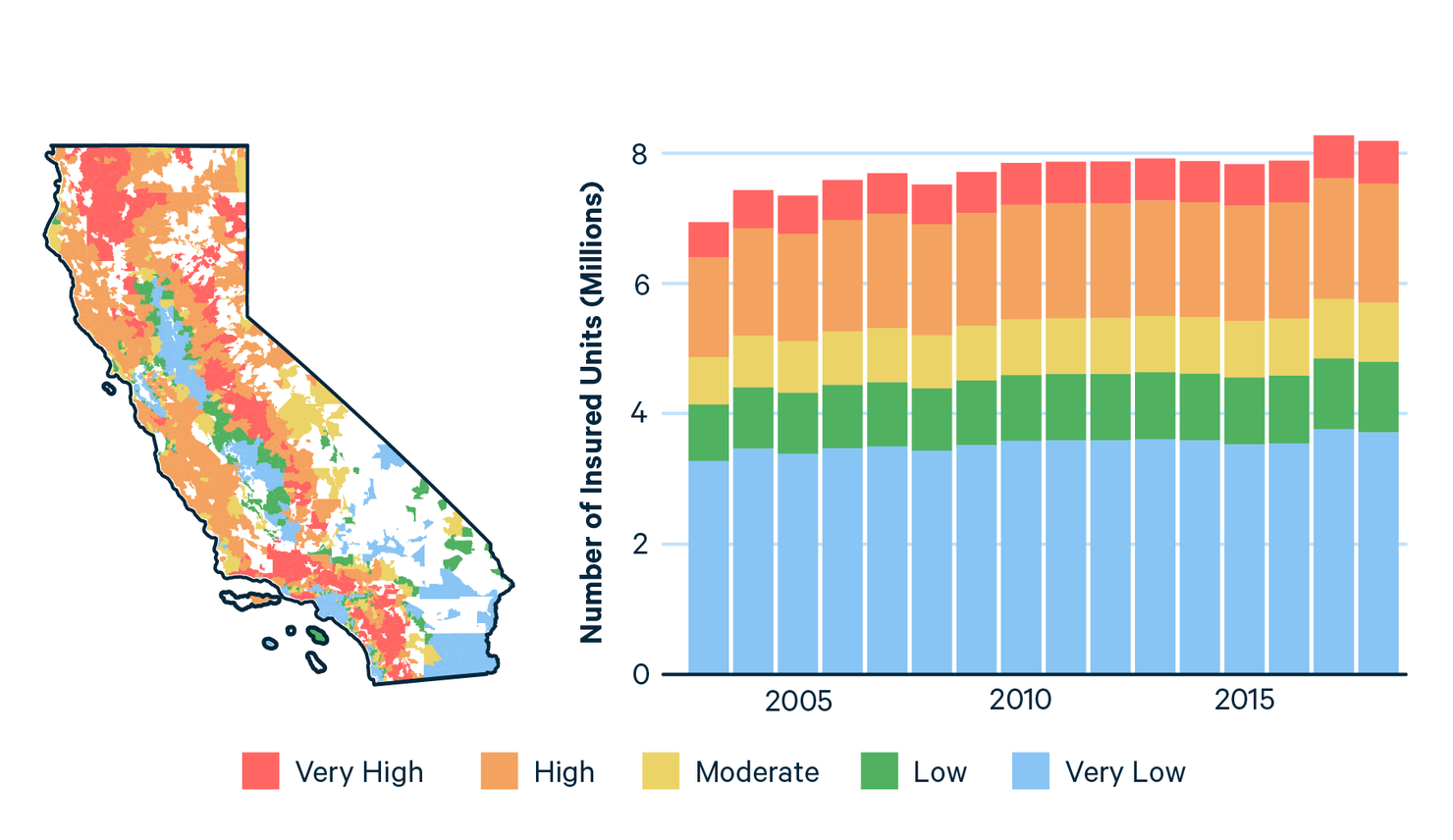

California’s diverse topography and susceptibility to drought create distinct wildfire risk zones. Areas within the Wildland-Urban Interface (WUI), where homes are built in proximity to or within wildlands, face the highest premiums. These zones are meticulously mapped by state and federal agencies, and insurers use these maps to assess the likelihood of a property being affected by a wildfire. Counties like Los Angeles and Orange County have substantial WUI areas, leading to higher insurance costs for many residents. Similarly, communities in more rural or mountainous regions, such as those in the Sierra Nevada foothills or parts of Santa Barbara County, often experience elevated premiums due to their inherent wildfire risk.

Insurance Market Conditions and Insurer Policies

The broader insurance market in California also plays a significant role. When insurers face substantial losses due to widespread wildfires, they often respond by increasing premiums across the board to recoup their financial burdens and maintain profitability. Furthermore, individual insurance companies have different risk appetites and underwriting guidelines. Some insurers may be more willing to offer coverage in high-risk areas, but often at a higher cost, while others might withdraw from certain markets altogether, limiting options and driving up prices for remaining policyholders. The availability of private insurance can also be impacted by legislative actions or market consolidation, further shaping the cost landscape.

What Does California Fire Insurance Typically Cover?

Understanding the scope of your fire insurance policy is essential to ensure adequate protection. While policies can vary, a standard homeowner’s fire insurance policy in California is designed to cover a range of damages directly resulting from a fire.

Direct Fire Damage and Related Perils

The core coverage of your fire insurance policy will address the physical damage to your home and its contents caused by fire. This includes damage from flames, smoke, and soot. Importantly, policies typically extend coverage to other perils commonly associated with fire events, such as damage from water used by firefighters to extinguish the blaze, and structural damage caused by the collapse of walls or roofs due to fire. Policies often cover not only the dwelling itself but also detached structures like garages or sheds, and your personal belongings within the home, up to specified limits.

Additional Living Expenses (ALE)

A crucial, and often overlooked, component of fire insurance is coverage for Additional Living Expenses (ALE), also known as Loss of Use. If a fire renders your home uninhabitable, ALE coverage helps pay for the necessary expenses incurred while you are displaced. This can include the cost of temporary housing, such as a hotel or rental apartment, as well as increased food expenses (if your temporary accommodation lacks cooking facilities), laundry costs, and other essential living expenses that exceed your normal budget. This coverage is vital for ensuring you can maintain a semblance of normalcy during the rebuilding or repair process, which can often take months or even years in severe cases.

Exclusions and Limitations

It is critical to be aware of what a standard fire insurance policy does not cover. While comprehensive, most policies have exclusions. Flood damage, for instance, is typically not covered by a fire insurance policy; separate flood insurance is required for that. Windstorms or hail damage might be covered under a broader homeowner’s policy, but the primary focus of “fire insurance” is the fire peril. Furthermore, claims for damage resulting from neglect, arson, or intentional acts by the policyholder are usually denied. It’s also important to check policy limits for specific items, such as jewelry, art, or firearms, as high-value items may require separate endorsements or riders for full coverage. Understanding these exclusions will help you determine if you need additional coverage to protect against all potential risks.

Strategies for Managing and Reducing Fire Insurance Costs

Given the rising premiums and the critical need for fire insurance in California, homeowners are actively seeking ways to manage these costs without compromising on essential protection. A proactive approach can lead to significant savings.

Enhancing Property Defensibility and Fire Resistance

Investing in your property’s fire resistance can have a direct and positive impact on your insurance premiums. Creating and maintaining defensible space is paramount. This involves clearing flammable vegetation, such as dry brush and trees, within a specified radius around your home. Many insurance companies and local fire departments recommend specific distances for this clearance. Additionally, upgrading your home’s exterior with fire-resistant materials can substantially reduce risk. This includes installing a Class A fire-rated roof (such as asphalt shingles or metal roofing), using non-combustible siding, and ensuring that vents are covered with fine mesh to prevent ember intrusion. Many insurers offer discounts for homes that meet specific fire-resilient building standards.

Shopping Around and Comparing Quotes

The insurance market is competitive, and premiums can vary significantly between different providers for the same coverage. It is highly advisable to shop around and obtain quotes from multiple insurance companies annually or whenever your policy is up for renewal. Don’t solely rely on your current insurer; explore options from national carriers, regional insurers, and independent insurance agents who can compare policies from various companies. When comparing quotes, ensure you are looking at comparable coverage levels, deductibles, and endorsements. A slightly higher deductible, for example, can often lead to a lower premium, so weigh the potential savings against your financial ability to cover a larger out-of-pocket expense in the event of a claim.

Exploring Insurance Options and Programs

For homeowners in high-risk wildfire areas, the traditional private insurance market may become unaffordable or unavailable. In such cases, it’s important to be aware of alternative insurance options and programs. The California FAIR Plan is a state-mandated insurance program that provides basic fire and extended coverage for homeowners who cannot obtain insurance through the voluntary market. While it offers essential protection, it typically comes at a higher cost and with limited coverage compared to standard private policies. Additionally, some insurers may offer specialized policies or endorsements designed for wildfire-prone areas, which might include specific mitigation requirements. Engaging with an experienced insurance broker who specializes in California property insurance can provide invaluable guidance in navigating these complex options and finding the most suitable and cost-effective coverage for your specific needs.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.