The question “When did Proposition 13 end in California?” often arises from a misunderstanding of this landmark piece of legislation. The direct answer is simple: Proposition 13 has not ended in California. It remains a foundational element of the state’s fiscal and political landscape, continuing to shape everything from public services to real estate, and in turn, subtly influencing the experiences of travelers, the operations of hotels, and the broader tourism economy across the Golden State.

Enacted in 1978, Proposition 13 fundamentally altered the way property taxes are assessed in California. Its enduring presence means that while the state has evolved dramatically over the past four decades, the mechanisms governing property taxation have largely remained the same, creating a unique environment with far-reaching implications. For visitors exploring the sun-drenched beaches of Malibu, the iconic streets of San Francisco, or the pristine wilderness of Yosemite National Park, the effects of Proposition 13 might not be immediately apparent. However, delve deeper, and you’ll find its fingerprints on the infrastructure that supports travel, the availability of accommodations, and even the local culture that draws millions to California each year. This article will explore the persistent legacy of Proposition 13, its profound impact on life and leisure in California, and why, despite numerous challenges, it has remained firmly in place.

The Enduring Legacy of Proposition 13: A California Cornerstone

To understand why the question of Proposition 13’s “end” is so pertinent, we must first revisit its origins and core tenets. Its passage represented a seismic shift in property taxation, born out of a period of rapidly escalating property values and a public outcry over rising tax burdens. The initiative was overwhelmingly approved by voters, driven by a powerful populist movement.

A Brief History and Its Immediate Impact

Proposition 13, officially known as the “People’s Initiative to Limit Property Taxation,” was passed by California voters on June 6, 1978. Its primary architect was Howard Jarvis, a conservative activist who tapped into widespread taxpayer frustration. Before Proposition 13, property taxes in California were assessed annually based on market value, which had been soaring. This meant that many homeowners, particularly those on fixed incomes, faced the prospect of being taxed out of their homes, even if they had paid off their mortgages years ago.

The proposition introduced several key provisions:

- Property Tax Rate Cap: It capped the maximum ad valorem tax on real property at 1% of the property’s “full cash value.”

- Assessed Value Rollback: It rolled back property assessments to their 1975 levels.

- Annual Increase Limit: It limited annual increases in assessed value to no more than 2% for inflation, regardless of actual market appreciation, until the property is sold.

- Reassessment Upon Change of Ownership: A property is only reassessed to its current market value when there is a change in ownership.

- Two-Thirds Vote for New Taxes: It required a two-thirds vote in both legislative houses for state tax increases and a two-thirds vote of local voters for special local taxes.

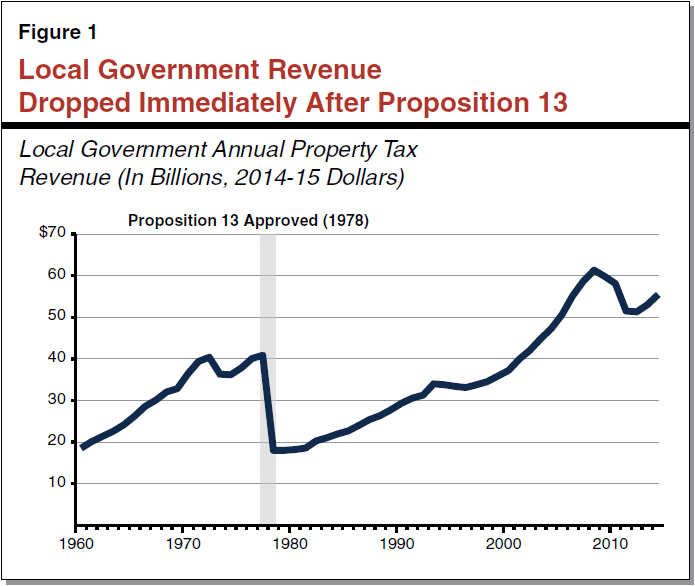

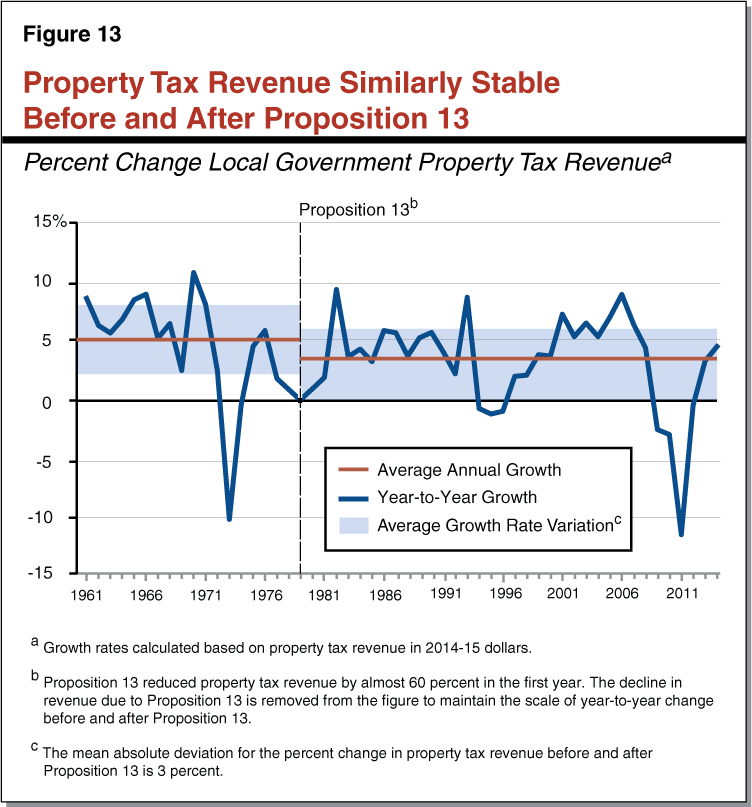

The immediate impact was a dramatic decrease in property tax revenue for local governments, schools, and other public agencies. While it provided much-needed relief for homeowners and businesses, it also forced a restructuring of public finance in California, leading to increased reliance on sales and income taxes and a centralization of control over local budgets at the state level.

The “Lock-in” Effect and Its Societal Implications

One of the most profound and often debated aspects of Proposition 13 is its “lock-in” effect. Because property is only reassessed to market value upon a change of ownership, long-term property owners pay significantly lower property taxes compared to new buyers, even on identical properties in the same neighborhood. This creates a powerful disincentive for homeowners to sell, as doing so would mean losing their low tax base and facing potentially vastly higher taxes on a new property.

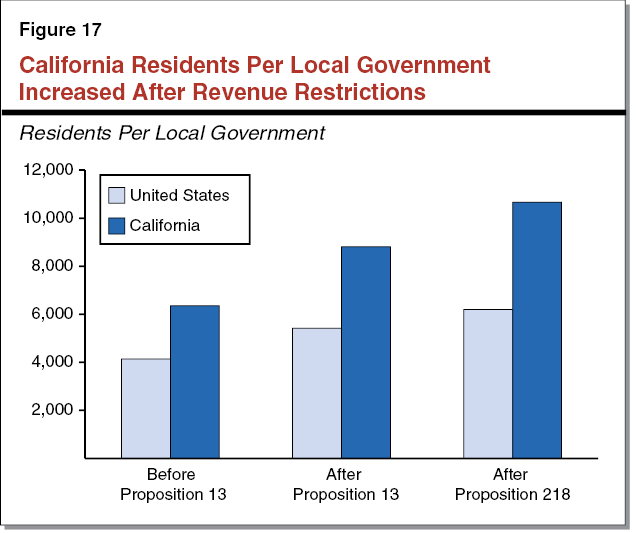

This “lock-in” effect has several significant societal implications. It contributes to housing shortages by reducing the turnover of properties, making it harder for younger generations or new residents to enter the housing market in desirable areas. It also fuels intergenerational wealth transfer, as properties with low tax bases can be passed down within families, perpetuating the tax advantage. For municipalities, this means that their property tax revenues do not grow in pace with property values, making it challenging to fund essential services that grow with population and inflation. The outcome is a fiscal squeeze that impacts public schools, libraries, emergency services, and the maintenance of public infrastructure—all elements that, directly or indirectly, shape the quality of life for residents and the experience for tourists visiting popular destinations like Santa Monica Pier or Golden Gate Bridge.

Navigating California’s Landscape: Proposition 13’s Influence on Travel and Lifestyle

The intricate web of Proposition 13’s effects extends far beyond property deeds and tax bills. Its influence subtly permeates the travel and tourism sectors, affecting everything from how infrastructure is maintained to the cost and availability of accommodation.

Infrastructure and Public Services: The Tourist’s Perspective

A smooth travel experience hinges on well-maintained infrastructure. Roads, public transportation, and accessible parks are crucial for tourists exploring California’s diverse attractions, from the bustling streets of Los Angeles to the serene beauty of Big Sur. Proposition 13’s constraints on local property tax revenue have, at times, made it challenging for local governments to fund these vital public services. While California remains a top-tier tourist destination, with world-renowned sites like Disneyland, Universal Studios Hollywood, and countless California State Parks, the ongoing challenge of infrastructure funding is a constant backdrop.

For example, funding for local street repairs, public transit expansions in cities like San Diego, or improvements to regional parks might be constrained. While the state has other revenue sources and bond measures to address some of these needs, the direct, stable local funding stream that property taxes once provided is significantly curtailed. This can impact the quality of the visitor experience, from the ease of navigating the state to the upkeep of the very landmarks and natural wonders that draw people here. A visit to the historic Alcatraz Island or a drive through Napa Valley relies on well-maintained access points and supporting municipal services.

Accommodation and the Real Estate Market

The real estate market in California is notoriously competitive and expensive, and Proposition 13 plays a significant role in this dynamic. The “lock-in” effect limits housing supply, contributing to high property values and, consequently, high rental rates. This directly impacts the accommodation sector, from hotels and resorts to vacation rentals.

For new hotel developments or existing properties that undergo a change of ownership (e.g., a major hotel chain acquiring a new property), the property tax burden is assessed at current market value. This higher fixed cost must then be factored into room rates, potentially making stays more expensive for tourists. Companies like Marriott International, Hilton Worldwide, or Hyatt Hotels Corporation operating in California navigate these property tax structures, which can influence their investment decisions in prime locations like Beverly Hills or Palm Springs.

Furthermore, the high cost of housing means that finding affordable long-term accommodation for workers in the tourism and hospitality industries can be challenging, particularly in popular destinations. This can impact staffing levels and service quality. For travelers seeking alternatives to traditional hotels, platforms like Airbnb and Vrbo have flourished, but even these face local regulations and property costs influenced by Proposition 13’s effects on the broader housing market. The cost of living is intrinsically linked to property values and taxes, and this, in turn, influences the entire economic ecosystem supporting California’s robust tourism industry.

The Ongoing Debate: Efforts to Reform and the Future of California Tourism

Despite its deeply entrenched status, Proposition 13 is not without its critics, and there have been numerous attempts to modify or repeal parts of it. These ongoing debates are crucial for understanding the future trajectory of California’s economy and, by extension, its tourism landscape.

“Split Roll” Proposals and Commercial Property

One of the most significant proposed reforms to Proposition 13 has been the “split roll” initiative. This proposal aims to maintain the current property tax protections for residential properties but reassess commercial and industrial properties at market value, often annually or every few years. Proponents argue that commercial properties, particularly those held by large corporations, benefit disproportionately from Proposition 13’s low tax rates, allowing them to avoid paying their “fair share” for public services. They believe that a split roll would generate billions in new revenue for schools and local governments without impacting homeowners.

For the tourism sector, a split roll could have mixed implications. On one hand, increased tax revenue could lead to improved public services and infrastructure, making California an even more attractive destination. Local public transport systems, road networks, and public park maintenance (essential for visitors to places like Death Valley National Park or Lake Tahoe) could see a much-needed boost in funding. On the other hand, commercial properties, including many hotels, resorts, and tourist attractions, would face significantly higher property tax bills. This could translate into increased operational costs, which might be passed on to consumers through higher prices for hotel stays, theme park tickets (e.g., The Walt Disney Company), or local dining experiences. The potential impact on smaller businesses within the tourism ecosystem, such as independent restaurants or boutique shops, is also a concern for opponents of the split roll.

Funding Local Culture and Attractions

Local culture and unique attractions are key drawcards for tourism. From world-class museums like the Getty Center in Los Angeles and the Monterey Bay Aquarium to historic sites like Hearst Castle, California offers a rich tapestry of experiences. Many of these cultural institutions and attractions rely on local funding, either directly through public grants or indirectly through community support enabled by healthy local economies.

Under the fiscal constraints imposed by Proposition 13, local governments often face tough choices about how to allocate limited resources. This can impact funding for arts programs, historical preservation, and the maintenance of public spaces that contribute to a vibrant local culture. While some major attractions are privately funded, many smaller cultural gems, local festivals, and community events that enhance the tourist experience depend on local government support. The ongoing debate over Proposition 13 reform is, in part, a conversation about how to ensure that California can continue to invest in the very assets that make it such a compelling destination for travelers worldwide.

The Lifestyle Paradox: Affordability, Luxury, and the California Dream

Proposition 13 has contributed to a distinct “lifestyle paradox” in California, characterized by both immense wealth and significant affordability challenges. This paradox directly influences travel choices, from luxury getaways to budget-conscious trips, and shapes the long-term prospects for residents and visitors alike.

Disparities in Homeownership and Travel Budgets

The “lock-in” effect of Proposition 13 has undeniably exacerbated wealth disparities within California. Long-term homeowners, often older generations who purchased properties decades ago, enjoy property tax burdens that are a fraction of what new homeowners or businesses pay. This creates a significant financial advantage, freeing up discretionary income that can be allocated to lifestyle choices, including travel. For these residents, luxury travel to exclusive resorts or international destinations is often more attainable.

Conversely, newer generations or those who moved to California more recently face much higher property taxes and overall living costs. This can severely limit their disposable income, forcing them to prioritize budget travel options, staycations, or less frequent trips. The high cost of living, partly driven by property values inflated by Proposition 13’s supply constraints, means that even middle-income families may struggle to afford basic necessities, let alone extensive travel. This dynamic creates a visible split in the travel market, catering to both the ultra-wealthy seeking experiences at five-star hotels like Four Seasons Hotels and Resorts and Ritz-Carlton, and those meticulously planning every aspect of a budget-friendly trip using services like Booking.com or Expedia.

Long-term Stays and Investment Opportunities

For individuals considering a long-term stay in California, whether for work in Silicon Valley, retirement, or extended travel, Proposition 13 presents a complex landscape. Renting an apartment or villa for an extended period means facing rental prices that largely reflect current market values, and thus, are significantly influenced by the high cost of property ownership for landlords. This makes long-term accommodation expensive in popular areas.

For investors, Proposition 13 creates a unique investment environment. While the appreciation potential for California real estate is often strong, the property tax implications for new purchases are substantial. This can deter some investors or influence the type of properties they acquire. For businesses seeking to establish a presence in California, from technology companies to film studios like Universal Pictures or Warner Bros. Studio Tour Hollywood, the property tax burden on their facilities is a significant operating cost that is carefully weighed. The long-term implications for growth and expansion are always considered against the backdrop of this unique tax structure.

In conclusion, the question “When did Proposition 13 end in California?” misunderstands its enduring power. It has not ended; rather, it has become an indelible part of the state’s identity. Its legacy is a double-edged sword: providing tax stability for long-term property owners while simultaneously contributing to housing unaffordability, infrastructure challenges, and a complex fiscal environment for local governments and businesses. For anyone experiencing California, whether as a fleeting tourist exploring Redwood National Park or Sequoia National Park, a temporary resident, or a long-term inhabitant, the unseen hand of Proposition 13 continues to shape the landscape, the opportunities, and the very fabric of the Golden State. It remains a pivotal, discussed, and continuously relevant cornerstone of California life.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.