The question of whether Puerto Rico pays taxes to the United States is a complex one, often shrouded in misunderstanding due to its unique political status as an unincorporated territory of the U.S. For many, the idea of a territory conjuring images of pristine beaches, vibrant culture, and world-class resorts might not immediately bring to mind tax obligations. However, the reality of Puerto Rico‘s relationship with the United States regarding taxation is nuanced and has significant implications for both its residents and the broader U.S. fiscal system. This exploration aims to demystify this intricate topic, drawing parallels with common travel and tourism experiences to offer clarity.

Understanding the U.S. Territorial Tax Structure

At its core, the tax relationship between the United States and its territories, including Puerto Rico, is not as straightforward as that between a state and the federal government. The U.S. Constitution grants Congress the power to “dispose of and make all needful Rules and Regulations respecting the Territory or other Property belonging to the United States.” This broad authority has led to a patchwork of tax laws and obligations that differ significantly from those in the fifty states.

Federal Income Tax: A Conditional Obligation

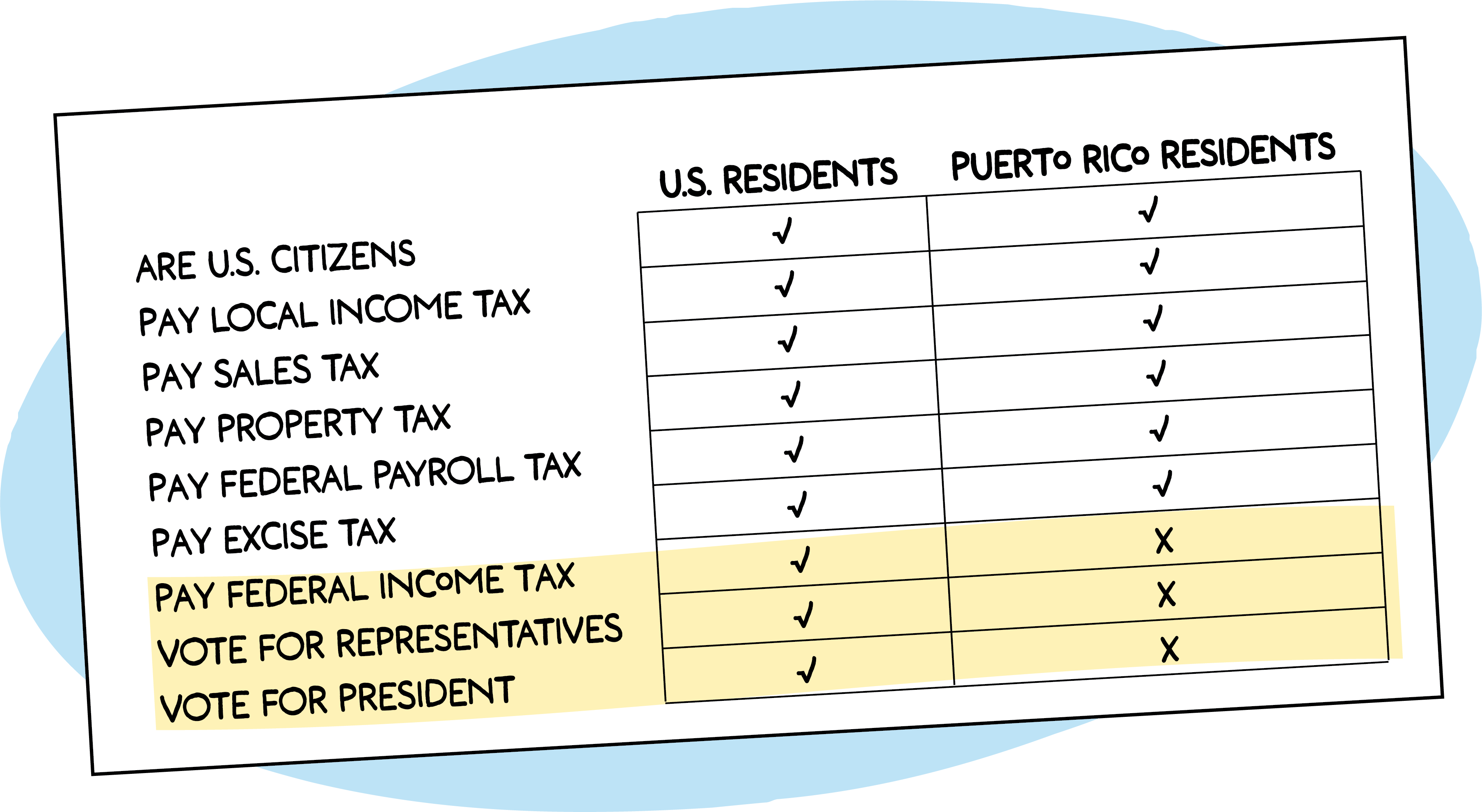

One of the most common questions is about federal income tax. Generally speaking, residents of Puerto Rico are not required to pay U.S. federal income tax on income earned within Puerto Rico. This exemption stems from Section 933 of the Internal Revenue Code. This means that if you live in Puerto Rico and earn your income there, you don’t file a federal tax return with the Internal Revenue Service (IRS). This is a significant difference compared to residents of the fifty states, who are subject to federal income tax on their worldwide income.

However, this exemption has important caveats. For example, U.S. citizens who are residents of Puerto Rico are still generally required to pay U.S. Social Security and Medicare taxes, often referred to as FICA taxes. These taxes fund crucial social programs. Additionally, if a Puerto Rican resident has income from U.S. sources outside of Puerto Rico, that income may be subject to federal income tax. This could include income from investments held in the mainland U.S. or wages earned while temporarily working in a state.

Furthermore, for individuals who are not U.S. citizens but are residents of Puerto Rico, the tax situation can be even more varied, depending on their specific immigration status and any treaties that might apply. The distinction between residents and non-residents, and the source of income, are critical factors in determining tax liability.

Corporate Taxation and Economic Incentives

The tax landscape for businesses operating in Puerto Rico is also distinct. While residents are largely exempt from federal income tax on locally earned income, corporations can present a more complex picture, especially those seeking to leverage Puerto Rico‘s economic development incentives.

Historically, Puerto Rico has utilized various tax incentives to attract investment and foster economic growth. These incentives have often involved significant reductions or exemptions from both local and federal corporate income taxes. Act 22, now known as Act 60, for example, is a landmark piece of legislation designed to attract new residents and businesses by offering substantial tax benefits, including a 0% tax rate on passive income for new residents who qualify. Such programs highlight Puerto Rico‘s strategic use of its tax authority to stimulate its economy, particularly in sectors like tourism, manufacturing, and technology.

However, the interplay between U.S. federal tax law and these local incentives is intricate. While companies operating in Puerto Rico might benefit from exemptions from U.S. corporate income tax on their Puerto Rican earnings, they are still subject to other federal taxes and regulations. The U.S. Treasury Department and IRS closely monitor these arrangements to ensure compliance with federal laws and to prevent tax avoidance schemes.

The debate surrounding Puerto Rico‘s tax status often intersects with discussions about its political future. Advocates for statehood often point to the tax disparities as a reason for full integration, arguing that Puerto Ricons should have the same rights and responsibilities, including taxation, as citizens in the states. Conversely, those who favor independence or a different form of self-governance may see the current tax structure as a vestige of colonial rule or a tool for economic self-determination.

Local Taxation in Puerto Rico

While the federal tax picture is nuanced, Puerto Rico does have its own robust system of taxation, managed by the Puerto Rico Department of the Treasury (Departamento de Hacienda). Residents and businesses operating on the island are subject to Puerto Rican income tax, sales tax (IVU – Impuesto sobre Ventas y Uso), property taxes, and various other local levies.

Puerto Rican Income Tax

For residents of Puerto Rico, the primary income tax obligation is to the Puerto Rican government. The tax rates and brackets are set by the Puerto Rico Legislative Assembly and can be adjusted periodically. These rates are generally progressive, meaning higher earners pay a larger percentage of their income in taxes. This local income tax is a crucial source of revenue for funding public services, infrastructure, education, and healthcare on the island.

Sales and Property Taxes

Like many jurisdictions, Puerto Rico imposes a sales tax on goods and services, known as IVU (Impuesto sobre Ventas y Uso). This tax is collected by businesses and remitted to the government. The rate of IVU can vary, and certain essential items may be exempt.

Property taxes are also levied on real estate within Puerto Rico. These taxes are a vital component of municipal and territorial revenue, contributing to local services and development projects. The valuation of property and the tax rates are determined by Puerto Rican law.

Other Local Taxes and Fees

Beyond income, sales, and property taxes, Puerto Rico also imposes a variety of other taxes and fees. These can include excise taxes on certain goods, excise taxes on vehicles, and fees related to business permits and licenses. These local taxes are integral to the functioning of the Puerto Rican government and its ability to provide essential services to its residents and to support the burgeoning tourism industry, which relies heavily on well-maintained infrastructure and public safety.

Taxation of U.S. Citizens Living or Visiting Puerto Rico

The tax implications for U.S. citizens who are not permanent residents of Puerto Rico but either live there temporarily or are visiting are also important to understand, especially for travelers and potential expatriates.

Temporary Residents and U.S. Source Income

For U.S. citizens who establish residency in Puerto Rico but are not yet fully compliant with residency requirements for the federal income tax exemption (under Section 933), or who have income from U.S. sources, the tax situation can be mixed. Generally, if a U.S. citizen resides in Puerto Rico, their Puerto Rican source income is exempt from federal income tax. However, income sourced from the United States would still be taxable by the IRS. This distinction can be crucial for individuals who maintain business interests or investments in the U.S. while living in Puerto Rico.

Tourists and Short-Term Visitors

For tourists visiting Puerto Rico from the United States, the tax implications are minimal. You do not pay U.S. federal income tax on purchases made while on vacation in Puerto Rico. You are still subject to U.S. federal income tax on your income earned back home. While you might pay Puerto Rican sales tax (IVU) on your purchases, this is a local tax that funds the island’s economy. There are no special “tourist taxes” that go directly to the U.S. federal government beyond the standard airport fees that are part of your airfare.

The experience of enjoying Puerto Rico‘s rich culture, exploring landmarks like El Morro or the Bioluminescent Bays in Vieques, and staying in exquisite resorts such as the Dorado Beach, a Ritz-Carlton Reserve, or the St. Regis Bahia Beach Resort, is largely free from additional federal tax burdens. The local IVU is simply part of the cost of goods and services, similar to sales tax in any U.S. state.

The Broader Implications and Future

The tax relationship between Puerto Rico and the United States is not merely an academic exercise; it has profound real-world consequences for the island’s economy, its residents’ livelihoods, and its political aspirations. The debate over Puerto Rico‘s status, whether it be statehood, independence, or enhanced commonwealth status, is intrinsically linked to tax policy.

Economic Development and Tax Policy

Puerto Rico‘s tax policies, both local and its unique federal exemptions, have been instrumental in shaping its economic development. The allure of tax incentives has attracted significant investment in sectors like pharmaceuticals, manufacturing, and increasingly, tourism. However, the economic challenges Puerto Rico has faced, including its substantial public debt, have also led to scrutiny of its tax structure and calls for reform. The U.S. federal government’s oversight of Puerto Rico‘s finances, including its debt restructuring, highlights the ongoing interdependence between the territory and the mainland.

Resident Tax Burden and Public Services

For Puerto Rican residents, the tax system dictates the level of funding available for public services. The Puerto Rican government relies heavily on local tax revenue to maintain schools, hospitals, infrastructure, and public safety. The economic conditions on the island, including employment rates and average income, directly influence the tax base. This is why policies aimed at economic growth and job creation are so critical. The ability of residents to enjoy quality of life, whether exploring the vibrant streets of Old San Juan or relaxing on the beaches of Luquillo, is directly tied to the effectiveness of the island’s own revenue generation and expenditure.

Political Status and Tax Autonomy

Ultimately, the question of Puerto Rico‘s tax obligations is inseparable from its political status. As an unincorporated territory, Puerto Rico possesses a degree of autonomy but remains subject to U.S. federal law. Advocates for greater self-determination argue that Puerto Rico should have more control over its fiscal policies, including its tax rates and incentives, to better address its unique economic and social needs. The ongoing political discourse surrounding Puerto Rico‘s future will undoubtedly continue to shape its tax landscape and its relationship with the United States.

In conclusion, while residents of Puerto Rico generally do not pay U.S. federal income tax on income earned on the island, they are subject to Puerto Rico‘s own comprehensive tax system. This nuanced tax structure reflects Puerto Rico‘s unique territorial status and plays a significant role in its economic development and the provision of public services for its residents. For visitors and travelers, the primary tax consideration is the local IVU, while the broader federal tax implications remain a complex aspect of Puerto Rico‘s intricate relationship with the United States.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.