Navigating the intricacies of property taxes in California can feel like exploring a new, complex landscape. For anyone considering purchasing a home, investing in real estate, or simply managing their assets within the Golden State, understanding this essential financial component is crucial. While the website often focuses on the delights of travel, from discovering breathtaking Landmarks to indulging in luxurious Hotels and experiencing vibrant Tourism, the practicalities of homeownership are an equally significant aspect of life. This article delves into how property tax is calculated in California, aiming to demystify the process and empower you with knowledge.

Understanding the Foundation: Proposition 13

The bedrock of California’s property tax system is Proposition 13, a landmark initiative passed by voters in 1978. This initiative fundamentally reshaped how property is assessed and taxed. Its core principles have remained largely intact, influencing every subsequent calculation. Proposition 13 established two primary mechanisms that govern property taxes:

The Assessed Value: The 1975 Base Year

One of the most significant impacts of Proposition 13 is its establishment of a base year for property assessment. For properties that were owned and occupied as a principal residence or were income-producing before March 1, 1975, their assessed value is fixed at their 1975 market value. This means that many long-time homeowners in California are currently paying property taxes based on an assessment from nearly five decades ago, often considerably lower than current market values.

However, for properties acquired after March 1, 1975, the assessed value is generally based on the actual purchase price or the fair market value at the time of acquisition. This means that newer homeowners will have a higher assessed value compared to those who have owned their property for an extended period, assuming similar properties. This disparity is a direct consequence of Proposition 13’s design, aiming to provide tax stability for existing owners while reflecting market realities for new transactions.

Annual Inflation Adjustments

Beyond the initial assessment, Proposition 13 also limits annual increases to the assessed value. The assessed value of a property can only increase by a maximum of 2% per year, or by the percentage of the annual increase in the California Consumer Price Index (CPI), whichever is less. This inflation adjustment is applied to the already established assessed value from the base year or acquisition date. This means that even if the market value of a property skyrockles, the assessed value, and consequently the property tax, will only increase gradually, capped at a modest annual rate.

This provision was designed to protect homeowners from being priced out of their homes due to rapidly escalating property values and unpredictable tax hikes. It provides a predictable and manageable increase in property tax liability for property owners.

The Tax Rate: A Uniform 1% Base

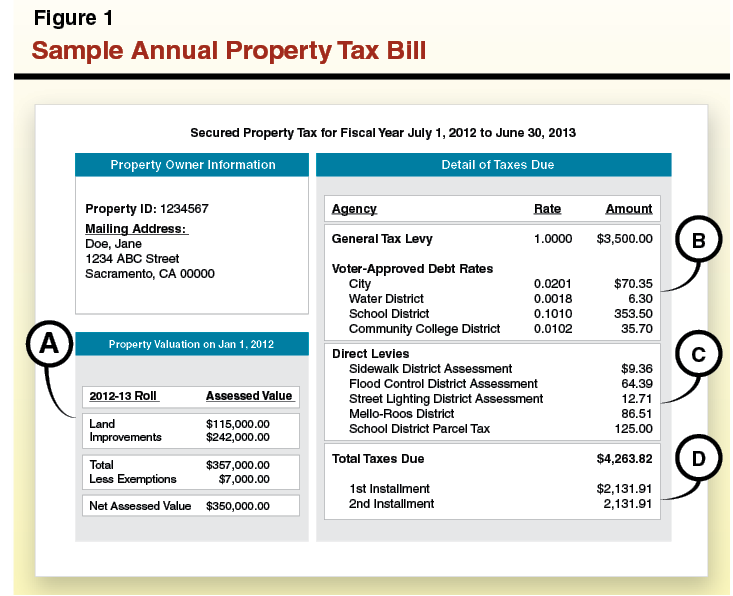

In conjunction with the assessed value, the tax rate plays a critical role in determining the final property tax bill. Proposition 13 also established a uniform statewide property tax rate of 1% of the assessed value. This 1% rate applies to most general property taxes levied by local governments, including school districts, cities, and counties.

This flat rate simplifies the tax structure, ensuring that everyone pays the same percentage of their assessed value, regardless of the specific taxing jurisdiction within California. However, it’s important to note that this 1% is a base rate, and additional levies, often referred to as “special assessments” or “voter-approved taxes,” can be added to this base rate. These additional levies are typically used to fund specific local services or projects and require voter approval.

Beyond the Base: Special Assessments and Voter-Approved Taxes

While the 1% rate forms the core of property tax calculations, it’s not the entirety of the bill for many properties. Over time, local governments and school districts have sought and obtained voter approval for additional taxes and assessments to fund essential services and infrastructure improvements. These can include:

- School Bonds: Many districts have voter-approved bonds to fund school construction, renovations, and modernization. These are often levied as a per-parcel tax or a percentage of the assessed value.

- Local Improvement Districts: These can fund projects like street paving, sewer upgrades, or park maintenance within specific neighborhoods or districts.

- Special Service Levies: Some areas might have additional taxes for specific services like fire protection or flood control.

These additional levies are added to the 1% base rate, meaning a property owner’s total property tax rate can exceed 1%. The specific amounts and types of these additional levies vary significantly from one jurisdiction to another across California. To determine the exact tax rate for a particular property, one must consider the base 1% rate plus any applicable voter-approved taxes and special assessments levied by the local authorities.

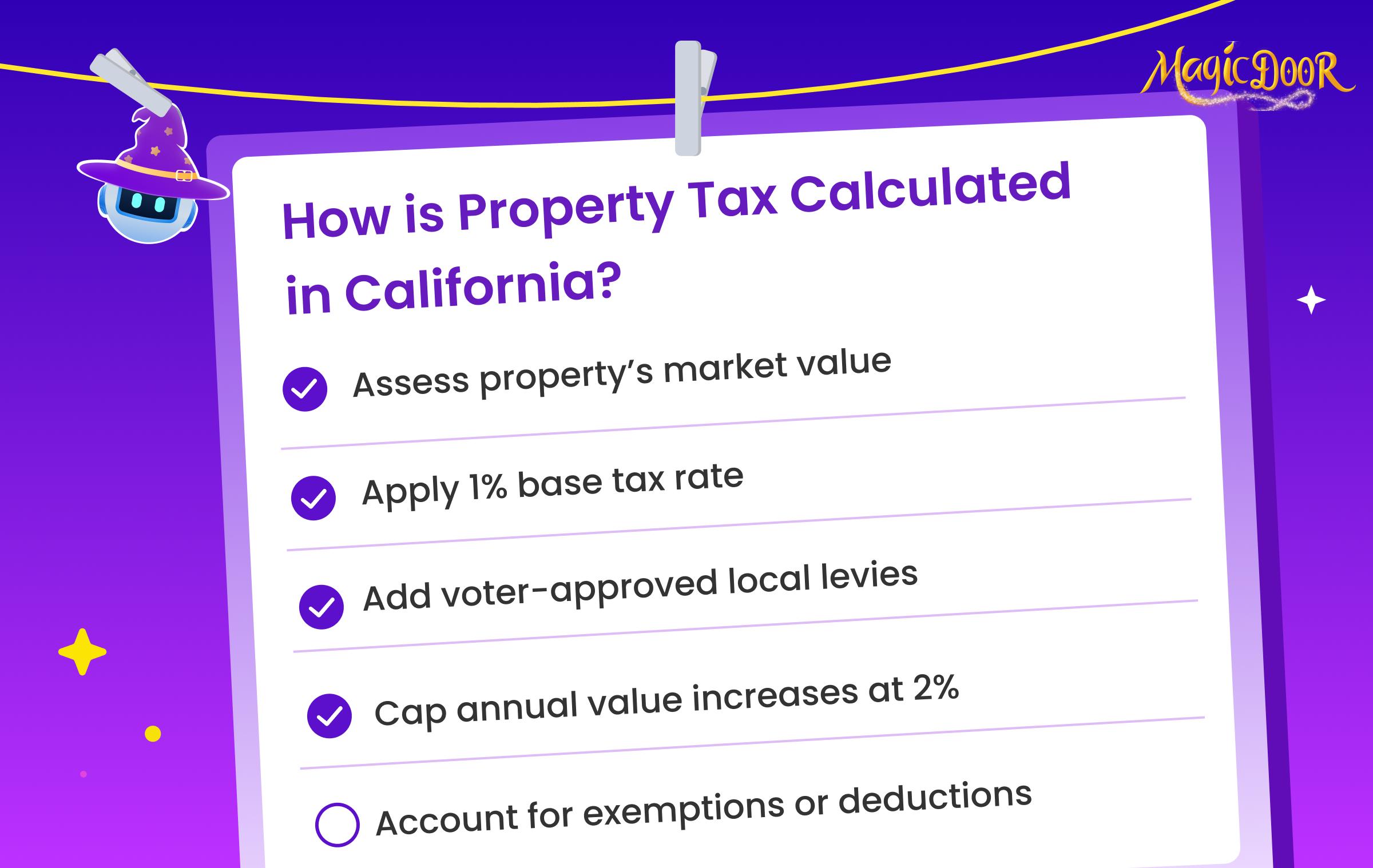

The Calculation Process: Putting It All Together

With the fundamental principles of assessed value and tax rate established, the actual calculation of property tax in California becomes more straightforward.

The basic formula is as follows:

Property Tax = Assessed Value x Tax Rate

Let’s break down how this applies in practice:

Step 1: Determining the Assessed Value

As discussed, the assessed value is determined by the property’s market value at the time of acquisition (for properties acquired after March 1, 1975) or its 1975 market value (for properties acquired before that date). This base value is then subject to annual inflation adjustments of no more than 2% per year.

For example, if you purchased a property in Los Angeles in 2000 for $300,000, your initial assessed value would likely be $300,000. If the assessed value was then increased by the maximum 2% for each subsequent year, the assessed value would grow gradually over time, irrespective of market fluctuations.

Step 2: Applying the Tax Rate

Once the current assessed value is determined, the statewide base tax rate of 1% is applied.

Continuing our Los Angeles example, if your assessed value in the current year is $450,000, the base property tax would be:

$450,000 x 1% = $4,500

Step 3: Adding Special Assessments and Voter-Approved Taxes

If there are any additional local levies or voter-approved taxes applicable to your property, these are added to the base tax calculated in Step 2. Let’s assume in our Los Angeles example, there is a voter-approved school bond requiring an additional 0.5% tax and a special assessment for local park maintenance of $100 per year.

The additional tax from the school bond would be:

$450,000 x 0.5% = $2,250

The total property tax bill would then be:

$4,500 (base tax) + $2,250 (school bond) + $100 (park assessment) = $6,850

This demonstrates how the final tax liability can exceed the initial 1% base rate.

Proposition 13’s Impact and Exceptions

Proposition 13 has had a profound and lasting impact on California’s property tax landscape. Its primary goal was to limit property tax burdens and prevent the reassessment of properties to current market values upon changes in ownership, thereby protecting existing homeowners from unaffordable tax increases. This has contributed to housing affordability for long-term residents and stability for local government revenue streams, albeit with the consequence of a growing disparity between older and newer property tax assessments.

Property Reassessments

While Proposition 13 limits annual increases, there are specific events that trigger a reassessment of a property to its current market value. These include:

- Change in Ownership: When a property is sold, transferred, or inherited, it typically triggers a reassessment. This means the new owner’s property tax will be based on the property’s fair market value at the time of the transfer, not the seller’s historical assessed value. However, there are important exclusions, such as transfers between parents and children or between spouses, which may allow the property to retain its existing assessed value.

- Completion of New Construction: If substantial new construction is added to a property, that new construction will be assessed at its current market value, while the existing structure will continue to be assessed under Proposition 13 rules.

Homeowner’s Exemptions

California offers a homeowner’s exemption that reduces the taxable value of a principal residence by a fixed amount. This exemption is automatically applied to eligible properties and further reduces the property tax burden for homeowners. For the 2023-2024 fiscal year, the homeowner’s exemption reduced the taxable value of eligible properties by $7,000.

Other Exemptions and Relief Programs

Beyond the homeowner’s exemption, California provides various other property tax relief programs for specific groups, such as:

- Disabled Veterans’ Exemption: Provides a significant exemption for qualifying disabled veterans.

- Senior Citizens’ Property Tax Assistance: While not a direct reduction in property tax liability, this program provides financial assistance to low-income seniors to help pay their property taxes.

- Welfare Exemption: Applies to properties owned and used by qualifying charitable organizations.

Understanding these nuances and exceptions is vital for anyone seeking to accurately calculate and manage their property tax obligations in California. While the principles of Proposition 13 provide a foundational framework, the presence of special assessments, voter-approved taxes, and various exemptions means that each property’s tax calculation is unique. For those planning a trip, perhaps to explore the natural beauty of Yosemite National Park or the vibrant arts scene in San Francisco, it’s worth remembering that property taxes are an integral part of the California living experience.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.