Planning a trip to the Golden State, a destination renowned for its breathtaking national parks, vibrant cities, and diverse landscapes, often sparks practical questions about budgeting. While dreams of exploring Disneyland, hiking in Yosemite National Park, or indulging in the culinary delights of San Francisco are exhilarating, understanding the financial aspects is crucial for a smooth and enjoyable experience. Among these considerations, a common question that arises, especially for those planning extended stays or considering relocation, is: “How much are California state income taxes?” This article delves into the intricacies of California’s income tax system, offering insights relevant to travelers, potential residents, and anyone curious about the financial climate of this iconic state.

California’s tax structure is a complex yet vital component of its economy, funding essential public services that contribute to the state’s allure, from maintaining its beautiful beaches to supporting its world-class educational institutions. For visitors, understanding this might seem peripheral, but for those contemplating a longer sojourn, perhaps a sabbatical in a charming California villa or a business venture in Los Angeles, grasping the tax implications is paramount. This guide aims to demystify California’s income tax, breaking down the rates, brackets, and other factors that influence the final tax liability.

Understanding California’s Progressive Income Tax System

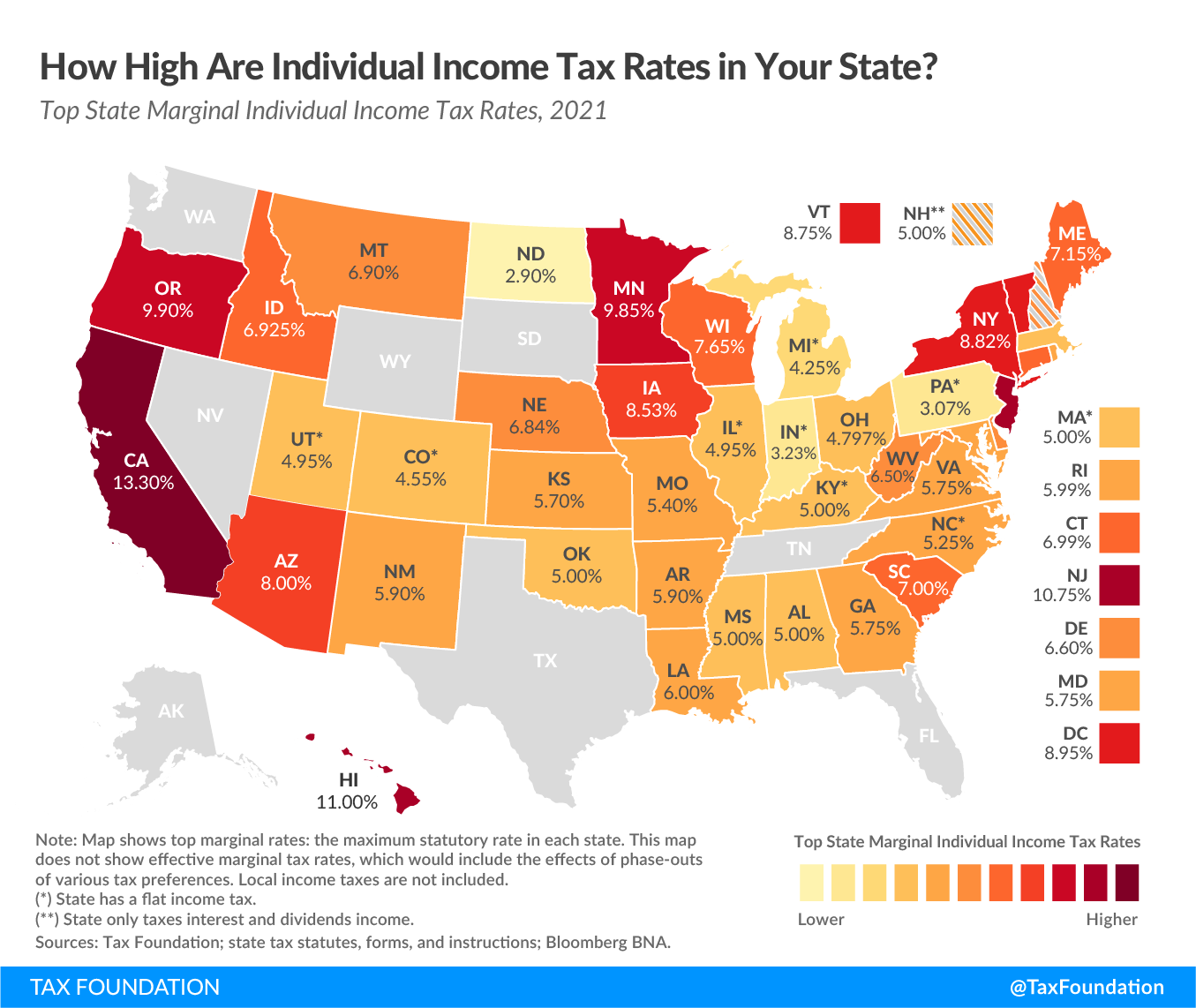

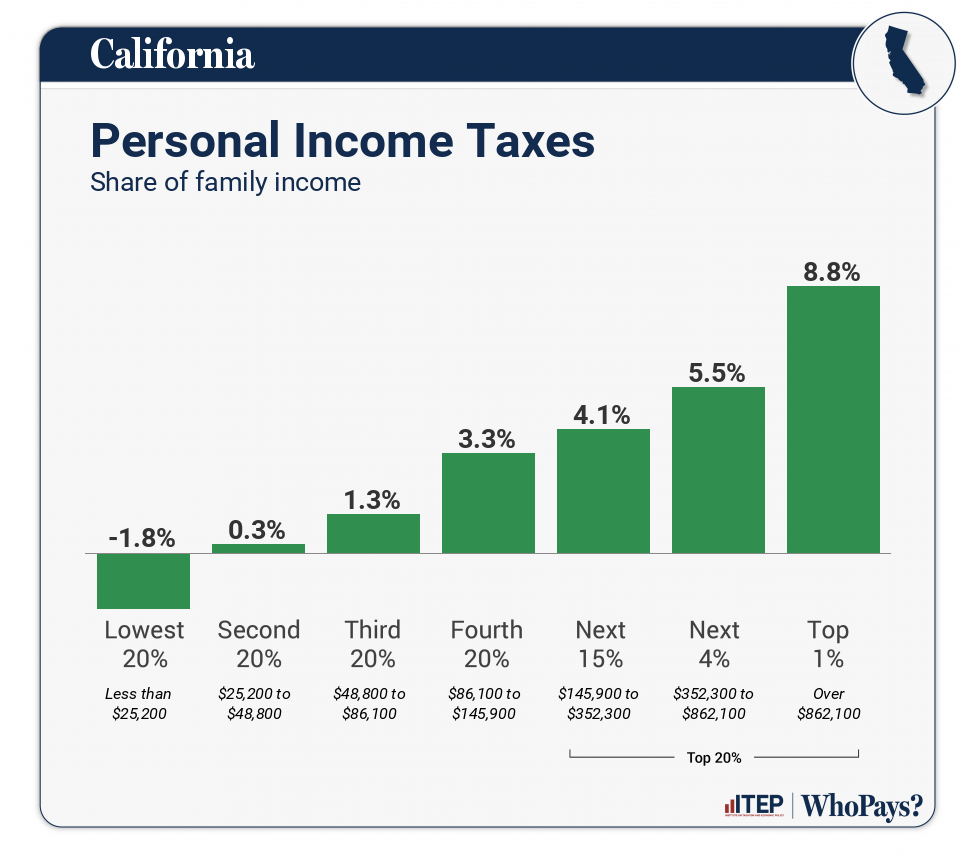

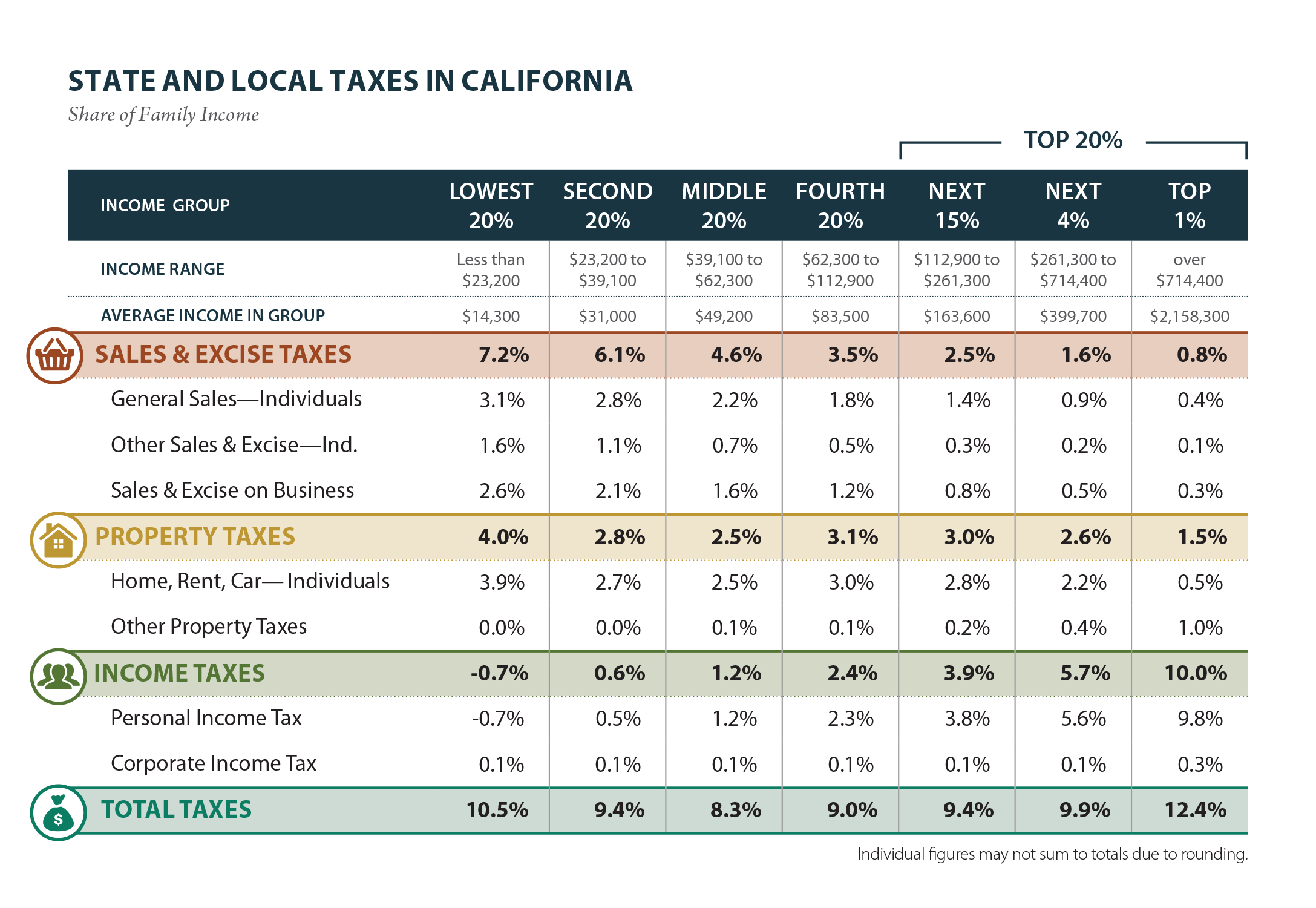

California employs a progressive income tax system. This means that as your income increases, so does the percentage of tax you pay on that income. The state utilizes a tiered bracket system, where different portions of your income are taxed at different rates. This system is designed to place a greater tax burden on higher earners while providing a lower tax rate for those with more modest incomes. For the California resident, and increasingly for those who spend significant time working or earning income within the state, understanding these brackets is the first step in estimating tax obligations.

California Income Tax Brackets and Rates

The specific tax brackets and rates are subject to change annually due to inflation adjustments. However, the general structure remains consistent. For the most recent tax year, the California Franchise Tax Board (FTB) outlines these progressive rates. These rates can range from a low percentage for the lowest income brackets to a higher percentage for the highest earners. It’s important to note that these are marginal tax rates, meaning only the income within a specific bracket is taxed at that bracket’s rate. For instance, if you fall into a higher tax bracket, only the portion of your income that exceeds the lower bracket thresholds is taxed at the higher rate.

To illustrate, let’s consider a simplified example. If the lowest tax bracket is 1%, and the next bracket is 2%, and your income falls into both, you wouldn’t pay 2% on your entire income. Instead, the income up to the threshold of the first bracket would be taxed at 1%, and the income above that threshold, up to the limit of the second bracket, would be taxed at 2%. This progressive nature is a cornerstone of the California tax system.

Filing Status and Its Impact

Your filing status significantly influences your California income tax liability. The primary filing statuses recognized by the FTB are:

- Single: For unmarried individuals.

- Married/Registered Domestic Partner Filing Separately: For married couples or registered domestic partners who choose to file individual tax returns.

- Married/Registered Domestic Partner Filing Jointly: For married couples or registered domestic partners who file a single, combined tax return.

- Head of Household: For unmarried individuals who pay more than half the cost of keeping up a home for a qualifying child.

Each filing status has its own set of income tax brackets and standard deductions, which can lead to different tax outcomes. For example, married couples filing jointly might benefit from lower combined tax rates on their shared income compared to filing separately, depending on their income levels. Understanding which filing status applies to you is a crucial step in accurately calculating your potential tax burden, whether you are a seasoned resident of San Diego or a newcomer considering a move to the Bay Area.

Deductions and Credits: Reducing Your Taxable Income

Beyond the progressive tax brackets, California offers various deductions and credits designed to lower your taxable income and, consequently, your tax bill. These can be particularly beneficial for individuals and families.

Standard vs. Itemized Deductions

Similar to the federal tax system, California taxpayers can choose between taking the standard deduction or itemizing their deductions.

- Standard Deduction: This is a fixed dollar amount that reduces your taxable income. The amount of the standard deduction varies based on your filing status. It’s a simpler option for many taxpayers.

- Itemized Deductions: If your eligible expenses exceed the standard deduction amount, itemizing may be more beneficial. Common itemized deductions in California include:

- State and local taxes (SALT), though this is subject to federal limitations.

- Home mortgage interest.

- Charitable contributions.

- Medical expenses (above a certain threshold).

- Certain other expenses.

Choosing between the standard and itemized deduction requires careful calculation to determine which method will result in the greatest tax savings. For someone considering a long-term stay in a California apartment or buying a home, understanding these deductions is essential for financial planning.

Tax Credits

Tax credits are even more valuable than deductions because they directly reduce the amount of tax you owe, dollar for dollar. California offers a variety of tax credits, which can include:

- Child and Dependent Care Credit: For expenses incurred for the care of qualifying dependents while you work or look for work.

- Earned Income Tax Credit (EITC): For low-to-moderate income working individuals and families. This is a significant credit for many Californians.

- Renters’ Credit: For eligible renters who pay rent for their principal residence in California.

- Other specific credits: These can be for various purposes, such as energy efficiency improvements, donations to specific organizations, or for certain business activities.

Staying informed about available credits can lead to substantial tax savings. Planning your activities, such as investing in energy-efficient upgrades for your California residence, could potentially qualify you for specific credits.

Who Pays California State Income Tax?

The question of “who pays” California state income tax is multifaceted. Generally, any individual or entity that earns income within California is subject to its income tax laws. This includes:

- Residents: Individuals who live in California for more than 183 days during the tax year are considered residents and are taxed on their worldwide income. This means all income earned, regardless of where it is generated, is subject to California income tax. This is a crucial distinction for individuals considering a move to or from the state, perhaps from a lower-tax state like Nevada.

- Nonresidents: Individuals who earn income in California but do not meet the residency criteria are considered nonresidents. They are only taxed on their income derived from California sources. This could include income from a business located in California, rental properties within the state, or wages earned for work performed in California, even if their primary residence is elsewhere.

- Part-year Residents: Individuals who move into or out of California during the tax year are considered part-year residents. They are taxed on their income earned while they were a resident of California (worldwide income) and on their income earned from California sources while they were a nonresident.

For tourists, the income tax is typically not a concern. However, for individuals engaged in remote work while enjoying the California lifestyle, or for those who own rental properties in California, understanding their tax status and obligations is crucial. This can include individuals staying in a boutique hotel in Santa Barbara for an extended period while working remotely, or property owners renting out their California villas to vacationers.

Business Income and Other Earnings

The scope of California income tax extends beyond individual wage earners.

- Business Income: Businesses operating in California, whether sole proprietorships, partnerships, or corporations, are subject to California income or franchise taxes. The specific tax structure for businesses is complex and depends on the business entity type and revenue.

- Investment Income: Income from investments, such as dividends, interest, and capital gains, is also taxable in California for residents. Nonresidents may be taxed on California-source investment income.

- Gig Economy and Freelance Income: For individuals working in the gig economy or as freelancers in California, income earned is generally considered taxable. Proper record-keeping and understanding of estimated tax payments are vital to avoid penalties. This is particularly relevant for those enjoying the dynamic lifestyle opportunities in cities like Austin, Texas (though not in California, it serves as an example of a gig economy hub), who might also have business interests in California.

Planning Your Finances in the Golden State

Whether you’re planning a memorable family trip to the California coast, considering a long-term stay in a luxury resort, or contemplating a more permanent move, understanding California’s income tax system is a vital part of your financial planning.

The Importance of Professional Advice

The California tax code is intricate, with frequent updates and nuances that can affect your tax liability. For individuals with complex financial situations, significant income, or uncertainty about their tax obligations, consulting with a qualified tax professional is highly recommended. A tax advisor can help you:

- Determine your residency status.

- Identify all applicable deductions and credits.

- Ensure accurate tax filing.

- Develop strategies for tax optimization.

This is especially true for those considering significant financial decisions, such as purchasing property in California or investing in California-based businesses. Even for frequent travelers who might stay in various California hotels or apartments, understanding potential tax implications for extended stays or short-term rental income can prevent unforeseen liabilities.

Resources for Tax Information

The California Franchise Tax Board (FTB) is the primary source for official tax information in California. Their website provides comprehensive resources, including:

- Tax forms and publications.

- Information on tax rates and brackets.

- Details on deductions and credits.

- Guidance on residency.

- Updates on tax law changes.

By staying informed and seeking professional guidance when needed, you can navigate the complexities of California state income taxes with confidence, ensuring your financial plans align with your travel dreams and lifestyle aspirations in the Golden State. Whether you’re drawn to the iconic Golden Gate Bridge, the sunny beaches of Southern California, or the serene beauty of the Sierra Nevada mountains, a clear understanding of your financial obligations will enhance your experience in this remarkable state.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.