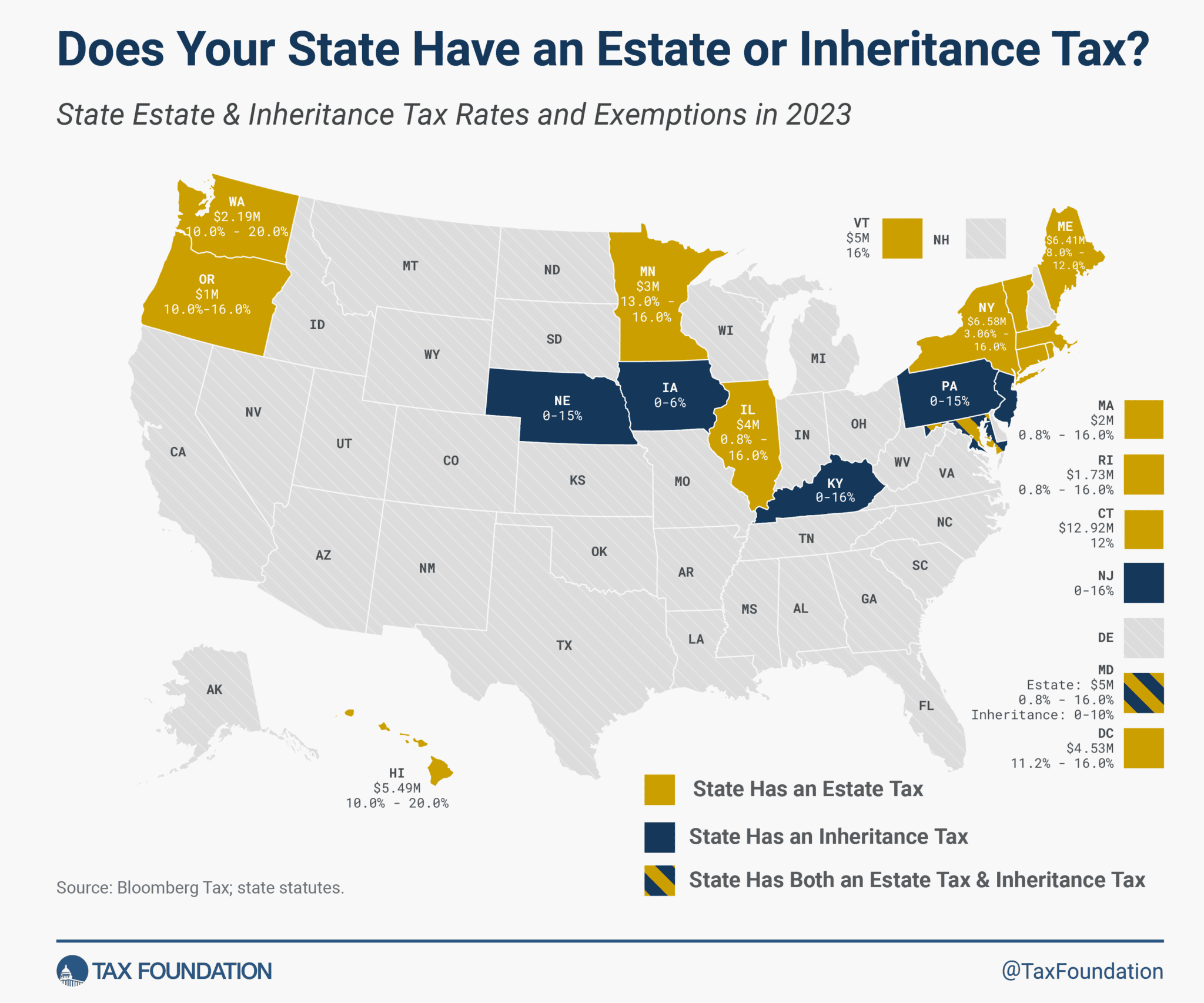

The term “death tax” often conjures images of complex financial maneuvers and steep financial penalties for grieving families. In California, while there isn’t a state-level “death tax” in the way some other states impose an inheritance tax, residents and their heirs can still face significant estate tax implications at the federal level. Understanding these implications and strategically planning can help minimize the financial burden on your loved ones. This guide will delve into the nuances of estate taxation, particularly as it pertains to California residents, and explore various methods for wealth preservation and tax mitigation.

The concept of a “death tax” is often misunderstood. It generally refers to taxes levied on the transfer of a deceased person’s assets. While California itself does not have an inheritance or estate tax, the United States has a federal estate tax. This tax applies only to very large estates, and California residents are subject to the same federal rules as citizens of any other state. Therefore, the primary focus for Californians concerned about “death taxes” is the federal estate tax and how to plan for it effectively.

Understanding Federal Estate Tax Implications

The federal estate tax is a tax on the right to transfer property at death. It is levied on the total value of a decedent’s taxable estate. However, there’s a significant exemption amount that shields most estates from this tax. For many years, this exemption has been quite generous, meaning only the wealthiest individuals have had to worry about paying federal estate tax.

The Federal Estate Tax Exemption

The federal estate tax exemption is adjusted annually for inflation. For the year 2024, the exemption amount is substantial. This means that an individual can pass a considerable amount of wealth to their heirs without incurring any federal estate tax. For a married couple, the exemption can effectively be doubled through portability, allowing the surviving spouse to use the deceased spouse’s unused exemption. This is a crucial planning tool that can significantly reduce or eliminate federal estate tax liability for many couples.

It’s important to note that the taxable estate is not simply the gross value of assets. Certain deductions are allowed, such as debts, funeral expenses, administrative costs, and charitable bequests. These deductions can reduce the value of the taxable estate, potentially bringing it below the exemption threshold.

Portability for Married Couples

Portability is a provision that allows the surviving spouse to elect to use the deceased spouse’s unused federal estate tax exemption. This election must be made by filing a federal estate tax return (Form 706) for the deceased spouse, even if no tax is due. Without this election, the unused portion of the first spouse’s exemption is lost. This is a vital strategy for married couples to maximize their combined estate tax exclusion. Imagine a couple who each have significant assets. If one spouse passes away, and they haven’t elected portability, their heirs will only benefit from the surviving spouse’s individual exemption. However, with portability, the surviving spouse can utilize both exemptions, potentially doubling the amount that can be passed on tax-free. This is particularly relevant for couples with substantial real estate holdings, investment portfolios, or business interests.

Gifts and Lifetime Exemptions

The federal estate tax also considers taxable gifts made during an individual’s lifetime. The unified credit against estate and gift taxes applies to both lifetime gifts and transfers at death. Any portion of the unified credit used to eliminate gift tax on lifetime gifts reduces the amount of credit available for estate tax purposes. Therefore, while making gifts can be a valuable estate planning tool, it’s essential to track these gifts and understand their impact on the remaining estate tax exemption. For instance, if someone makes substantial gifts during their lifetime that exceed the annual gift tax exclusion, they will use up a portion of their unified credit. This will, in turn, reduce the amount they can pass on to their heirs tax-free at death. Careful consideration of lifetime gifting strategies, in conjunction with overall estate planning, is paramount.

Strategies to Mitigate Estate Tax Liability

While the federal estate tax exemption is high, for individuals with estates exceeding this threshold, proactive planning is essential. Several strategies can help minimize estate tax liability, ensuring more of your wealth is preserved for your beneficiaries. These strategies often involve carefully structured trusts, strategic gifting, and thoughtful use of insurance.

Utilizing Trusts

Trusts are powerful legal instruments that can play a significant role in estate tax planning. Different types of trusts can be established to achieve specific goals, such as reducing the taxable estate, providing for beneficiaries, and avoiding probate.

Irrevocable Trusts

Irrevocable trusts are generally considered outside of the grantor’s taxable estate, provided certain conditions are met. Once assets are transferred into an irrevocable trust, they typically cannot be reclaimed by the grantor. This separation of assets can be instrumental in reducing the overall size of the taxable estate.

- Irrevocable Life Insurance Trusts (ILITs): An ILIT can be used to own life insurance policies. The death benefit paid out by the policy is not included in the grantor’s taxable estate, provided the grantor does not own the policy directly and has no incidents of ownership. This can provide liquidity to pay estate taxes without forcing the sale of other assets. For example, if an estate has significant illiquid assets like a family business or real estate, the proceeds from an ILIT can be used to cover estate tax obligations, preserving those other assets for the heirs.

- Grantor Retained Annuity Trusts (GRATs): GRATs allow you to transfer assets to beneficiaries while retaining the right to receive an annuity payment for a specified term. At the end of the term, the remaining assets in the trust pass to the beneficiaries with minimal gift or estate tax implications, especially if the assets appreciate significantly during the trust term. The success of a GRAT often depends on the growth of the underlying assets exceeding the IRS-defined interest rate.

- Spousal Lifetime Access Trusts (SLATs): SLATs are often used by married couples to take advantage of estate tax exemptions while still allowing the spouse who did not fund the trust (the beneficiary spouse) to potentially benefit from the trust assets during their lifetime. This offers a degree of flexibility while still removing assets from the taxable estate. The specific terms and conditions of SLATs are critical to their effectiveness.

Revocable Trusts

While revocable trusts do not typically reduce estate tax liability because the assets remain under the grantor’s control, they are invaluable for probate avoidance. Probate can be a costly and time-consuming process, and assets held in a revocable trust bypass it entirely. For Californians, avoiding probate is a significant benefit given the state’s probate fees, which are often calculated as a percentage of the estate’s value.

Lifetime Gifting Strategies

Strategic gifting during your lifetime can be an effective way to reduce the size of your taxable estate. By giving assets away, you deplete your estate and can utilize the annual gift tax exclusion or the unified credit.

Annual Gift Tax Exclusion

Each year, individuals can give a certain amount of money or assets to as many people as they wish without incurring any gift tax or using up their lifetime exemption. This annual exclusion amount is adjusted for inflation. Gifts made within this annual limit do not require filing a gift tax return and do not reduce the unified credit. This allows for systematic wealth transfer over time. For example, a grandparent could gift the annual exclusion amount to each of their grandchildren every year, significantly reducing their eventual taxable estate without incurring any immediate tax consequences.

Direct Payments for Education and Medical Expenses

Payments made directly to an educational institution for tuition or directly to a healthcare provider for medical expenses are not considered taxable gifts, regardless of the amount. This is an excellent way to provide for loved ones’ education or healthcare needs without impacting your gift or estate tax exemption. For instance, paying for a grandchild’s college tuition directly to the university or paying for a parent’s medical bills directly to the hospital are both considered exempt gifts.

Charitable Giving and Estate Planning

Charitable giving can be a powerful component of estate planning, offering both philanthropic satisfaction and tax benefits.

Charitable Remainder Trusts (CRTs)

A CRT allows you to transfer assets into a trust, receive an income stream for life or a term of years, and then have the remaining assets go to a designated charity. This can provide you with income during your lifetime and a potential income tax deduction when the trust is established, while also reducing your taxable estate.

Charitable Lead Trusts (CLTs)

Conversely, a Charitable Lead Trust provides income to a charity for a specified term, after which the remaining assets are distributed to your non-charitable beneficiaries. This can be structured to reduce the gift or estate tax liability on the assets passing to your heirs.

Life Insurance and Estate Liquidity

Life insurance can be a critical tool for providing liquidity to an estate, especially for larger estates that may face significant estate tax obligations.

The Role of Life Insurance

As mentioned with ILITs, life insurance can provide a tax-free death benefit that can be used to pay estate taxes, debts, or other expenses. This ensures that heirs are not forced to sell valuable assets at unfavorable times to meet these obligations. For example, if an estate owns a valuable piece of art or a valuable collectible, the heirs might not want to sell it. Having life insurance in place can provide the necessary funds to pay estate taxes without liquidating these cherished assets.

Business Succession Planning

For business owners, estate tax considerations can be particularly complex. Life insurance can be used to fund buy-sell agreements, ensuring that the business can continue to operate smoothly after the owner’s death and that the heirs receive fair value for their stake. This can prevent the business from being dismantled or sold off due to a lack of liquidity to cover estate taxes. Imagine a family-owned business, like a vineyard or a manufacturing company. If the owner passes away, the heirs might not be equipped to run the business. Life insurance can provide the funds for other heirs to buy out the business interest, or it can cover estate taxes, allowing the next generation to inherit and continue the legacy.

Navigating California’s Specific Landscape

While California does not have its own estate or inheritance tax, understanding its property tax laws, particularly Proposition 19, is crucial for estate planning. Additionally, consulting with experienced legal and financial professionals is paramount for navigating the complexities of estate tax avoidance.

Proposition 19 and Property Tax Transfers

California’s Proposition 19 significantly altered property tax rules regarding parent-child exclusions and transfers for individuals over 55 or with severe disabilities. Previously, parents could transfer their primary residence to their children without reassessment of property taxes. Proposition 19 has limited this exclusion, generally allowing for tax-free transfers only to children who will use the property as their primary residence. This change has implications for estate planning, as it can lead to higher property tax bills for heirs who inherit property in California but do not plan to live in it. This means that if parents were planning to pass on a valuable property to their children, and those children do not intend to make it their primary residence, the property will likely be reassessed at its current market value, leading to a substantial increase in property taxes. This is a critical factor to consider for Californians with real estate holdings.

Seeking Professional Guidance

Estate tax planning is a complex and ever-evolving field. Laws and regulations can change, and individual circumstances vary greatly. Therefore, it is highly recommended to consult with qualified professionals.

- Estate Planning Attorneys: An experienced estate planning attorney can help you draft wills, trusts, and other legal documents tailored to your specific needs and goals. They can advise on the best strategies for asset protection and tax minimization. Attorneys specializing in California estate law will be familiar with state-specific nuances, such as Proposition 19.

- Financial Advisors and CPAs: Financial advisors and Certified Public Accountants (CPAs) can assist with investment strategies, asset valuation, and the financial implications of various estate planning tools. They can help project future estate values and the potential tax liabilities.

By working with these experts, Californians can develop a comprehensive estate plan that not only aims to avoid or minimize potential “death taxes” but also ensures their assets are distributed according to their wishes, providing for their loved ones and leaving a lasting legacy. Planning ahead is key to protecting your wealth and ensuring peace of mind for yourself and your family. Remember, proactive planning is the most effective strategy when it comes to managing potential estate tax implications.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.