Navigating the complexities of real estate transactions can feel like planning a luxurious itinerary for a dream vacation to a destination as captivating as Paris or as serene as the Maldives. You’ve meticulously scouted the perfect boutique hotel in San Francisco, perhaps even a sprawling villa in Napa Valley, and the excitement of your new accommodation is palpable. Yet, just as you’re about to finalize your booking and anticipate the delectable local cuisine and enriching experiences, a new set of details emerges – the closing costs. In the Golden State of California, understanding who shoulders these often substantial expenses is as crucial as knowing the best time to visit Yosemite National Park or the most authentic street food stalls in Mexico City. This guide aims to demystify the often-opaque world of closing costs in California, ensuring your real estate journey, much like a well-planned luxury travel adventure, is smooth and predictable.

Closing costs represent a collection of fees and expenses incurred by both the buyer and the seller at the conclusion of a real estate transaction. These aren’t just minor administrative charges; they can add up to a significant percentage of the property’s purchase price, often ranging from 2% to 5%. For buyers, these costs can include loan origination fees, appraisal fees, title insurance, escrow fees, recording fees, and prepaid items like property taxes and homeowner’s insurance. For sellers, common closing costs involve real estate agent commissions, transfer taxes, escrow fees, and potential attorney fees. In California, as in many other states, the allocation of these costs is not rigidly fixed by law but is primarily determined through negotiation between the buyer and seller, influenced by market conditions and the specific terms of the purchase agreement.

The Buyer’s Burden: Understanding Common Buyer Closing Costs

When embarking on the exciting journey of purchasing a home, especially one as charming as a craftsman bungalow in Pasadena or a modern loft in Downtown Los Angeles, buyers typically assume a larger portion of the closing costs. These expenses are often tied to securing the financing and ensuring a clear title to the property, akin to securing the best room at the Grand Hyatt Hotel or booking an exclusive guided tour of Disneyland. Understanding these costs upfront allows buyers to budget effectively, just as one would budget for a once-in-a-lifetime family trip to Walt Disney World Resort or a sophisticated business stay in New York City.

Loan-Related Expenses

The most significant portion of a buyer’s closing costs often relates to obtaining a mortgage. These fees are paid to the lender for processing and approving the loan.

- Loan Origination Fee: This is a fee charged by the lender for processing the mortgage application. It’s typically a percentage of the loan amount, often around 0.5% to 1%. This is similar to a booking fee you might encounter when securing an unusual accommodation, like a unique treehouse or a remote cabin.

- Appraisal Fee: Lenders require an appraisal to determine the market value of the property. This ensures that the loan amount is not higher than the property’s worth, acting as a safeguard for both parties. The cost can range from $400 to $800 or more, depending on the property’s size and complexity.

- Credit Report Fee: Lenders pull your credit report to assess your creditworthiness. This fee covers the cost of obtaining your credit history.

- Discount Points: Buyers can choose to pay “points” upfront to lower their interest rate over the life of the loan. One point is equal to 1% of the loan amount. This is a strategic financial decision, much like investing in premium travel insurance for an extended safari in Kenya.

Title and Escrow Fees

These costs are essential for ensuring a clean and legal transfer of property ownership.

- Title Search and Title Insurance: A title company researches the property’s history to ensure there are no liens or encumbrances. Title insurance protects both the buyer and the lender against future claims on the title. The cost for this can be substantial, reflecting the importance of a clear title, just as a reputable tour operator is crucial for a safe and enjoyable trek in the Himalayas.

- Escrow Fees: An escrow company acts as a neutral third party, holding funds and documents until all conditions of the sale are met. Their fee is for managing this process, ensuring a fair exchange. This service is analogous to the role of a concierge at a high-end resort, coordinating all aspects of your stay.

- Recording Fees: The county recorder’s office charges a fee to record the deed and mortgage, making the transaction a matter of public record. This is a standard administrative step, much like registering your visa for international travel.

Prepaid Items and Reserves

Buyers are also typically responsible for prepaying certain expenses and setting aside reserves for future costs.

- Prepaid Property Taxes: Buyers often need to pay a prorated amount of property taxes from the closing date until the end of the tax year.

- Prepaid Homeowner’s Insurance: Lenders require proof of homeowner’s insurance, and buyers usually pay the first year’s premium at closing. This is akin to booking your travel insurance well in advance for a trip to a destination like New Zealand.

- Homeowner’s Association (HOA) Fees: If the property is part of an HOA, buyers may need to pay prorated dues or an initial capital contribution fee. This is especially common in communities with shared amenities, much like a condominium complex in Miami Beach with access to a private beach club.

The Seller’s Share: Common Seller Closing Costs

While buyers often bear the brunt of closing costs, sellers also have their financial responsibilities at the end of the transaction. These costs are typically associated with the sale of the property and ensuring a smooth transfer of ownership, much like preparing a property for guests at a luxury lodge in the Canadian Rockies.

Real Estate Agent Commissions

This is often the largest single expense for sellers.

- Real Estate Agent Commissions: Real estate agents, representing both the buyer and seller, typically earn a commission based on a percentage of the sale price. This commission is usually split between the buyer’s agent and the seller’s agent. This is a significant expense, comparable to the cost of hiring a professional planner for a large-scale event or a bespoke tour of ancient ruins in Egypt.

Transfer Taxes and Fees

These are government-imposed taxes related to the transfer of property ownership.

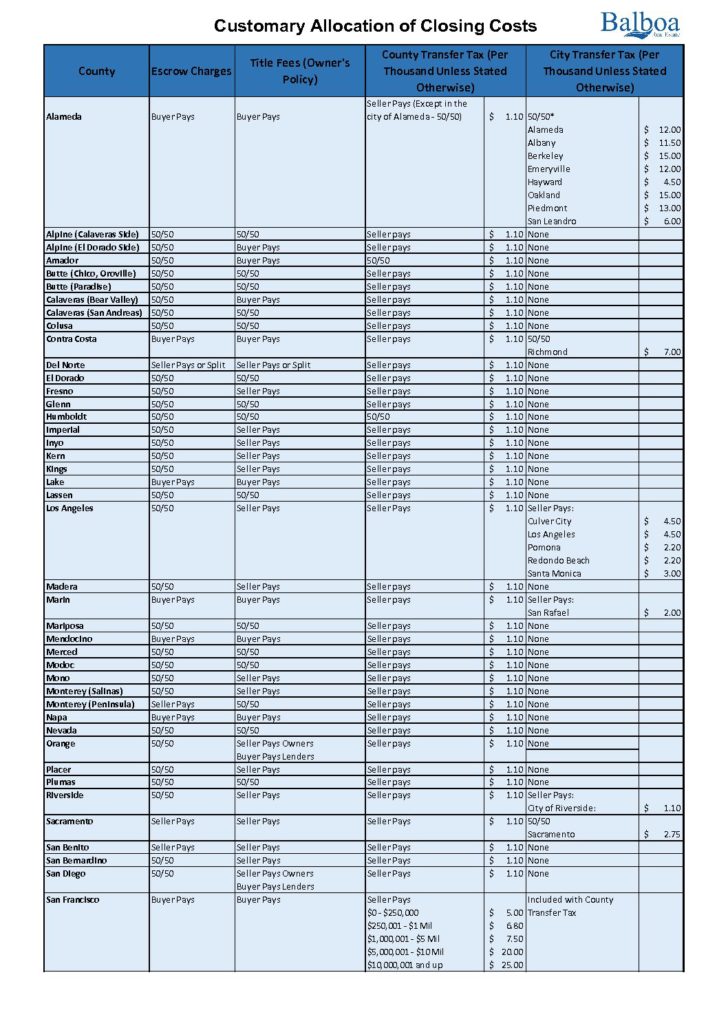

- Transfer Taxes: Many cities and counties in California impose transfer taxes on real estate transactions. These taxes are usually calculated based on the sale price of the property. The responsibility for paying these taxes can be negotiated, but traditionally, sellers bear this cost. This is a mandatory fee, much like airport taxes for international flights.

- Documentary Transfer Tax: This is a state-level tax levied on the transfer of real estate. The rate varies by county.

Escrow and Other Service Fees

Sellers may also incur escrow fees and other service-related costs.

- Escrow Fees: Similar to buyers, sellers also pay a portion of the escrow fees for the services provided by the escrow company in managing the closing process.

- Title Insurance (Owner’s Policy): While lenders require a lender’s policy, sellers sometimes opt to pay for the buyer’s owner’s title insurance policy as an incentive, particularly in a competitive market, much like including complimentary amenities in a hotel suite to attract guests.

- Attorney Fees: If the seller used an attorney for legal advice or to draft specific clauses in the contract, attorney fees would be an additional closing cost. This is often seen in complex transactions or when dealing with unique property situations, similar to seeking specialized advice before a long-term lease of a vacation rental in Hawaii.

- HOA Document Fees: If the property is in an HOA, sellers are responsible for providing various documents to the buyer, and there might be fees associated with obtaining these.

Negotiating Closing Costs: A Buyer and Seller’s Dance

In California, the negotiation of closing costs is a critical element of the real estate transaction, much like negotiating the price of a unique souvenir at a bustling market in Marrakech. While certain costs are standard, how they are divided between buyer and seller can vary significantly. Market conditions play a pivotal role; in a seller’s market, where demand outstrips supply, sellers have more leverage and may be less inclined to concede on closing cost contributions. Conversely, in a buyer’s market, buyers can often negotiate for sellers to pay a larger portion of their closing costs, potentially even contributing towards the buyer’s down payment.

The purchase agreement, the foundational document for the sale, outlines who is responsible for which closing costs. Buyers can request that sellers contribute a certain amount towards their closing costs. This can be a powerful negotiation tool, especially for buyers who might have stretched their budget for the property itself, similar to how a travel agent might offer a discount on excursions when booking a comprehensive resort package. Sellers might agree to this to make the deal more attractive or to close the sale faster, especially if the property has been on the market for an extended period, like a less popular flight route that requires incentives.

It’s crucial for both buyers and sellers to work with experienced real estate agents and escrow officers who can guide them through this negotiation process. They can advise on customary practices, market trends, and strategies to achieve a mutually agreeable outcome. Understanding these costs and having open communication can transform a potentially stressful closing period into a manageable step towards homeownership or a successful property sale, ensuring the entire experience is as seamless as a first-class flight to Tokyo.

Ultimately, who pays closing costs in California is a matter of negotiation, market dynamics, and the specifics of the real estate transaction. While buyers generally assume a larger share, sellers can be persuaded to contribute, particularly in a buyer-friendly market. A thorough understanding of these costs, coupled with effective communication and expert guidance, will pave the way for a successful and financially sound property transfer, allowing you to fully enjoy your new home or the fruits of your sale, much like savoring the last moments of a spectacular sunset cruise in Santorini.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.