For those enchanted by the allure of the Golden State—whether you dream of a sun-drenched second home in Palm Springs, a chic urban apartment in San Francisco, a sprawling vineyard estate in Napa Valley, or a tranquil cabin overlooking Lake Tahoe—understanding the intricacies of property tax is as crucial as finding the perfect resort. While our focus at Life Out Of The Box typically revolves around the thrill of travel, the luxury of accommodation, and the richness of lifestyle experiences, the financial landscape of property ownership in California often intertwines directly with these aspirations. Many of our readers contemplate extended stays, invest in vacation rentals, or even consider a permanent relocation to embrace the California dream. In such scenarios, property taxes are an undeniable, significant component of budgeting and financial planning.

The question, “When is California property tax due?” might seem straightforward, but it opens a deeper conversation about the fiscal responsibilities that come with enjoying the state’s unparalleled beauty and opportunities. This guide is designed to demystify the payment schedule, clarify various tax types, and provide essential insights for anyone looking to navigate the property market in California, ensuring your focus remains on savoring the unique lifestyle it offers rather than being blindsided by unexpected deadlines or charges. From the bustling streets of Los Angeles to the serene coastal towns, the rules of property tax are consistent, yet their impact can vary dramatically depending on your location and property type. By understanding these timelines, prospective buyers, current owners, and those planning long-term accommodations can approach their California ventures with confidence and clarity.

The California Property Tax Calendar: Key Dates for Homeowners and Investors

Navigating the property tax landscape in California begins with a clear understanding of the annual calendar. Unlike some states with a single annual payment, California operates on a semi-annual schedule for its regular property tax, complemented by additional assessments for new property owners or new construction. Missing these deadlines can result in significant penalties, adding an unnecessary burden to your investment or living costs. Therefore, whether you’re considering a luxury villa in Malibu or a charming bungalow in San Diego, marking these dates on your calendar is paramount.

Understanding the Annual Property Tax Cycle

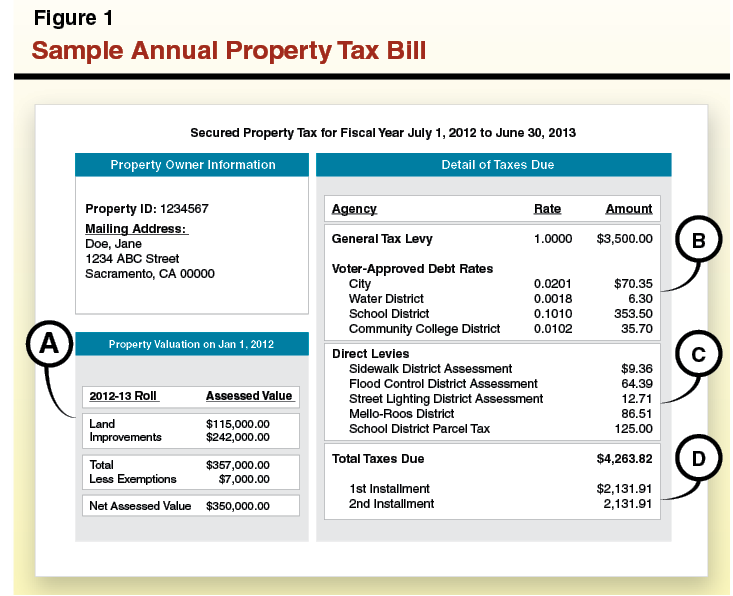

The California property tax system is based on a fiscal year that runs from July 1 to June 30 of the following year. However, the assessment date—the day your property’s value is determined for the upcoming tax year—is actually January 1 of the preceding calendar year. For example, the taxes you pay in the fiscal year July 1, 2024, to June 30, 2025, are based on your property’s value as of January 1, 2024.

The process generally unfolds as follows:

- January 1: This is the lien date, the official assessment date for the property’s value that will be used for the upcoming fiscal year’s property taxes.

- July 1: The new fiscal year officially begins. At this point, the assessed values are typically finalized, and counties begin preparing tax bills.

- September / October: Property tax bills are usually mailed out by county tax collectors during these months. It’s crucial to note that even if you don’t receive a bill, the responsibility for timely payment remains yours. If you haven’t received your bill by late October, it is highly recommended to contact your county tax collector’s office.

The Semi-Annual Payment Schedule

Once your property tax bill arrives, you’ll notice it’s divided into two installments. These are the fixed, predictable deadlines that every California property owner must adhere to.

-

First Installment:

- Due Date: November 1

- Delinquent After: December 10, at 5:00 PM. If December 10 falls on a weekend or holiday, the deadline is extended to the next business day.

- A 10% penalty is applied to any payment received after the delinquency date.

-

Second Installment:

- Due Date: February 1

- Delinquent After: April 10, at 5:00 PM. Similarly, if April 10 falls on a weekend or holiday, the deadline shifts to the next business day.

- A 10% penalty plus a $30 cost is applied to any payment received after the delinquency date.

Understanding these two critical deadlines is the cornerstone of managing your property taxes effectively in California. For many homeowners, especially those with mortgages, these payments are often handled through an escrow account by their lender. However, it is always wise to confirm this arrangement and monitor your property tax statements to ensure payments are made on time.

Supplemental Taxes: What New Buyers Need to Know

Beyond the regular annual property tax, California has a unique system called “supplemental assessments” that can catch new buyers off guard. This system comes into play whenever there’s a “change in ownership” or “new construction” on a property.

Here’s how it works:

When you purchase a property, the Assessor reassesses its value to reflect the current market price. If this new assessed value is higher than the previous owner’s assessed value, a supplemental assessment is generated. This supplemental tax covers the difference in tax between the old and new assessed values for the remainder of the fiscal year, from the date of the change in ownership until the following June 30.

- Calculation: The supplemental tax is calculated based on the difference between the prior assessed value and your new purchase price (or new construction value), prorated for the number of months remaining in the fiscal year.

- Billing: You will receive a separate supplemental tax bill, which is not part of your regular annual tax bill and is not typically paid through escrow. These bills can arrive at any time of the year, often several months after your purchase, and usually have two installment due dates, similar to the annual bill, but specifically for the supplemental amount. The first installment is due on the date the bill is mailed, and the second is due a few months later.

- Importance for New Owners: For those investing in a luxury vacation home in Santa Barbara or a long-term rental property in Orange County, budgeting for these supplemental taxes is critical. They represent an additional, often unexpected, cost that must be factored into your initial financial planning. Ignoring these bills can lead to the same penalties as regular property taxes.

Being aware of the supplemental tax system ensures that new buyers can account for all potential property-related expenses, providing a smoother transition into California property ownership.

Property Tax in California’s Premier Destinations: What It Means for Your Lifestyle and Investments

The allure of California lies in its diverse landscapes, vibrant cities, and unparalleled lifestyle opportunities. From the glitz of Beverly Hills to the natural splendor of the Redwood Coast, owning property here is a dream for many. However, the dream comes with financial realities, and property tax is a major component. Understanding how it impacts your lifestyle choices and investment strategies in various California destinations is essential for smart decision-making.

Investing in California Real Estate: Vacation Rentals and Second Homes

California’s tourism appeal makes it fertile ground for vacation rental investments and second homes. Imagine owning a beachfront condo in Laguna Beach, a desert oasis near Joshua Tree National Park, or a ski retreat in Mammoth Lakes. These properties not only offer personal enjoyment but also potential income streams.

When considering such investments, property taxes are a critical line item in your budget:

- Cost of Ownership: High property values in desirable areas like Santa Monica, La Jolla, or Pebble Beach mean higher property tax bills. While California’s base property tax rate is around 1% of the assessed value, additional local levies and bond measures can push the effective rate higher, sometimes to 1.25% or even 1.5% in some communities. This significantly impacts your overall carrying costs.

- Return on Investment (ROI): For vacation rentals, property taxes directly reduce your net rental income. A comprehensive financial model for any investment property must accurately project these tax expenses alongside mortgage payments, insurance, maintenance, and property management fees. Investors in popular tourist areas such as Anaheim (near Disneyland) or Hollywood must factor in these costs to ensure their venture remains profitable.

- Lifestyle Considerations: For second home owners, these taxes are an ongoing expense, regardless of how often you use the property. Budgeting for these annual costs allows you to fully enjoy your California retreat without financial strain, whether it’s a quiet getaway in Carmel-by-the-Sea or an active lifestyle in Truckee.

Long-Term Stays and Relocation: Budgeting for the California Dream

For those contemplating an extended stay that moves beyond hotel accommodations, or even a full relocation to California, property taxes become an integral part of your overall cost of living. The dream of living the California lifestyle—be it surfing in Huntington Beach, exploring the tech scene in San Jose, or enjoying the state capital in Sacramento—requires careful financial planning.

- Regional Variations: While the state’s property tax rules are uniform, the amount you pay varies significantly by region due to differing property values. A luxury home in Bel Air will naturally incur far higher property taxes than a comparable property in a less expensive inland community. Researching the local tax rates and average property values in your desired cities is vital.

- Total Cost of Living: Property taxes contribute significantly to your monthly housing expenses, alongside mortgage, utilities, and homeowners association (HOA) fees. Understanding this full financial picture is crucial when comparing lifestyle options, such as renting a high-end apartment versus purchasing a home. For instance, a long-term stay in a furnished luxury apartment might negate property tax concerns, but for someone buying a vacation property in Sonoma County, these taxes are a fixed annual commitment.

- Lifestyle Impact: High property taxes can influence the size or location of the property you can afford, directly impacting your chosen lifestyle. Savvy planning ensures you can live comfortably and sustainably, whether your dream involves a sprawling estate with ocean views or a vibrant urban loft.

The Impact of Proposition 13 on California Property Values and Taxes

No discussion of California property tax is complete without mentioning Proposition 13, a landmark amendment passed in 1978. Prop 13 fundamentally reshaped property taxation in the state and continues to have profound implications for homeowners and investors.

Here are its key provisions:

- Assessed Value Cap: Property taxes are capped at 1% of the property’s 1975 assessed value or its subsequent purchase price. This means your base tax amount is essentially set at the price you paid for the property.

- Annual Increase Limit: The assessed value of a property can increase by no more than 2% per year, even if the market value rises significantly faster. This provides long-term homeowners with predictable and relatively stable tax bills, protecting them from rapid increases in property values.

- Reassessment Upon Change of Ownership: The primary exception to the 2% cap is a change in ownership. When a property is sold, it is reassessed to its current market value, and the new owner’s tax base is reset to the purchase price. This is why new buyers often face significantly higher property tax bills than long-time residents in the same neighborhood.

- New Construction Reassessment: Similarly, new construction on a property will trigger a reassessment for the value added by that construction.

Prop 13 has created a dual-track system where long-term homeowners often pay substantially less in property taxes than new buyers for comparable properties. For investors considering properties in highly appreciated markets like Silicon Valley or trendy neighborhoods in Oakland, understanding that your tax liability will be based on the full purchase price, not a lower historical value, is crucial. It directly affects the profitability of investment properties and the affordability of homes for those new to the California market.

Navigating Property Tax Resources and Maximizing Your California Experience

Successfully managing property taxes in California is not just about knowing the due dates; it’s also about understanding where to find accurate information, how to make payments, and how these taxes fit into the broader financial picture of living or investing in the state. For those looking to fully embrace the travel, tourism, and lifestyle aspects California has to offer, a proactive approach to financial planning ensures a smooth and enjoyable experience.

Official Resources and Payment Methods

The most reliable source of information regarding your specific property tax obligations is your local County Tax Collector and County Assessor’s Office. Each of California’s 58 counties has its own dedicated departments responsible for assessing property values and collecting taxes.

- County Websites: Every county maintains a website where you can look up your property’s assessed value, view your current tax bill, and find detailed information about payment options and deadlines. Simply search for “[Your County Name] Tax Collector” or “[Your County Name] Assessor.” For example, if you own property in San Francisco, you would visit the City and County of San Francisco Office of the Treasurer & Tax Collector website.

- Payment Methods: Most counties offer several convenient ways to pay:

- Online: This is often the easiest and most preferred method, allowing you to pay with a credit card (often with a convenience fee) or an e-check (usually free or low fee).

- Mail: You can always mail a check with your payment coupon. Ensure it is postmarked by the due date to avoid penalties.

- In Person: Many county tax collector offices allow in-person payments, which can be useful if you prefer direct interaction or need assistance.

- Phone: Some counties offer payment by phone, typically with a credit card.

- Monitoring Your Bill: Even if your property taxes are handled by your mortgage lender through an escrow account, it’s advisable to periodically check your county’s tax collector website or confirm with your lender that payments are being made on time. If you do not receive a tax bill by October each year, contact your county tax collector immediately. The absence of a bill does not excuse you from payment obligations or penalties.

Beyond Taxes: The Full Cost of California Living and Investing

While property taxes are a significant expense, they are just one piece of the financial puzzle when buying or living in California property. To truly maximize your California experience, especially if it involves long-term stays or investment, consider the broader financial landscape:

- Homeowners Association (HOA) Fees: Many properties, especially condos, townhouses, and homes within planned communities, come with HOA fees. These fees cover common area maintenance, amenities (like pools, gyms, security), and sometimes even utilities. HOAs are prevalent in high-amenity areas such as the gated communities of Rancho Santa Fe or the luxury high-rises in Downtown Los Angeles. These fees can be substantial and are a recurring monthly cost.

- Special Assessments (Mello-Roos): In many newer developments across California, especially in rapidly growing areas like parts of Riverside County or Placer County, you might encounter Mello-Roos Community Facilities Districts (CFD) taxes. These are additional property taxes levied to finance specific public improvements, such as roads, schools, parks, and utilities within the district. Mello-Roos taxes can significantly increase your overall property tax burden and are not subject to Proposition 13 limits. Always inquire about these during the property purchase process.

- Homeowner’s Insurance: Given California’s unique geography, insurance costs can be higher, especially for properties in wildfire-prone areas or coastal zones susceptible to flooding. This is an essential cost to research early.

- Maintenance and Utilities: Ongoing maintenance, repairs, and utility costs for a property, whether it’s a primary residence or a vacation rental, need to be factored in. For luxury properties, these costs can be substantial to maintain the desired standard.

- Income Taxes on Rental Properties: If you’re investing in vacation rentals, remember that any rental income is subject to federal and state income taxes. Understanding allowable deductions and tax liabilities is crucial for an accurate ROI calculation.

By taking a holistic view of all potential costs associated with property ownership or long-term stays in California, you can make informed decisions that align with your financial goals and lifestyle aspirations. This comprehensive budgeting approach allows you to fully immerse yourself in the wonders of California, from its world-class attractions and stunning natural landmarks to its vibrant local culture and diverse culinary scene, without financial surprises.

In conclusion, knowing “When is California property tax due?” is more than just remembering a date; it’s about understanding a critical aspect of engaging with the state’s real estate market. Whether you’re an aspiring investor eyeing a vacation rental, a traveler planning an extended stay, or someone dreaming of calling California home, a firm grasp of property tax deadlines, supplemental assessments, and the broader financial landscape is indispensable. By diligently managing these fiscal responsibilities, you can ensure your journey through the Golden State remains focused on the extraordinary experiences and the unparalleled lifestyle that make California truly unique.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.