Navigating the intricacies of state taxation can often feel like deciphering a complex map, especially when you’re exploring the diverse landscapes of travel, accommodation, and lifestyle choices. For those residing in or visiting the Golden State, understanding the California Use Tax is a crucial piece of this financial puzzle. While many are familiar with sales tax, the use tax often remains a less understood, yet equally important, component of California’s fiscal policy. It’s not just for businesses; individuals, including travelers and tourists, can find themselves subject to this tax under certain circumstances.

This article delves into the core aspects of California Use Tax, explaining what it is, why it exists, and how it impacts consumers, businesses, and even visitors who might purchase goods outside the state and bring them back to their California base. Whether you’re furnishing a new short-term rental property, acquiring souvenirs during an out-of-state trip, or simply making online purchases, a clear grasp of this tax can help you manage your financial responsibilities and avoid unexpected costs.

Understanding California Use Tax: The Basics

At its heart, the California Use Tax is a companion to the state’s sales tax. Its primary purpose is to ensure fair taxation and prevent residents and businesses from bypassing sales tax by purchasing goods from out-of-state retailers who do not collect California sales tax. Think of it as a compensatory tax that applies when a sale occurs outside California’s jurisdiction, but the purchased item is subsequently stored, used, or consumed within the state.

The California Department of Tax and Fee Administration (CDTFA) is the state agency responsible for administering sales and use taxes. According to the CDTFA, use tax is imposed on the retail sale of goods for storage, use, or other consumption in California, even if the sale itself happens outside the state. The critical distinction lies in who is responsible for collecting and remitting the tax. With sales tax, the seller collects it from the buyer and sends it to the state. With use tax, if the seller doesn’t collect it, the buyer is directly responsible for paying it to California.

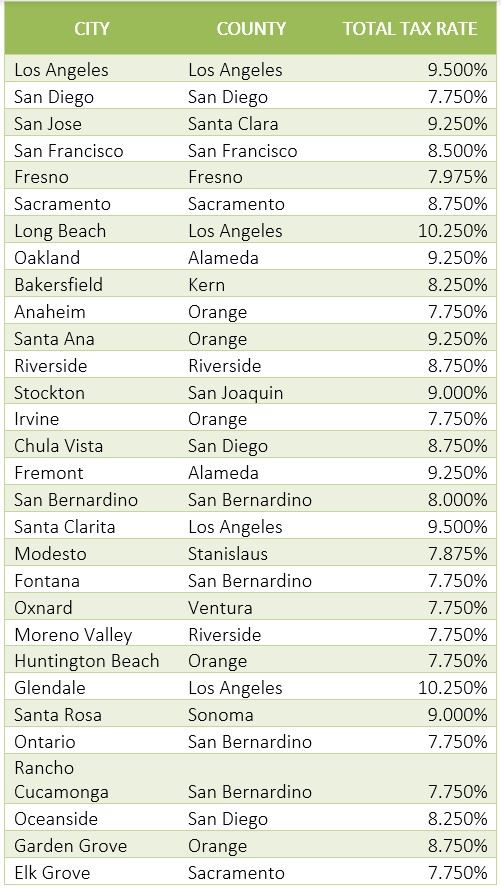

The use tax rate is identical to the sales tax rate in the location where the item is used or consumed. This rate varies across California, typically ranging from 7.25% to over 10% depending on local district taxes. For example, a purchase made for use in Los Angeles County would be subject to the Los Angeles County sales and use tax rate, while a similar item intended for San Francisco would follow that city’s rate. This localized approach ensures that local municipalities and transit districts receive their fair share of revenue, regardless of where the initial transaction took place.

Why Does California Have a Use Tax?

The existence of a use tax might seem like an added layer of complexity, but it serves several vital functions within California’s economic framework. Fundamentally, it’s about fairness and revenue.

Firstly, the use tax creates a level playing field for California businesses. Imagine a scenario where a consumer could simply purchase goods from an online retailer based in Oregon (a state with no sales tax) or Nevada (with a lower sales tax rate) and avoid paying any tax when bringing the item into California. This would put local California businesses, which are legally obligated to collect California sales tax, at a significant competitive disadvantage. The use tax eliminates this incentive, ensuring that all goods consumed in California contribute equally to the state’s revenue, regardless of where they were purchased. This protects local economies, including the vibrant tourism and hospitality sectors found in cities like San Diego or popular travel destinations like Napa Valley, where local shops and boutiques rely on sales tax revenue.

Secondly, the use tax is a critical revenue generator for state and local services. Funds collected through sales and use taxes support a wide array of public services, including education, infrastructure, public safety, and health programs. For travelers, this translates into well-maintained roads leading to iconic landmarks like the Golden Gate Bridge, accessible public transportation in urban centers, and the preservation of natural wonders such as Yosemite National Park. Without the use tax, a substantial portion of revenue from out-of-state purchases would be lost, potentially impacting the quality and availability of these essential services that enhance the overall California experience for residents and tourists alike.

Sales Tax vs. Use Tax: Clarifying the Distinction

While intimately related, it’s crucial to distinguish between sales tax and use tax, as they dictate different responsibilities for buyers and sellers. Understanding this difference is key to proper tax compliance, whether you’re a long-term resident or enjoying a temporary stay in a California resort.

Sales tax is typically imposed on the retailer for the privilege of selling tangible personal property at retail. The retailer then passes this tax on to the consumer as part of the purchase price. When you buy a souvenir from a shop in Hollywood, a bottle of wine in Napa Valley, or groceries from a supermarket in Sacramento, you pay sales tax to the merchant, who then remits it to the CDTFA. This is the most common form of transaction tax people encounter daily.

Use tax, on the other hand, is imposed directly on the purchaser. It applies when you acquire goods from a seller who is not required to collect California sales tax, but you intend to use, store, or consume those goods within California. The seller might be located in another state, or perhaps they don’t have enough of a “nexus” (physical or economic presence) in California to be legally obligated to collect California sales tax. In these situations, the responsibility shifts from the seller to the buyer to report and pay the use tax.

The Role of Nexus in Online Shopping

The rise of e-commerce has significantly shaped the landscape of sales and use tax. Historically, a seller only had to collect sales tax if they had a physical presence (a “nexus”) in the state where the buyer was located, such as a store, office, or warehouse. This meant that many online purchases from out-of-state vendors didn’t include California sales tax. However, the landmark 2018 Supreme Court case South Dakota v. Wayfair changed this, allowing states to require out-of-state sellers to collect sales tax even without a physical presence, based on economic activity (economic nexus).

Today, most major online retailers like Amazon, eBay, Walmart, and Target that frequently ship to California customers now collect California sales tax on their transactions. This is because their sales volume or number of transactions into California meets the economic nexus threshold, obligating them to collect the tax. When these retailers collect the tax, you’re essentially paying the sales tax at the point of purchase, fulfilling your tax obligation.

However, use tax still applies in situations where a seller doesn’t collect sales tax. This could be smaller online retailers, individual sellers on marketplaces, or even larger companies that might not meet the nexus requirements for all states. For instance, if you purchase a piece of custom artwork from a gallery in New York and have it shipped to your California apartment, and the New York gallery doesn’t collect California sales tax, then you, as the buyer, would be responsible for reporting and paying the California Use Tax.

When and How California Use Tax Applies

The application of California Use Tax extends beyond simple online purchases, touching various scenarios that might be relevant to your lifestyle, travel, and business activities within the state.

Out-of-State Purchases Brought into California

This is a common scenario, particularly for travelers. Imagine you’re on a road trip through neighboring states like Oregon, which has no sales tax, or Nevada, which has a lower sales tax rate than California. If you purchase significant items – say, electronics, furniture for your California home, or even expensive clothing – and bring them back for use in California, you are liable for California Use Tax.

The intent is crucial here: if the item is bought specifically for use in California, the tax applies. For example, if you visit Las Vegas and buy a new television for your living room back in San Diego, and Nevada’s sales tax was less than California’s, you would owe the difference in use tax to California. If no sales tax was paid at all, such as in Oregon, you would owe the full California rate.

Business Purchases and Operations

For businesses operating in California, the use tax is a routine part of financial management. Hotels, for instance, might purchase furniture, linens, or amenities from out-of-state suppliers. If these suppliers do not collect California sales tax, the hotel (e.g., a Grand Hyatt Hotel or a Marriott International property) is responsible for reporting and paying use tax on those purchases. Similarly, a tourism company buying new fleet vehicles from a dealer in Arizona would need to consider use tax if the vehicles are intended for use on California roads and the Arizona dealer didn’t collect the appropriate California tax.

This also applies to less tangible items like software licenses purchased from out-of-state vendors for use in California business operations, if they qualify as tangible personal property under California tax law. Accurate tracking of such purchases is essential for businesses to remain compliant with state tax regulations and avoid penalties.

Gifts, Inheritances, and Special Circumstances

While less common, use tax can also apply to items received as gifts or through inheritance if they were originally purchased out-of-state without California sales tax being paid, and are then brought into California for use. There are nuances and specific conditions that apply here, and it’s always advisable to consult the CDTFA guidelines or a tax professional for clarity in such situations.

Certain specific items, like vehicles, vessels, and aircraft, have their own reporting mechanisms for use tax, often collected during registration with the Department of Motor Vehicles or other relevant agencies. When someone moves from a state like Washington (which has sales tax, but potentially a different rate) to California and brings their car, they might owe use tax if no sales tax was paid or if the sales tax paid in the previous state was less than California’s rate, and the vehicle was purchased within 12 months of becoming a California resident.

Navigating Use Tax for Travelers, Businesses, and Residents

Understanding how use tax impacts different groups is crucial for effective planning and compliance. The requirements and reporting methods can vary based on whether you’re an individual consumer, a business owner, or a visitor to the state.

For Individual Consumers and Residents

For the average California resident, the most common encounter with use tax comes from online purchases where the seller didn’t collect sales tax or from out-of-state purchases brought back into California. The state provides a straightforward way for individuals to report and pay use tax: through their annual California income tax return, specifically Form 540. There’s usually a line item where you can declare your total purchases subject to use tax. For smaller amounts, taxpayers can often estimate a safe harbor amount, but for larger purchases, accurate calculation is necessary.

It’s important to keep receipts for any significant purchases made out-of-state or online, especially if no sales tax was collected. This documentation can be vital if your tax filing is ever questioned. Responsible tax habits are part of a broader lifestyle choice, ensuring you contribute to the state’s welfare while enjoying all it has to offer, from the beaches of Big Sur to the slopes of Lake Tahoe.

For Businesses and the Hospitality Sector

Businesses, from small boutiques in Santa Monica to large hotel chains like Hilton Worldwide or The Ritz-Carlton, have more rigorous reporting requirements. They typically file sales and use tax returns with the CDTFA on a monthly, quarterly, or annual basis, depending on their sales volume. These returns include both sales tax collected from customers and use tax owed on purchases made by the business itself where sales tax wasn’t paid.

For the accommodation sector, this means meticulously tracking purchases of everything from linens and furniture to cleaning supplies and technology if acquired from out-of-state vendors without California sales tax. For a resort planning a major renovation, procuring materials and fixtures from suppliers across the United States could easily trigger substantial use tax liabilities. Proper accounting procedures and integration of use tax considerations into procurement policies are essential to ensure compliance and avoid audits or penalties. Businesses that fail to adequately report and pay use tax can face significant fines and interest charges, highlighting the importance of professional accounting and tax advice.

For Travelers and Tourists

While tourists generally spend their money on experiences, dining, and local attractions, they too can encounter use tax if they make certain purchases. If you visit California and buy an expensive item from an out-of-state online retailer to be shipped directly to your hotel in Anaheim (perhaps near Disneyland), and that retailer doesn’t collect California sales tax, you could technically be liable for use tax. Similarly, if you’re a California resident returning from an international trip with goods that exceed duty-free limits and haven’t had California sales tax applied, use tax could be due.

However, for most common tourist purchases—souvenirs, meals, attraction tickets—sales tax is collected at the point of sale by local California businesses, so use tax typically isn’t a concern. The primary scenario for travelers to be aware of use tax is when they engage in substantial out-of-state purchases intended for use within California and sales tax wasn’t collected. While the CDTFA doesn’t typically pursue small use tax liabilities from transient tourists, it’s part of the broader legal framework that underpins the state’s economy.

Reporting and Paying California Use Tax

The process for reporting and paying California Use Tax is streamlined, especially for individual consumers. Transparency and diligence are key to fulfilling this obligation.

For Individuals: On Your Income Tax Return

For individual residents, the simplest and most common method to pay use tax is by reporting it on their annual California income tax return, specifically Form 540. The CDTFA and the Franchise Tax Board (FTB) collaborate on this, making it a relatively integrated process. The income tax return typically has a line where you can enter the total amount of untaxed purchases made during the year. The tax due is then calculated and added to your overall state tax liability or deducted from your refund.

The CDTFA provides resources and guidance on how to calculate this amount, including a “Use Tax Calculator” on their website for assistance. It is highly recommended to keep records of purchases subject to use tax, including invoices and receipts, for at least four years, as this aligns with common audit periods.

For Businesses: Sales and Use Tax Returns

Businesses registered with the CDTFA are required to file regular sales and use tax returns. On these returns, businesses report the sales tax they collected from their customers, as well as the use tax owed on any purchases they made for their own use that were not subject to California sales tax. These filings are crucial for maintaining good standing with the state and ensuring all tax obligations are met.

Large purchases, such as significant equipment or property for a new hotel development, might warrant direct contact with the CDTFA to ensure proper reporting and payment. Businesses often have dedicated accounting teams or external tax consultants who manage these complex filings, reflecting the critical nature of compliance in the business world.

Exceptions and Credits

It’s important to note that you generally won’t owe California Use Tax if you paid sales tax to another state, and that sales tax rate was equal to or greater than California’s rate. If the out-of-state sales tax paid was less than what would have been owed in California, you would only owe the difference. For example, if you bought an item in Texas where the sales tax rate is 6.25% and brought it to California where your local rate is 8.25%, you would owe 2% use tax to California.

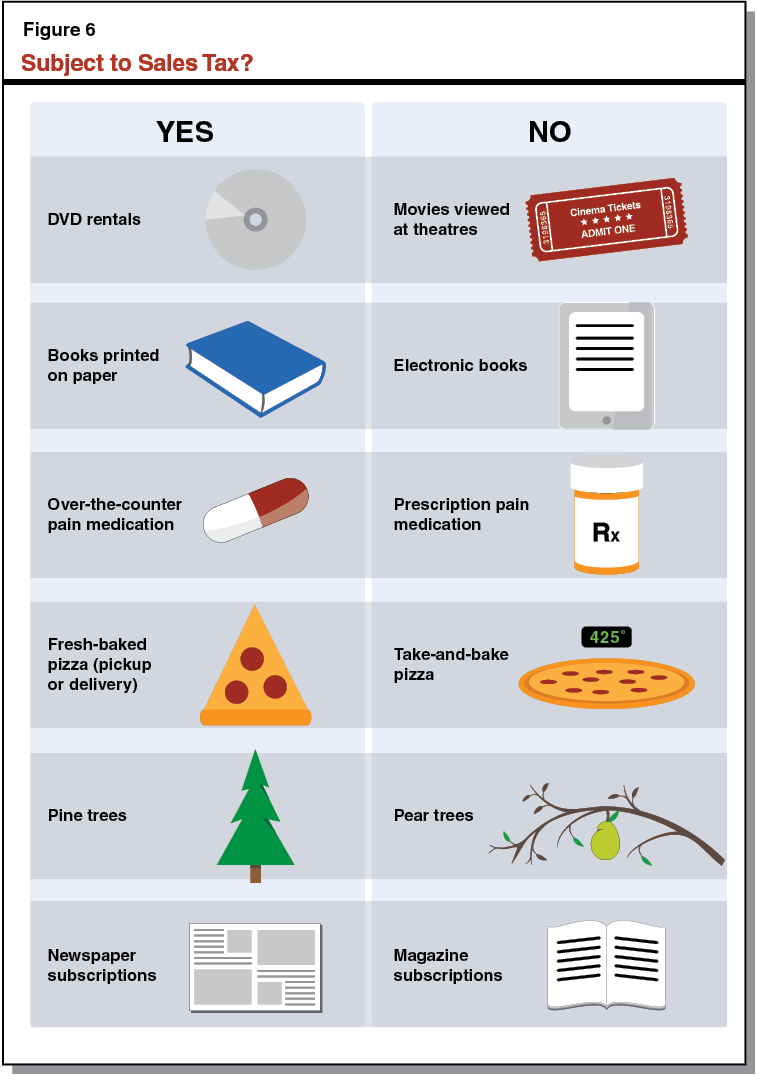

Additionally, certain items are exempt from sales and use tax entirely, such as food products for home consumption, prescription medicines, and certain publications. Items purchased for resale by a business are also exempt from use tax, as the sales tax will be collected when the item is eventually sold to an end consumer. Understanding these exceptions is crucial for accurate tax planning and compliance.

In conclusion, while the California Use Tax might seem like a niche concept, it plays a vital role in the state’s economy and affects a wide range of individuals and businesses. From ensuring fair competition for local shops and resorts to funding essential public services, its impact is far-reaching. By understanding its purpose, when it applies, and how to report it, you can confidently navigate your financial responsibilities in the Golden State, whether you’re building a business empire, enjoying a luxury travel experience, or simply living your daily life. Staying informed about tax regulations like the California Use Tax is an integral part of a responsible and informed lifestyle, allowing you to focus on the myriad experiences and opportunities that California has to offer.