For anyone considering a move, investing in a vacation home, or simply managing their existing property in the diverse and vibrant landscape of New York State, understanding the intricacies of property taxes is paramount. From the bustling streets of New York City to the tranquil beauty of the Adirondacks or the serene vineyards of the Finger Lakes, property ownership offers unparalleled opportunities for lifestyle enrichment, travel, and investment. However, these benefits come with responsibilities, not least among them the timely payment of property taxes. A common, and indeed critical, question that arises for homeowners and prospective buyers alike is: Does New York State charge interest on back property taxes? The unequivocal answer is yes, and understanding the implications of these charges is essential for maintaining financial well-being and protecting your investment. Ignoring these details can quickly turn a dream property into a source of significant financial stress, potentially impacting your ability to enjoy the very lifestyle and travel experiences you sought in New York.

The Fundamentals of Property Taxes in New York State

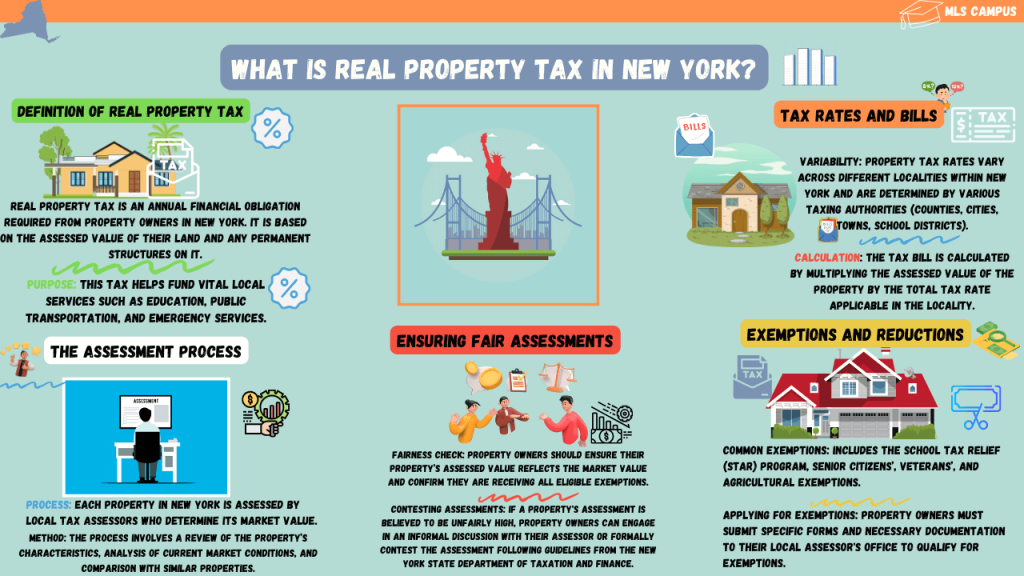

Property taxes in New York State are not collected by the state itself, but rather by various local governmental units. This decentralized system means that the rules, due dates, and even the specific interest rates and penalties can vary significantly depending on where your property is located. Whether you own a luxury apartment in Manhattan, a charming historic home in the Hudson Valley, or a picturesque lakeside cabin in Upstate New York, your property tax obligations will be determined by the county, town, city, village, and school district in which your property resides. This local control emphasizes the importance of understanding your specific municipality’s tax calendar and policies.

Who Collects Property Taxes in New York?

The primary collectors of property taxes are typically county treasurers, town or city tax collectors, and school district officials. Each of these entities levies taxes based on the assessed value of your property and their respective tax rates, which fund local services like schools, roads, police, and fire departments. For instance, in New York City, the Department of Finance manages property tax collections across all five boroughs, including Brooklyn, Queens, the Bronx, and Staten Island. In contrast, a property owner in a rural part of Long Island might deal with their town’s tax receiver and a separate school district office.

The assessment process, which determines your property’s value for tax purposes, is usually handled by local assessors. They evaluate properties based on market value, improvements, and other factors. It’s crucial for property owners to understand their assessment and appeal it if they believe it’s inaccurate, as this directly impacts their tax bill. Missing the deadline to appeal could mean paying higher taxes than necessary for the entire tax year, affecting your budget for future travel or lifestyle enhancements.

The Annual Tax Cycle

Property tax bills are typically issued annually, though some municipalities might offer semi-annual or quarterly payment options. The due dates vary widely. For example, some counties might have property taxes due in January, while school taxes might be due in September. It’s imperative to mark these dates on your calendar or set up automatic reminders. Many municipalities now offer online payment portals, making it easier than ever to ensure timely payments from anywhere in the world, whether you’re enjoying a European tour or a relaxing beach vacation in the Caribbean.

Understanding this localized system is the first step in avoiding the pitfalls of delinquent taxes. A proactive approach to managing your property tax obligations ensures that your investment remains secure and your financial plans for travel and leisure aren’t disrupted by unforeseen penalties.

Understanding Interest and Penalties for Delinquent Taxes

When property taxes in New York State are not paid by the specified due date, they are considered delinquent. Once a tax bill becomes delinquent, the charging of interest and penalties is standard practice across virtually all local jurisdictions. This isn’t just a minor inconvenience; these charges can accumulate rapidly, significantly increasing the total amount owed and potentially jeopardizing your property ownership.

How Interest Rates Are Determined

The specific interest rates and penalty structures are determined at the local level by county legislatures, city councils, or town boards. There isn’t a single, uniform state-mandated rate that applies to all municipalities. However, general patterns exist:

- Monthly Interest: Many localities impose interest at a rate of 1% to 1.5% per month or fraction thereof that the taxes remain unpaid. This means if you are even a few days late into the next month, you could incur another full month’s interest. This compounding effect can lead to a substantial increase in your debt over time.

- Initial Penalty: In addition to monthly interest, some municipalities may levy an initial penalty or a flat late fee immediately after the due date passes. This could be a fixed dollar amount or a percentage of the unpaid tax, typically ranging from 2% to 5%.

- Accelerated Rates: For taxes that remain delinquent for an extended period (e.g., six months or a year), some jurisdictions may increase the monthly interest rate or add further penalties. For instance, a common structure might be 1% per month for the first six months, escalating to 1.25% or 1.5% per month thereafter.

Consider a homeowner with a $5,000 property tax bill. If it’s 3 months late at an interest rate of 1% per month plus a 5% initial penalty:

- Initial Penalty: $5,000 * 0.05 = $250

- Month 1 Interest: ($5,000 + $250) * 0.01 = $52.50

- Month 2 Interest: ($5,250 + $52.50) * 0.01 = $53.03

- Month 3 Interest: ($5,303.03 + $53.03) * 0.01 = $53.56

- Total owed after 3 months (approximately): $5,409.12

This example illustrates how quickly the principal amount can grow, making it more challenging to catch up. This financial strain can force you to re-evaluate planned trips to Europe or delay booking that luxury suite you’ve been eyeing.

Notification of Delinquency

While it is ultimately the homeowner’s responsibility to know and meet tax deadlines, municipalities typically send reminder notices for upcoming due dates and subsequent delinquency notices if taxes remain unpaid. However, relying solely on these notices is not advisable, as postal delays or changes in mailing addresses could lead to missed communications. It’s always best to proactively confirm your tax status and due dates directly with the local tax collector’s office or via their official website. Many offices in New York, including those in Albany and other major cities, offer user-friendly online platforms for checking tax balances and payment history.

Consequences of Non-Payment: Beyond Just Interest

The accumulation of interest and penalties is just one facet of the consequences of failing to pay property taxes in New York State. For homeowners, the long-term implications can be severe, potentially leading to the loss of their property. For those who view their New York property as an investment or a lifestyle choice, these consequences underscore the critical importance of financial vigilance.

Tax Liens and Tax Sales

When property taxes remain delinquent for a significant period (which can range from one to three years, depending on the municipality), local governments have the authority to enforce collection by placing a tax lien on the property. A tax lien is a legal claim against your property, effectively a cloud on your title, which indicates that taxes are owed. This lien then allows the municipality to eventually sell the tax debt or the property itself to recover the unpaid taxes.

- Sale of Tax Liens: In many New York counties, the municipality will sell these tax liens to third-party investors. These investors pay the delinquent tax amount to the county and, in return, acquire the right to collect the debt from the homeowner, often with additional interest and fees that can be higher than the initial municipal rates. This process creates a new creditor who will pursue payment aggressively.

- Tax Foreclosure or Tax Deed Sales: If the tax lien remains unpaid for an extended period after its sale, the lienholder or the municipality itself can initiate tax foreclosure proceedings. This is a legal process where the property is sold to satisfy the outstanding tax debt. The outcome can be a tax deed sale, where the property is sold at public auction to the highest bidder, and the original homeowner loses all rights to the property. While state law provides some protections and redemption periods, these windows are finite and can be complex to navigate, especially for property owners who are not well-versed in legal procedures. The thought of losing a cherished family vacation home in the Hamptons or a meticulously renovated brownstone in Brooklyn due to unpaid taxes is a stark reminder of the gravity of the situation.

Impact on Credit and Future Finances

Beyond the risk of losing your property, delinquent property taxes can have a significant negative impact on your credit score. Although property tax delinquencies are not typically reported directly to credit bureaus in the same way mortgage or credit card defaults are, a tax lien filed against your property is public record. This public record can affect your ability to obtain new loans, refinance existing mortgages, or even secure other forms of credit. Potential lenders and financial institutions conduct thorough checks, and a tax lien signals financial distress, making you a higher risk borrower. This can curtail plans for major purchases, further investments, or even funding a dream sabbatical to Asia.

Moreover, if you plan to sell your property in New York, any outstanding tax liens must be satisfied before the sale can close. This means the unpaid taxes, interest, and penalties will be deducted from your sale proceeds, potentially reducing your profit or even resulting in a net loss, depending on the equity you have in the property.

Strategies for Managing Property Taxes in New York

Given the potential financial repercussions, proactive and informed management of property taxes is not just recommended, it’s essential for anyone owning property in New York State. By adopting smart strategies, you can mitigate risks, avoid penalties, and ensure your property remains a source of enjoyment and financial stability rather than stress.

Stay Informed and Organized

- Know Your Due Dates: Identify all applicable property tax due dates for your county, town/city, village, and school district. Create a master calendar and set multiple reminders.

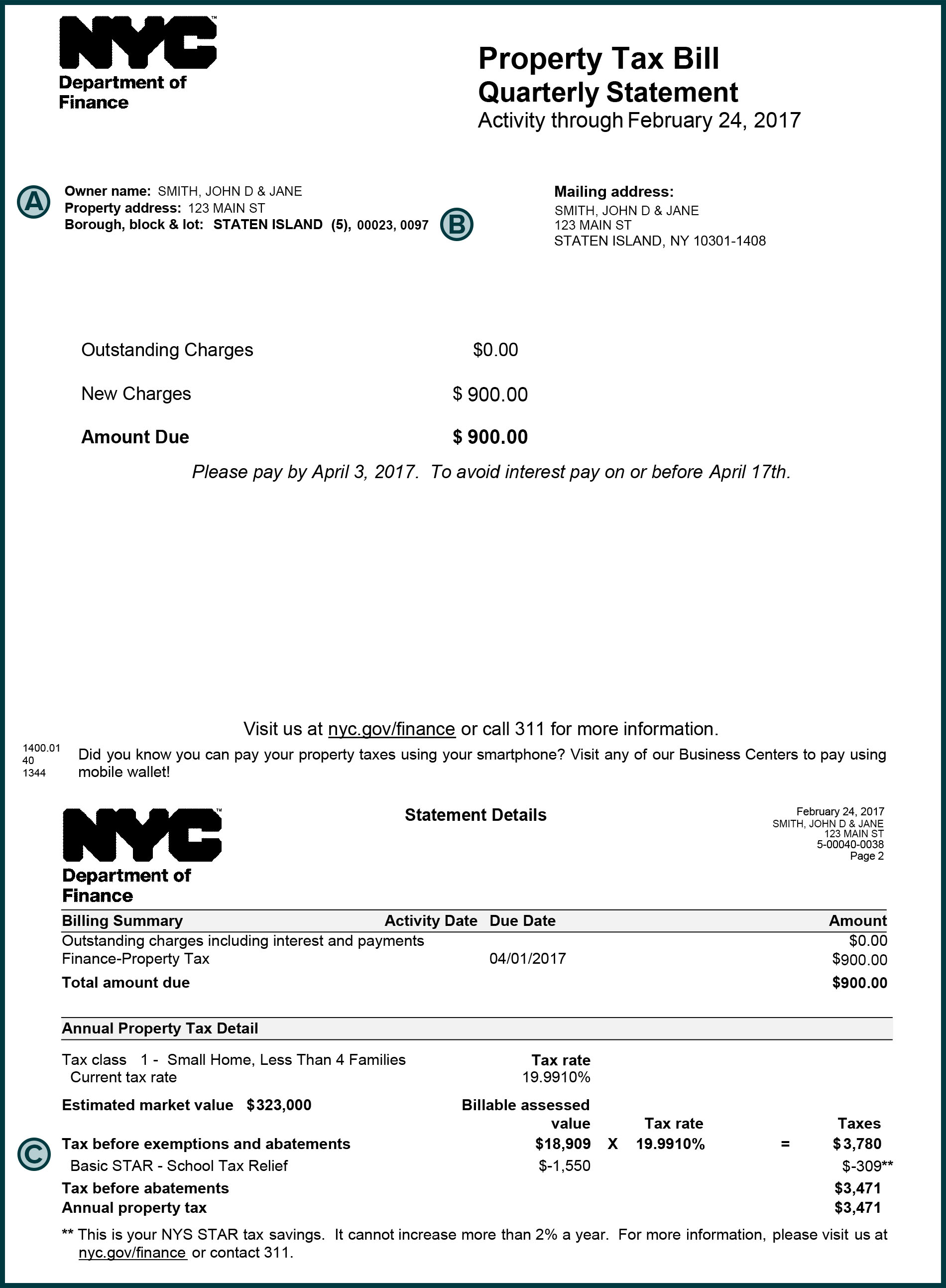

- Verify Your Bills: Carefully review each tax bill you receive. Check the assessed value, tax rate, and any exemptions applied. If anything seems incorrect, contact your local assessor or tax collector immediately.

- Utilize Online Resources: Most New York municipalities have official websites where you can look up your property tax information, view payment history, and often pay bills online. These portals are invaluable tools for staying current.

- Keep Records: Maintain meticulous records of all tax bills, payment confirmations, and any correspondence with tax authorities. This documentation can be crucial if disputes arise.

Explore Payment Options and Assistance Programs

- Payment Plans: If you anticipate difficulty in making a lump-sum payment, contact your local tax collector’s office before the due date. Some municipalities may offer installment plans or allow you to enter into an agreement to pay delinquent taxes over time, potentially at a reduced interest rate or with waived penalties, especially in cases of hardship.

- Tax Exemptions: New York State offers various property tax exemptions that can reduce your tax bill, such as STAR (School Tax Relief) for primary residents, exemptions for seniors, veterans, or individuals with disabilities. Research which exemptions you might qualify for and apply for them promptly. These savings can be significant, freeing up funds for travel or other lifestyle expenses.

- Escrow Accounts: If you have a mortgage, your lender likely collects property taxes (and insurance) through an escrow account. This means a portion of your monthly mortgage payment goes into this account, and the lender pays the taxes on your behalf. This system provides convenience and reduces the risk of missed payments. Ensure your escrow account is adequately funded and monitor its activity.

Seek Professional Advice

For complex situations, such as inherited property, significant changes in property value, or long-standing delinquency issues, consulting with a tax professional or a real estate attorney who specializes in New York State property law can be invaluable. They can help you understand your options, negotiate with tax authorities, and guide you through the process of resolving outstanding tax issues. This expert guidance can save you money, time, and considerable stress in the long run.

Property Tax Considerations for New York Homeowners and Investors

For those drawn to New York State for its unparalleled lifestyle offerings, diverse attractions, and robust real estate market, understanding property taxes is not just a regulatory chore but an integral part of responsible ownership and investment. Whether you’re purchasing a charming brownstone in Brooklyn, a sprawling estate in the Hamptons, or a cozy vacation rental in Upstate New York, the property tax landscape will directly influence your financial planning and overall experience.

Impact on Lifestyle and Travel Planning

A significant aspect of the “life out of the box” philosophy involves freedom and flexibility, often manifested through travel and leisure. Unexpected property tax penalties can severely curtail these aspirations. Imagine planning a dream trip to Japan or booking a luxurious resort stay, only to find those funds reallocated to cover compounded interest and late fees on your New York property taxes. Proactive tax management ensures that your discretionary income remains available for experiences that truly enrich your life, whether it’s exploring new destinations, indulging in local cuisine, or simply enjoying the amenities of a high-end hotel.

For those who own properties intended for short-term rentals (e.g., Airbnb accommodations), understanding the tax burden is even more critical. Unpaid property taxes can lead to liens, affecting your ability to operate your rental business smoothly and potentially leading to legal complications that disrupt your income stream and guest bookings. A well-managed property, including its tax obligations, contributes to a stable financial foundation, which in turn supports a more adventurous and stress-free lifestyle.

Investing in New York Real Estate

New York State real estate can be an excellent investment, offering potential for appreciation and rental income. However, investors must factor property taxes, along with interest and penalties for delinquency, into their financial models. High property taxes in certain desirable areas, like parts of Long Island or affluent suburbs of New York City, can significantly impact profitability. Diligence in researching a property’s tax history and current obligations is a non-negotiable step before making a purchase. This due diligence ensures that your investment remains sound and aligns with your financial goals, supporting your broader lifestyle and travel aspirations.

In conclusion, the answer is unequivocally “yes” – New York State municipalities charge interest and penalties on back property taxes. This system is designed to incentivize timely payment and fund essential local services. For property owners and aspiring investors in New York, understanding these rules is not just about compliance; it’s about safeguarding your financial health, protecting your investments, and ensuring that your journey through life, full of travel and enriching experiences, remains uninterrupted by preventable financial burdens. Embrace proactive management, stay informed, and enjoy all that New York has to offer, confidently.