For many envisioning a vibrant retirement filled with cultural experiences, breathtaking natural beauty, and unparalleled urban excitement, the Empire State often tops the list. From the iconic buzz of New York City to the serene landscapes of the Hudson Valley and the majestic grandeur of Niagara Falls, New York offers a diverse tapestry of destinations and experiences for every taste. Whether you dream of strolling through Central Park, catching a Broadway show, exploring historic landmarks, or simply enjoying the culinary delights of local culture, the promise of a fulfilling post-career lifestyle here is undeniable.

However, a crucial question often arises for those considering a move or extended long-term stay in New York, particularly as they approach their golden years: “Does New York tax Social Security benefits?” The answer to this seemingly straightforward question is vital for financial planning, impacting everything from your choice of accommodation to your budget for travel and tourism activities. Understanding the tax implications is a cornerstone of making your New York retirement dream a comfortable and sustainable reality. Let’s delve into the specifics, providing a comprehensive guide to navigating the tax landscape for retirees in the Empire State.

Understanding Social Security Taxation in the Empire State

When it comes to Social Security benefits, the tax picture can be a bit nuanced, involving both Federal and State considerations. It’s essential to distinguish between these two levels of government to fully grasp how your benefits might be taxed in New York.

Federal vs. State Taxation: A Crucial Distinction

First and foremost, it’s important to understand that a portion of your Social Security benefits might be subject to Federal income tax, regardless of which state you reside in. The Internal Revenue Service (IRS) determines the taxability of these benefits based on your total income.

The IRS uses a calculation involving your “provisional income” (also known as Modified Adjusted Gross Income, or MAGI), which includes your Adjusted Gross Income, tax-exempt interest, and half of your Social Security benefits.

- If your provisional income is between $25,000 and $34,000 for an individual, or between $32,000 and $44,000 for those filing jointly, up to 50% of your Social Security benefits may be taxable at the Federal level.

- If your provisional income exceeds $34,000 for an individual, or $44,000 for those filing jointly, up to 85% of your Social Security benefits may be taxable.

This Federal taxation applies across the entire United States. Now, let’s turn our attention to the state level, which is where New York offers a distinct advantage for retirees.

The New York State Exemption Threshold

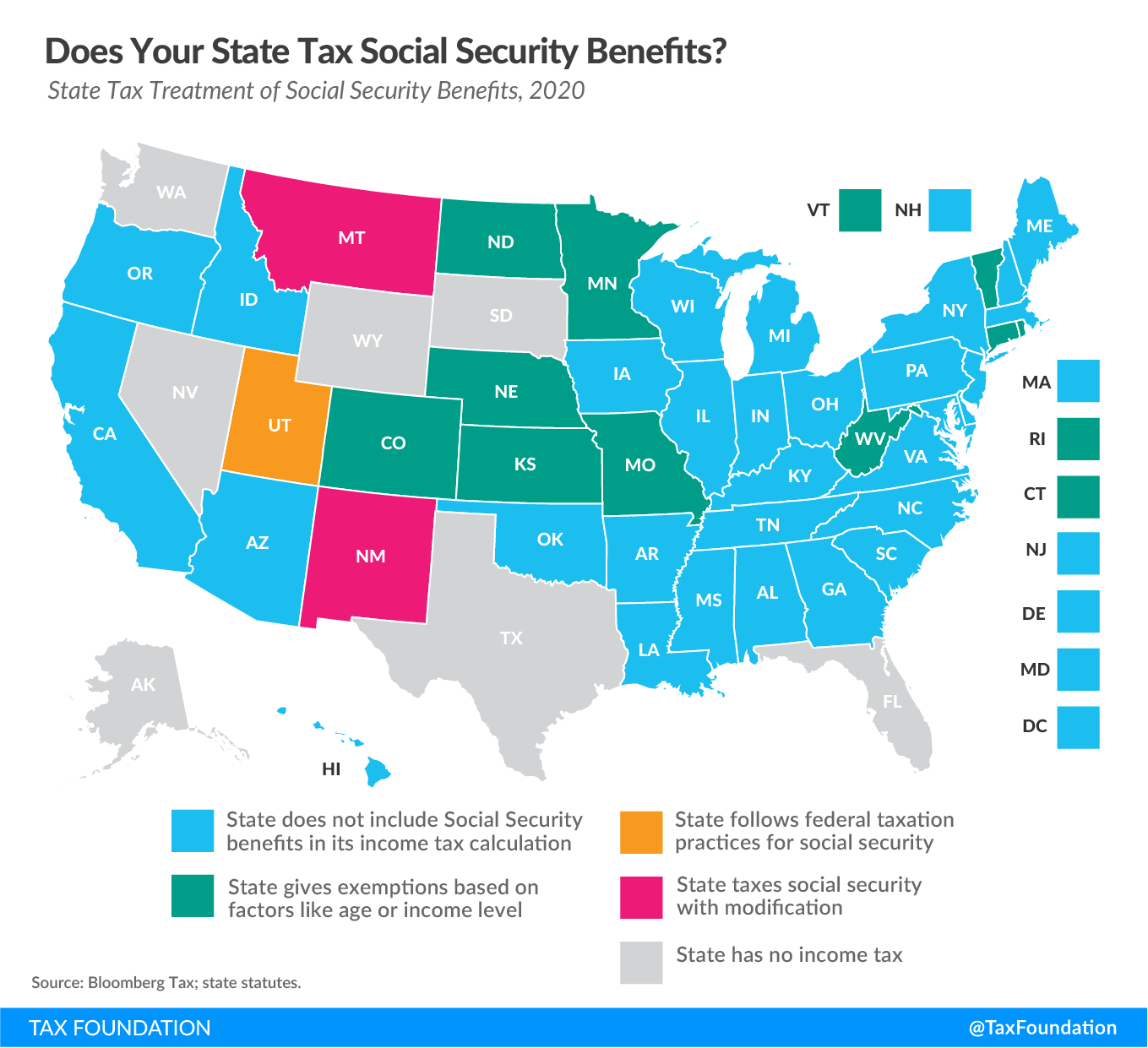

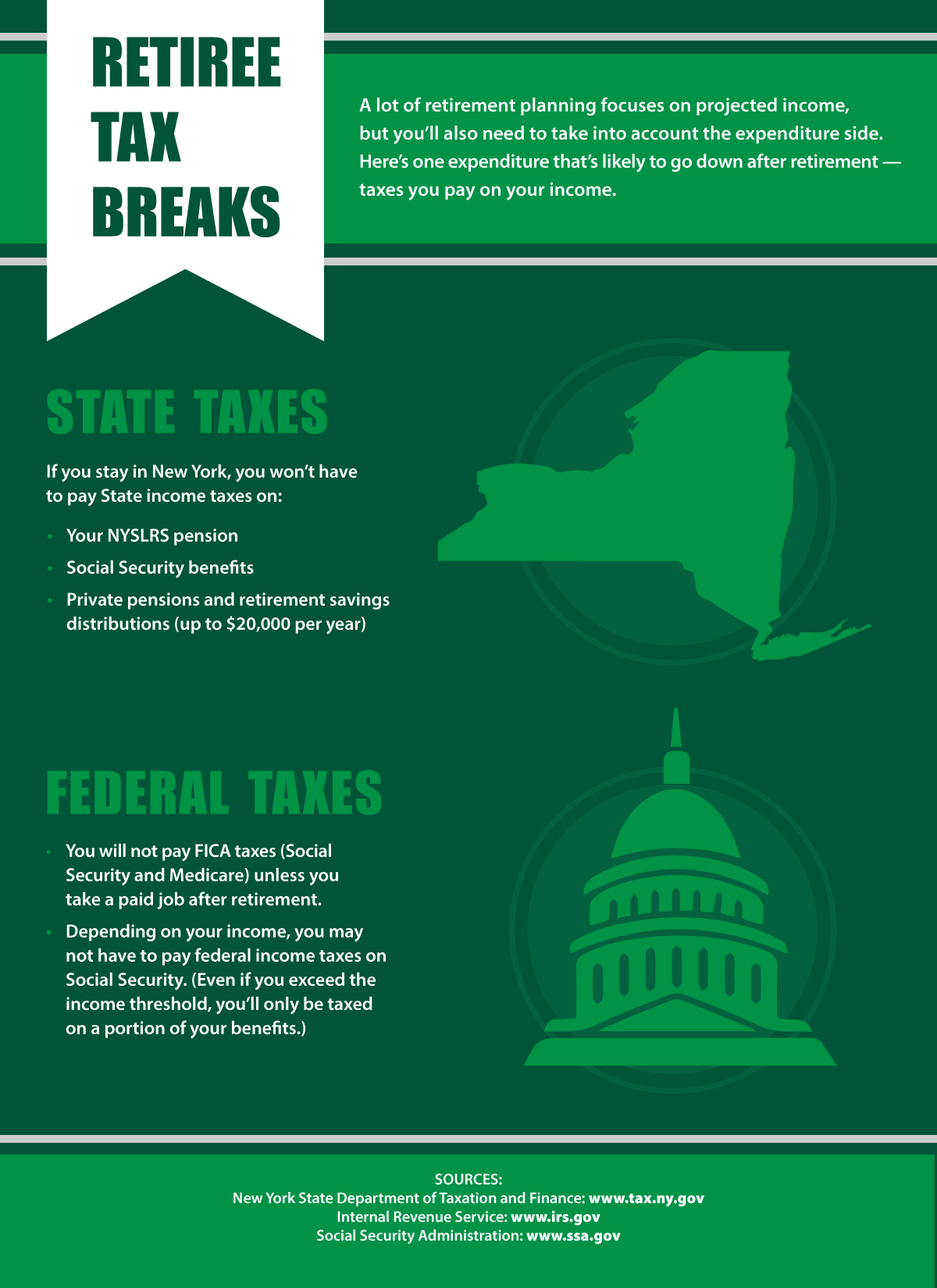

Here’s the good news for anyone considering New York as their retirement haven: New York State generally does NOT tax Social Security benefits.

This blanket exemption is one of the most attractive aspects of New York’s tax policy for seniors. However, there’s a specific condition to be aware of, administered by the New York State Department of Taxation and Finance. To qualify for this exemption, your Adjusted Gross Income (AGI) must be above a certain threshold. For the 2023 tax year, this threshold was generally $20,000 for individuals, and this amount is adjusted periodically. If your New York AGI (which excludes your Social Security benefits when determining eligibility for the exemption) is below this threshold, your Social Security might not be fully exempt. However, for most retirees receiving Social Security benefits, their income will typically exceed this low threshold, ensuring their Social Security payments are fully exempt from New York State income tax.

This means that while a portion of your Social Security might be subject to Federal taxation based on your overall income, New York State offers a significant tax break by leaving those benefits untouched. This policy can free up considerable funds, allowing retirees to better enjoy the myriad of attractions, hotels, and cultural richness that define the New York lifestyle.

Navigating Other Retirement Income in New York

While the exemption of Social Security benefits is a major plus, a comprehensive financial plan for retirement in New York must also account for other sources of income. Most retirees have a diversified income stream, including pensions, annuities, and withdrawals from various retirement accounts. Understanding how New York taxes these can significantly influence your financial strategy, affecting your ability to afford preferred accommodation options, luxury travel, or even regular budget travel.

Pension and Annuity Income

New York State offers a substantial exclusion for many types of pension and annuity income. If you are 59 ½ or older, you may be able to exclude up to $20,000 of qualifying pension and annuity income from your New York State taxable income. This applies to distributions from various sources, including:

- Federal, state, and local government pensions.

- Private pension and annuity plans.

- IRAs and 401(k) plans (which we’ll discuss next).

This exclusion is per person, meaning that a married couple filing jointly, where both spouses receive qualifying pension or annuity income, could potentially exclude up to $40,000. This is a considerable benefit that can help offset the generally higher cost of living in certain parts of New York, particularly in popular areas like New York City or Long Island.

IRA and 401(k) Distributions

For many retirees, distributions from Individual Retirement Accounts (IRAs) and 401(k) plans constitute a significant portion of their retirement income. In New York State, these distributions are generally treated as taxable income, similar to regular wages, unless they qualify for the pension and annuity exclusion mentioned above.

This means that if you are 59 ½ or older, withdrawals from your Traditional IRA, 401(k), or other qualified retirement plans (excluding Roth IRA distributions, which are typically tax-free if certain conditions are met) can be included in the $20,000 pension and annuity exclusion. Any amount exceeding this exclusion will be subject to New York State income tax rates, which can range from approximately 4% to 10.9% depending on your income level and filing status.

For retirees planning their finances to cover extended stays in resorts, apartments, or villas in prime New York locations, understanding the impact of these taxes on your disposable income is critical. It influences your budget for food, activities, and even how often you can indulge in luxury experiences.

The Broader Financial Landscape for Retirees in New York

Beyond income taxes on Social Security and retirement distributions, the overall financial health of a retiree in New York is influenced by a range of other factors. These include property taxes, sales tax, and the general cost of living – all of which play a role in shaping your lifestyle and travel budget.

Property Taxes and Cost of Living

New York is notorious for having some of the highest property taxes in the United States. This is a significant consideration for any retiree planning to purchase a home or even rent, as property taxes often influence rental prices. While the rates vary dramatically by county, city, and even school district, homeowners should be prepared for substantial annual property tax bills, especially in desirable areas like Long Island, Westchester County, and many suburban areas around New York City.

The overall cost of living in New York, particularly in urban centers like New York City, is significantly higher than the national average. Housing, transportation, utilities, and even groceries can be more expensive. For example, living in a spacious suite or apartment in Manhattan will require a far greater budget than a similar living space in a more rural part of the state like the Adirondack Mountains. This elevated cost means that even with favorable Social Security and pension tax policies, careful budgeting and financial planning are paramount for New Yorkers in retirement.

However, it’s also worth noting that the state offers programs like the Enhanced STAR exemption for eligible senior homeowners to help reduce their property tax burden. Investigating such programs is a crucial tip for minimizing expenses.

Sales Tax and Other Financial Considerations

New York State has a statewide sales tax rate of 4%, but local jurisdictions can add their own rates, bringing the combined sales tax rate to over 8% in many areas, and exceeding 8.875% in New York City. This tax applies to most goods and some services, impacting your daily spending, whether it’s on souvenirs from famous landmarks, dining out at local food establishments, or purchasing travel essentials.

Other financial considerations include:

- Income Tax on Other Investments: New York taxes investment income, such as capital gains, interest income, and dividend income, at the standard state income tax rates. This can be a significant factor for retirees with substantial investment portfolios.

- Estate Tax: New York State also has its own estate tax, which applies to estates above a certain exemption threshold. This is an important consideration for estate planning.

- Healthcare Costs: While Medicare handles much of the primary healthcare for seniors, supplemental insurance and out-of-pocket costs can still be substantial. New York offers robust healthcare services, but understanding your coverage and potential expenses is vital for your retirement budget. Medicaid is also available for those who qualify based on income and assets.

These broader financial elements highlight the need for a holistic view when planning your retirement in New York. While the tax treatment of Social Security is favorable, other costs can add up, requiring careful consideration and strategic planning to ensure your chosen lifestyle remains affordable and enjoyable.

Making Informed Decisions for Your New York Retirement

Deciding where to spend your retirement is a deeply personal choice, balancing financial considerations with desired lifestyle and access to desired activities and attractions. New York offers a unique blend of opportunities, and understanding its tax landscape is key to making an informed decision.

The Allure of New York for Retirees: Beyond the Numbers

Despite some of its higher costs, New York continues to draw retirees for compelling reasons, many of which align perfectly with the themes of lifeoutofthebox.com. The state boasts an incredible array of:

- Cultural Experiences: World-class museums like the Metropolitan Museum of Art, vibrant Broadway theaters, diverse music venues, and countless galleries.

- Natural Beauty: From the scenic Finger Lakes wine region to the majestic Adirondack Mountains and the stunning coastline, there are endless opportunities for outdoor activities and relaxation.

- Diverse Destinations: Whether you prefer the bustling energy of New York City, the historic charm of Albany, the vibrant community of Buffalo, or the tranquil beauty of upstate towns, there’s a perfect spot for every taste.

- Convenient Travel Hub: New York’s extensive transportation networks make it an ideal base for both domestic and international travel, allowing retirees to explore the world with ease. Many hotels and various accommodation types are readily available for visitors and residents alike.

- High-Quality Healthcare: The state is home to some of the nation’s leading hospitals and medical facilities, providing peace of mind for health-conscious retirees.

The decision to retire in New York often comes down to weighing these unparalleled lifestyle and tourism benefits against the financial realities. The favorable tax treatment of Social Security and certain pensions can make a significant difference in tipping the scales for many.

Seeking Professional Guidance

Given the complexities of tax laws and the varying local costs, the most prudent approach for anyone considering retirement in New York is to consult with a qualified financial advisor or tax professional. They can provide personalized advice based on your specific income sources, assets, and desired lifestyle.

A professional can help you:

- Calculate your precise Federal and state tax liabilities.

- Optimize your retirement income withdrawals, including strategies for IRA and 401(k) distributions.

- Understand the impact of property taxes on your chosen location, whether you’re eyeing a cozy apartment in Brooklyn, a charming home in Rochester, or a spacious villa in the countryside.

- Develop a comprehensive estate planning strategy.

- Plan for other potential costs, such as long-term care.

Ultimately, while New York State generally does not tax your Social Security benefits, your overall financial picture in retirement is shaped by many factors. With careful planning and expert guidance, you can ensure that your golden years in the Empire State are as financially secure and enjoyable as they are culturally enriching and adventurous. This will allow you to focus on discovering all the amazing attractions, experiences, and destinations that New York has to offer, from the bustling energy of Times Square to the serene beauty of its natural parks.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.