Embarking on a journey, whether for leisure or business, often brings a mix of excitement and the practicalities of planning. From selecting the perfect hotel suite to mapping out local attractions, travelers meticulously prepare for their adventures. Amidst the thrill of anticipation, a common question often arises, especially for those who already hold a safety net for their everyday lives: “Does my renters insurance cover hotel stays?”

It’s a valid and important inquiry, underscoring a broader concern about protecting personal belongings and financial liability while away from home. Renters insurance is designed primarily to safeguard your possessions within your rented dwelling and protect you against liability claims that arise there. However, the world of insurance policies is intricate, with nuances that can extend or limit coverage in unexpected situations, including your temporary accommodations in a hotel or resort.

This comprehensive guide delves into the specifics of how renters insurance may, or may not, apply to your travels. We’ll explore the various facets of a standard renters insurance policy – personal property, liability, and additional living expenses – and examine their applicability when you’re checked into a room in Paris, lounging by a pool in Cancun, or exploring the vibrant streets of Tokyo. Understanding these distinctions is crucial not only for peace of mind but also for making informed decisions about supplementary travel protection, ensuring your explorations remain carefree and secure.

Understanding the Scope of Renters Insurance

To properly assess whether your renters insurance extends to hotel stays, it’s essential to first grasp the fundamental coverages it provides for your primary residence. Renters insurance typically comprises three main components: personal property coverage, liability coverage, and additional living expenses (ALE). Each of these components serves a distinct purpose, and their application outside your home can vary significantly.

Personal Property Protection: Your Belongings on the Go

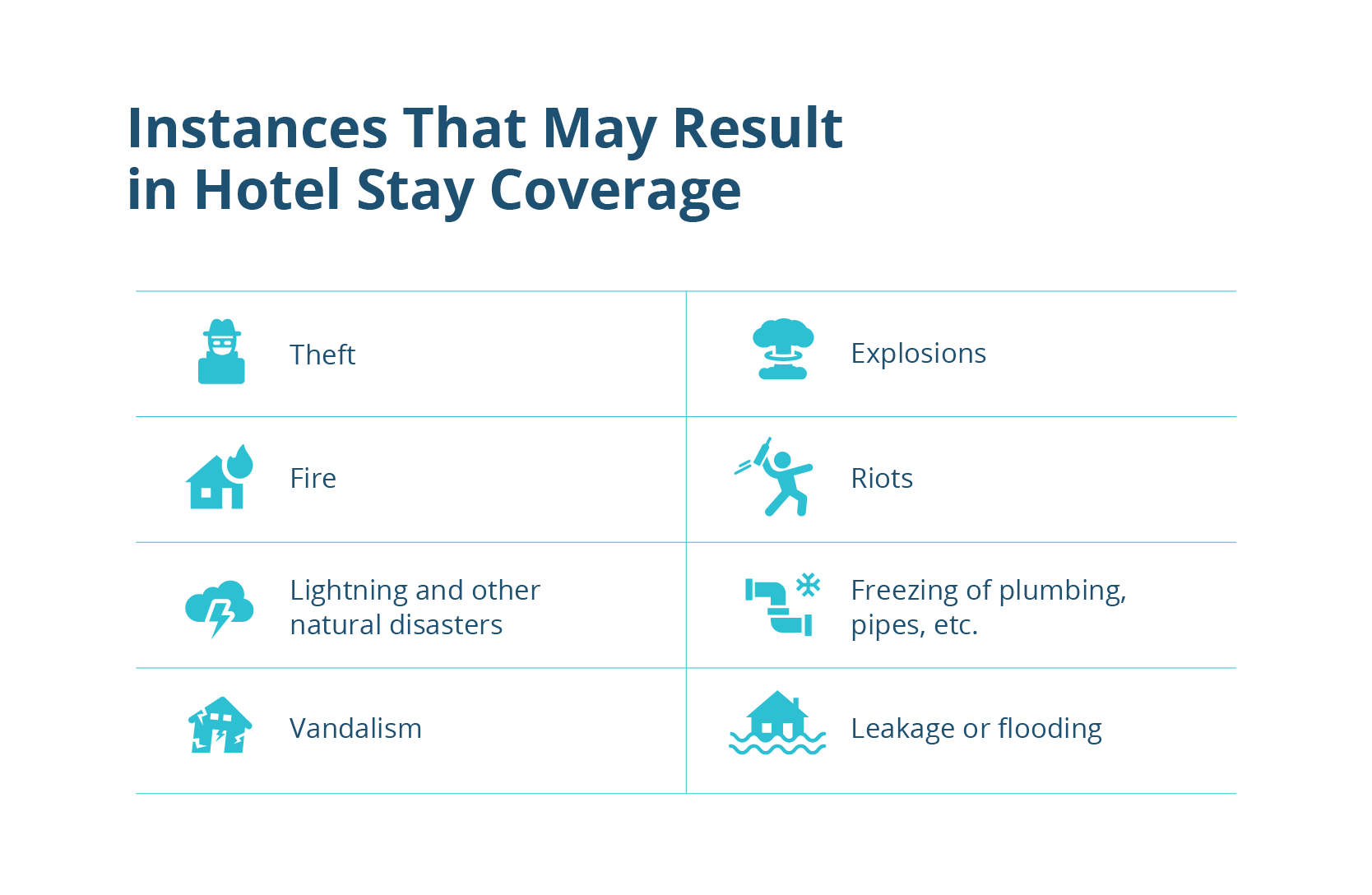

The cornerstone of any renters insurance policy is its personal property coverage. This protects your belongings – everything from your furniture and electronics to clothing and jewelry – against specified perils such as theft, fire, smoke, vandalism, and certain natural disasters. Crucially, many renters insurance policies include an “off-premises” clause, meaning your personal property isn’t just covered within the four walls of your apartment; it often extends to items you take with you when you travel.

This is where the potential for hotel coverage begins. If your policy has an off-premises clause, it means that if your laptop is stolen from your hotel room in London or your luggage goes missing from a secured storage area at a resort in the Riviera Maya, your renters insurance might offer reimbursement. However, there are typically limitations. Most policies will cover a percentage of your total personal property coverage while off-premises, commonly ranging from 10% to 20%. For example, if you have $30,000 in personal property coverage, you might have $3,000 to $6,000 in coverage for items stolen or damaged outside your home.

It’s also vital to consider your deductible. If a $500 camera is stolen and your deductible is $500, you wouldn’t receive any payout. Furthermore, certain high-value items, like expensive jewelry, fine art, or rare collectibles, often have sub-limits within a standard policy or may require separate riders or endorsements for adequate coverage, even at home. When planning a trip with such items, it’s imperative to review your policy details carefully or consult with your insurance provider.

Liability Coverage: When Accidents Happen Away from Home

The liability component of renters insurance is designed to protect you financially if you are found responsible for causing bodily injury to another person or damage to their property. This coverage typically extends beyond the confines of your rented home. So, if you accidentally injure another guest in a common area of a hotel or inadvertently damage someone else’s property while staying at a vacation apartment in Barcelona, your renters insurance liability coverage could come into play.

For instance, imagine you’re rushing through the hotel lobby of the Four Seasons and accidentally knock over another guest, causing them to break their expensive camera. Your renters insurance might cover the medical expenses for their injury and the cost to replace their camera, up to your policy limits. This aspect of coverage is particularly reassuring for travelers, as accidents can happen anywhere, regardless of how careful one tries to be.

However, there are important caveats. Liability coverage generally does not cover damage you intentionally cause, nor does it typically cover damage to property owned by the hotel itself. If you accidentally break a window or damage furniture in your room, that’s usually a different story, which we’ll explore in a later section. The key distinction here is damage to others’ property or injury to others.

Additional Living Expenses (ALE): A Lifeline During Displacement

Additional Living Expenses (ALE), also known as Loss of Use coverage, is another critical part of renters insurance. Its primary purpose is to cover the costs of temporary housing and living expenses if your rented home becomes uninhabitable due to a covered peril (e.g., fire, flood, extensive damage). This could include the cost of staying in a hotel, eating out, or even laundry services, while your home is being repaired or you’re searching for a new place.

This is where the distinction between “displacement” and “planned travel” becomes absolutely crucial. ALE coverage might cover a hotel stay if you are forced to evacuate your home or if it’s rendered unlivable and you’re temporarily relocating to a local hotel in, say, New York City. In such a scenario, the hotel stay is a direct consequence of a covered loss at your primary residence.

However, ALE coverage will almost certainly not cover the cost of a planned vacation or business trip. If you choose to go on a holiday to Rome or a conference in Las Vegas, your renters insurance will not reimburse you for your hotel bills, even if your home remains perfectly intact. It’s a safety net for unexpected home-related disasters, not a fund for discretionary travel expenses. This is a common misconception, and understanding this limitation is vital to avoid disappointment.

Navigating the Nuances: When Renters Insurance Applies to Hotel Stays

While renters insurance isn’t a comprehensive travel policy, there are specific scenarios where its protections can extend to your hotel stays, providing a valuable, albeit limited, safety net.

Theft of Personal Property: A Common Concern for Travelers

One of the most frequent applications of renters insurance during travel involves the theft of personal property. Imagine you’re staying at a busy hotel near Times Square in New York City, and despite your best efforts, your bag, containing a new camera and some clothing, is stolen from your room while you’re out sightseeing. Provided your policy includes off-premises coverage, your renters insurance could reimburse you for the loss of these items, up to your policy’s sub-limits and overall off-premises coverage amount, after your deductible.

To facilitate a claim, it’s incredibly helpful to have an inventory of your belongings, ideally with photos or receipts, especially for more valuable items. Reporting the theft to the local police immediately and obtaining a police report is usually a mandatory step for filing an insurance claim. While your insurance may help with the financial recovery, it’s still prudent to take precautions, such as utilizing the hotel safe for valuables and always keeping your luggage secured.

Liability Incidents: Unexpected Events in New Environments

As mentioned earlier, your personal liability coverage generally travels with you. This can be particularly relevant during hotel stays, where interactions with other guests and unfamiliar environments can lead to unforeseen incidents. Suppose you accidentally spill a drink on another guest’s expensive laptop at a poolside bar at the Atlantis Resort, or while enjoying a meal at a fine dining restaurant in Venice, you inadvertently trip a waiter, causing them injury and dropping a tray of food.

In these situations, your renters insurance liability coverage could step in to cover the costs of property damage or medical expenses for the injured party. This is a significant benefit, as such incidents, though rare, can lead to substantial financial claims. It’s important to remember that this coverage typically applies when you are deemed negligent, not for intentional acts or business-related liabilities. Always report any such incident to your insurance provider as soon as reasonably possible.

When Renters Insurance Typically Does Not Cover Hotel Stays

Despite the limited applications discussed above, it’s more common for renters insurance not to cover most aspects of a typical hotel stay. Understanding these limitations is key to identifying potential gaps in your travel protection.

Damage to the Hotel Itself: A Key Distinction

One of the most important distinctions to grasp is that renters insurance liability coverage generally does not extend to damage you cause to the structure or furnishings of the hotel room or any other part of the hotel property. If you accidentally spill red wine on the carpet, break a mirror, or damage a piece of furniture in your room at a Marriott or a Hilton, your renters insurance will not cover the cost of repairs or replacement.

Hotels typically have their own property insurance to cover such incidents, and they will often charge the guest directly for any damages incurred. Your personal liability coverage is designed to protect you from claims made by third parties (other individuals) or for damage to their property, not for damage to property under your temporary care or control, such as a hotel room you are occupying. This is a crucial point that often surprises travelers.

Trip Cancellations and Interruptions: Beyond Renters Insurance Scope

Renters insurance is unequivocally not a substitute for travel insurance when it comes to trip cancellations, interruptions, or delays. If you have to cancel your meticulously planned trip to Dubai because of a sudden illness, or if your flight is delayed for an extended period, causing you to miss a connecting cruise, your renters insurance will provide no financial relief for lost deposits, non-refundable bookings, or additional expenses incurred due to the disruption.

Similarly, renters insurance does not cover medical emergencies that occur while you are traveling, especially internationally. If you fall ill or have an accident while hiking in the Swiss Alps, your renters insurance will not cover hospital bills or emergency evacuation costs. These are the core coverages provided by a dedicated travel insurance policy, highlighting the specialized nature of different insurance products.

Everyday Travel Mishaps: The Small Print Matters

Beyond major incidents, renters insurance also doesn’t cover a myriad of common travel mishaps. If you simply lose your wallet (as opposed to it being stolen), forget an item in your room, or experience general wear and tear on your luggage during transit, these events typically fall outside the scope of coverage. Renters insurance is designed for specified perils, not for simple carelessness or the ordinary risks associated with travel.

Furthermore, any issues with the quality of your hotel stay, such as unsatisfactory service, uncomfortable beds, or amenities that don’t meet expectations, are entirely outside the realm of insurance. These are matters to be resolved directly with the hotel management or through travel booking platforms, not through your renters insurance provider.

Alternative and Supplementary Protections for Travelers

Given the significant limitations of renters insurance for travelers, it becomes clear that relying solely on it for protection during your trips is inadequate. Fortunately, several other options exist to ensure comprehensive coverage.

Travel Insurance: The Comprehensive Solution for Trips

For virtually any planned trip, especially international travel, a dedicated travel insurance policy is the most robust and comprehensive solution. Travel insurance is specifically designed to address the unique risks associated with being away from home.

A good travel insurance policy can offer:

- Trip Cancellation/Interruption: Reimburses non-refundable costs if your trip is canceled or cut short due to covered reasons (e.g., illness, family emergency, severe weather).

- Medical Emergencies: Covers emergency medical treatments, hospital stays, and even emergency medical evacuation, which can be astronomically expensive overseas.

- Baggage Loss/Delay: Provides compensation for lost, stolen, or damaged luggage, and often offers funds for essential items if your bags are delayed.

- Rental Car Coverage: Many policies include coverage for damage to a rental car.

- 24/7 Assistance: Access to a helpline for travel emergencies.

Policies vary widely, from basic coverage to premium plans that include “cancel for any reason” options. It’s crucial to compare different providers and policy types to find one that matches your specific travel needs and budget, whether you’re embarking on an adventurous backpacking journey or a luxurious cruise.

Credit Card Travel Benefits: Hidden Gems for Savvy Travelers

Many premium travel credit cards offer an impressive array of travel-related benefits that can supplement or even replace some aspects of a traditional travel insurance policy. These benefits often include:

- Trip Cancellation/Interruption Insurance: Similar to standalone travel insurance, but typically with lower coverage limits and specific conditions.

- Baggage Delay/Loss Coverage: Reimbursement for essential purchases if your luggage is delayed, or for lost/stolen bags.

- Rental Car Collision Damage Waiver (CDW/LDW): Primary or secondary coverage for damage or theft of a rental vehicle.

- Travel Accident Insurance: Coverage for accidental death or dismemberment during travel.

- Emergency Assistance Services: Referral services for medical or legal emergencies.

It’s vital to thoroughly read your credit card’s guide to benefits, as terms, conditions, and coverage limits can vary significantly between cards and issuers. Often, you must have paid for the entire trip (or a substantial portion) with that specific card to activate the benefits. These benefits can be a fantastic perk, especially for frequent travelers within the United States or for shorter international trips, but they typically don’t offer the same depth of coverage as a comprehensive travel insurance policy, especially regarding medical emergencies.

Homeowners Insurance: A Similar, But Distinct, Coverage

For homeowners, it’s worth noting that homeowners insurance policies generally include similar “off-premises” personal property and liability coverage as renters insurance. Therefore, homeowners would face similar considerations and limitations when it comes to their hotel stays. The fundamental principle remains: these policies are designed for your primary residence, with limited extensions for travel, and are not a substitute for dedicated travel insurance.

Practical Tips for Safeguarding Your Belongings and Peace of Mind During Hotel Stays

Beyond understanding insurance policies, proactive steps can significantly enhance your security and peace of mind during your travels.

Before You Go: Preparation is Key

- Review Your Renters Insurance Policy: Before any trip, take the time to read your policy documents or call your insurance provider. Clarify your off-premises personal property limits and any specific exclusions.

- Inventory Valuables: Create a list of all valuable items you plan to bring, including their estimated worth, serial numbers, and photos. Store this list digitally (e.g., in cloud storage) so you can access it even if your physical bag is lost or stolen.

- Consider Travel Insurance: Obtain quotes for travel insurance, especially for expensive or international trips. Compare coverages and choose a policy that addresses your specific concerns, such as medical emergencies or adventure activities.

- Check Credit Card Benefits: Understand what travel benefits your credit cards offer and whether they require specific actions (e.g., booking with the card) to activate.

- Pack Wisely: Only bring essential valuables. Leave irreplaceable items at home.

During Your Stay: Smart Habits

- Use the Hotel Safe: Most reputable hotels provide in-room safes. Utilize them for passports, extra cash, expensive jewelry, and small electronics.

- Keep Valuables Out of Sight: When leaving your room, don’t leave expensive items like laptops, tablets, or cameras openly displayed. Tuck them away in a drawer, closet, or your secured luggage.

- Secure Your Luggage: Even within your room, consider using luggage locks or chaining your bags together if security is a major concern.

- Be Aware of Your Surroundings: Whether you’re in a bustling hotel lobby or enjoying a stroll through a picturesque villa in Tuscany, stay vigilant. Be mindful of your bag and pockets in crowded areas.

- Report Theft Immediately: If an item is stolen, report it to the hotel management and the local police immediately to obtain a police report. This document will be essential for any insurance claim.

- Document Incidents: For any liability incident or damage, take photos and gather contact information from witnesses if possible.

Conclusion: A Tailored Approach to Travel Protection

The question “Does renters insurance cover hotel stays?” yields a nuanced answer: partially, and only in very specific circumstances. While your renters insurance can offer a limited safety net for personal property theft and certain liability incidents that occur during your travels, it is emphatically not designed to be a comprehensive travel insurance policy. It will not cover trip cancellations, medical emergencies abroad, or damage you inflict upon the hotel property itself.

For those who frequently travel, whether domestically or internationally, a tailored approach to protection is always recommended. This means understanding the precise boundaries of your renters insurance, leveraging the travel benefits offered by your credit cards, and, most importantly, investing in a dedicated travel insurance policy for robust coverage against the myriad of unforeseen events that can impact a journey.

By taking the time to plan your insurance coverage as meticulously as you plan your itinerary, you can truly embrace the adventure, explore new destinations, and create unforgettable memories with the ultimate peace of mind. Safe travels!

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.