The sunshine state of Florida is a dream destination for many, whether you’re seeking a permanent residence, a vacation home, or a lucrative investment property. From the vibrant nightlife of Miami to the pristine beaches of the Florida Keys, and the family-friendly attractions of Orlando, Florida offers a diverse range of lifestyle and tourism opportunities. However, for those considering selling assets in the Sunshine State, understanding capital gains tax is crucial. This article delves into how capital gains tax works in Florida, clarifying the state’s position and federal implications, offering insights relevant to homeowners, investors, and potential residents alike.

While Florida is renowned for its lack of a state income tax, this absence of a broad tax on earnings often leads to a common misconception: that there’s no capital gains tax at all. This couldn’t be further from the truth. Capital gains tax, a levy on the profit made from selling an asset that has appreciated in value, is a federal matter. However, Florida’s unique tax structure means that residents and property owners in the state are still subject to these federal taxes when they sell assets like real estate, stocks, or other investments.

Understanding Capital Gains Tax: Federal vs. State

At its core, capital gains tax is levied on the profit – the capital gain – realized when you sell an asset for more than you paid for it. This applies to a wide range of assets, including:

- Real Estate: Selling a home, vacation property, or investment rental property.

- Stocks and Bonds: Profits from selling shares of companies or government/corporate debt.

- Collectibles: Art, antiques, coins, and other valuable items.

- Other Investments: Mutual funds, cryptocurrencies, and business interests.

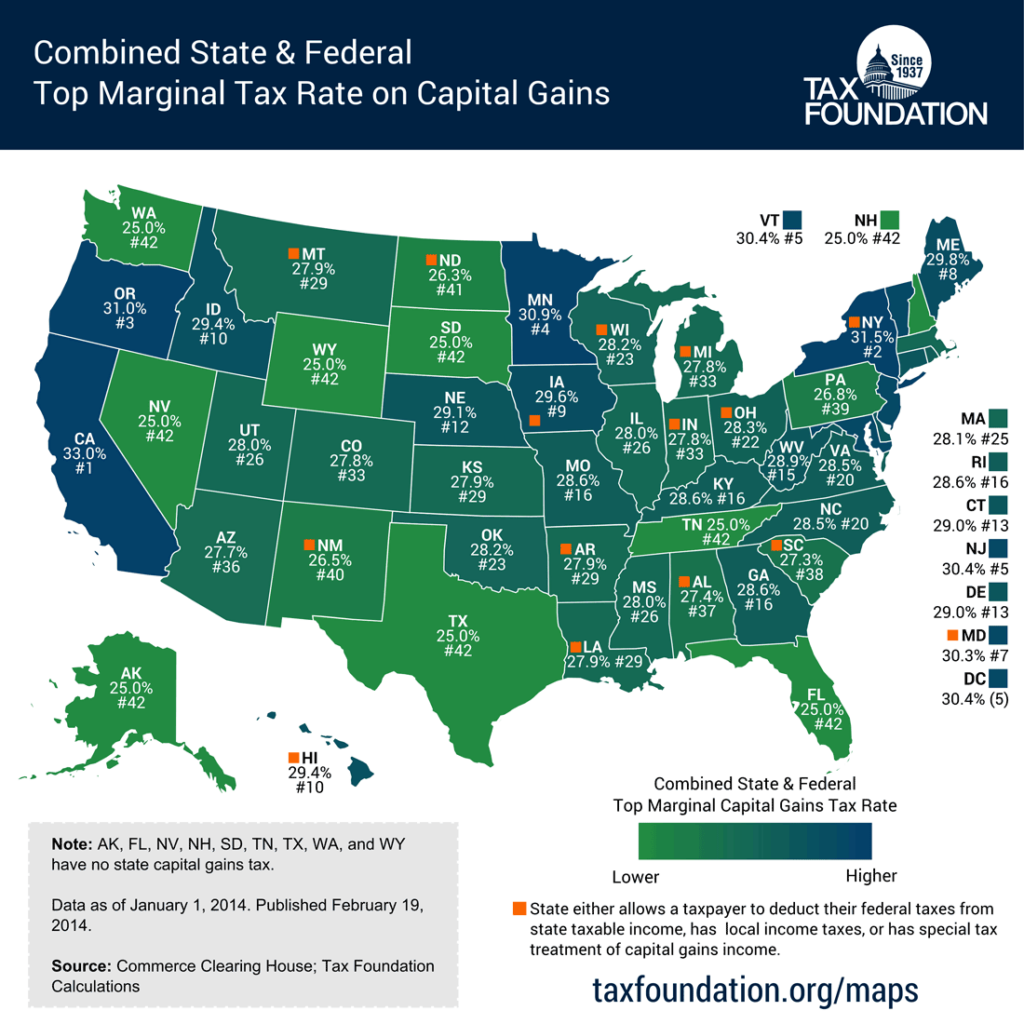

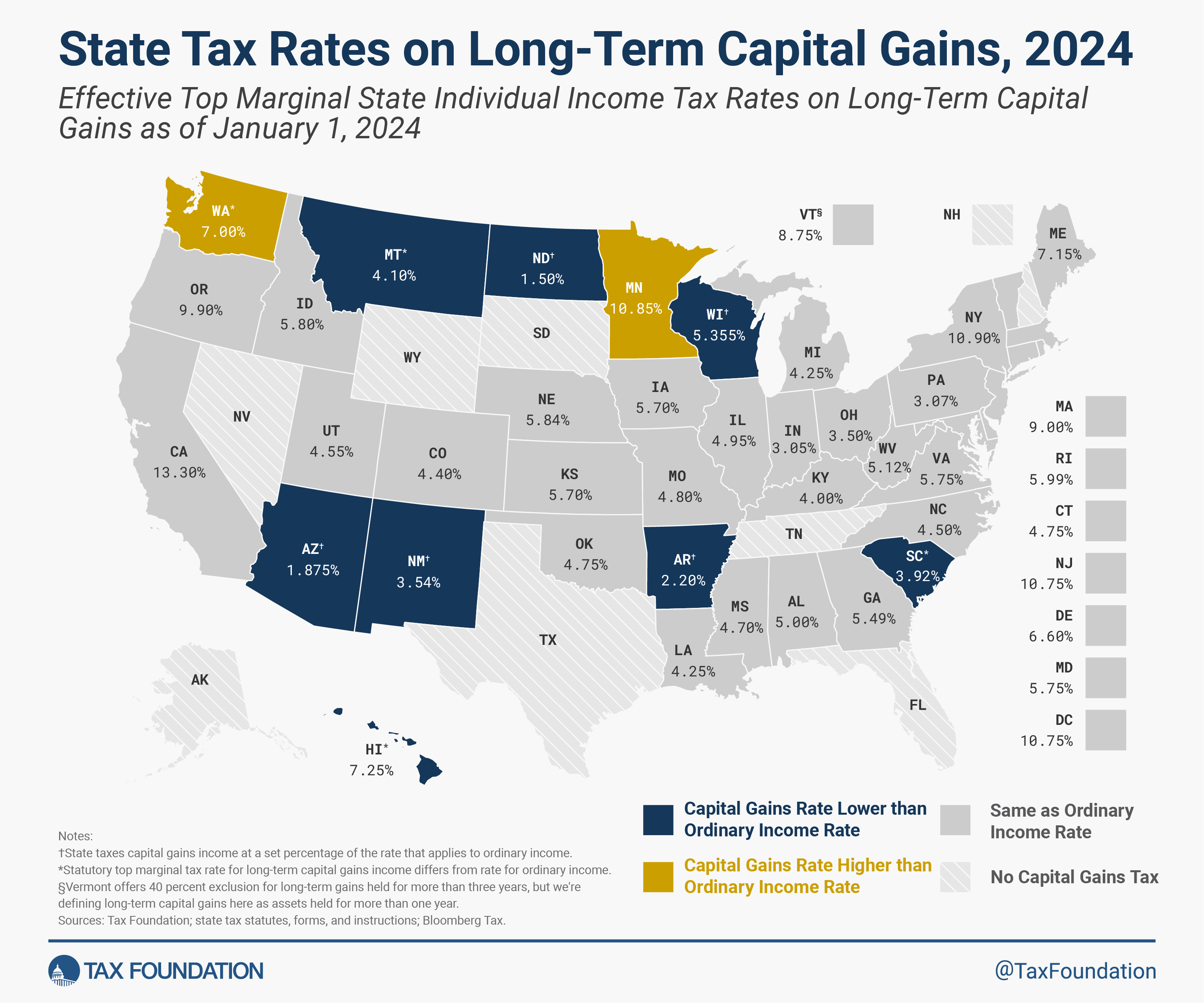

The critical distinction to understand when discussing capital gains tax in Florida is the absence of a state-level capital gains tax. Florida does not impose its own tax on profits derived from the sale of assets. This is a significant advantage for residents and investors in the state, as it eliminates a layer of taxation that exists in many other U.S. states.

However, this does not exempt individuals from paying the federal capital gains tax. The United States federal government taxes capital gains, and this applies universally to all U.S. citizens and residents, regardless of the state they reside in. Therefore, when you sell an asset in Florida that has increased in value, you will owe capital gains tax to the Internal Revenue Service (IRS).

Federal Capital Gains Tax Rates

The federal capital gains tax rates depend on how long you owned the asset before selling it. This is categorized into two main types:

- Short-Term Capital Gains: These are profits from selling assets that you owned for one year or less. Short-term capital gains are taxed at your ordinary income tax rate. For instance, if you bought a piece of art in Tampa and sold it for a profit within 12 months, the profit would be added to your regular income and taxed accordingly. Ordinary income tax brackets can range from 10% to 37%, depending on your total taxable income.

- Long-Term Capital Gains: These are profits from selling assets that you owned for more than one year. Long-term capital gains benefit from preferential tax rates, which are generally lower than ordinary income tax rates. The current long-term capital gains tax rates are 0%, 15%, and 20%, depending on your taxable income level.

The exact threshold for these rates changes annually based on inflation adjustments made by the IRS. It’s essential to consult the most recent IRS guidelines or a tax professional to determine your specific bracket. For example, if you sell a condominium in Clearwater after owning it for five years and make a profit, that profit will be subject to long-term capital gains rates.

Calculating Your Capital Gain

To calculate your capital gain, you subtract the “cost basis” from the “selling price.”

- Selling Price: This is the amount you receive from the sale of the asset.

- Cost Basis: This is generally what you paid for the asset. However, it can also include certain improvements and expenses. For real estate, this might include the purchase price, closing costs, and the cost of significant home improvements (like adding a pool or renovating a kitchen). For stocks, it would be the purchase price plus any commissions or fees.

Example:

Let’s say you purchased a vacation rental property in the Florida Panhandle for $300,000. Over the years, you invested $50,000 in significant renovations, such as updating the kitchen and bathrooms. Your total cost basis would be $350,000 ($300,000 + $50,000). If you later sell this property for $500,000, your capital gain would be $150,000 ($500,000 – $350,000). If you owned the property for more than a year, this $150,000 gain would be taxed at the federal long-term capital gains rates.

Exclusions and Deductions

There are certain situations and provisions that can reduce your taxable capital gain, particularly concerning your primary residence.

The Primary Residence Exclusion

One of the most significant tax benefits for homeowners is the primary residence exclusion. Under Section 121 of the Internal Revenue Code, individuals can exclude a portion of the capital gain from the sale of their primary home from their taxable income.

- Single Filers: Can exclude up to $250,000 of capital gain.

- Married Couples Filing Jointly: Can exclude up to $500,000 of capital gain.

To qualify for this exclusion, you must meet two tests: the ownership test and the residence test.

- Ownership Test: You must have owned the home for at least two years out of the five years preceding the sale.

- Residence Test: You must have lived in the home as your primary residence for at least two years out of the five years preceding the sale.

These two years do not need to be consecutive. For example, if you lived in your home in St. Petersburg for three years, moved away for two years, and then moved back and sold it, you might still qualify if you meet the ownership test. This exclusion is a powerful tool for homeowners, especially in appreciating markets like Florida, where property values have seen substantial growth.

Other Deductions and Considerations

Beyond the primary residence exclusion, other factors can influence your capital gains tax liability:

- Selling Expenses: Costs associated with selling the property, such as real estate agent commissions, closing costs, legal fees, and advertising expenses, can be deducted from the selling price, thus reducing your capital gain.

- 1031 Exchange: For investors in “like-kind” investment properties (e.g., selling one rental property and buying another), a 1031 exchange allows for the deferral of capital gains taxes. This is a complex strategy that requires strict adherence to IRS rules. It’s particularly relevant for those investing in Florida’s robust real estate market, from commercial properties in Jacksonville to multi-family units in Fort Lauderdale.

- Net Investment Income Tax (NIIT): For individuals with higher incomes, a 3.8% Net Investment Income Tax may also apply to capital gains. This tax is levied on the lesser of your net investment income or the amount your modified adjusted gross income exceeds a certain threshold ($200,000 for single filers, $250,000 for married couples filing jointly).

Florida’s Unique Tax Environment

Florida’s appeal as a place to live, invest, and vacation is significantly enhanced by its favorable tax climate. The absence of state income tax is a primary driver for many individuals and businesses relocating to the state. This includes:

- No State Income Tax: As mentioned, Florida does not have a personal income tax. This means your salary, wages, and other forms of earned income are not subject to state-level taxation.

- No State Capital Gains Tax: This is the core of our discussion. Florida does not impose its own tax on the profits from selling assets. This is a significant financial advantage compared to states that do tax capital gains at the state level.

- Homestead Exemption: For primary residences, Florida offers a homestead exemption that can significantly reduce property taxes. While not directly related to capital gains tax, it contributes to the overall cost-effectiveness of owning a home in the state.

- Sales Tax: Florida does have a state sales tax, which applies to the purchase of goods and services. This is a consumption tax, distinct from income or capital gains taxes.

This tax structure makes Florida an attractive state for individuals looking to minimize their overall tax burden. However, it’s crucial to remember that federal taxes, including capital gains tax, still apply.

Impact on Real Estate Investments

Florida’s real estate market is one of the most dynamic in the United States. From luxury condos in Naples to beachfront resorts in Palm Beach and family homes in suburban areas, property investment opportunities abound. For investors, the absence of state capital gains tax is a considerable benefit when selling profitable properties.

Consider an investor who purchased a rental property in Sarasota for $400,000 and, after several years of appreciation, sells it for $700,000. Their capital gain is $300,000. If they lived in a state with a 5% capital gains tax, they would owe $15,000 in state taxes on that gain, in addition to federal taxes. In Florida, they only owe the federal tax.

However, investors must still account for federal capital gains tax. If the property was held for over a year, the $300,000 gain would be taxed at the applicable long-term capital gains rate (0%, 15%, or 20% based on income). The ability to use strategies like the 1031 exchange further enhances the appeal of real estate investment in Florida, allowing for tax-deferred growth.

Planning Your Financial Future in Florida

When considering a move to Florida or making significant investments in the state, it’s wise to consult with a qualified tax advisor or financial planner. They can help you:

- Understand Your Specific Tax Liability: Based on your income, the type of asset sold, and how long you owned it, they can calculate your estimated federal capital gains tax.

- Maximize Deductions and Exclusions: Ensure you are taking advantage of all eligible deductions, such as those for your primary residence or selling expenses.

- Explore Tax Deferral Strategies: If you’re considering selling an investment property, they can guide you through options like the 1031 exchange.

- Long-Term Financial Planning: Integrate capital gains tax considerations into your broader financial goals, such as retirement planning or wealth building.

While Florida offers a wonderfully tax-friendly environment at the state level, a clear understanding of federal capital gains tax obligations is essential for any individual or investor engaging in property sales or other asset liquidations in the Sunshine State. This knowledge empowers you to make informed decisions, optimize your financial outcomes, and fully enjoy the benefits of living and investing in this vibrant U.S. state. Whether you’re drawn by the allure of a Disney World vacation, the historic charm of St. Augustine, or the economic opportunities in cities like Fort Myers, being financially savvy in Florida includes understanding capital gains tax.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.