[California], a land of sun-kissed beaches, towering redwoods, and vibrant cities, beckons millions of travelers and new residents each year. From the iconic [Golden Gate Bridge] in [San Francisco] to the bustling boulevards of [Los Angeles] and the serene vineyards of [Napa Valley], the [Golden State] offers an unparalleled tapestry of experiences. However, for anyone planning an extended stay, a road trip across the [Pacific Coast Highway], or a permanent move, understanding the cost of living essentials, particularly car insurance, is paramount. This isn’t just a legal requirement; it’s a fundamental aspect of budgeting for your [California] adventure, whether you’re exploring [Yosemite National Park] or enjoying the luxury resorts near [Palm Springs].

Navigating the intricacies of car insurance in [California] can seem daunting, but it’s an indispensable step for ensuring peace of mind and financial security on its diverse roads. When we talk about how much car insurance costs, we’re not just looking at a number; we’re considering a crucial component of your travel budget, lifestyle choices, and overall ability to fully experience all that [California] has to offer. For tourists accustomed to public transport in their home countries, or for those relocating from states with different insurance landscapes, understanding the local specifics is key. This comprehensive guide aims to demystify car insurance costs in [California], framing it within the broader context of travel, accommodation, and lifestyle planning that defines the unique allure of the state.

Navigating the Golden State: Car Insurance as a Travel Essential

The allure of [California] is undeniable. Imagine cruising down Highway 1, the majestic [Big Sur] coastline unfolding before you, or taking a scenic drive through [Joshua Tree National Park] at sunset. These quintessential [California] experiences often necessitate a vehicle. Whether you’re renting a car for a week-long exploration of [Southern California] or bringing your own vehicle for a long-term stay, car insurance is not just a suggestion; it’s a legal mandate. For many, especially those from international destinations, the concept and cost of car insurance might be a significant new variable to factor into their travel preparations.

The Cost of Freedom: Why Car Insurance Matters for California Adventures

The average cost of car insurance in [California] can fluctuate significantly, but generally, it hovers around $2,000 to $2,500 per year for full coverage, though liability-only policies can be considerably cheaper. This figure is an average, and individual rates vary wildly based on numerous factors, which we will delve into. For tourists, this cost often comes indirectly through rental car insurance options. For new residents, it’s a direct expense that must be budgeted alongside rent, food, and entertainment.

Consider a family planning a multi-city tour, perhaps starting in [San Diego], then heading up to [Santa Barbara], and finally exploring the iconic attractions of [Los Angeles] like [Disneyland] or [Universal Studios Hollywood]. The freedom to move between these destinations, explore hidden gems, or even commute to unique local cultural experiences largely depends on reliable transportation. Without adequate insurance, not only are you risking legal penalties, but you’re also exposing yourself to potentially crippling financial liabilities in the event of an accident. This makes understanding and securing the right insurance a core element of responsible travel and lifestyle planning in the [Golden State].

Renting vs. Owning: Insurance Implications for Tourists and New Residents

For tourists, the car insurance question typically arises when renting a vehicle. Rental car companies offer various insurance products, often at a daily rate. These can range from basic liability waivers to comprehensive coverage that protects against collision damage, theft, and third-party claims. While convenient, these daily rates can add up, sometimes significantly increasing the overall cost of your trip. Many personal car insurance policies (for those who own a car at home) or credit card benefits might offer some level of rental car coverage, so it’s crucial for travelers to check their existing policies before purchasing additional coverage at the rental counter. This due diligence can lead to substantial savings, allowing more budget for visiting landmarks like the [Getty Center] or enjoying the vibrant food scene in [San Francisco].

For those considering a move or an extended stay in [California], perhaps for a job opportunity or a lifestyle change, the car insurance landscape is different. You’ll need to purchase your own policy from a [California]-licensed insurer. This transition can be complex, especially if you’re new to the state or even the country. Factors like your driving history (which might need to be verified internationally), the type of vehicle you drive, and even your new [California] address will all play a significant role in determining your premium. Understanding these nuances is vital for anyone planning to embrace the [California] lifestyle, from navigating the bustling streets of [Santa Monica] to exploring the quiet charm of [Carmel-by-the-Sea].

Factors Influencing Car Insurance Rates in California

Car insurance premiums in [California] are not one-size-fits-all. They are the result of a complex algorithm that takes into account a myriad of personal and environmental factors. Understanding these variables is the first step towards predicting your potential costs and finding ways to manage them. For anyone planning to integrate into the [California] way of life, from enjoying the luxury travel options to seeking out budget-friendly adventures, this knowledge is power.

Demographics and Driving History: Personalizing Your Premium

Your personal profile is a major determinant of your car insurance rates. Age plays a significant role, with younger, less experienced drivers typically facing higher premiums due to perceived higher risk. Conversely, older, experienced drivers often benefit from lower rates, assuming a clean driving record. However, rates can begin to rise again for very senior drivers. Gender historically influenced rates, but [California] is one of the states that have largely eliminated gender as a rating factor, focusing instead on objective risk factors.

Your driving history is arguably the most impactful factor. A clean record, free of accidents, speeding tickets, or other moving violations, is your best asset for securing lower rates. Conversely, a history of claims or infractions will almost certainly lead to higher premiums. Insurance companies also look at your credit score (though [California] has some restrictions on its use for insurance rating compared to other states) and your marital status, with married individuals sometimes receiving slightly lower rates. For those new to the state or country, establishing a driving history in the [US] or providing verifiable international driving records can be crucial.

Vehicle Type and Coverage Levels: Protecting Your Investment

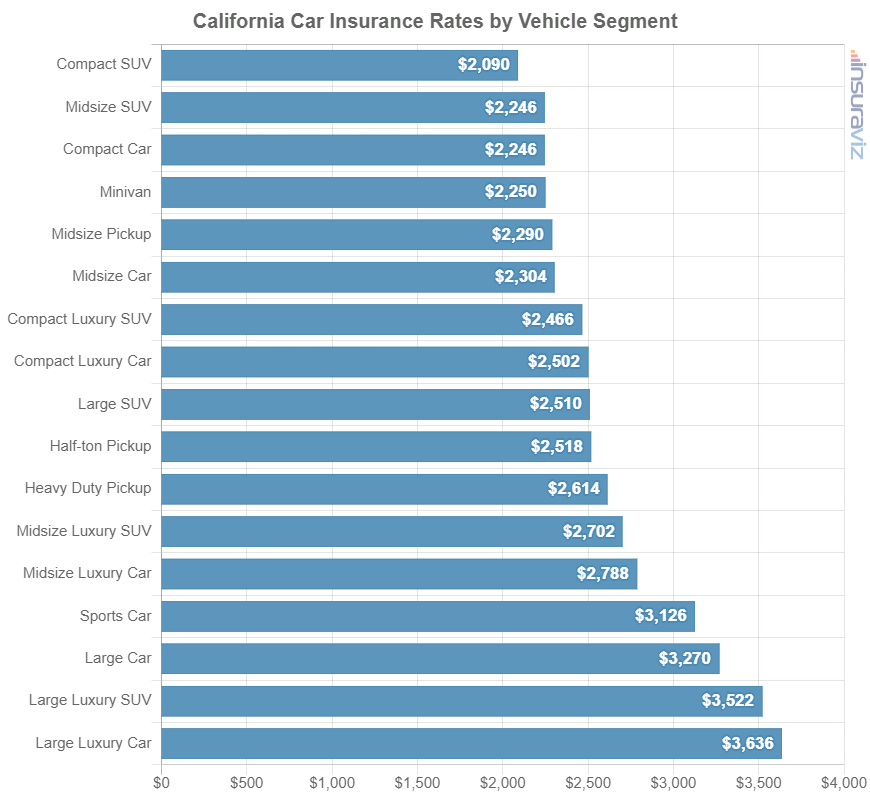

The type of vehicle you drive significantly impacts your insurance costs. Generally, newer, more expensive cars, sports cars, or vehicles with higher theft rates will cost more to insure. This is because the potential cost of repairs or replacement is higher. On the flip side, older, more modest vehicles, or those with strong safety ratings and lower repair costs, often come with lower premiums. If you’re planning to explore [California]’s natural beauty, perhaps visiting [Sequoia National Park] or [Lake Tahoe], and need a rugged SUV, be prepared for potentially higher insurance costs compared to a compact sedan.

Equally important are the coverage levels you choose. [California] mandates minimum liability coverage, which protects you financially if you cause an accident resulting in injury or property damage to others. However, these minimums are often insufficient for serious accidents, and most experts recommend higher liability limits. Beyond liability, you can opt for:

- Collision coverage: Pays for damage to your own vehicle in an accident, regardless of fault.

- Comprehensive coverage: Covers non-collision incidents like theft, vandalism, fire, or damage from natural disasters (e.g., wildfires, earthquakes – a relevant concern in [California]).

- Uninsured/Underinsured Motorist (UM/UIM) coverage: Crucial in [California] where many drivers carry only minimum coverage or no insurance at all. This protects you if an at-fault driver doesn’t have enough insurance to cover your damages.

- Medical Payments (MedPay) or Personal Injury Protection (PIP): Covers medical expenses for you and your passengers after an accident, regardless of fault.

Choosing higher deductibles (the amount you pay out-of-pocket before insurance kicks in) for collision and comprehensive coverage can lower your monthly premiums, but means more expense at the time of a claim. Balancing these choices is key to finding the right protection for your budget, whether you’re staying in luxury hotels or choosing more budget-friendly accommodation options for your extended [California] tour.

Location, Location, Location: Urban vs. Rural Rates

Just as real estate prices vary dramatically across [California], so do car insurance rates based on your specific location. Cities with higher population densities, increased traffic congestion, and higher rates of vehicle theft or vandalism typically have higher insurance premiums. For example, drivers in densely populated areas like downtown [Los Angeles] or [San Francisco]’s Financial District will likely pay more than those residing in more suburban or rural areas such as [Sacramento] or the Central Valley.

The number of accidents, the prevalence of uninsured motorists, and even the cost of medical care and auto repairs in a specific zip code can influence rates. If you’re contemplating a move to [California], or even choosing where to stay for an extended period, understanding how your chosen neighborhood impacts insurance costs can be a significant factor in your overall lifestyle budget. Exploring the historical charm of [Old Town San Diego] might have different insurance implications than parking near [Pier 39] in [San Francisco].

Practical Tips for Saving on Car Insurance in California

While car insurance is a necessary expense, there are numerous strategies drivers can employ to help mitigate costs without sacrificing essential coverage. These tips are especially relevant for travelers who might want to reallocate savings to experiences like visiting [Alcatraz Island] or exploring the wonders of [Death Valley National Park], or for new residents looking to optimize their monthly expenses.

Bundling and Discounts: Smart Strategies for Lower Premiums

One of the most effective ways to save on car insurance is by bundling your policies. Many insurers offer significant discounts when you purchase multiple insurance products from them, such as car insurance combined with renters insurance (crucial for those living in apartments or long-term accommodation) or homeowners insurance. This consolidation often results in a lower overall premium for all policies.

Beyond bundling, a wide array of discounts are often available:

- Good Driver Discount: For maintaining a clean driving record over a specified period.

- Multi-Car Discount: For insuring more than one vehicle with the same provider.

- Student Discounts: For high school or college students who maintain good grades.

- Defensive Driving Course Discount: For completing an approved safety course.

- Safety Feature Discounts: For vehicles equipped with anti-lock brakes, airbags, anti-theft devices, or advanced driver-assistance systems.

- Low Mileage Discount: If you don’t drive frequently, perhaps relying on public transport or working from home, you might qualify for lower rates.

- Loyalty Discount: For staying with the same insurer for an extended period.

- Payment Discounts: For paying your premium in full, opting for automatic payments, or receiving documents electronically.

Always ask your insurance provider about all available discounts. A few minutes of inquiry could lead to substantial annual savings, freeing up funds for more adventures, like a visit to the iconic [Hollywood Sign] or a leisurely stroll along the [Santa Monica Pier].

Choosing the Right Policy: Understanding Your Options

The cheapest policy isn’t always the best. It’s crucial to find a balance between affordability and adequate protection. Start by getting quotes from multiple insurance providers. The competitive [California] market means rates can vary significantly between companies for the same coverage. Online comparison tools and independent insurance agents can be invaluable resources in this process.

When reviewing quotes, don’t just compare the bottom line. Look closely at the coverage limits, deductibles, and any exclusions. Consider what level of risk you’re comfortable with. For example, if you have an older car with low market value, you might consider dropping collision and comprehensive coverage to save money, as the cost of these coverages might outweigh the potential payout. However, if you have a newer, valuable vehicle, these coverages are usually indispensable.

Understanding your needs, your driving habits, and your comfort with risk will guide you in selecting a policy that offers the best value. This informed decision-making extends beyond just insurance; it’s a critical part of planning any aspect of your [California] lifestyle, from choosing the right accommodation (be it a luxury villa or a charming boutique hotel) to budgeting for unique experiences like a visit to [Hearst Castle] or the [Monterey Bay Aquarium].

Beyond the Premium: Car Insurance as Part of Your California Lifestyle Budget

Car insurance, while a significant line item, should be viewed as an integral part of your overall financial strategy for living or extensively traveling in [California]. It’s not merely a transaction; it’s an investment in your peace of mind and your ability to fully immerse yourself in the [Golden State]’s diverse offerings. From family trips to business stays, managing this cost effectively allows for greater flexibility in other areas of your budget.

Budgeting for Exploration: From Los Angeles to San Francisco

The cost of car insurance directly impacts your discretionary spending for tourism and travel. A lower premium means more funds available for exploring [California]’s myriad attractions. Imagine saving a few hundred dollars on your annual premium; that could translate into a weekend getaway to [Lake Tahoe], an extra night at a charming hotel in [Napa Valley], or tickets to a major event in [Los Angeles] or [San Francisco]. For those who love local culture and food, these savings could fund numerous culinary adventures, from fine dining experiences to sampling street tacos in [San Diego].

When planning your itinerary, consider how your vehicle and insurance costs factor into the overall picture. If you’re on a budget travel plan, selecting an economical car and a carefully chosen insurance policy can significantly reduce your daily overhead, allowing you to stretch your resources further to experience more of [California]’s unique destinations.

Long-Term Stays and Accommodation: Integrating Insurance Costs

For individuals planning long-term stays, perhaps utilizing extended-stay apartments or considering a move to [California], car insurance becomes a monthly recurring expense, much like rent, utilities, or groceries. Integrating this cost into your comprehensive budget is essential for financial stability. When comparing accommodation options, whether it’s a high-rise apartment in [Los Angeles] or a sprawling villa in [Southern California], remember that your insurance rates will also be tied to that location.

Careful planning ensures that your car insurance doesn’t become an unexpected burden. By understanding the factors that influence rates, diligently seeking discounts, and choosing the right coverage, you can effectively manage this essential expense. This proactive approach not only keeps you legally compliant but also frees up your resources to fully enjoy the unparalleled travel, tourism, and lifestyle opportunities that make [California] such a captivating destination. From the iconic landmarks like the [Griffith Observatory] to the natural wonders of [Big Sur], a well-managed car insurance policy is your ticket to truly experiencing the freedom and adventure of the [Golden State].