Florida, the Sunshine State, beckons with its pristine beaches, vibrant cities, and endless adventure. From the magical theme parks of Orlando to the historic charm of St. Augustine and the breathtaking natural beauty of the Florida Keys, it’s a destination that captivates millions. Whether you’re planning a luxurious escape, a budget-friendly family trip, or even considering a long-term stay or relocation, the freedom to explore Florida often hinges on having a reliable set of wheels. This invariably brings up a crucial, often overlooked, aspect of planning your Florida experience: car insurance.

For many, the question “How much is car insurance in Florida?” is more than just a passing thought; it’s a significant financial consideration that impacts everything from daily commutes to epic road trips along the Florida Keys Scenic Highway. Understanding the landscape of car insurance in Florida is essential, not just for residents but also for snowbirds, long-term visitors, and even those renting vehicles for short-term travel. The state has a unique approach to auto insurance, and the costs can vary widely depending on a myriad of factors. This comprehensive guide will help you navigate the complexities, demystify the expenses, and equip you with the knowledge to make informed decisions, ensuring your adventures in Florida are as smooth and worry-free as possible.

Understanding Florida’s Unique Insurance Landscape

Florida stands out with its distinctive approach to auto insurance, primarily centered around its “no-fault” system. This system significantly influences the types of coverage required and, consequently, the overall cost of car insurance in the state. To fully grasp how much you might pay, it’s vital to first understand these foundational elements.

The No-Fault System Explained

At the heart of Florida’s auto insurance requirements is its no-fault system. This means that regardless of who caused an accident, your own insurance company is responsible for paying for your medical expenses and certain other costs, up to the limits of your Personal Injury Protection (PIP) coverage. This system was designed to reduce litigation and ensure that accident victims receive prompt medical attention without lengthy legal battles to determine fault.

While the no-fault system aims to streamline claims for injuries, it doesn’t absolve drivers of responsibility for property damage. If you cause an accident, your property damage liability (PDL) coverage will kick in to cover damage to the other party’s vehicle or property. Similarly, if someone else causes an accident, their PDL coverage would cover damage to your vehicle. This dual approach means that while medical care is handled on a no-fault basis, property damage still follows a fault-based system. Understanding this distinction is crucial for appreciating why certain types of coverage are mandatory in Florida.

Mandatory Coverage Requirements

Florida law mandates specific types of car insurance coverage for all registered vehicles. These requirements are in place to ensure that all drivers have a basic level of financial protection in the event of an accident.

-

Personal Injury Protection (PIP): This is the cornerstone of Florida’s no-fault system. Drivers are required to carry a minimum of $10,000 in PIP coverage. As mentioned, PIP covers 80% of your medical expenses, 60% of lost wages, and 100% of replacement services (like hiring someone to do household tasks you can’t perform) resulting from an injury in an accident, regardless of who was at fault. It’s important to note that this $10,000 limit can be quickly exhausted in serious accidents, which is why many drivers opt for higher limits or additional medical coverage.

-

Property Damage Liability (PDL): Florida requires a minimum of $10,000 in PDL coverage. This pays for damage you cause to another person’s property, such as their vehicle, fences, or other structures, if you are at fault in an accident. While $10,000 might seem like a substantial amount, the cost of repairing or replacing modern vehicles can easily exceed this minimum, especially if you damage a luxury car or multiple vehicles.

What’s notable about Florida’s mandatory coverage is what it doesn’t require: Bodily Injury Liability (BIL) and Uninsured/Underinsured Motorist (UM/UIM) coverage are not mandatory. BIL pays for medical expenses and lost wages for others if you cause an accident. While not legally required, most insurance experts and financial advisors strongly recommend carrying sufficient BIL coverage to protect your assets in the event of a severe accident where you are at fault. Similarly, UM/UIM coverage protects you if you’re hit by a driver who has no insurance or insufficient insurance, a unfortunately common scenario in Florida. This flexibility in mandatory requirements means that while minimum coverage can be relatively inexpensive, opting for adequate protection will inevitably increase your premiums, but significantly enhance your peace of mind while cruising through destinations like Miami or Tampa.

Key Factors Influencing Your Florida Car Insurance Premiums

While Florida’s no-fault system and mandatory coverage provide a baseline, the actual amount you pay for car insurance is highly individualized. Numerous factors come into play, creating a wide spectrum of premiums across the state. Understanding these variables is crucial for anyone trying to budget for car insurance, whether you’re a long-term resident enjoying the senior lifestyle in Sarasota or a young professional exploring career opportunities in Jacksonville.

Where You Live: City vs. Suburban Costs

One of the most significant determinants of your car insurance premium in Florida is your precise location within the state. Urban areas generally face higher rates than suburban or rural ones. Cities like Miami, Fort Lauderdale, and Orlando typically have higher population densities, increased traffic congestion, and a greater likelihood of accidents, theft, and vandalism. More vehicles on the road mean more opportunities for incidents, leading insurers to charge higher premiums.

For example, a driver in bustling Miami-Dade County might pay significantly more than a driver in a more tranquil area like Naples or a small town in the Florida Panhandle. Even within a large metropolitan area, specific ZIP codes can influence rates. Areas with higher crime rates or a greater frequency of traffic accidents will see higher premiums. This means that if you’re considering a move or a long-term stay, investigating car insurance costs specific to potential neighborhoods should be part of your accommodation planning, alongside checking out various resorts and apartments.

Your Driving Profile and Vehicle Choice

Beyond location, your personal driving history and the type of vehicle you insure play an enormous role in determining your premiums.

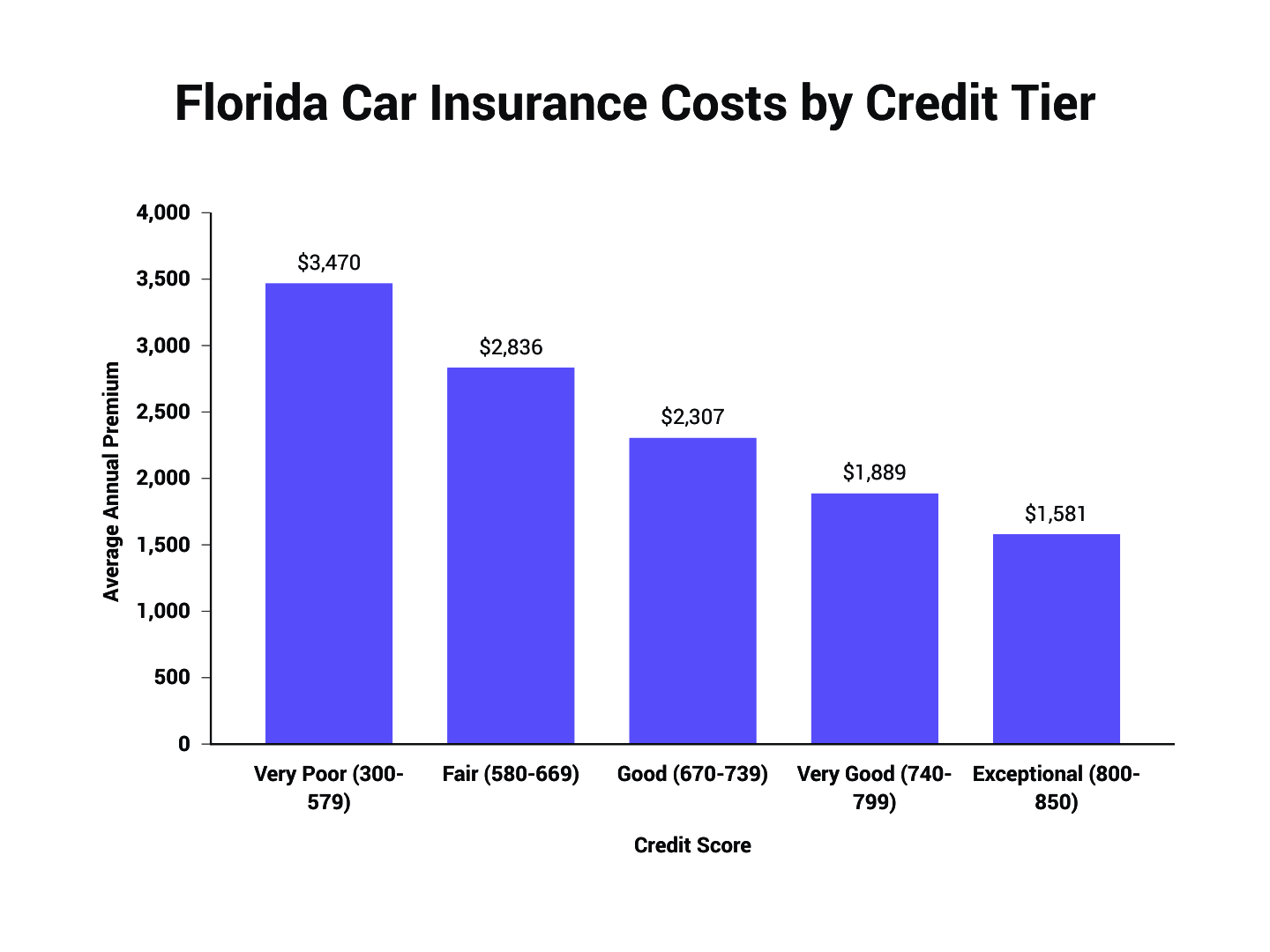

- Driving History: This is perhaps the most obvious factor. A clean driving record—free of accidents, speeding tickets, or other violations—will almost always result in lower premiums. Drivers with a history of at-fault accidents or multiple moving violations are considered high-risk and will face substantially higher rates. Insurers typically look back three to five years when assessing your record.

- Age and Experience: Younger, less experienced drivers (especially those under 25) generally pay more for insurance due to higher statistical accident rates. As drivers gain experience and mature, their rates tend to decrease, assuming a clean record. Seniors, too, might see rate fluctuations, with some insurers offering discounts and others adjusting rates based on age-related risk factors.

- Vehicle Make and Model: The car you drive is another major factor. Insurers consider several aspects:

- Cost of Repairs: Expensive or luxury vehicles (Rolls-Royce, Lamborghini, Porsche) are more costly to repair or replace, leading to higher comprehensive and collision premiums.

- Safety Features: Vehicles with advanced safety features (e.g., automatic emergency braking, lane-keeping assist) can qualify for discounts due to their potential to prevent or mitigate accidents.

- Theft Rates: Certain car models are more frequently targeted by thieves, leading to higher comprehensive coverage costs.

- Engine Size/Performance: High-performance cars often come with higher premiums, as they are statistically associated with more risky driving behaviors.

For families planning a trip to Walt Disney World Resort in a minivan or a couple embarking on a romantic getaway to Key West in a convertible, the specific vehicle choice can have a noticeable impact on insurance costs, particularly for rental agreements.

Beyond the Basics: Optional Coverages for Peace of Mind

While Florida’s mandatory PIP and PDL coverages provide a basic safety net, most drivers opt for additional coverages to protect themselves more comprehensively. These optional coverages can significantly increase your premium but offer invaluable peace of mind, especially when navigating the bustling streets of tourist hot spots or the quiet, winding roads of the Everglades National Park.

- Bodily Injury Liability (BIL): As mentioned, this is not mandatory but highly recommended. It covers medical expenses, lost wages, and pain and suffering for others if you are at fault in an accident. Minimums usually start at $10,000 per person/$20,000 per accident (10/20), but many financial experts advise much higher limits, such as $100,000 per person/$300,000 per accident (100/300), to adequately protect your assets.

- Uninsured/Underinsured Motorist (UM/UIM): This coverage protects you and your passengers if you are hit by a driver who either has no insurance or insufficient insurance to cover your damages. Given the number of uninsured drivers in Florida, UM/UIM is a crucial addition, covering medical bills and lost wages that your PIP might not fully address.

- Collision Coverage: This pays for damage to your own vehicle resulting from an accident, regardless of who is at fault. It’s often required if you have a car loan or lease.

- Comprehensive Coverage: This covers damage to your car from non-collision events, such as theft, vandalism, fire, hail, falling objects, or hitting an animal. Like collision, it’s typically required for financed or leased vehicles.

- Medical Payments (MedPay): Similar to PIP, MedPay covers medical expenses for you and your passengers, regardless of fault, and can often fill gaps where PIP might fall short, or if you have a high deductible on your health insurance.

- Rental Car Reimbursement: This covers the cost of a rental car while your vehicle is being repaired after a covered accident.

- Roadside Assistance: Provides help for breakdowns, flat tires, lockouts, or running out of gas.

Adding these coverages can push your average monthly premium from around $150–$200 for minimum coverage to $250–$400 or more for full coverage, depending on all the factors discussed. The peace of mind, however, is often worth the investment, especially when you consider the potential costs of an accident without adequate protection.

Navigating Insurance for Your Florida Lifestyle

Whether you’re visiting Florida for a short vacation, planning an extended stay in a cozy villa, or making the Sunshine State your new home, understanding how car insurance integrates with your specific lifestyle is paramount. The needs of a tourist renting a car differ vastly from those of a new resident establishing roots in a new community like Gainesville or Tallahassee.

For the Tourist: Rental Car Insurance Considerations

Tourists flocking to Florida’s attractions like Universal Orlando Resort or the white sands of Clearwater Beach often rely on rental cars for their mobility. The question of rental car insurance can be confusing, but it’s vital to address before you hit the road.

When renting a car in Florida, you’ll typically be offered various insurance products at the counter:

- Loss Damage Waiver (LDW) or Collision Damage Waiver (CDW): This isn’t technically insurance, but a waiver that relieves you of financial responsibility if the rental car is damaged or stolen. It often covers the car itself, not liability for other vehicles or injuries.

- Liability Insurance (Supplemental Liability Insurance – SLI): This provides additional liability coverage beyond the state minimums that the rental company might carry, protecting you if you cause an accident resulting in damage or injury to others.

- Personal Accident Insurance (PAI): This offers medical and accidental death benefits for you and your passengers.

- Personal Effects Coverage (PEC): Covers loss or damage to your personal belongings while in the rental car.

Before purchasing these, check your existing coverage:

- Personal Auto Policy: Your personal car insurance policy might extend coverage to a rental car. Specifically, your collision and comprehensive coverage might cover damage to the rental vehicle, and your liability might extend to protect you from claims from other parties. Review your policy documents or call your insurer to confirm the specifics of your coverage in Florida.

- Credit Card Benefits: Many credit cards, especially premium travel cards, offer secondary (or sometimes primary) rental car insurance benefits. This typically covers damage or theft of the rental vehicle if you pay for the rental with that card. Again, check with your credit card issuer for details, as terms and conditions can vary widely.

- Travel Insurance: Some comprehensive travel insurance policies may include rental car protection.

In many cases, your existing coverage might make purchasing all the rental counter insurance unnecessary, saving you a considerable amount on your travel budget. However, if you lack sufficient personal auto insurance or want maximum protection, opting for the rental company’s offerings can provide complete peace of mind, allowing you to focus on enjoying Everglades National Park or the lively streets of South Beach.

For the New Resident: Establishing Coverage in the Sunshine State

Relocating to Florida, whether for retirement, a new job, or simply to embrace the relaxed lifestyle, involves a host of practical considerations beyond finding the perfect apartment or villa. Establishing car insurance is a critical step, as you’ll need to meet Florida’s specific requirements to register your vehicle and obtain a Florida driver’s license.

- Transferring Your Policy vs. Getting a New One:

- Many national insurance carriers operate in Florida. If your current insurer does, inquire about transferring your policy. They will update your address and adjust your coverage to meet Florida’s specific PIP and PDL requirements.

- If your current insurer doesn’t operate in Florida, or if you’re looking for potentially better rates, you’ll need to obtain a new policy from a Florida-licensed insurer.

- Gathering Documentation: Be prepared to provide your new Florida address, driver’s license information (even if it’s from another state initially), vehicle identification number (VIN), and details of your driving history.

- Understanding Rate Changes: Be aware that your premiums might change significantly when you move to Florida. Factors like Florida’s unique no-fault system, the specific city you choose to live in, and local traffic patterns can all impact your rates, even if your driving history remains unchanged. It’s wise to get quotes before you move to factor this into your budget.

- Registering Your Vehicle: Once you have proof of Florida car insurance (which must meet the minimum PIP and PDL requirements), you can proceed with registering your vehicle at a local Florida Department of Highway Safety and Motor Vehicles (FLHSMV) office. You’ll also need to get a Florida driver’s license.

Transitioning your car insurance is a crucial aspect of settling into your new Florida lifestyle, ensuring you can legally and safely drive to your new favorite local spots, from the bustling markets of West Palm Beach to the serene landscapes of Sanibel Island.

Strategic Savings: Tips for Lowering Your Premiums

No one wants to pay more than necessary for car insurance. Fortunately, there are several strategies you can employ to potentially lower your premiums in Florida, ensuring you have more money for experiences, whether that’s a luxury travel adventure or exploring local culture and food.

- Shop Around and Compare Quotes: This is perhaps the most effective tip. Insurance rates can vary wildly between companies for the exact same coverage. Obtain quotes from multiple insurers – national carriers, regional companies, and even local agencies. Online comparison tools can streamline this process. It’s recommended to do this annually, even if you’re happy with your current provider.

- Increase Your Deductibles: A deductible is the amount you pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. Choosing a higher deductible (e.g., $1,000 instead of $500) will lower your premium. Just ensure you have enough savings to cover that deductible if you need to file a claim.

- Ask About Discounts: Insurance companies offer a wide array of discounts. Don’t be afraid to ask your agent about all available options:

- Multi-Policy Discount: Bundling auto insurance with homeowners, renters, or life insurance policies from the same provider.

- Good Driver Discount: For maintaining a clean driving record over a certain period.

- Good Student Discount: For young drivers who maintain a B average or better.

- Defensive Driving Course Discount: Completing an approved defensive driving course.

- Vehicle Safety Features Discount: For cars with anti-lock brakes, airbags, anti-theft devices, etc.

- Low Mileage Discount: If you don’t drive many miles annually.

- Payment Discounts: For paying in full, setting up auto-pay, or choosing paperless billing.

- Loyalty Discount: For staying with the same insurer for many years.

- Maintain a Clean Driving Record: This cannot be overstated. Avoiding accidents and traffic violations is the single best way to keep your premiums low over the long term. Even minor infractions can lead to surcharges.

- Choose the Right Car: As discussed, the type of car you drive significantly impacts rates. Research insurance costs for different models before purchasing a new vehicle. Safer, less expensive-to-repair cars generally have lower premiums.

- Review Your Coverage Regularly: As your life circumstances change (e.g., your car gets older, you pay off your car loan, children leave home), your insurance needs may evolve. You might be able to drop collision and comprehensive coverage on an older, low-value car, for instance, or adjust your liability limits.

By strategically applying these tips, you can often find significant savings, making your Florida lifestyle more affordable and allowing you to invest more in exploring the state’s incredible destinations, enjoying local cuisine, or relaxing at luxurious hotels.

In conclusion, understanding “How much is car insurance in Florida?” requires delving into the state’s unique no-fault system, appreciating the mandatory coverage requirements, and recognizing the multitude of factors that influence individual premiums. From your specific location in the state to your driving history, vehicle choice, and the optional coverages you select, each element plays a role in the final cost. Whether you’re a tourist considering rental car insurance for a visit to Busch Gardens Tampa Bay, a new resident navigating the complexities of establishing coverage, or a seasoned local looking to save, being informed is your best tool. By shopping wisely, maintaining a good driving record, and leveraging available discounts, you can secure adequate protection without overspending, ensuring your time exploring the diverse landscapes and vibrant culture of Florida is always safe, enjoyable, and financially sound.