Navigating the Sunshine State often conjures images of pristine beaches, vibrant theme parks, and a relaxed lifestyle. However, for anyone planning to drive their own vehicle, or even rent one, understanding the cost of car insurance in Florida is a crucial part of budgeting. The Sunshine State, with its unique driving landscape, presents a distinct set of factors that influence monthly premiums. This guide aims to demystify the costs associated with car insurance in Florida, breaking down the key elements that contribute to your premium and offering insights to help you make informed decisions, whether you’re a permanent resident or a frequent visitor planning your next adventure from the convenience of your own car.

Understanding the Factors Driving Florida Car Insurance Costs

The cost of car insurance is rarely a one-size-fits-all figure. In Florida, a combination of state-mandated requirements, geographic considerations, individual driving habits, and vehicle specifics all play a significant role in determining your monthly premium. Unlike some other states, Florida has unique laws and a higher prevalence of certain risks that insurance companies factor into their pricing models.

State-Mandated Coverage and Its Impact

Florida operates under a no-fault insurance system, which means that regardless of who is at fault in an accident, your own insurance policy will cover your medical expenses and lost wages up to a certain limit. This system is a fundamental driver of insurance costs.

- Personal Injury Protection (PIP): This is the cornerstone of Florida‘s no-fault system. Every Florida driver is legally required to carry at least $10,000 in PIP coverage. This coverage pays for 80% of your necessary medical expenses and 60% of your lost wages, regardless of who caused the accident. The mandatory nature and the coverage limits of PIP directly contribute to the baseline cost of car insurance in the state.

- Property Damage Liability (PDL): While Florida is a no-fault state for bodily injury, you are still required to have PDL coverage. This covers damage to other people’s property in an accident where you are at fault. The minimum required PDL coverage in Florida is $10,000.

These minimums are the bare minimum required by law. Many drivers opt for higher coverage limits to ensure adequate protection, which, naturally, will increase their monthly premiums.

Geographic Influences: Where You Live Matters

The “where” of your Florida address has a substantial impact on your car insurance rates. Certain regions within the state are statistically more prone to accidents, theft, and severe weather events, leading to higher premiums for residents in those areas.

- High-Risk Areas: Cities and counties along the coast, particularly in South Florida, often see higher insurance costs. This is due to several factors, including a higher population density, increased traffic, and a greater susceptibility to hurricanes and other severe weather. For example, residents in Miami-Dade County might pay more than those in more rural inland areas.

- Weather-Related Risks: Florida is no stranger to hurricanes, tropical storms, and hailstorms. These events can cause widespread damage to vehicles, leading to a higher volume of claims for insurance companies. Areas that experience more frequent or severe weather events will generally have higher insurance premiums.

- Traffic Density and Crime Rates: Densely populated urban areas often experience higher rates of traffic accidents and vehicle theft. Insurance providers analyze these statistics when setting rates, making coverage in cities like Orlando, Tampa, or Jacksonville potentially more expensive than in smaller towns.

When considering where to reside in Florida, or if you’re planning a long-term stay in an apartment or villa, factoring in the local insurance rates is a practical step.

Individual Factors: Your Driving Record and Profile

Beyond state laws and geographic location, your personal circumstances are paramount in determining your car insurance premium. Insurance companies view individual drivers through a lens of risk assessment.

- Driving Record: This is arguably the most significant individual factor. A clean driving record, free of accidents and traffic violations, will result in lower premiums. Conversely, speeding tickets, DUIs, reckless driving charges, and at-fault accidents will lead to substantial increases in your rates. Insurers want to see a history of safe and responsible driving.

- Age and Gender: Younger, less experienced drivers, particularly males under 25, generally pay higher premiums. This is statistically attributed to a higher incidence of accidents in this demographic. As drivers gain experience and age, premiums tend to decrease. While gender-based pricing is becoming less common in some areas, it can still be a factor.

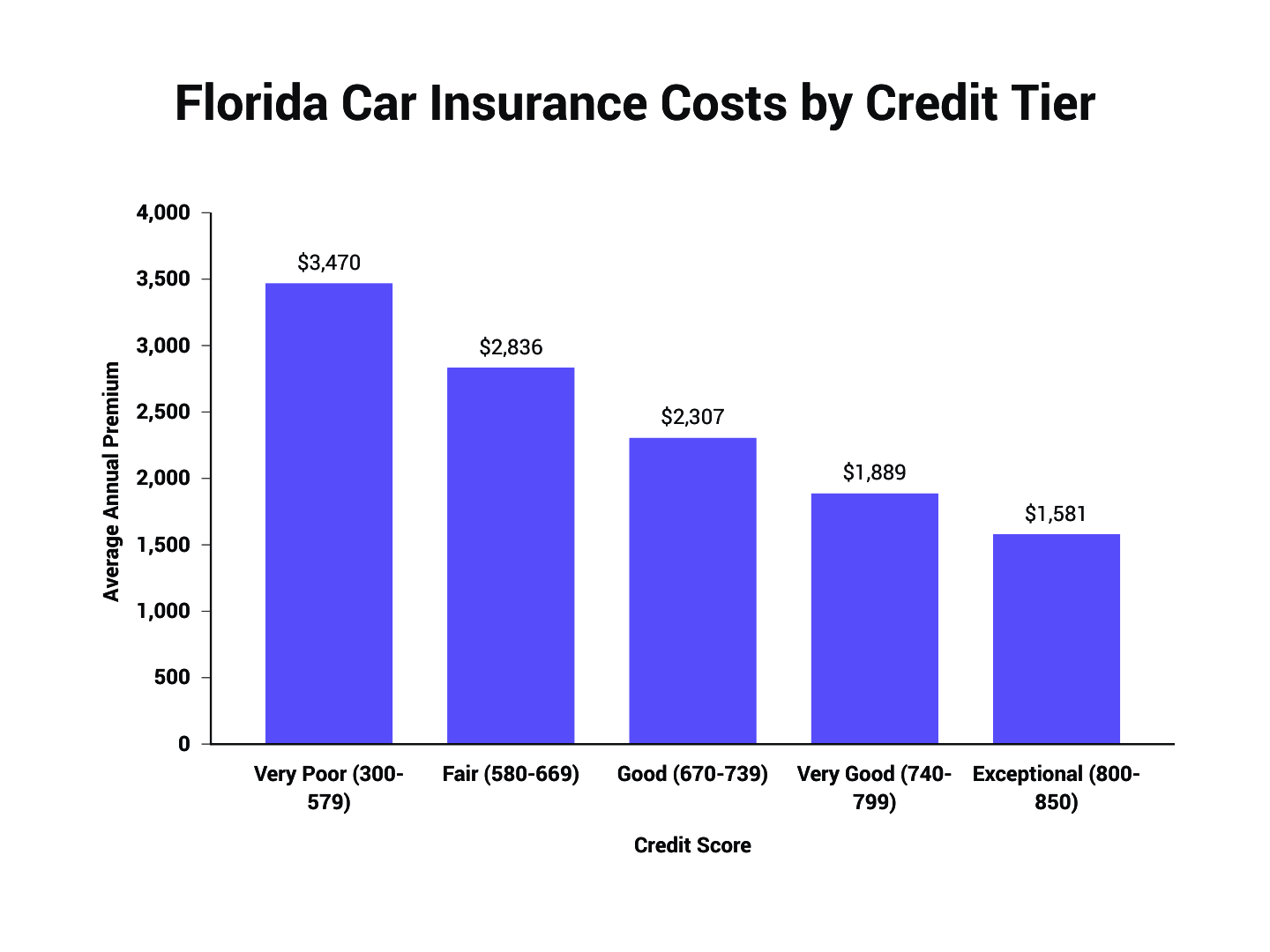

- Credit Score: In many states, including Florida, credit history is used as a predictor of insurance risk. Individuals with good credit scores are often seen as more responsible and less likely to file claims, leading to lower premiums. Conversely, a poor credit score can result in higher insurance costs.

- Marital Status: Statistically, married individuals tend to have lower accident rates than single individuals, which can sometimes translate into slightly lower insurance premiums.

- Coverage Choices and Deductibles: The types and levels of coverage you choose, beyond the state-mandated minimums, will directly impact your monthly cost. Opting for comprehensive and collision coverage, which protect your vehicle, will increase your premium. Similarly, choosing lower deductibles (the amount you pay out-of-pocket before insurance kicks in) will also raise your monthly payments, as the insurer assumes more risk. Conversely, higher deductibles will lower your premium.

Common Scenarios and Their Impact on Monthly Costs

The average monthly cost of car insurance in Florida can vary widely. However, understanding typical scenarios can provide a clearer picture. These figures are general estimates and can fluctuate significantly based on the factors mentioned above.

Average Monthly Premiums in Florida

As of recent data, the average monthly cost of car insurance in Florida can range from approximately $150 to $250 or even higher. This broad range reflects the diverse factors at play. For example, a young driver with a history of tickets living in a coastal city might pay upwards of $300-$400 per month, while a mature, married driver with a spotless record and a good credit score in a less populated inland area might pay closer to $100-$150 per month for similar coverage.

Factors Affecting Premiums for Different Driver Types

- New Drivers: For teenagers or newly licensed drivers, expect significantly higher premiums. Their lack of driving experience is viewed as a considerable risk. Bundling them onto a parent’s policy can sometimes mitigate costs compared to a standalone policy, but it will still increase the overall premium.

- Drivers with a History of Accidents or Tickets: If you have recent accidents, especially at-fault ones, or multiple traffic violations, your premiums will be considerably higher. Insurance companies may even label you as a high-risk driver, leading to limited policy options and elevated costs. You might need to seek out specialized insurers.

- Seniors: While experienced drivers, senior citizens might sometimes see a slight increase in premiums due to age-related factors that can affect reaction times. However, their extensive driving history and generally lower risk profile often keep their rates lower than younger drivers.

- Non-US Residents: For tourists or those who are not permanent residents, the situation can be different. If you’re renting a car, the rental company’s insurance will likely be offered, which can be quite expensive. If you own a car in Florida as a non-resident, you will still be subject to the same state laws and pricing factors.

Strategies to Lower Your Florida Car Insurance Costs

While Florida‘s insurance rates can be higher than the national average, there are several effective strategies to reduce your monthly outlays without compromising on necessary coverage. Proactive measures and smart shopping can lead to significant savings.

Bundling and Discounts

Many insurance providers offer discounts to customers who bundle multiple policies or demonstrate safe driving habits.

- Multi-Policy Discounts: Insuring your car and your home or renters insurance with the same company often leads to a discount on both policies. This is a common and effective way to save money.

- Safe Driver Discounts: Maintaining a clean driving record for a specified period can earn you a safe driver discount. Some insurers also offer telematics programs that monitor your driving habits via a smartphone app or device, rewarding safe driving with further discounts.

- Good Student Discounts: If you have a young driver on your policy who is a full-time student and maintains a good GPA, you might qualify for a good student discount.

- Defensive Driving Courses: Completing an approved defensive driving course can sometimes qualify you for a discount, especially if you have a minor traffic violation.

Reviewing Your Coverage and Deductibles

Regularly assessing your insurance needs is crucial. What you needed five years ago might not be what you need today.

- Adjusting Coverage Limits: While it’s important to have adequate coverage, ensure you’re not over-insured, especially on older vehicles. If your car is worth less than your annual insurance premium, it might be time to consider dropping comprehensive and collision coverage.

- Increasing Deductibles: As mentioned earlier, a higher deductible means you’ll pay more out-of-pocket in the event of a claim, but it will lower your monthly premium. Carefully assess your financial situation to determine a deductible amount you can comfortably afford.

- Vehicle Type: The type of car you drive also influences rates. Sports cars and vehicles with high theft rates generally incur higher premiums than sedans or minivans.

Shopping Around and Comparing Quotes

Perhaps the most impactful strategy for saving money on car insurance in Florida is to compare quotes from multiple insurance providers regularly.

- Don’t Stick with One Insurer: Loyalty doesn’t always pay when it comes to car insurance. Prices can vary significantly between companies for the exact same coverage. It’s advisable to get new quotes at least once a year, or whenever you experience a life change that might affect your rates (e.g., moving, adding a driver, a change in driving record).

- Use Online Comparison Tools: Numerous online platforms allow you to compare quotes from various insurers simultaneously, streamlining the process. However, always ensure you are comparing policies with identical coverage levels and deductibles for an accurate comparison.

- Consider Local Agents: Independent insurance agents can be invaluable. They can access quotes from multiple companies and help you understand the nuances of different policies, ensuring you get the best value for your money.

By understanding the factors that influence car insurance costs in Florida and proactively employing these cost-saving strategies, you can significantly reduce your monthly expenses while ensuring you have the necessary protection on the road, allowing you to fully enjoy the diverse attractions and experiences the Sunshine State has to offer, whether it’s exploring the art deco district of Miami Beach, visiting Walt Disney World in Orlando, or enjoying a relaxing stay at a resort in the Florida Keys.