Florida, the Sunshine State, beckons millions of visitors annually with its pristine beaches, world-class theme parks, vibrant cities, and a lifestyle synonymous with warmth and relaxation. From the magic of Orlando to the Art Deco charm of Miami Beach and the laid-back allure of Key West, Florida offers an unparalleled array of travel experiences and desirable locations for long-term stays or even permanent relocation. Whether you dream of a luxurious beachfront villa, a cozy retirement apartment, or a family-friendly resort vacation, the state’s diverse accommodation options and iconic landmarks cater to every taste.

However, beneath the idyllic facade lies a significant reality: Florida is uniquely vulnerable to natural disasters, particularly flooding. For anyone considering purchasing property, planning an extended stay, or even just understanding the nuances of local life, grasping the intricacies and costs of flood insurance is not merely a bureaucratic detail – it’s a critical component of financial prudence and peace of mind. This guide aims to demystify the question, “How much is flood insurance in Florida?”, exploring the factors that influence its cost and offering insights relevant to travelers, property owners, and those envisioning a life in this beautiful, yet exposed, corner of the United States.

Understanding Florida’s Elevated Flood Risk: More Than Just Hurricanes

To truly appreciate the necessity and cost of flood insurance in Florida, one must first understand the geological and meteorological realities that make the state so prone to water-related hazards. It’s not just about the occasional hurricane; it’s a constant interplay of natural elements.

Why Florida is Prone to Flooding

Florida’s geography is its primary determinant of flood risk. The state is essentially a low-lying peninsula, bordered by the Atlantic Ocean to the east and the Gulf of Mexico to the west. This extensive coastline, combined with generally flat terrain, means that large portions of the land are just a few feet above sea level. This low elevation makes it highly susceptible to storm surge – a phenomenon where strong winds from tropical storms and hurricanes push seawater inland, inundating coastal areas.

Beyond coastal surge, Florida’s subtropical climate brings heavy rainfall, especially during the wet season and from passing tropical depressions. The state is crisscrossed by an intricate network of rivers, lakes, and wetlands, including the vast Everglades ecosystem. When heavy rains combine with existing high water tables, rivers can overflow their banks, and urban drainage systems can become overwhelmed, leading to widespread inland flooding. Even a localized thunderstorm can cause significant street flooding in densely populated areas. Furthermore, rapid urban development has sometimes replaced natural wetlands and permeable surfaces with concrete and asphalt, exacerbating runoff issues and reducing the land’s natural capacity to absorb excess water.

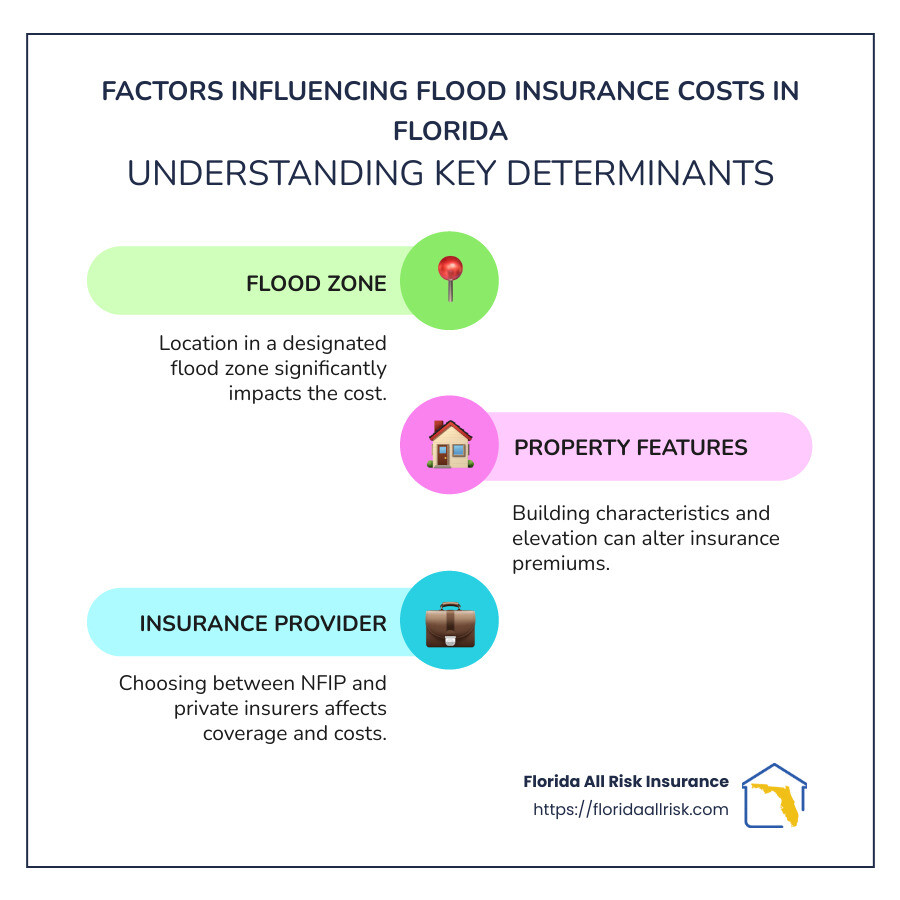

The National Flood Insurance Program (NFIP) and Private Options

Historically, flood damage was largely excluded from standard homeowners’ insurance policies because of the catastrophic and widespread nature of floods. To address this gap, the U.S. Congress established the National Flood Insurance Program (NFIP) in 1968. Administered by the Federal Emergency Management Agency (FEMA), the NFIP remains the primary source of flood insurance for property owners in participating communities across the United States, including virtually all of Florida. A key aspect of the NFIP is that it makes flood insurance available to property owners in communities that adopt and enforce floodplain management ordinances, which are designed to reduce future flood losses.

In recent years, spurred by increased awareness of flood risk and technological advancements, a private flood insurance market has begun to emerge. These private policies can sometimes offer more comprehensive coverage, higher limits, or more competitive pricing than the NFIP, particularly for properties outside the highest-risk flood zones. This growing competition provides property owners in Florida with more options, making it crucial to compare offerings from both the NFIP and private insurers to find the best fit.

Factors Influencing Flood Insurance Premiums in the Sunshine State

The cost of flood insurance in Florida is not a fixed number; it’s a highly individualized calculation based on a multitude of factors. Understanding these elements is key to deciphering your potential premium.

Location, Location, Location: Flood Zones Explained

The most significant factor influencing flood insurance premiums has traditionally been the property’s flood zone designation, as determined by FEMA flood maps. These maps delineate areas based on their risk of flooding, with different zones indicating varying probabilities of a flood occurring within a given period.

- High-Risk Zones (e.g., A, V zones): These are areas with a 1-in-4 chance of flooding over a 30-year mortgage. Properties in these zones are typically required to have flood insurance if they have a federally backed mortgage. Premiums here are the highest due to the elevated risk. V zones, specifically, are coastal areas with additional hazards from storm wave action. Many of Florida’s iconic coastal destinations like Naples, Miami Beach, and barrier islands fall into these categories.

- Moderate-to-Low Risk Zones (e.g., B, C, X zones): While not typically mandatory for federally backed mortgages, flood insurance is still highly recommended in these areas. Around 25% of all NFIP claims and one-third of federal disaster assistance for flooding occur in these “lower risk” zones. The cost of insurance in these zones is significantly lower, making it a highly cost-effective safeguard. Even cities further inland, like parts of Orlando, can experience flooding, demonstrating that no area is entirely immune.

Property Characteristics and Building Practices

Beyond the flood zone, the specific characteristics of the property itself play a crucial role in determining the premium.

- Elevation: For structures in high-risk flood zones, the elevation of the lowest floor relative to the Base Flood Elevation (BFE) is paramount. Homes built above the BFE will generally have lower premiums than those built below it, reflecting the reduced risk of water entering the living space.

- Foundation Type: Properties with different foundation types (slab, crawlspace, pilings/columns) are rated differently. Homes elevated on stilts or pilings, common in coastal areas, often face lower premiums if properly constructed to allow floodwaters to pass underneath.

- Construction Materials: The materials used in construction, especially those resistant to flood damage, can also factor into the overall risk assessment.

- Age and Design: Older homes, particularly those built before modern floodplain management regulations were in place, may face higher premiums if they do not meet current elevation or construction standards. The presence of flood vents, which allow water to flow freely through enclosed areas like crawlspaces or garages, can also positively impact rates.

Coverage Limits and Deductibles

Like other insurance policies, the amount of coverage you choose and your deductible will directly impact your premium.

- Building Coverage: This covers the physical structure of your home, including its foundation, walls, electrical and plumbing systems, and permanently installed fixtures. The NFIP offers up to $250,000 in building coverage for residential properties.

- Contents Coverage: This protects your personal belongings, such as furniture, electronics, clothing, and other valuables. The NFIP provides up to $100,000 in contents coverage, which must be purchased separately from building coverage.

- Deductibles: Choosing a higher deductible (the amount you pay out-of-pocket before your insurance kicks in) will result in a lower annual premium. However, it means you’ll pay more upfront if a flood occurs. It’s a balance between annual savings and potential out-of-pocket expenses during a claim.

NFIP’s Risk Rating 2.0: A New Era of Pricing

The National Flood Insurance Program (NFIP) introduced a new pricing methodology called Risk Rating 2.0: Equity in Action, which began implementation in 2021. This significant overhaul aims to make flood insurance rates more equitable and reflective of individual property risk, moving away from a system heavily reliant on broad flood zone classifications.

Risk Rating 2.0 considers a wider array of flood risk factors specific to each property, including:

- Individual property elevation: Not just compared to a base flood elevation, but precise elevation relative to ground level.

- Distance to water sources: Such as rivers, lakes, and coastlines.

- Types of flooding: For example, riverine, storm surge, heavy rainfall, or coastal erosion.

- Building characteristics: Foundation type, elevation of machinery, and other structural features.

- Cost to rebuild: Rather than simply the value of the property.

This new system means that properties with similar flood zone designations might now have vastly different premiums, reflecting their unique flood vulnerabilities. While some property owners in Florida may see their rates decrease, others might experience increases, especially those in historically undervalued high-risk areas. Risk Rating 2.0 represents a more sophisticated and precise approach to pricing flood risk, making it even more important for property owners to understand their specific risk profile.

Navigating the Costs: What to Expect and How to Save

Given the complex interplay of factors, providing an exact figure for flood insurance in Florida is impossible. However, we can offer general ranges and strategies to help you navigate the costs.

Average Costs: A Broad Overview (with caveats)

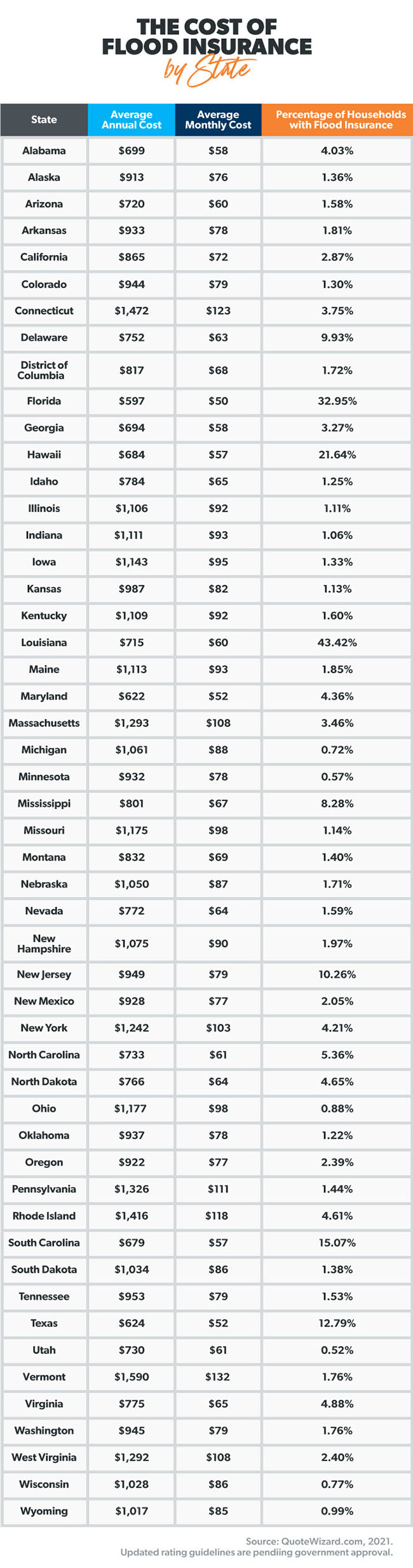

Before Risk Rating 2.0, the average NFIP premium in Florida was often cited in the range of $700 to $1,000 annually. However, this average masked significant variations, with properties in low-to-moderate risk zones paying as little as a few hundred dollars, while those in high-risk zones, particularly along the coast, could face premiums of several thousand dollars or more per year.

With Risk Rating 2.0, these averages are in flux. FEMA anticipates that approximately one-third of policyholders will see an immediate decrease in their premiums, while another third will see a modest increase, and the remaining third will see more significant increases. The overall goal is to ensure that premiums more accurately reflect the true flood risk of each individual property.

For example, a home in a historically low-risk area that is now identified as having a specific, albeit infrequent, flood risk due to its proximity to a small creek might see an increase. Conversely, a home in a high-risk zone that is well-elevated and built with robust mitigation features might see a decrease or a less dramatic increase than properties with similar flood zone designations but inferior construction.

Private flood insurance policies, while not subject to the same rate structures as the NFIP, will also price based on similar risk factors but may use proprietary models. Their pricing can sometimes be more competitive for certain properties, especially those that benefit from specific risk mitigation efforts.

Strategies for Reducing Your Flood Insurance Bill

While some factors are beyond your control, several strategies can help reduce your flood insurance costs:

- Obtain an Elevation Certificate (EC): This document, prepared by a licensed surveyor, verifies your home’s elevation relative to the Base Flood Elevation. It’s crucial for accurate rating under both the old and new NFIP systems, and particularly useful for properties in high-risk zones. A favorable EC can significantly lower your premium.

- Implement Mitigation Efforts: Elevating your home, installing flood vents in enclosed areas, elevating utilities (water heaters, HVAC systems), and improving drainage around your property can all reduce flood risk and, consequently, your insurance costs. Many communities offer grants or resources for such improvements.

- Shop Around: While the NFIP is a primary provider, always compare its offerings with those from private flood insurance companies. The private market can sometimes provide more flexible coverage or lower premiums, especially for properties where the NFIP’s rates are high.

- Understand Your Community’s Rating (CRS): The Community Rating System (CRS) is an NFIP program that provides discounts on flood insurance premiums for policyholders in communities that implement floodplain management practices that exceed the NFIP’s minimum requirements. Communities can earn points for activities like preserving open space, enforcing higher regulatory standards, and providing flood hazard information. The better your community’s CRS rating, the higher the discount for its residents.

- Choose a Higher Deductible: If you’re comfortable with a larger out-of-pocket expense in the event of a flood, opting for a higher deductible can lower your annual premium.

- Ensure Proper Zoning and Permitting: When building or renovating, adhere strictly to local floodplain management regulations and obtain all necessary permits. Non-compliance can lead to higher rates or even denial of coverage.

Important Considerations for Travelers and Property Seekers

For those visiting or considering a property in Florida, understanding flood insurance extends beyond mere compliance:

- For Short-Term Visitors: If you’re planning a vacation, particularly during hurricane season (June to November), ensure your travel insurance policy covers trip interruptions, cancellations, or medical emergencies due to natural disasters like hurricanes or floods. While flood insurance directly applies to property, understanding the risk helps inform travel planning.

- For Vacation Home Buyers/Long-Term Stays: Due diligence on flood risk and insurance costs is paramount. A property’s flood zone and the associated insurance premium can significantly impact its overall affordability and long-term investment value. Before making an offer, get an insurance quote and review the FEMA flood maps for the specific address. Don’t assume flood insurance is included in your standard homeowners’ policy.

- Impact on Real Estate Decisions: High flood insurance premiums can make a property less desirable or harder to sell. Conversely, a well-mitigated property with a reasonable flood insurance cost in a desirable area offers significant peace of mind and value. When considering properties in popular areas like Key West or Miami Beach, where much of the land is low-lying, flood insurance will be a non-negotiable part of the cost of ownership.

Conclusion

The question “How much is flood insurance in Florida?” doesn’t have a simple answer, but it’s one of the most vital inquiries for anyone looking to embrace the Florida lifestyle. As a state renowned for its beauty and tourist appeal, Florida also demands respect for its natural vulnerabilities. While an additional cost, flood insurance is not just a regulatory requirement for many; it’s an indispensable safeguard that protects your most significant investments and ensures financial resilience against nature’s unpredictable forces.

Whether you’re exploring Florida’s countless attractions, dreaming of a luxurious resort stay, or planning a long-term relocation to its vibrant communities, understanding the nuances of flood risk and insurance empowers you to make informed decisions. Proactive research, engagement with insurance professionals, and a commitment to flood mitigation efforts can significantly influence your premiums and, more importantly, provide the ultimate peace of mind. By addressing this critical aspect of property ownership and residency, you can truly enjoy all that the Sunshine State has to offer, without the looming worry of unforeseen flood damage.