Texas, the Lone Star State, beckons travelers and adventurers from all corners of the globe. Its vast landscapes, from the sun-drenched beaches of the Gulf Coast to the rugged beauty of Big Bend National Park, offer an unparalleled diversity of experiences. Whether you’re drawn to the vibrant music scene of Austin, the historical richness of San Antonio, the bustling urban energy of Dallas and Houston, or the tranquil charm of a small town in the Texas Hill Country, Texas promises a lifestyle as grand as its reputation.

For many, a visit to Texas evolves into a desire for a longer stay, perhaps even the dream of owning a piece of this iconic state. Whether it’s a charming historic home, a modern city apartment, a sprawling ranch, or a cozy vacation rental, finding the perfect accommodation is a crucial part of embracing the Texas lifestyle. And for anyone considering making Texas their home – be it a primary residence, a seasonal escape, or an investment property – understanding the nuances of home insurance is as vital as exploring its famous landmarks or savoring its legendary barbecue.

Home insurance in Texas is not merely a formality; it’s a critical financial safeguard, shaped by the state’s unique geography, climate, and diverse property landscape. Unlike some areas where insurance costs might be more uniform, Texas presents a complex picture, with premiums varying significantly based on location, property type, and the specific risks prevalent in different regions. This guide aims to demystify home insurance costs in Texas, helping you make informed decisions whether you’re transitioning from a luxury hotel suite to your own Texas abode, or simply curious about the financial aspects of a long-term stay in the Lone Star State. We’ll explore the factors that influence these costs, what typical coverage entails, and how to navigate the options to secure your investment and peace of mind, allowing you to fully immerse yourself in all that Texas has to offer.

Embracing the Texas Lifestyle: What Influences Home Insurance Premiums?

The allure of Texas often begins with its diverse appeal. From the bustling cultural hubs to serene natural escapes, the state caters to every preference. However, this very diversity also plays a significant role in determining how much you’ll pay for home insurance. The factors that influence premiums are deeply intertwined with the lifestyle choices one makes when settling in Texas.

Geographic Diversity and Natural Elements

Texas is a land of extremes, not just in its vibrant culture and wide-open spaces, but also in its weather patterns. This geographical and meteorological diversity is the primary driver of varying home insurance costs across the state.

For instance, properties along the Gulf Coast, in cities like Galveston or Corpus Christi, face a heightened risk of hurricanes, tropical storms, and associated flooding. The scenic beauty of these coastal destinations, often enjoyed by tourists flocking to charming resorts and beachfront villas, comes with the caveat of needing robust, specialized insurance coverage. Homeowners in these areas often require separate windstorm and hail insurance, typically provided by the Texas Windstorm Insurance Association (TWIA), in addition to standard homeowners policies and potentially flood insurance through the National Flood Insurance Program (NFIP). These additional coverages significantly increase the overall cost of protecting a coastal property, but are non-negotiable for anyone dreaming of a seaside escape or a permanent residence by the water.

Moving inland to major metropolitan areas like Dallas, Fort Worth, Austin, and San Antonio, the risks shift. While these cities are popular tourist destinations with rich cultural scenes and a plethora of accommodation options, they are also situated in “Hail Alley” and “Tornado Alley.” This means residents frequently experience severe thunderstorms, large hail, and tornadoes. Consequently, insurance premiums in North Texas and Central Texas often reflect the high likelihood of roof and property damage from these events. Many standard homeowners policies cover wind and hail, but the frequency and intensity of these storms can lead to higher deductibles or increased premiums over time.

Further west, in regions like El Paso and West Texas, the climate is more arid, reducing the risk of hurricanes and significant flooding. Here, the concerns might lean more towards wildfires, particularly in areas bordering natural landscapes, or even dust storms. The comparative absence of frequent large-scale catastrophic weather events can sometimes translate to slightly lower premiums for the basic perils, although property age and specific location risks will always play a role. Understanding these regional distinctions is paramount for anyone planning their ultimate Texas lifestyle, whether it involves urban exploration or remote retreats.

Property Types and Accommodation Choices

The type of property you choose in Texas is another major determinant of your home insurance costs. This is directly relevant for those moving from temporary hotel stays to more permanent accommodations.

- Older Homes vs. New Constructions: A charming historic home in San Antonio’s King William District, while offering unparalleled character and proximity to cultural landmarks, may come with higher insurance costs. Older plumbing, electrical systems, and roofing can be more prone to issues, leading to higher claims and thus higher premiums. Insurers often view newer constructions, especially those built to modern building codes with updated materials, as lower risk.

- Urban Lofts vs. Suburban Houses vs. Rural Ranches: A modern condominium or loft in downtown Houston or Dallas typically has different insurance needs compared to a single-family home in the suburbs or a sprawling ranch in the countryside. Condo insurance (HO-6 policy) primarily covers the interior of your unit and your personal belongings, as the building’s master policy usually covers the exterior and common areas. This can sometimes be less expensive than a full homeowners policy (HO-3 or HO-5) for a standalone house, which covers the entire structure and land. Rural properties, while offering space and tranquility, might face higher premiums due to greater distance from fire departments or potential risks like brush fires.

- Vacation Homes and Rental Properties: If your Texas dream involves a vacation home on South Padre Island or a rental property in Austin, the insurance landscape changes. Vacation homes, often unoccupied for extended periods, are generally considered higher risk by insurers and can incur higher premiums. Similarly, if you plan to rent out your property, you’ll need a landlord policy (DP-3), which covers different perils than a standard homeowners policy, focusing more on the structure and liability specific to a rental situation. These considerations are vital for those looking to invest in the flourishing Texas tourism and accommodation market.

Your Travel and Residency Plans

Your intent behind owning property in Texas also directly impacts insurance. Are you relocating permanently, seeking a part-time retreat, or investing in the thriving tourism industry?

- Primary Residence: For a home where you live most of the year, standard HO-3 or HO-5 policies are applicable. Insurers prefer primary residences because they are typically occupied, reducing the risk of vandalism, unnoticed damage, or theft.

- Secondary/Vacation Home: A property designated as a secondary or vacation home often incurs higher premiums. The perceived risk of a vacant property is greater, and insurers may require specific endorsements or separate policies to cover it adequately. This is an important consideration for those who travel extensively or split their time between Texas and another location.

- Investment/Rental Property: As mentioned, a property purchased with the intent to generate rental income, whether long-term or short-term (like a VRBO or Airbnb), requires a different type of insurance. Landlord policies protect against risks associated with tenants, property damage, and liability claims from renters or their guests. This is particularly relevant for individuals looking to capitalize on Texas’s robust tourism economy by offering unique accommodation experiences.

Understanding these intertwined factors – from the regional weather patterns across the Texas Panhandle to the Rio Grande Valley to the specific characteristics of your chosen dwelling and how you plan to use it – is the first step in estimating your home insurance costs and securing your piece of the Texas dream.

Navigating the Numbers: Average Costs and Coverage Types in the Lone Star State

Once you understand the factors influencing home insurance premiums in Texas, the next logical step is to delve into the actual costs and the types of coverage available. This section provides a practical guide to what you can expect financially when it comes to protecting your Texas home, whether it’s a temporary base or a long-term investment.

What to Expect: Average Premiums Across Texas

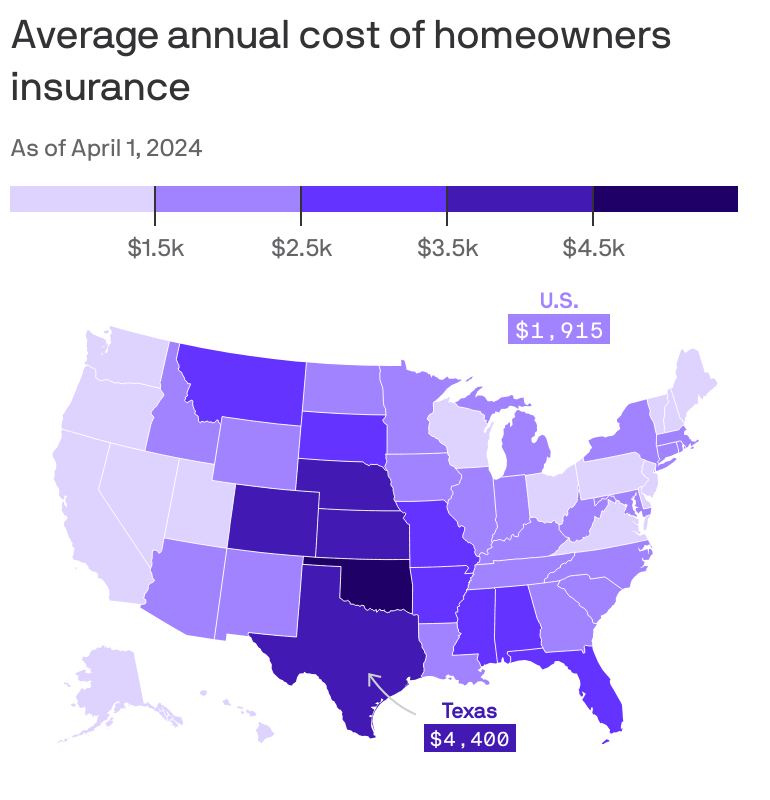

It’s challenging to provide a single average for home insurance in Texas due to the vast disparities mentioned earlier. However, general estimates suggest that the average annual premium for homeowners insurance in Texas typically falls between $2,500 and $4,000. This is notably higher than the national average, primarily due to the state’s exposure to severe weather events.

- Coastal Regions: Expect the highest premiums here. In cities like Galveston, Corpus Christi, or areas along the Upper Texas Coast, the combined cost of a standard homeowners policy, windstorm insurance (through TWIA), and potentially flood insurance could push annual costs well over $5,000, sometimes even reaching $8,000 or more, especially for high-value properties in high-risk flood zones. These costs are a direct reflection of the significant risk of hurricane damage that has impacted the region, a vital consideration for anyone considering a picturesque beachfront retreat.

- Major Metro Areas (Houston, Dallas, Austin, San Antonio): Premiums in these vibrant urban centers, which attract countless tourists and new residents, usually fall within the $2,500 to $3,500 range. While they don’t face the same hurricane risk as coastal areas, they are susceptible to hail and tornado damage, which keeps premiums elevated. Proximity to emergency services (fire departments) and crime rates within specific neighborhoods can also influence costs. For those exploring the unique cultures and landmarks of these cities, understanding these local insurance dynamics is key to planning a sustainable lifestyle.

- West Texas and the Panhandle: In regions like El Paso or Amarillo, where major weather catastrophes are less frequent, premiums might be on the lower end of the state average, possibly in the $1,800 to $2,800 range. However, risks like wildfires, particularly in areas bordering ranches or undeveloped land, can still factor into the pricing.

It’s crucial to remember that these are averages. Your actual premium will depend on numerous personalized factors, including your home’s age and construction, roof type, claims history, chosen deductible, and specific coverage limits. When planning your accommodation in Texas, getting multiple quotes is always recommended.

Beyond the Basics: Essential Coverage for Texas Homeowners

Standard homeowners insurance policies (typically HO-3 or HO-5 for comprehensive coverage) in Texas are designed to protect your most significant asset. They typically include several key components:

- Dwelling Coverage: This protects the physical structure of your home (walls, roof, foundation, built-in appliances) against covered perils like fire, wind, hail, vandalism, and theft. For anyone moving from the transient comfort of a hotel to the permanence of a home, this coverage is fundamental.

- Other Structures Coverage: This covers detached structures on your property, such as garages, sheds, fences, and guesthouses – amenities that can significantly enhance a Texas property.

- Personal Property Coverage: This protects your belongings inside your home, including furniture, electronics, clothing, and other valuables. If you’ve collected unique souvenirs during your Texas travels or invested in decor reflecting the local culture, this ensures their protection.

- Loss of Use (Additional Living Expenses): If your home becomes uninhabitable due to a covered loss, this coverage helps pay for temporary living expenses, such as hotel stays, restaurant meals, and laundry services, allowing you to maintain a sense of normalcy during repairs. This is a crucial safety net for any homeowner, preventing the disruption from turning into a financial catastrophe.

- Personal Liability Coverage: This protects you if someone is injured on your property and you are found legally responsible. It also covers damage you or a household member accidentally cause to someone else’s property. Whether you’re hosting a backyard barbecue or entertaining guests, this provides invaluable peace of mind.

- Medical Payments Coverage: This pays for medical expenses for guests injured on your property, regardless of fault.

Special Considerations for Texas:

- Windstorm and Hail: Given the prevalence of severe weather, ensure your policy has adequate windstorm and hail coverage. Many standard Texas policies have a separate, higher deductible for wind and hail damage, often expressed as a percentage of your dwelling coverage (e.g., 1% or 2%).

- Flood Insurance: Standard homeowners policies do not cover flood damage. For properties in flood-prone areas, particularly along the Gulf Coast or near rivers and lakes, separate flood insurance through the National Flood Insurance Program (NFIP) or a private insurer is highly recommended, and often mandatory for mortgage holders. Understanding your property’s flood risk, which can be checked via FEMA flood maps, is an essential step when planning a move to Texas, especially if you’re drawn to waterfront properties or regions susceptible to heavy rainfall.

- Deductibles: Your deductible is the amount you pay out of pocket before your insurance coverage kicks in. Choosing a higher deductible can lower your annual premium, but it means you’ll pay more upfront in the event of a claim. It’s a balance between managing monthly costs and preparing for potential out-of-pocket expenses.

Securing the right coverage for your Texas home is about more than just checking a box; it’s about safeguarding your lifestyle, your investment, and your future in this magnificent state. It ensures that your Texas journey, from tourist to homeowner, is as secure and enjoyable as possible.

Smart Decisions for Your Texas Home: Tips for Saving on Insurance

Investing in a home in Texas is a dream for many, symbolizing a deeper connection to its rich culture and diverse landscapes. While home insurance is an unavoidable expense, especially given Texas’s unique risk profile, there are numerous strategies to manage and potentially reduce your premiums without compromising essential coverage. These tips are particularly valuable for those transitioning from budget-conscious travel to establishing a long-term presence in the Lone Star State.

Bundling and Discounts: Maximizing Your Savings

Just as savvy travelers seek out package deals and loyalty programs, smart homeowners can leverage bundling and various discounts to cut down insurance costs. This is often one of the most straightforward ways to achieve significant savings.

- Multi-Policy Discount (Bundling): One of the most common and effective ways to save is to purchase multiple insurance policies from the same provider. If you already have car insurance, life insurance, or even umbrella liability insurance, inquire about bundling your homeowners policy with them. Many insurers offer a substantial discount, often 10-20% off the total premium, for holding multiple policies. This not only streamlines your insurance management but also allows for a better overall rate, similar to how booking a flight and hotel together often costs less than booking separately.

- Security System Discounts: Enhancing the security of your Texas home is a win-win situation. Installing a monitored home security system, smoke detectors, carbon monoxide detectors, and even smart home technology that detects water leaks can qualify you for discounts. Insurers view these measures as reducing the likelihood of theft, fire, or significant property damage, thus lowering their risk. For those who frequently travel, a robust security system offers extra peace of mind, knowing your Texas base is protected.

- New Home Discounts: If you’re purchasing a newly constructed home in a burgeoning Texas community, you may be eligible for a new home discount. Newer homes are built to modern building codes, often featuring updated electrical systems, plumbing, and roofing materials, which are less prone to issues and thus less risky for insurers.

- Renovation and Upgrade Discounts: Even if your Texas home isn’t brand new, recent upgrades can lead to savings. Installing a new, impact-resistant roof (especially beneficial in hail-prone areas like Dallas or Fort Worth), updating outdated plumbing or electrical systems, or even replacing old windows with energy-efficient ones can make your home safer and more resilient, potentially reducing your premiums.

- Claim-Free Discount: Maintaining a clean claims history can earn you a discount over time. Insurers reward homeowners who haven’t filed claims for a certain period, reflecting a lower risk profile.

- Loyalty Discount: Staying with the same insurance provider for several years can also lead to loyalty discounts, as insurers value long-term customer relationships.

Always ask your insurance agent about all available discounts. A little research and proactive inquiry can uncover significant savings that contribute to your overall budget for experiencing the Texas lifestyle.

Risk Mitigation and Property Upgrades

Beyond discounts, actively managing and mitigating risks associated with your property can directly influence your insurance costs. This involves making strategic improvements to your home that reduce the likelihood or severity of potential damage.

- Fortify Your Roof: Given Texas’s susceptibility to hail and high winds, investing in an impact-resistant roof (e.g., Class 4 rated shingles) can lead to substantial discounts on your windstorm and hail premiums. This upgrade is particularly effective in areas frequently impacted by severe thunderstorms, safeguarding your home and potentially saving you thousands over the long run.

- Protect Against Wind Damage: For homes in coastal regions, installing storm shutters or hurricane clips can make your property more resilient to high winds, potentially reducing your windstorm insurance costs. This proactive approach is crucial for protecting your investment in popular coastal travel destinations like Galveston or Port Aransas.

- Manage Water Risks: Water damage, whether from burst pipes or leaks, is a common claim. Regularly inspecting and maintaining plumbing, and considering water leak detection systems, can prevent costly damage and potential future premium increases. This is especially important for properties that might be unoccupied during travel periods.

- Maintain Your Property: Simple, consistent maintenance goes a long way. Keeping trees trimmed away from your roof, ensuring gutters are clean to prevent water buildup, and addressing small repairs promptly can prevent minor issues from escalating into major claims. A well-maintained property signals lower risk to insurers.

- Review Your Coverage Annually: Life changes, and so do property values and insurance needs. Annually review your policy with your agent. Ensure your dwelling coverage accurately reflects the cost to rebuild your home (not its market value), and adjust personal property limits if you’ve acquired or disposed of significant assets. You might find you’re over-insured in some areas or under-insured in others.

By taking a proactive approach to property maintenance and leveraging available discounts, homeowners in Texas can significantly reduce the burden of insurance costs. This allows for more resources to be allocated towards enjoying the vibrant culture, exploring the breathtaking attractions, and truly experiencing the unique lifestyle that makes Texas such a beloved destination and a wonderful place to call home.

Your Texas Journey: From Tourist to Homeowner

The journey through Texas is often one of discovery and delight, whether you’re exploring the historic Alamo in San Antonio, enjoying the live music scene on Austin’s Sixth Street, or marveling at the vastness of the Davis Mountains. For many, this exploration sparks a deeper connection, transforming a temporary visit into a desire for a more permanent embrace of the Texas lifestyle.

Understanding home insurance in Texas is an indispensable step in this transition. It’s not just a financial obligation; it’s a foundational piece of securing your comfort, protecting your investment, and ensuring peace of mind as you settle into your Texas home. The varied costs and complex considerations reflect the state’s unique character – its diverse geography, dynamic climate, and the sheer scale of opportunities it presents for homeowners and investors alike.

From the specific risks associated with coastal living in Galveston to the hail concerns in Dallas and Fort Worth, every region of Texas presents its own insurance landscape. By carefully assessing these factors, comparing quotes from multiple reputable insurers, and actively seeking out discounts and making strategic home improvements, you can navigate these costs effectively.

Whether your Texas dream involves a bustling urban loft, a quiet suburban haven, or a sprawling rural retreat, securing appropriate home insurance allows you to focus on what truly matters: immersing yourself in the local culture, exploring hidden gems, and building lasting memories. This vital preparation ensures that your Texas home remains a sanctuary, a base from which to continue your adventures, and a cherished part of your life out of the box.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.