Navigating the landscape of home insurance in Texas can feel like charting a course through uncharted territory, especially when aiming for clarity on monthly premiums. While the initial query might revolve around a specific cost, the reality is that the answer is far from a single, definitive number. Instead, understanding the factors that influence your monthly Texas home insurance payments is key to making informed decisions, whether you’re settling into a new home or re-evaluating your existing coverage. This guide aims to demystify these costs, offering insights that can help you budget effectively and secure the right protection for your valuable asset, much like planning a memorable trip requires understanding various expenses.

The Lone Star State presents a unique set of challenges and opportunities when it comes to homeowners insurance. From its diverse climate, including the potential for severe weather events like hurricanes along the coast and hailstorms inland, to its booming real estate market, several elements contribute to the overall cost of insuring a property. Just as a luxurious resort stay in Cancun will have a different price point than a cozy guesthouse in the French countryside, home insurance rates in Texas are highly individualized.

Understanding the Core Components of Your Texas Home Insurance Premium

When you receive a quote for home insurance in Texas, it’s not an arbitrary figure. It’s a carefully calculated price based on a multitude of variables that insurance providers assess to gauge risk. Think of it like building an itinerary for a family trip; you consider accommodation, activities, and transportation, each contributing to the overall budget. Similarly, your insurance premium is an aggregation of several components designed to cover different aspects of potential loss.

Dwelling Coverage: Protecting Your House

At the heart of your homeowners insurance policy is dwelling coverage. This is the part that pays to repair or rebuild your home’s structure if it’s damaged by a covered event. This includes the walls, roof, foundation, and any attached structures like a garage. The amount of dwelling coverage you need is directly tied to the cost to rebuild your home from the ground up, not its market value. This is a crucial distinction. For instance, if you own a historic home in Galveston with unique architectural features, the cost to rebuild might be significantly higher than for a standard construction home, leading to a higher premium.

Factors influencing dwelling coverage costs include:

- Reconstruction Cost: This is the primary driver. Insurers use specialized software and local construction cost data to estimate how much it would cost to rebuild your home, considering materials, labor, and local building codes. A larger home or one with high-end finishes will naturally cost more to insure.

- Age and Condition of the Home: Older homes, especially those built before modern building codes, might carry higher risks and therefore higher premiums. Any deferred maintenance can also increase risk and costs.

- Construction Type: Homes built with brick or stone tend to be more durable and less susceptible to certain types of damage than wood-frame homes, potentially leading to lower premiums.

- Roof Type and Age: The material and age of your roof are significant. A newer, impact-resistant roof can lead to lower insurance rates, especially in hail-prone areas like Dallas or San Antonio.

Other Structures Coverage: Beyond the Main Residence

Beyond the primary dwelling, most policies include coverage for “other structures” on your property. This typically covers detached garages, sheds, fences, and gazebos. Similar to dwelling coverage, the amount is usually a percentage of your dwelling coverage, but it can be adjusted based on the value of these additional structures. If you have an elaborate workshop or a detached guest house, you’ll want to ensure this coverage is adequate. For those who enjoy outdoor living with extensive patio setups and landscaping in a sprawling Austin estate, this coverage becomes even more important.

Personal Property Coverage: Protecting Your Belongings

This coverage protects your personal belongings, such as furniture, electronics, clothing, and appliances, in the event of a covered loss. Most policies offer a baseline amount, often a percentage of your dwelling coverage, but you can increase this if you have valuable items like jewelry, art, or collectibles. Insurers often require a separate “rider” or endorsement for high-value items. If your personal property is extensive, perhaps reflecting a lifestyle of collecting fine art or designer furniture, you’ll want to consider a higher personal property limit.

Loss of Use Coverage: Keeping You Housed During Repairs

If a covered event makes your home uninhabitable, loss of use coverage (also known as additional living expenses) will pay for the temporary costs of living elsewhere. This can include hotel bills, restaurant meals, and other essential expenses while your home is being repaired. The limit for this coverage is usually a percentage of your dwelling coverage or a set dollar amount per day for a specified period. For families displaced from a home in a hurricane-prone area like Houston, this coverage is invaluable, providing peace of mind during a stressful time, akin to having a robust travel insurance plan for unexpected disruptions.

Liability Coverage: Protection from Claims

Liability coverage protects you financially if someone is injured on your property and sues you, or if you accidentally cause damage to someone else’s property. It can help pay for legal fees, medical bills, and settlements. Standard policies typically offer $100,000 or $300,000 in liability coverage, but many homeowners opt for higher limits, especially if they have significant assets to protect. Umbrella policies can provide even more coverage beyond your standard homeowners insurance.

Factors Influencing Texas Home Insurance Premiums

Now that we understand the components of a policy, let’s delve into the specific factors that influence how much you’ll pay per month for home insurance in Texas. These are the variables that insurance providers scrutinize to determine your risk profile.

Location, Location, Location: The Texas Weather Factor

Texas is a vast state with diverse weather patterns, and your location is arguably the most significant factor in determining your insurance premium.

- Coastal Areas: Homes along the Texas coast, from Galveston to Corpus Christi, face a higher risk of hurricane damage, windstorms, and flooding. This significantly increases insurance costs. Flood insurance is typically a separate policy but is often bundled or considered alongside homeowners insurance for coastal properties.

- Hail Alley: The central and northern parts of Texas, often referred to as “Hail Alley,” experience frequent and severe hailstorms. This can lead to substantial claims for roof and siding damage, driving up premiums for homes in areas like Fort Worth, Plano, and Lubbock.

- Tornado Risk: While not as concentrated as in some other states, Texas does experience tornadoes, particularly in the northern and eastern regions. The potential for tornado damage also plays a role in risk assessment.

- Wildfire Risk: Certain areas, especially in West Texas and the Hill Country, have a higher risk of wildfires, which can influence insurance costs.

Your Home’s Characteristics: A Deeper Dive

Beyond location, the physical characteristics of your home play a crucial role.

- Age and Condition: As mentioned earlier, older homes and those with outdated systems (electrical, plumbing, roofing) are often more expensive to insure. Regular maintenance and upgrades can help mitigate these costs.

- Building Materials: Homes constructed with less durable materials or those that are more susceptible to damage from wind, hail, or fire will naturally carry higher premiums.

- Roof Type and Age: The material and age of your roof are critical. Impact-resistant shingles and metal roofs can significantly reduce premiums, especially in hail-prone areas. A newer roof is always a plus for insurers.

- Swimming Pools and Trampolines: Features like swimming pools or trampolines can increase your liability risk, potentially leading to higher premiums. You might also be required to have specific safety features like fences around pools.

- Security Systems and Fire Protection: Homes equipped with monitored security systems, smoke detectors, and fire sprinklers may qualify for discounts, as these features can reduce the likelihood and severity of losses.

Your Insurance History and Credit Score

Insurers use various data points to assess your risk, and your personal history is a significant part of that.

- Claims History: If you have a history of filing frequent or large claims, your premiums will likely be higher. Insurers view this as an indicator of higher future risk.

- Credit-Based Insurance Score: In Texas, like many other states, insurance companies often use a credit-based insurance score to predict the likelihood of a future claim. Generally, individuals with higher credit scores tend to receive lower insurance premiums. This is based on statistical data that suggests a correlation between financial responsibility and claim behavior.

- Payment History: Consistent and on-time payments can sometimes lead to better rates or fewer penalties.

Coverage Choices and Deductibles

The amount of coverage you choose and the deductibles you select directly impact your monthly payments.

- Coverage Limits: The higher your dwelling coverage, other structures coverage, and personal property limits, the higher your premium will be. You need to balance adequate protection with affordability.

- Deductibles: Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. A higher deductible typically results in a lower monthly premium, and vice versa. For example, choosing a $2,500 deductible instead of a $1,000 deductible can lower your monthly cost. It’s important to select a deductible you can comfortably afford in the event of a claim.

Strategies for Lowering Your Texas Home Insurance Costs

While the factors above are largely set in stone once your home and location are determined, there are proactive steps you can take to potentially lower your monthly premiums. Think of these as smart planning tips for any travel experience, ensuring you get the best value.

Shop Around and Compare Quotes

This is perhaps the most effective strategy. Insurance rates can vary significantly between companies, even for the same level of coverage. Dedicate time to gather quotes from multiple reputable insurance providers. Consider working with an independent insurance agent who can compare policies from various companies on your behalf. This is akin to comparing hotel prices across different booking platforms to find the best deal for your stay in a charming bed and breakfast in San Miguel de Allende or a luxury resort in the Maldives.

Increase Your Deductible

As discussed, opting for a higher deductible can directly reduce your monthly premium. However, ensure you have sufficient savings to cover the deductible in case of a claim. This is a trade-off between a lower upfront cost and a higher out-of-pocket expense when needed.

Bundle Your Policies

Many insurance companies offer discounts when you bundle your home insurance with other policies, such as auto insurance. This “bundling discount” can lead to significant savings on both your home and auto premiums.

Improve Your Home’s Security and Safety Features

- Install a Security System: A professionally monitored alarm system can often earn you a discount.

- Upgrade Your Roof: As mentioned, a newer, impact-resistant roof can significantly reduce premiums, especially in hail-prone areas.

- Install Safety Devices: Having working smoke detectors, carbon monoxide detectors, and potentially sprinkler systems can also lead to discounts.

Maintain a Good Credit Score

Since Texas insurers often use credit-based insurance scores, maintaining a good credit history can contribute to lower premiums. Pay bills on time, reduce debt, and monitor your credit reports for errors.

Review Your Policy Annually

Don’t let your policy renew automatically without review. Your circumstances may have changed, or market rates might have shifted. An annual review allows you to assess if your coverage is still appropriate and if there are better rate options available. This is similar to re-evaluating your travel plans each year to see if new destinations or travel styles align better with your current interests.

The Monthly Breakdown: Estimating Your Texas Home Insurance Costs

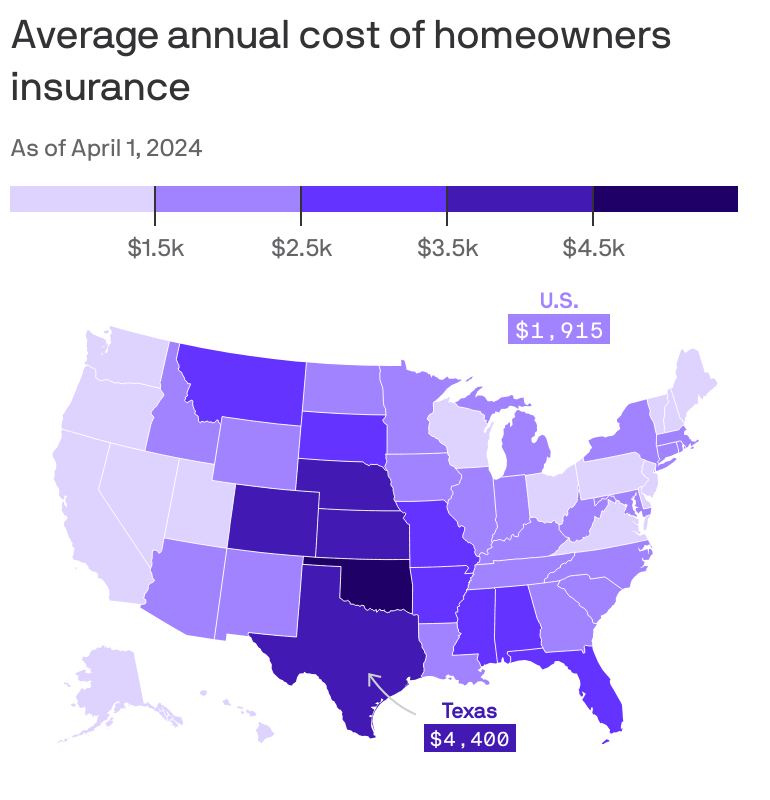

While providing an exact figure is impossible without a personalized quote, understanding the average cost can offer a benchmark. In Texas, the average cost of homeowners insurance can range from $1,000 to $4,000 or more annually, which translates to roughly $80 to $330+ per month. However, this is a broad average.

For example, a homeowner in a low-risk area with a newer, well-maintained home and a higher deductible might pay on the lower end of this spectrum, perhaps around $1,000-$1,500 annually ($83-$125 per month). Conversely, a homeowner in a coastal region with a higher risk of hurricanes, an older home, and lower deductibles could easily pay $3,000-$4,000 or even more annually ($250-$333+ per month).

Ultimately, the monthly cost of home insurance in Texas is a highly personalized figure. It’s a reflection of the risk an insurer takes on to protect your home, influenced by your location, the characteristics of your property, your personal insurance history, and the coverage you choose. By understanding these factors and employing smart strategies, you can work towards securing comprehensive protection at a rate that fits your budget, ensuring peace of mind for your most significant investment. Whether you’re looking for the perfect boutique hotel in Paris or planning to insure your dream home in San Angelo, informed decision-making is key.