Texas, the Lone Star State, is a land of vast horizons, vibrant culture, and diverse landscapes. From the bustling metropolitan areas of Houston and Dallas to the live music capital of Austin and the historic charm of San Antonio, it offers a unique blend of experiences for residents and visitors alike. Whether you’re considering a permanent move, investing in a vacation home, or planning an extended stay to explore its rich tourism offerings, understanding the financial aspects of homeownership, particularly house insurance, is paramount. This isn’t just a dry financial topic; it’s a fundamental part of the lifestyle and peace of mind for anyone making Texas their home, even if temporarily. The cost of home insurance in Texas can vary significantly, influenced by a unique combination of geographic risks, property characteristics, and individual choices. For travelers dreaming of relocating to this dynamic state or those already enjoying its diverse attractions, deciphering these costs is a crucial step in budgeting and securing their future in this exciting destination.

Understanding the Landscape of Home Insurance in the Lone Star State

Texas is as diverse in its geography as it is in its weather patterns, and both play a substantial role in determining the cost of home insurance. Unlike many other states, Texas has a highly competitive and somewhat complex insurance market due to its susceptibility to a wide array of natural disasters. This makes understanding the average costs and the factors that influence them incredibly important for anyone looking to settle down or invest in property here.

Average Costs: A Snapshot Across Texas

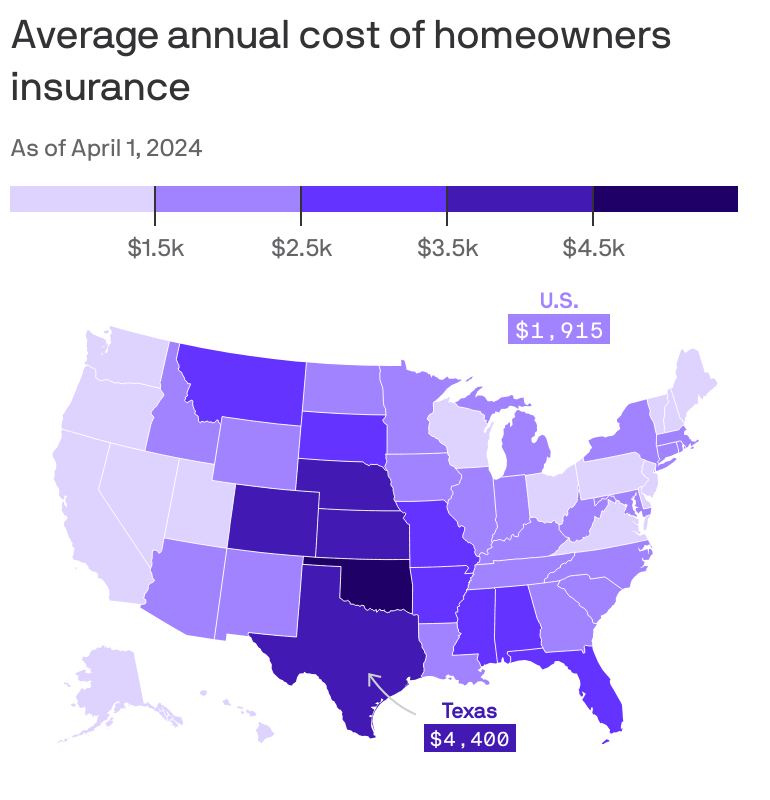

On average, homeowners in Texas might expect to pay anywhere from $2,500 to $4,500 annually for a standard home insurance policy. However, this is a broad average, and the reality is far more granular. The exact premium you pay can fluctuate wildly depending on where you are in the state and the specific characteristics of your home.

For instance, major metropolitan areas often present different average costs:

- In Houston, a city known for its proximity to the Gulf Coast and occasional flooding, premiums might lean towards the higher end of the spectrum, especially for properties in flood-prone zones, which would also require separate flood insurance.

- Dallas and Fort Worth in North Texas are frequently hit by hailstorms and tornadoes, driving up insurance costs related to wind and hail damage.

- Austin, while experiencing rapid growth and a desirable lifestyle, also faces its share of severe weather, influencing rates.

- San Antonio, with its rich history and attractions like the Alamo and the Riverwalk, might see slightly lower rates than coastal cities but still contends with regional weather challenges.

- Coastal cities like Galveston and Corpus Christi typically bear the highest burden due to the constant threat of hurricanes and tropical storms, making robust wind and hail coverage a necessity, often managed by the Texas Windstorm Insurance Association (TWIA) in some areas.

- In contrast, cities in West Texas, such as El Paso or Lubbock, might experience different risk profiles, perhaps more related to wildfires or less frequent but intense thunderstorms, leading to varying premium structures.

This regional variation means that anyone looking to purchase property, whether it’s a charming bungalow in College Station or a luxurious villa overlooking Lake Travis near Austin, must conduct thorough research specific to their chosen locale. It’s not just about the beauty of a destination or its amenities; it’s about understanding the practicalities of securing your investment.

Key Factors Influencing Your Premium

Beyond the general averages, several specific factors converge to determine your individual home insurance premium in Texas:

- Location, Location, Location: As mentioned, geographical risk is paramount. Properties on the Gulf Coast are more exposed to hurricanes, while those in “Tornado Alley” regions of North Texas or Central Texas face different threats. Even within a city, specific zip codes can have vastly different rates due to microclimates, proximity to fire stations, or historical claim data.

- Age and Construction of Your Home: Newer homes often cost less to insure because they are built to more stringent codes, potentially more resistant to certain perils, and feature modern electrical and plumbing systems. The type of construction material also matters. A brick home might be less susceptible to wind damage than a siding home, for instance. The age and condition of the roof, in particular, are huge drivers of cost given the prevalence of hail damage.

- Coverage Limits and Deductibles: The more coverage you opt for (e.g., higher dwelling coverage, more personal property coverage), the higher your premium will be. Similarly, your deductible – the amount you pay out of pocket before your insurance kicks in – has a direct impact. A higher deductible typically means a lower premium, but it also means more out-of-pocket expense in the event of a claim. In Texas, you’ll often see separate deductibles for wind/hail damage, which can be a percentage of your dwelling coverage, significantly impacting your costs.

- Your Personal Claim History: A history of filing multiple claims, especially for preventable incidents, can signal higher risk to insurers, leading to increased premiums.

- Your Credit Score: In Texas, like many other states, insurance companies often use a credit-based insurance score as one factor in determining premiums. A higher score typically correlates with lower premiums, as it’s often seen as an indicator of responsible financial behavior.

- Safety and Security Features: Homes equipped with features like security systems, smoke detectors, carbon monoxide detectors, sprinkler systems, and even smart home technology can qualify for discounts, as these mitigate risks of theft, fire, or other perils.

Understanding these factors allows potential homeowners and long-term renters to make informed decisions, not just about their insurance but about where they choose to live and the type of property they invest in. It’s an integral part of making a wise accommodation choice in Texas, whether for a lifestyle change or an investment property.

Navigating Texas’ Unique Risks and Coverage Options

The charm and allure of Texas are undeniable, drawing in millions for its dynamic cities, beautiful natural landmarks like Big Bend National Park and Guadalupe Mountains National Park, and its unique cultural experiences. However, the state’s geographical position also exposes it to a challenging array of natural phenomena. These aren’t just isolated incidents; they are an inherent part of the Texas experience, impacting everything from tourism seasons to the fundamental cost of living, particularly home insurance.

The Texas Weather Phenomenon: A Major Cost Driver

Texas is often described as a microcosm of America’s weather, experiencing everything from scorching droughts to devastating floods, and from blizzards to hurricanes. This diverse and often extreme weather directly translates into higher insurance premiums for homeowners.

- Hurricanes and Tropical Storms: The Gulf Coast of Texas, encompassing popular tourist destinations like Galveston and South Padre Island, is highly vulnerable to hurricanes. These powerful storms bring not only destructive winds but also torrential rains and storm surges, causing widespread damage. As a result, homeowners in these regions often face separate, percentage-based deductibles for wind and hail damage, or may even need to acquire windstorm coverage through the Texas Windstorm Insurance Association (TWIA) if private insurers deem the risk too high. These events can severely impact travel and tourism, leading to temporary closures of hotels, resorts, and attractions along the coast.

- Tornadoes: The central and northern parts of Texas, including major population centers like Dallas, Fort Worth, and Waco, lie within “Tornado Alley,” making them susceptible to violent spring and summer storms. These can cause catastrophic damage in minutes, tearing apart homes and infrastructure. Insurance policies must adequately cover wind damage from these events.

- Hailstorms: Perhaps the most common and costly weather peril in Texas is hailstorms. Cities like Plano, Frisco, and Irving in the Dallas-Fort Worth metroplex frequently experience large hailstones, leading to extensive roof and property damage. This widespread damage drives up insurance claims statewide and contributes significantly to higher premiums.

- Wildfires: While less frequent in urban areas, parts of Central Texas and West Texas are prone to wildfires, especially during hot, dry summers. These can be devastating, destroying homes and natural habitats, and posing a risk to national parks and outdoor recreation areas. Homeowners in these more rural or semi-rural areas need to ensure their policies cover fire damage comprehensively.

- Flooding: Crucially, standard homeowners insurance policies do not cover flood damage. Given that many parts of Texas – including Houston, San Antonio, and areas along rivers and bayous – are susceptible to flash flooding and riverine flooding, a separate flood insurance policy is often a critical necessity. This is typically purchased through the National Flood Insurance Program (NFIP) or private insurers. The impact of flooding can be severe, not only for homes but also for local businesses, hotels, and tourist attractions, disrupting travel plans and local economies.

For individuals planning their lifestyle in Texas, especially for long-term stays or property ownership, understanding these risks and the necessary coverage is not merely a financial decision but a practical one. It ensures that the appeal of Texas’ diverse attractions, from the NASA Johnson Space Center to Padre Island National Seashore, can be enjoyed with the peace of mind that comes from proper preparation.

Essential Coverage Types for Texas Homeowners

A typical homeowners insurance policy in Texas is a package policy, combining several types of coverage to protect your home and finances. Understanding each component is vital:

- Dwelling Coverage: This is the core of your policy, covering the cost to repair or rebuild the physical structure of your home (the house itself, attached garages, foundations, etc.) if it’s damaged by a covered peril like fire, wind, hail, or vandalism. The amount of coverage should ideally be enough to rebuild your home from the ground up at current construction costs.

- Other Structures Coverage: This protects unattached structures on your property, such as detached garages, sheds, fences, and gazebos. It’s usually a percentage (e.g., 10%) of your dwelling coverage.

- Personal Property Coverage: This covers your belongings inside your home, including furniture, clothing, electronics, and appliances, against covered perils. It can be provided on an actual cash value (depreciated value) or replacement cost (cost to replace new) basis, with replacement cost being more expensive but offering better protection. For those who frequently travel or have valuable collections acquired during their journeys, ensuring adequate coverage for personal property is especially important.

- Loss of Use (Additional Living Expenses): If your home becomes uninhabitable due to a covered loss, this coverage helps pay for temporary living expenses, such as hotel stays (like a Hyatt Regency or a local boutique hotel), meals, and other increased costs while your home is being repaired. This is particularly valuable in Texas where severe weather can displace many families simultaneously.

- Personal Liability Coverage: This protects you financially if someone is injured on your property or if you accidentally cause damage to someone else’s property, covering legal fees and settlement costs up to your policy limit. This is crucial for hosts who may have guests or for general peace of mind during social gatherings at home.

- Medical Payments to Others: This covers medical expenses for guests injured on your property, regardless of fault, up to a specified limit.

- Specific Endorsements/Riders: In Texas, you might consider adding endorsements for specific protections not covered by a standard policy, such as:

- Water Backup and Sump Pump Overflow: Crucial for protecting against damage from sewer backups or failed sump pumps.

- Identity Theft Protection: A growing concern in the digital age.

- Specific Wind/Hail Deductibles: As mentioned, these are common and important to understand in Texas due to the frequency of these events.

Choosing the right combination of these coverages ensures comprehensive protection for your home, allowing you to fully embrace the Texas lifestyle, whether it’s enjoying events in Dallas, exploring Big Bend, or simply relaxing in your Texas home without undue financial worry.

Smart Strategies for Securing Your Home and Savings

Navigating the home insurance market in Texas can seem daunting, especially with its unique risks and variable costs. However, with strategic planning and an informed approach, homeowners can significantly impact their premiums while ensuring robust protection for their property. For those considering relocation or a long-term lifestyle change in Texas, these strategies are essential for financial preparedness and peace of mind.

How to Lower Your Home Insurance Costs

Reducing your home insurance premium in Texas doesn’t mean compromising on necessary coverage. Instead, it involves smart choices and leveraging available discounts.

- Shop Around and Compare Quotes: This is arguably the most effective way to find savings. Do not settle for the first quote you receive. Obtain quotes from multiple insurance providers – both national carriers (like State Farm, Allstate, Farmers) and regional ones. Online comparison tools can be helpful, but also consider working with an independent insurance agent who can shop various carriers on your behalf. Prices for the same coverage can vary by hundreds, if not thousands, of dollars.

- Increase Your Deductible: Opting for a higher deductible on your policy will lower your annual premium. For example, moving from a $1,000 deductible to a $2,500 or $5,000 deductible can result in significant savings. However, ensure you have sufficient funds readily available to cover this higher amount in case you need to file a claim. Remember, in Texas, you might have a separate, percentage-based deductible for wind/hail damage, which can be substantial.

- Bundle Your Policies: Many insurance companies offer discounts if you bundle your home insurance with other policies, such as auto insurance, life insurance, or even umbrella liability policies. This convenience can also lead to considerable savings, making the choice of accommodation and associated expenses more streamlined.

- Fortify Your Home and Improve Security: Making your home more resistant to damage and less appealing to burglars can earn you discounts.

- Impact-Resistant Roofs: Given the prevalence of hail, installing a Class 3 or Class 4 impact-resistant roof can lead to substantial premium reductions in Texas. This is one of the most impactful improvements for savings.

- Security Systems: Installing a monitored home security system (burglary and fire alarms connected to a central station) can qualify for discounts. Even basic deadbolts and smoke detectors can sometimes lead to minor reductions.

- Smart Home Technology: Devices that detect water leaks, monitor temperature, or automatically shut off utilities can reduce certain risks and may earn discounts.

- Reinforce Against Wind: In coastal areas, features like storm shutters or reinforced garage doors can reduce wind damage risk and qualify for discounts.

- Maintain Good Credit: As mentioned, your credit score can influence your insurance premium in Texas. Maintaining a good credit history demonstrates financial responsibility and can lead to lower rates.

- Ask About All Available Discounts: Don’t hesitate to ask your agent about every possible discount. These can include:

- New Home Discount: For recently constructed homes.

- Loyalty Discount: For long-term policyholders.

- Senior/Retiree Discount: For older homeowners.

- Claims-Free Discount: For policyholders who haven’t filed a claim for a certain period.

- Non-Smoker Discount: For households without smokers.

- Gated Community Discount: For homes in secure, gated communities.

By proactively implementing these strategies, homeowners in Texas can effectively manage their insurance costs, making homeownership more affordable and ensuring that their lifestyle choice in the Lone Star State is sustainable.

Choosing the Right Insurer in Texas

Selecting the right insurance provider is just as important as finding the right policy. In a state like Texas, where weather perils are frequent, the quality of your insurer can make a significant difference during a claim.

- Reputation and Financial Stability: Research the financial strength ratings of insurance companies (from agencies like A.M. Best, Moody’s, or Standard & Poor’s). A financially stable insurer is more likely to be able to pay out claims, especially after large-scale disaster events. Also, look at customer reviews and satisfaction scores regarding their claims process. A company like Travelers or Liberty Mutual might have strong national recognition, but local Texas insurers might offer more specialized products for regional risks.

- Understand Policy Details Thoroughly: Don’t just look at the premium. Read the policy document carefully, or have your agent explain the nuances of coverage, especially regarding deductibles, exclusions, and endorsements relevant to Texas’ specific risks (e.g., wind/hail deductibles, water backup coverage). Make sure you understand what is and isn’t covered.

- Customer Service and Accessibility: A good relationship with your insurance agent can be invaluable. Do they respond promptly? Are they knowledgeable about Texas insurance laws and local risks? Having a reliable point of contact is crucial when you need to file a claim. This becomes particularly relevant for those who might split their time between Texas and other locations, as seamless communication is key.

- Claims Process Efficiency: Inquire about their claims process. How easy is it to file a claim? What is their typical response time? Fast and efficient claims handling is paramount, especially after a storm when many homes might be damaged simultaneously.

Ultimately, choosing the right insurer is about finding a balance between cost, comprehensive coverage, and reliable service. It’s about protecting your home, your investment, and your lifestyle in Texas, allowing you to focus on enjoying the state’s vibrant culture, diverse attractions, and unique sense of community. Whether you’re making Texas your base for extensive travel or simply settling into a permanent retreat, sound home insurance is the foundation of a secure and worry-free experience.

In conclusion, while the cost of house insurance in Texas can be higher than in many other states due to its unique blend of weather-related risks, it is a critical investment for protecting your home and financial well-being. By understanding the factors that influence premiums, implementing smart savings strategies, and carefully selecting a reputable insurer, homeowners can navigate the Texas insurance landscape with confidence. This proactive approach ensures that your home remains a sanctuary, allowing you to fully immerse yourself in the rich experiences and unparalleled lifestyle that the Lone Star State has to offer.