Florida, the Sunshine State, beckons riders with its palm-fringed coastlines, vibrant cities, and endless opportunities for adventure on two wheels. Whether you’re a seasoned rider cruising down the Overseas Highway or a newcomer eager to explore the charming streets of St. Augustine, understanding motorcycle insurance is paramount. It’s not just a legal requirement; it’s your financial safety net, protecting you from the unexpected. But when it comes to motorcycle insurance costs in Florida, a clear-cut answer remains elusive. The truth is, it’s a complex equation influenced by a multitude of factors, each playing a crucial role in determining your premium.

This guide delves into the intricacies of motorcycle insurance in Florida, aiming to demystify the pricing and help you make informed decisions. We’ll explore the various components that insurers consider, from your personal profile to the specifics of your ride, and how these elements can impact your wallet. While we’ll focus on the financial aspects, remember that the joy of riding in Florida, be it exploring the theme parks of Orlando, the beaches of Miami, or the historic streets of Savannah, is amplified when you’re covered with the right insurance.

Understanding the Core Components of Motorcycle Insurance in Florida

When you’re looking into motorcycle insurance in Florida, it’s essential to understand that no two policies, and consequently no two prices, will be exactly alike. Insurers meticulously assess risk, and several key elements contribute to the final premium you’ll pay. Think of it like planning a trip to a new destination; you consider the type of accommodation, the activities you’ll indulge in, and the overall lifestyle you want to experience. Similarly, insurance companies weigh various factors before offering you a quote.

Factors Influencing Your Motorcycle Insurance Premium

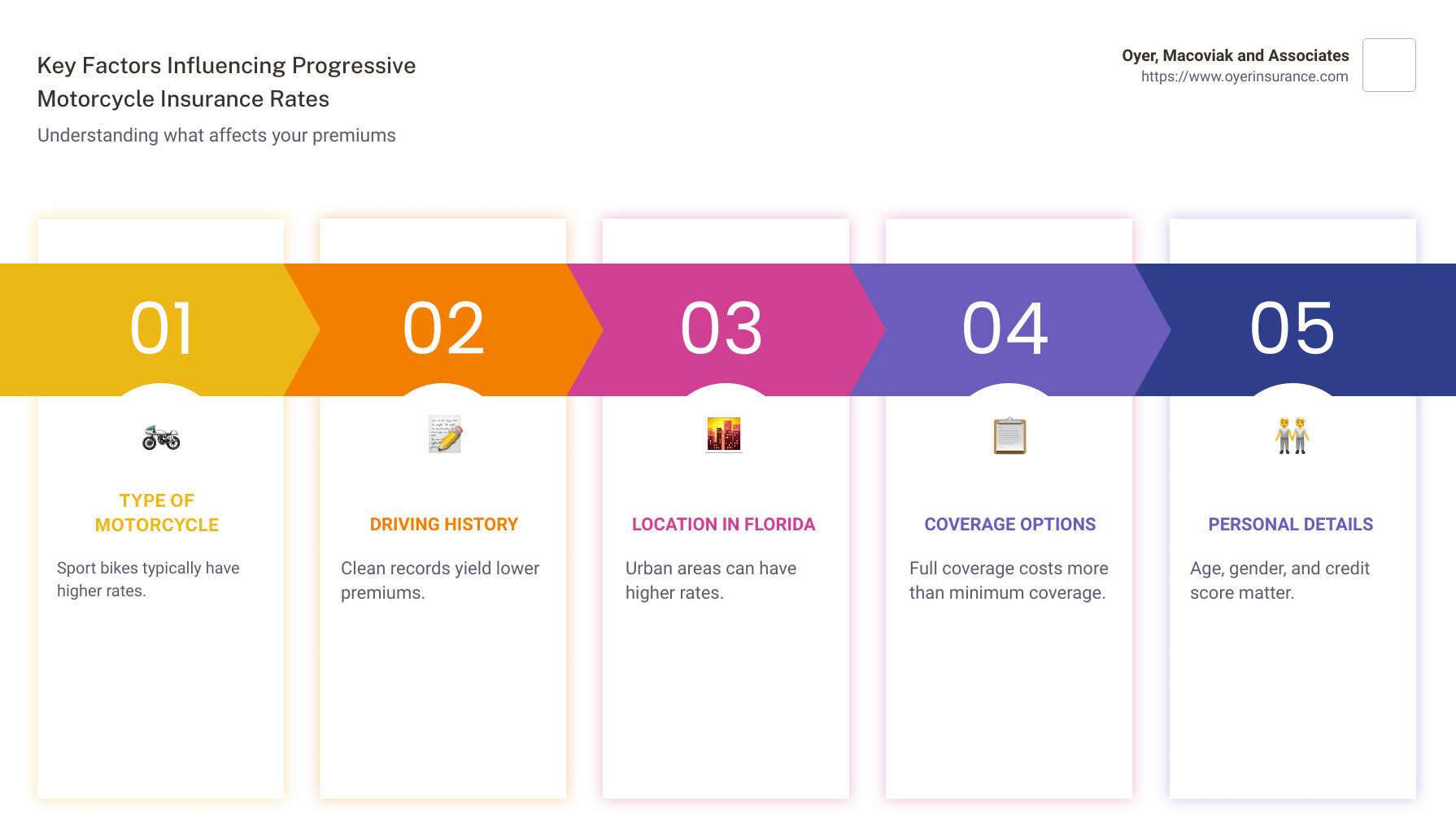

The cost of motorcycle insurance in Florida is not a static figure. It’s a dynamic reflection of your individual circumstances and the inherent risks associated with riding. Here are the primary drivers that insurers will scrutinize:

- Your Driving Record: This is arguably one of the most significant factors. A history of accidents, speeding tickets, or other traffic violations signals higher risk to insurers. Conversely, a clean driving record demonstrates responsibility and often leads to lower premiums. If you’ve recently moved to Florida, your previous driving history will likely be considered, so be prepared to provide that information.

- Your Age and Experience: Younger, less experienced riders generally face higher premiums because statistics show they are more prone to accidents. As you gain more years of riding experience and mature, your premiums may decrease. This is similar to how luxury hotels might offer different rates based on the length of your stay or the package you choose for a family trip.

- Your Location (ZIP Code): Where you live in Florida plays a surprisingly large role. Areas with higher rates of motorcycle theft, vandalism, or accidents will naturally have higher insurance costs. For instance, urban areas like Miami or Tampa might see different rates compared to more rural parts of the state.

- Type of Motorcycle: The bike itself is a major consideration. High-performance sportbikes, which are often associated with faster speeds and riskier riding, typically cost more to insure than cruiser-style motorcycles or smaller, less powerful models. The value of the motorcycle also impacts coverage costs, especially for comprehensive and collision. If you’re planning on a long-term stay in Florida with your prized motorcycle, ensuring it’s well-protected is key.

- Coverage Levels and Deductibles: This is where your personal choices significantly impact the price. Florida mandates specific minimum liability coverage, but most riders opt for more extensive protection.

- Liability Coverage: This covers damages or injuries you cause to others in an accident. It includes bodily injury liability and property damage liability. Higher limits mean higher premiums but provide greater financial protection.

- Collision Coverage: This pays for damage to your motorcycle if you collide with another vehicle or object, regardless of fault.

- Comprehensive Coverage: This covers non-collision related damages, such as theft, vandalism, fire, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: This is crucial in Florida, as it protects you if you’re hit by a driver who has no insurance or insufficient insurance.

- Medical Payments Coverage: This helps pay for medical expenses for you and your passenger, regardless of fault.

- Deductibles: This is the amount you pay out-of-pocket before your insurance coverage kicks in. A higher deductible generally results in a lower premium, and vice-versa. It’s a trade-off between upfront cost and potential future expenses.

- Annual Mileage: How much you ride your motorcycle each year can also affect your premium. If you’re a daily commuter in Orlando or frequently explore destinations like the Everglades, you’ll likely have higher annual mileage than someone who only rides on occasional weekend trips.

- Marital Status and Gender: Historically, insurers have used these factors, though regulations and practices are evolving. Some states have moved away from using gender, but it can still be a factor in pricing in certain areas.

Navigating Florida’s Motorcycle Insurance Requirements and Recommendations

Florida has specific laws regarding motorcycle insurance, and understanding these is the first step in securing appropriate coverage. While the state does not mandate full coverage for all riders, it does have requirements that every motorcycle owner must adhere to.

Florida’s Minimum Insurance Requirements

In Florida, motorcycle riders are required to carry $10,000 in Property Damage Liability and $10,000 in Bodily Injury Liability per person, per accident. This is the bare minimum to legally operate a motorcycle on Florida roads. However, it’s crucial to understand that these minimums may not be sufficient in the event of a serious accident. If you’re involved in an accident where damages exceed these limits, you could be personally liable for the remaining costs. This is a critical point, especially when considering the cost of extensive medical treatments or significant property damage.

Beyond the Minimum: Why More Coverage Might Be Wise

While meeting the state’s minimum requirements fulfills your legal obligation, most insurance experts and experienced riders strongly recommend opting for higher coverage limits. Consider the cost of a single serious accident: medical bills can quickly skyrocket into tens or hundreds of thousands of dollars. Similarly, if you cause an accident involving multiple vehicles, the property damage costs can also be substantial.

- Protecting Your Assets: If you own property, have savings, or anticipate a future income stream, inadequate liability coverage could put all of that at risk in a lawsuit following an accident. This is a significant consideration, whether you’re a resident or a tourist planning an extended stay in a luxurious villa in Naples.

- Peace of Mind: For many riders, the added cost of higher coverage is a worthwhile investment for the peace of mind it provides. Knowing that you’re protected against significant financial loss allows you to enjoy your rides through the scenic routes of Florida, from the historic charm of St. Augustine to the vibrant energy of Miami, without constant worry.

- Comprehensive and Collision: If your motorcycle is new or has a significant value, comprehensive and collision coverage are highly recommended. These cover repairs or replacement of your bike if it’s stolen or damaged in an accident, regardless of fault. This is akin to choosing a premium suite with all amenities for your stay in a resort, offering maximum comfort and security.

Factors Affecting Rates for Different Rider Profiles

The diverse landscape of Florida riders means that insurers tailor premiums to specific groups. Understanding these nuances can help you anticipate costs and explore potential discounts.

- New Riders: As mentioned, new riders, especially those under 25, will generally pay more. Insurers view them as a higher risk due to less experience on the road.

- Experienced Riders: Those with a long, clean driving record, particularly with motorcycles, will benefit from lower rates. Your history is a testament to your ability to navigate Florida’s roads safely.

- Leisure vs. Commuter Riders: If you use your motorcycle primarily for leisure rides along the coast or to explore attractions like Busch Gardens Tampa Bay, your annual mileage might be lower, potentially leading to slightly lower premiums compared to someone who uses their motorcycle as their primary mode of transportation for daily commuting.

- Multi-Bike Owners: If you own more than one motorcycle, you might be eligible for multi-bike discounts, similar to how booking multiple accommodations for a family trip might come with package deals.

Finding Affordable Motorcycle Insurance in Florida: Tips and Tricks

Securing affordable motorcycle insurance in Florida is achievable with a strategic approach. It’s not just about finding the cheapest policy, but rather the best value that provides adequate protection for your needs. Think of it as planning your travel budget; you want to find the best deals on hotels and experiences without compromising on quality.

Smart Strategies for Lowering Your Premiums

- Shop Around and Compare Quotes: This is the golden rule of insurance. Never settle for the first quote you receive. Dedicate time to comparing policies from multiple insurance companies. Rates can vary significantly between providers for the same coverage. Use online comparison tools and contact agents directly to get a comprehensive view of the market. Remember to compare identical coverage levels to ensure a fair comparison.

- Maintain a Clean Driving Record: As emphasized earlier, this is paramount. Avoid speeding tickets, DUIs, and accidents. A clean record is your best asset in negotiating lower premiums.

- Increase Your Deductibles: If you’re in a stable financial position and confident in your riding skills, consider a higher deductible. This can significantly reduce your monthly premium. However, ensure you have sufficient funds to cover the deductible in case of a claim.

- Ask About Discounts: Most insurance companies offer a variety of discounts. Inquire about:

- Multi-Bike Discounts: If you own more than one motorcycle.

- Safety Course Discounts: Completing an approved motorcycle safety course can often lead to a discount. Organizations like the Motorcycle Safety Foundation (MSF) offer excellent courses.

- Good Student Discounts: If you are a student and maintain good grades.

- Anti-Theft Device Discounts: Installing approved anti-theft devices can lower your comprehensive coverage costs.

- Loyalty Discounts: Some insurers offer discounts for long-term customers.

- Bundling Discounts: If you own other vehicles or a home, bundling your motorcycle insurance with other policies from the same insurer can lead to savings.

- Choose Your Motorcycle Wisely: If you’re in the market for a new motorcycle, consider the insurance implications. Less powerful, more common models are often cheaper to insure than high-performance or luxury bikes.

- Review Your Coverage Annually: Your insurance needs can change over time. As your motorcycle ages, you might consider dropping collision and comprehensive coverage if the bike’s value no longer justifies the cost. Conversely, if you’ve made significant upgrades or your financial situation has changed, you might need to increase your liability limits.

Understanding the Role of Insurance Agents and Brokers

When navigating the complexities of motorcycle insurance in Florida, insurance agents and brokers can be invaluable resources.

- Independent Agents: These professionals represent multiple insurance companies and can shop around on your behalf, presenting you with a range of options and prices. They can help you understand the nuances of different policies and recommend coverage that best suits your lifestyle, whether you’re planning weekend trips to the Florida Keys or exploring the natural beauty of the state.

- Captive Agents: These agents represent only one insurance company. While they can be knowledgeable about their company’s offerings, they won’t be able to compare rates from competitors.

Regardless of whether you use an agent or go directly to insurance companies, thorough research and a clear understanding of your needs are crucial. By arming yourself with knowledge and employing these smart strategies, you can find motorcycle insurance in Florida that offers the right balance of protection and affordability, allowing you to fully embrace the freedom of the open road. Whether you’re headed to a renowned resort like the Ritz-Carlton or exploring the local food scene, your peace of mind on the road is essential.