For many, the allure of California is undeniable. From the sun-drenched beaches of Southern California to the majestic redwoods of the north, and the bustling urban centers of Los Angeles and San Francisco, it’s a state that offers a diverse tapestry of experiences. However, for those who call California home, or who spend significant time within its borders, understanding the nuances of its healthcare system, particularly the individual health insurance mandate, is crucial. While many articles focus on the intricacies of the mandate itself, this guide takes a unique approach, exploring how individuals embracing a mobile, travel-focused lifestyle can navigate these regulations and potentially avoid penalties, all while maintaining peace of mind.

The modern world has ushered in an era of unprecedented mobility. More and more people are choosing lives less tethered to a single location, whether they’re digital nomads exploring different cultures, retirees spending seasons abroad, or professionals on extended assignments. This shift in lifestyle, which often involves significant travel and diverse accommodation arrangements, brings with it a host of considerations, including how to manage healthcare obligations. This article delves into how your travel habits, residency status, and lifestyle choices intersect with California’s health insurance mandate, providing actionable insights for the intrepid traveler.

Understanding California’s Health Insurance Landscape for the Modern Traveler

Before delving into strategies for penalty avoidance, it’s essential to grasp the fundamentals of California’s health insurance mandate and, critically, what defines a “resident” in the eyes of the law. For those whose lives involve frequent transitions between states or even countries, this definition can be far more fluid than for someone with a traditional, fixed residence.

The Mandate and Its Implications for Residents

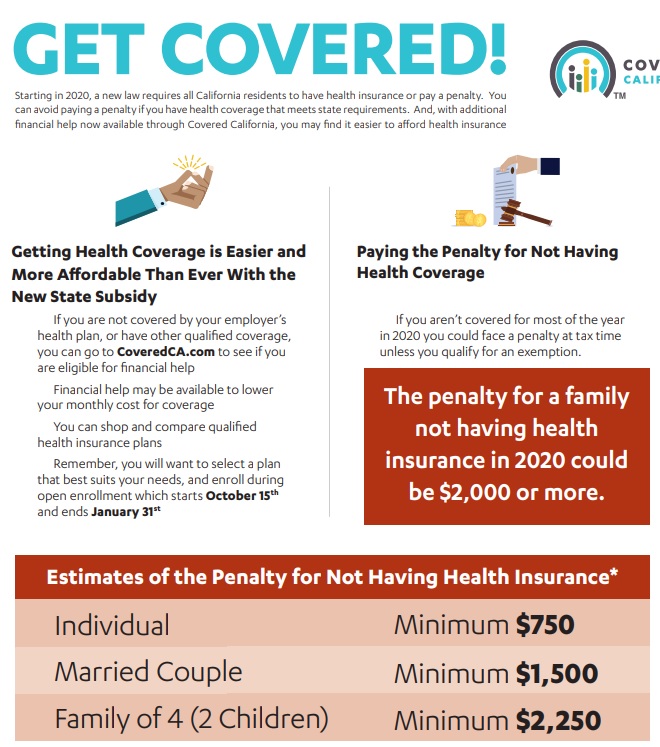

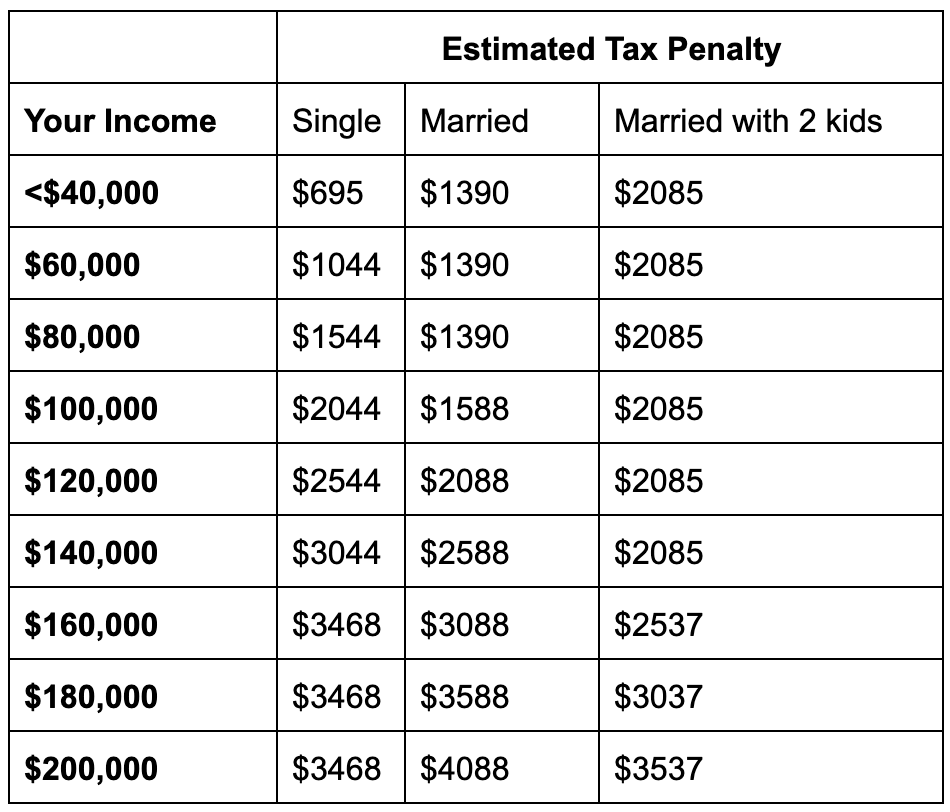

Since January 1, 2020, California has had an individual health insurance mandate, requiring most residents to have qualifying health coverage throughout the year. If you, your spouse, or your dependents do not have minimum essential coverage for each month, you may face a penalty, known as the Individual Shared Responsibility Payment. This penalty is assessed by the California Franchise Tax Board (FTB) when you file your state tax return. The amount of the penalty can vary but is often calculated as a flat dollar amount per adult and child, or a percentage of your household income, whichever is greater.

For a resident of California who is not frequently traveling, the path is clear: obtain coverage through an employer, Covered California (the state’s health insurance marketplace), or another qualifying plan. However, for those whose lifestyle involves prolonged periods outside the state, or who are considering making such a change, the application of this mandate becomes more complex. It’s not just about having coverage; it’s about where you are considered to reside for the majority of the year.

Who is Considered a California Resident?

This is perhaps the most critical question for any traveler or digital nomad hoping to navigate the California mandate. Generally, you are considered a California resident for tax purposes (and thus for the health insurance mandate) if you are in the state for other than a temporary or transitory purpose. This often boils down to where you spend the majority of your time and where your “closest connections” are.

Factors that the FTB considers when determining residency include:

- The amount of time spent in California versus outside the state: Typically, if you spend more than nine months out of the state, you might not be considered a resident.

- Location of your principal home: Do you own or rent a property in California? Or is your primary residence now in another state or country, such as an apartment in Mexico City or a villa in Bali?

- Location of your family: Are your spouse and dependents residing in California or elsewhere?

- Location of your employment or business: If your work is primarily conducted out-of-state or internationally, it strengthens your case for non-residency.

- Driver’s license and vehicle registration: Where are these registered?

- Voter registration: Where are you registered to vote?

- Bank accounts and investments: While less impactful than physical presence, these can contribute to the overall picture.

For the frequent traveler, these criteria offer potential avenues for demonstrating non-residency. Imagine a freelancer who, after enjoying the vibrant energy of San Diego, decides to spend eight months exploring Southeast Asia, staying in various hotels and guesthouses from Bangkok to Hanoi. If they genuinely move their “closest connections” to a new location, such as establishing a foreign address, opening local bank accounts, and not maintaining a permanent residence in California, they may qualify as a non-resident. This distinction is paramount because non-residents are generally exempt from the California health insurance mandate.

Travel-Centric Strategies for Penalty Avoidance

The individual mandate isn’t a blanket rule; it comes with several exemptions. For those with a mobile lifestyle, the most relevant exemptions often revolve around their physical presence and residency status. Understanding these can allow you to embrace a life of exploration without the added worry of state-imposed health insurance penalties.

Extended Stays Outside California: The Residency Exception

One of the most direct ways to avoid the California health insurance penalty is to simply not be a California resident for the majority of the tax year. This is particularly relevant for individuals who engage in long-term travel, sabbaticals, or temporary relocations. If you spend more than half the tax year (183 days or more) outside of California and can demonstrate that your absence was not merely “temporary or transitory,” you likely fall under the non-resident exemption.

Consider a family that decides to take a year-long family trip across Europe, exploring landmarks like the Eiffel Tower in Paris and the Colosseum in Rome. During this time, they might rent out their California home or let go of their apartment lease. If their primary base of operations, mail, and even their children’s schooling shift to temporary residences in various European countries for over six months, their ties to California significantly diminish. Documenting this extended absence with flight itineraries, hotel bookings, lease agreements for foreign accommodations, and utility bills from abroad becomes crucial evidence if ever questioned.

This strategy requires a genuine shift in your primary dwelling. Simply taking a two-month vacation while maintaining a permanent home in California won’t suffice. The key is demonstrating a clear intent to establish your primary presence elsewhere for a substantial period.

The Case for International Living and Digital Nomadism

The rise of the digital nomad has made international living more accessible than ever. Many individuals now earn their living remotely, allowing them the freedom to explore destinations across the globe, from the beaches of Thailand to the bustling streets of Tokyo. For these individuals, maintaining residency in California might not align with their lifestyle or their financial interests regarding healthcare mandates.

If you choose to become an expatriate or a long-term digital nomad living outside the United States for the entire tax year, you are typically not considered a California resident. This grants a clear exemption from the mandate. This path, while liberating, does come with its own set of considerations, particularly regarding international health insurance, which differs significantly from domestic plans. Many specialized international health insurance plans are designed specifically for expats and long-term travelers, offering comprehensive coverage across multiple countries, often with options for emergency medical evacuation.

Embracing this lifestyle means consciously severing ties with California residency. This could involve changing your driver’s license to another state (if you maintain a US base), updating your mailing address, and ensuring your tax filings reflect your non-resident status. It’s about more than just physically being out of the state; it’s about shifting your primary legal and personal connections.

Short-Term Visits vs. Establishing Residency Elsewhere

It’s crucial to distinguish between a short-term visit and establishing residency elsewhere. A two-week vacation to Hawaii, a business trip to New York City, or even a month-long stay in a resort in Palm Springs does not typically alter your California residency status. You would still be subject to the mandate if California remains your primary and most significant connection.

However, if you are considering a more significant move – perhaps spending a year working remotely from Portugal, or exploring retirement options in Florida – then the question of residency becomes critical. By actively establishing residency in another state or country, even if you plan to return to California at some point, you can avoid the penalty for the period you genuinely reside elsewhere. This involves taking concrete steps like obtaining a driver’s license in the new location, registering to vote there, and maintaining a physical address that serves as your primary home.

For instance, a retiree looking to escape the winter chill might purchase a condo in Scottsdale, Arizona, for six months of the year. If they genuinely establish legal residency in Arizona and spend more than half the year there, their California tax obligations, including the health insurance mandate, could change significantly. The key is intentionality and clear documentation of your new primary residence.

Navigating Health Coverage Options for the Mobile Individual

While avoiding the California penalty by proving non-residency is a valid strategy for many travelers, it’s paramount to never be without adequate health coverage. The goal is to avoid the penalty, not to avoid healthcare entirely. The choices you make for your health coverage will depend heavily on your travel duration, destinations, and individual needs.

Travel Insurance vs. Comprehensive Health Plans

For those embarking on a trip, the terms “travel insurance” and “health insurance” are often confused. It’s vital to understand the distinction:

- Travel Insurance: Primarily designed for emergencies that occur during a trip. It typically covers medical emergencies, trip cancellations/interruptions, lost luggage, and other travel-related mishaps. While it includes emergency medical benefits, it is generally not comprehensive health insurance and rarely covers routine check-ups, pre-existing conditions (unless specifically added), or long-term care. It would not satisfy California’s individual mandate if you are still considered a resident.

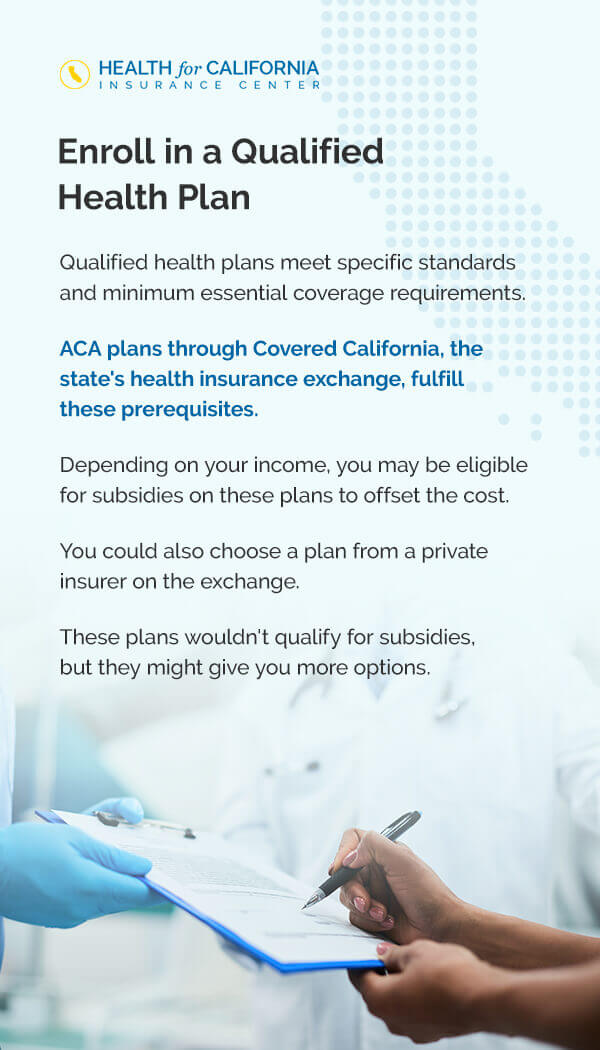

- Comprehensive Health Plans: These are designed to provide ongoing medical care, including preventive services, specialist visits, prescriptions, and hospital stays. If you are a California resident, you need a plan that meets the Affordable Care Act (ACA) standards, typically purchased through Covered California or an employer.

For the digital nomad or expat, dedicated international health insurance plans are the most suitable option. These plans offer comprehensive coverage specifically tailored for individuals living abroad long-term. They often provide extensive networks of providers in multiple countries, emergency evacuation services, and coverage for a wide range of medical needs, much like a domestic comprehensive plan. Providers like SafetyWing, Cigna Global, or GeoBlue specialize in these types of plans. Securing such a plan while genuinely living outside California is a smart way to protect your health without incurring a state penalty.

Exploring Employer-Sponsored Plans and Spousal Coverage

If your travel is periodic rather than a full-time nomadic lifestyle, or if you maintain strong professional ties to California, your employer-sponsored health plan might still be your best bet. Many employers offer plans that cover employees even during extended travel within the United States, and sometimes internationally for emergencies. It’s crucial to verify the extent of this coverage with your HR department, especially if you plan to be out of network or abroad for significant periods.

Similarly, if you are married, you might be eligible for coverage under your spouse’s health plan. This can be a robust solution, particularly if your spouse’s employer-sponsored plan is comprehensive and meets ACA requirements. This method ensures you have qualifying coverage, regardless of your personal travel schedule, as long as you remain a dependent on that plan and the plan meets the mandate’s requirements.

Special Enrollment Periods and Life Changes

Life changes often trigger “Special Enrollment Periods” (SEPs) for health insurance. These are windows outside of the annual open enrollment period when you can sign up for a new health plan. For travelers and those undergoing lifestyle shifts, relevant SEPs might include:

- Moving: If you move to a new area outside of your plan’s service area (e.g., leaving California permanently for Texas).

- Losing other health coverage: Such as losing job-based coverage, COBRA, or Medicaid.

- Changes in household size: Marriage, divorce, or having a baby.

Understanding SEPs is vital. If you decide to move out of California to become a non-resident for a significant portion of the year, this move itself could be a qualifying life event to enroll in a new plan in your new state of residence (if applicable) or to disenroll from a California plan. Always consult Covered California or a certified insurance broker to understand how your specific life changes impact your enrollment options.

Practical Considerations for a Seamless Transition

Embarking on a travel-ready lifestyle while navigating health insurance mandates requires careful planning and diligent record-keeping. The last thing you want is to return from an amazing adventure only to find yourself facing unexpected penalties.

Documenting Your Travel and Residency Status

The burden of proof often falls on the individual to demonstrate non-residency if challenged by the FTB. Therefore, meticulous record-keeping is not just advisable; it’s essential. Keep a comprehensive file (digital and/or physical) that includes:

- Travel Itineraries: Flight, train, bus, and cruise tickets.

- Accommodation Records: Hotel bookings, Airbnb receipts, lease agreements for apartments or villas in other states or countries. For a long-term stay at an Extended Stay America in Arizona, keep those receipts!

- Utility Bills and Mail: Evidence of addresses outside of California.

- Bank Statements: Showing transactions and accounts opened in other locations.

- Employment Records: Documentation of where your work is performed.

- New Driver’s License and Vehicle Registration: If you moved to another state, these are crucial.

- Voter Registration: Proof of registration outside California.

- Foreign Visas/Residency Permits: If applicable for international living.

This documentation serves as your evidence that California was not your permanent home for the specified period, thereby supporting your claim for exemption from the mandate. Imagine you spent an entire year experiencing tourism in South America, perhaps visiting Machu Picchu in Peru and exploring Buenos Aires in Argentina. The collective weight of your hotel receipts, flight stubs, and even photos from famous landmarks can paint a clear picture of your non-resident status.

Professional Guidance: When to Consult an Expert

While this article provides general guidance, individual situations can be complex. Tax laws, especially those concerning residency, are nuanced and can have significant financial implications beyond just the health insurance penalty. It’s always a wise decision to consult with a qualified tax professional or an attorney specializing in residency issues if:

- You have substantial assets in California.

- Your travel plans are extensive or involve multiple states/countries.

- You maintain some ties to California while claiming non-residency elsewhere.

- You are unsure about how to properly file your tax returns to reflect your residency status.

These professionals can provide personalized advice based on your unique circumstances, ensuring compliance with both state and federal regulations, and helping you optimize your financial planning for your mobile lifestyle.

Embracing the Freedom to Explore Without Financial Burden

The prospect of a health insurance penalty should not deter you from pursuing a lifestyle of travel and exploration. By understanding California’s mandate and thoughtfully planning your residency and health coverage, you can enjoy the freedom of the open road, the cultural richness of new destinations, and the comfort of diverse accommodations without the added stress of unnecessary penalties. Whether you dream of a luxury travel experience around the globe, a budget travel adventure through Central America, or a business stay that takes you to various cities, informed planning is your best companion.

The world is vast, and opportunities for unique living experiences abound. From serene resorts in Hawaii to bustling city apartments in London, the choices for accommodation and tourism are endless. By strategically managing your residency and health insurance, you empower yourself to embrace these experiences fully, truly living a life out of the box, free from the constraints of a fixed address and avoidable penalties.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.