Navigating the complexities of winding down a business in California can feel as intricate as planning a multi-city European adventure or booking the perfect resort for a long-awaited family vacation. While the allure of new travel experiences, the comfort of well-appointed accommodations, and the richness of local tourism are the focus of many discussions, understanding the necessary administrative steps for business closure is equally vital. This guide aims to demystify the process of dissolving a company in the Golden State, providing a clear roadmap for entrepreneurs and business owners. Whether you’re moving on to new entrepreneurial ventures, retiring, or simply closing a chapter, dissolving your company correctly ensures compliance and avoids potential future liabilities.

Understanding the Dissolution Process in California

Dissolving a company is more than just stopping operations; it’s a formal legal procedure. In California, this process is overseen by the California Secretary of State and involves several key steps to ensure all outstanding obligations are met and the entity is officially removed from the state’s records. The exact procedures can vary slightly depending on the type of business entity you’ve established, whether it’s a sole proprietorship, partnership, Limited Liability Company (LLC), or corporation. However, the core principles remain consistent: ceasing business activities, settling debts, distributing assets, and filing the necessary paperwork. Think of it as packing up your travel gear after an incredible journey, ensuring everything is accounted for and stored properly before embarking on your next adventure.

Dissolving a California LLC

For Limited Liability Companies (LLCs) in California, the dissolution process is initiated by the members or managers. The first step typically involves formally adopting a resolution to dissolve the LLC. This resolution should be documented in the company’s official records. Following this, the LLC must cease its normal business operations, except for those necessary to wind up its affairs. This includes liquidating assets, collecting any outstanding debts owed to the LLC, and paying off all known debts and liabilities.

Filing the Certificate of Dissolution

Once the winding-up process is substantially complete, the LLC must file a Certificate of Dissolution (Form LLC-3) with the California Secretary of State. This document formally notifies the state that the LLC is in the process of dissolving. It’s crucial to fill out this form accurately and completely. The California Secretary of State will process this filing, and it marks the official commencement of the dissolution proceedings.

Winding Up LLC Affairs

The winding-up period is critical. During this phase, the LLC’s management is responsible for:

- Ceasing business operations: Stop engaging in any new business activities.

- Collecting assets: Recover any money or property owed to the LLC.

- Liquidating assets: Sell off company property and assets.

- Paying debts and liabilities: Settle all outstanding bills, taxes, and obligations to creditors. This includes any outstanding franchise taxes or fees owed to the California Franchise Tax Board. It’s important to notify known creditors of the dissolution.

- Distributing remaining assets: After all debts are paid, any remaining assets are distributed to the LLC members according to their operating agreement or California law.

- Filing final tax returns: Ensure all federal and state tax returns are filed, indicating that the business is dissolved. This includes filing a final tax return with the Internal Revenue Service (IRS) and the California Franchise Tax Board.

The process can feel akin to carefully curating the final days of a wonderful trip to Italy, ensuring every souvenir is packed, every farewell is said, and all arrangements for your return home are settled, leaving no loose ends.

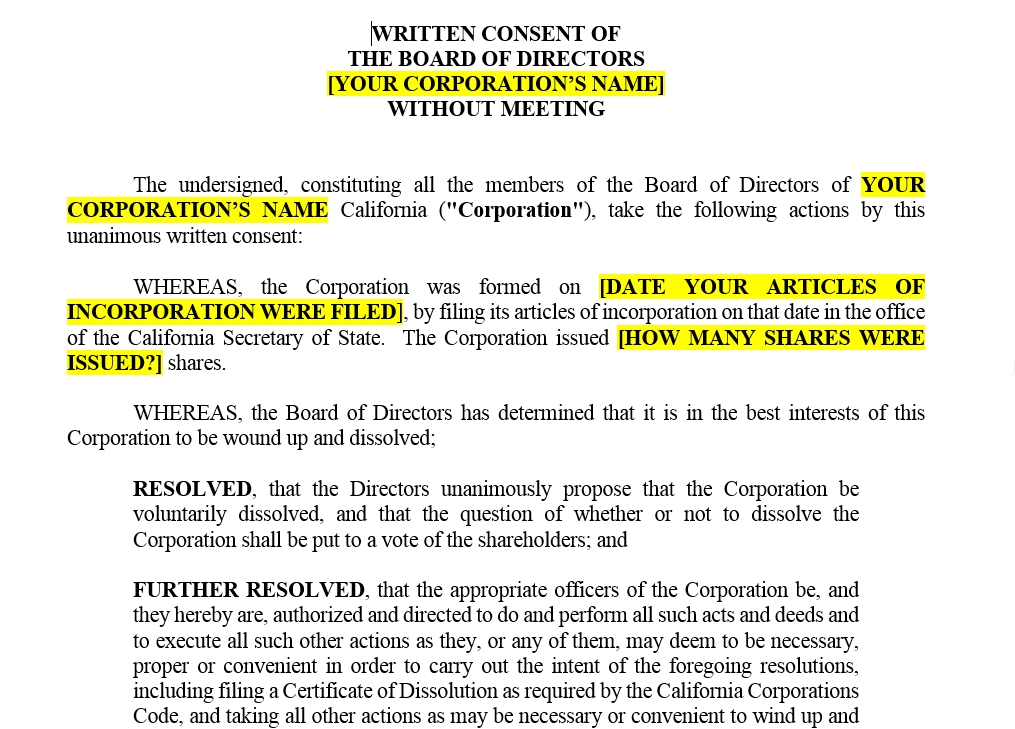

Dissolving a California Corporation

Dissolving a California Corporation follows a similar principle of formal closure but involves different documentation and specific corporate governance steps.

Corporate Dissolution Steps

- Board Resolution: The board of directors must adopt a resolution recommending the dissolution of the corporation.

- Shareholder Approval: This resolution is then submitted to the shareholders for approval. The required voting percentage typically depends on the corporation’s bylaws and California corporate law.

- Filing the Certificate of Dissolution (Corporations): For corporations, the relevant form is the Certificate of Dissolution (Form ARTS-170). This is filed with the California Secretary of State after shareholder approval. This filing signifies the intent to dissolve and triggers the winding-up process.

- Winding Up Corporate Affairs: Similar to LLCs, the corporation must wind up its affairs. This involves:

- Continuing business only as necessary to wind up.

- Collecting and liquidating corporate assets.

- Paying or making provision for all known debts, liabilities, and obligations, including taxes. This includes settling accounts with creditors and any shareholders or members whose claims are not satisfied.

- Distributing remaining assets to shareholders according to their respective rights and preferences.

- Filing final tax returns with the IRS and the California Franchise Tax Board.

The meticulous planning and execution required for corporate dissolution can be compared to organizing a complex business stay in a foreign city, where every detail, from securing the right hotel to managing logistical challenges, must be precisely handled to ensure a smooth and successful outcome.

Filing the Certificate of Cancellation

Once the winding-up of corporate affairs is completed, the corporation must file a Certificate of Cancellation (Form CONSW-170) with the California Secretary of State. This is the final document that formally terminates the corporation’s existence in California. It confirms that the winding-up is complete and all necessary steps have been taken.

Important Considerations During Dissolution

Beyond the core legal filings, several critical considerations can significantly impact the dissolution process, much like understanding local tourism tips before visiting a new destination.

Tax Obligations and Final Filings

One of the most crucial aspects of dissolving a company in California is settling all tax obligations. This includes:

- Franchise Tax: Ensure all franchise taxes owed to the California Franchise Tax Board are paid up to the date of dissolution. Even if a business has ceased operations, annual minimum franchise taxes may still apply until the entity is officially dissolved.

- Income Tax: File final federal and state income tax returns for the business. These returns should reflect all income and expenses up to the date of dissolution and report any distributions of assets to owners.

- Sales Tax: If your business collected sales tax, you must file final sales and use tax returns and remit any outstanding amounts to the California Department of Tax and Fee Administration.

- Employment Taxes: If you had employees, ensure all final payroll tax returns are filed and all taxes are paid. This includes federal and state withholdings and unemployment insurance contributions.

Failing to address these tax obligations can lead to penalties and interest, and in some cases, personal liability for the business owners. It’s often advisable to consult with a tax professional or accountant to ensure all tax requirements are met correctly. This attention to detail is akin to researching the best local culture and food experiences to maximize your enjoyment of a travel destination.

Notifying Creditors and Stakeholders

California law requires that you make a reasonable effort to notify all known creditors of the dissolution. This notice should inform them of the dissolution and provide a deadline by which they must submit their claims. For unknown creditors, publishing a notice of dissolution in a newspaper may be sufficient, depending on the circumstances. Properly notifying creditors helps protect the business owners from potential future claims against them personally.

This proactive communication mirrors the importance of clear booking processes and customer service in the accommodation sector, ensuring all parties are informed and expectations are managed.

Distribution of Assets

After all debts, liabilities, and obligations of the company have been paid or adequately provided for, any remaining assets are distributed to the owners (members of an LLC or shareholders of a corporation). The method of distribution depends on the operating agreement for an LLC or the corporate bylaws and relevant laws for a corporation. Proper documentation of these distributions is essential for tax purposes and to avoid disputes.

This final distribution is the culmination of the business’s journey, much like experiencing the culmination of a well-planned luxury travel itinerary, where the rewards are enjoyed after all the planning and effort.

Professional Assistance and Common Pitfalls

While it is possible to navigate the dissolution process independently, seeking professional assistance can significantly streamline the process and help avoid costly mistakes.

When to Seek Professional Help

- Legal Counsel: An attorney specializing in business law can provide guidance on the legal requirements, draft necessary documents, and ensure compliance with California statutes. This is particularly important if the company has complex assets, outstanding lawsuits, or intricate ownership structures.

- Accountants and Tax Advisors: Tax professionals are invaluable for ensuring all tax obligations are met, including final tax returns and any potential tax implications of asset distribution.

- Registered Agents: If you are dissolving an LLC or corporation, you may need to update your registered agent information and understand your final obligations.

Engaging professionals ensures that the dissolution process is as smooth and efficient as possible, much like relying on expert guides when exploring remote landmarks or navigating unfamiliar destinations.

Common Dissolution Pitfalls to Avoid

- Failure to File Final Taxes: Not filing final federal and state tax returns can result in penalties and ongoing tax liabilities.

- Incomplete Winding Up: Insufficiently settling debts and liabilities before distributing assets can lead to personal liability for the owners.

- Improper Notification of Creditors: Failing to properly notify creditors can leave the business vulnerable to future claims.

- Ignoring State Requirements: Not filing the correct dissolution or cancellation forms with the California Secretary of State means the company will not be officially dissolved.

- Continuing Operations Beyond Necessary Winding Up: Conducting new business activities after the intent to dissolve has been declared can complicate the process.

By understanding these potential pitfalls and proactively addressing them, business owners can ensure a clean and compliant dissolution, allowing them to move forward with peace of mind, ready for their next personal or professional lifestyle pursuit, be it a new family trip or a quiet retirement. The journey of a business, like a grand adventure, deserves a well-managed conclusion.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.