Navigating the complexities of inheritance, particularly when it involves assets within the Golden State, can often feel like deciphering an ancient map. While the allure of California, with its sun-drenched beaches, iconic landmarks, and vibrant cultural tapestry, draws millions for travel and tourism, the financial implications of inheriting property or wealth there can be a significant concern for many. This article aims to demystify the question: Is inheritance taxable in California? We will delve into the intricacies of the state’s tax landscape, exploring what you need to know if you are set to inherit assets, whether it’s a dream villa in Napa Valley or a legacy from a loved one.

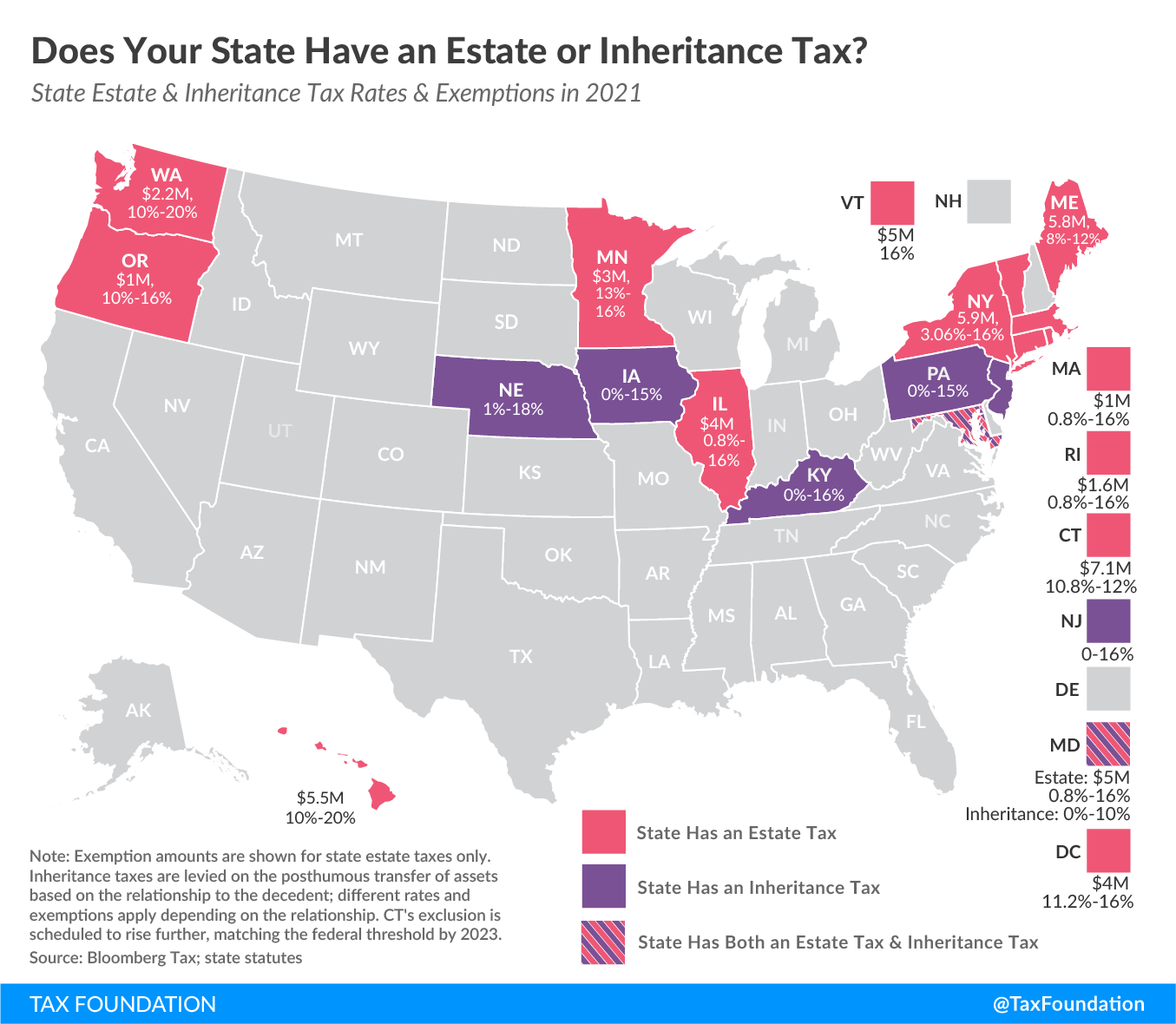

The primary reason for the widespread confusion surrounding inheritance taxes in California stems from a common misconception. Many individuals assume that if a state has an inheritance tax, it applies universally to all inherited assets. However, the reality is more nuanced. California, in fact, does not have a state-level inheritance tax. This is a crucial distinction, and it means that directly inheriting assets from a deceased relative generally does not trigger a tax liability at the state level in California. This is a significant relief for beneficiaries, as it simplifies the process of receiving bequests.

However, this does not mean that inheriting wealth is entirely tax-free. While California itself doesn’t levy an inheritance tax, other federal and state taxes, as well as specific circumstances, can still impact the net value of what you receive. Understanding these potential financial implications is essential for proper estate planning and for beneficiaries to manage their newfound assets effectively.

Understanding Federal Estate Tax and California’s Position

While California has opted out of imposing its own inheritance tax, the United States federal government does maintain an estate tax. This federal estate tax applies to the total value of a deceased person’s estate before it is distributed to heirs. The threshold for this tax is quite high, meaning that only very large estates are subject to it. For 2023, the federal estate tax exemption is set at $12.92 million per individual. For 2024, it is indexed for inflation and is $13.61 million. This means that an individual can pass on an estate valued up to this amount without incurring federal estate tax.

Federal Estate Tax Thresholds and Implications

The federal estate tax is levied on the total value of the deceased’s assets, including real estate, stocks, bonds, bank accounts, and personal property. If an estate exceeds the exemption amount, the portion above the threshold is taxed at a progressive rate, with the highest marginal rate currently at 40%. It’s important to note that this is a tax on the estate, not on the beneficiary. Therefore, if an estate falls below the federal exemption, no federal estate tax is due, and consequently, no California tax would be due either, as the state does not impose its own version.

For individuals who plan to leave behind substantial assets, understanding these federal thresholds and potentially seeking advice from estate planning professionals is paramount. This ensures that the estate is structured in a way that minimizes tax liabilities for beneficiaries, allowing more of the legacy to pass on. Planning for this can involve strategies like lifetime gifting, establishing trusts, or ensuring adequate insurance coverage to cover potential tax burdens.

State-Specific Considerations and Other Potential Taxes

Beyond the federal estate tax, it’s vital to consider other taxes and nuances that might affect inherited assets in California. While California doesn’t have an inheritance tax, there are other scenarios where taxes might come into play, particularly concerning income generated from inherited assets or specific types of property.

Income Tax on Inherited Assets

One of the most common areas where inherited assets can become taxable is through income tax. For instance, if you inherit stocks, bonds, or a rental property that generates income, that income will be subject to federal and California state income tax. This applies to dividends from stocks, interest from bonds, and rental income from properties. The specific tax treatment depends on the nature of the asset and how it’s managed after inheritance.

Capital Gains Tax

A key aspect of inheriting assets like stocks or real estate is the concept of “stepped-up basis.” When an individual passes away, the cost basis of their assets is generally adjusted to their fair market value at the date of death. This is incredibly beneficial for heirs. For example, if someone bought shares of a company for $10 per share many years ago, and those shares are worth $100 per share at their death, the heir’s cost basis becomes $100. If the heir then sells those shares for $100 per share, they will not owe any capital gains tax because there was no increase in value from the stepped-up basis. However, if the heir sells the shares for $110 per share, they will only owe capital gains tax on the $10 profit above the stepped-up basis. This “stepped-up basis” rule significantly reduces potential capital gains tax liabilities for beneficiaries who sell inherited assets shortly after receiving them.

However, if the asset has already appreciated significantly in value after the date of death, or if the original cost basis was already very low, then selling the asset could trigger capital gains tax. Understanding the stepped-up basis and the asset’s value at the time of inheritance is crucial for calculating any potential capital gains tax liability. This applies to various forms of appreciation, whether it’s the growth in the value of a San Francisco apartment or the increase in value of a vacation home in Lake Tahoe.

Property Taxes

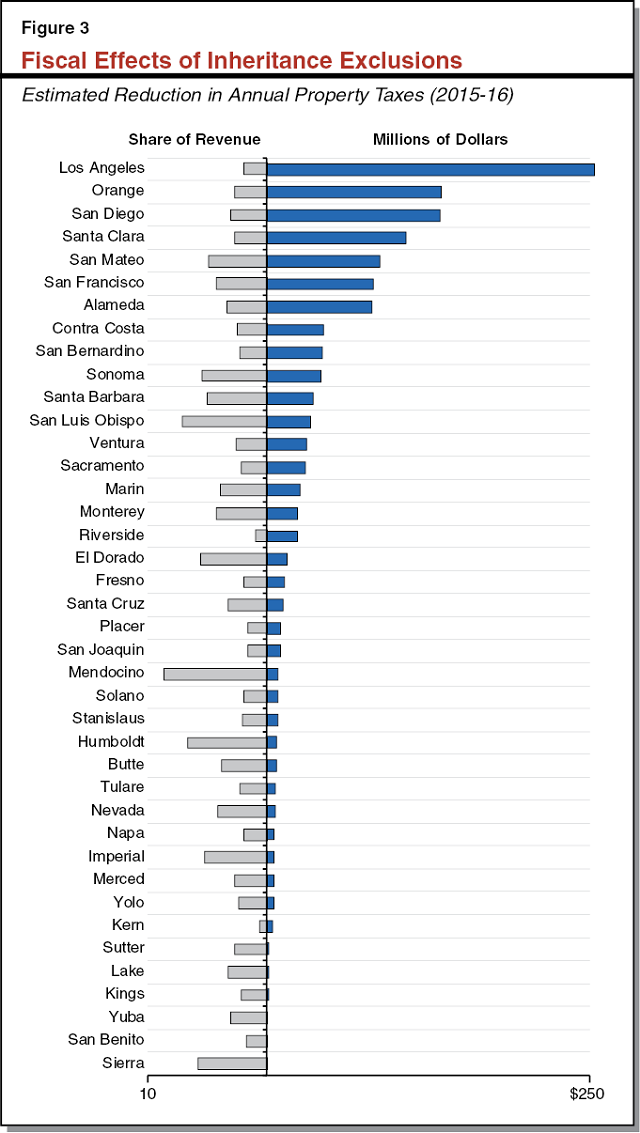

Inheriting real estate in California does not automatically trigger a reassessment of property taxes. Under Proposition 13, property tax is generally based on the assessed value at the time of acquisition, with an annual increase limited to 2%. However, there are specific rules regarding inheritance. If the property is transferred to a spouse, registered domestic partner, or in certain cases, children, it might be excluded from reassessment. But for other beneficiaries, or if the property is sold to a third party, a reassessment may occur, leading to higher property taxes based on the current market value. It is essential to consult with county tax assessor offices to understand the specific rules applicable to your inherited property in California.

Business Ownership and Other Assets

If you inherit a business, the tax implications can be more complex. Depending on the structure of the business (e.g., sole proprietorship, partnership, corporation) and whether it’s sold or continued, different tax rules will apply. Income generated by the business after inheritance will be subject to income tax. Similarly, inheriting other valuable assets, such as art collections or valuable jewelry, may not be taxed upon receipt in California, but their sale could result in capital gains tax if they have appreciated in value.

Planning for the Future: Estate Planning and Beneficiary Advice

Given the absence of a direct inheritance tax in California, many are under the impression that no financial planning is needed. However, robust estate planning is crucial for ensuring that assets are distributed according to the deceased’s wishes and that potential tax liabilities are minimized for beneficiaries. This is where understanding the nuances of federal taxes, income tax on inherited assets, and property tax reassessments becomes vital.

The Importance of Trusts and Wills

A well-crafted will or trust can significantly streamline the inheritance process and minimize complications. Trusts, in particular, can offer flexibility in how assets are distributed and managed, potentially shielding beneficiaries from immediate tax burdens or providing long-term asset protection. For instance, a trust might hold inherited real estate, allowing beneficiaries to receive rental income without directly owning the property and facing immediate reassessment for property taxes. When planning a trip to a place like Disneyland or considering a luxury resort in Beverly Hills, one might not think about estate planning, but these are the kinds of assets that could be part of an estate.

Seeking Professional Guidance

For both those planning their estates and those who stand to inherit, seeking professional advice is highly recommended. Estate attorneys can help draft wills and trusts that align with your goals and navigate the complexities of estate law. Financial advisors and tax professionals can offer guidance on managing inherited assets, understanding capital gains tax, and making informed investment decisions. This is especially true when dealing with significant inheritances, such as a sprawling vineyard in Sonoma County or a portfolio of investments.

Ultimately, while California does not impose an inheritance tax, understanding the potential tax implications of inherited assets, from federal estate tax to income and property taxes, is essential. Careful planning and professional advice can ensure that inheritances are handled smoothly and efficiently, allowing beneficiaries to fully enjoy the legacy left to them, whether it’s a sentimental heirloom or a substantial financial bequest. This peace of mind allows for a more relaxed enjoyment of life’s pleasures, from exploring the Golden Gate Bridge to experiencing the local cuisine in San Diego.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.