Embarking on a journey through the vast and diverse landscapes of Texas, whether you’re planning an epic road trip, relocating to a vibrant new city like Austin or Dallas, or simply enjoying a leisurely visit, understanding the local driving laws is paramount. The “Lone Star State” is renowned for its expansive highways, picturesque scenic routes, and bustling urban centers, making a personal vehicle an almost indispensable tool for exploration and daily life. From the historic charm of San Antonio and its iconic River Walk to the vibrant music scene of Austin, and the dynamic energy of Houston with its impressive NASA Space Center Houston, the ability to move freely and securely enhances any Texas experience.

However, behind the wheel, responsible travel and living necessitate adherence to state regulations, particularly concerning automobile insurance. This isn’t just about avoiding legal penalties; it’s a fundamental aspect of financial preparedness and peace of mind, integral to a smooth lifestyle whether you’re a long-term resident or a transient explorer. For travelers, understanding car insurance requirements can significantly impact decisions about rental cars, cross-state road trips, and even the overall budget for their Texas adventure. For those considering a move, integrating into the local regulations, including insurance mandates, is a crucial step in establishing a comfortable and secure new life. This comprehensive guide will navigate the intricacies of minimum car insurance in Texas, offering insights relevant to both visitors eager to explore its landmarks and new residents settling into their chosen community.

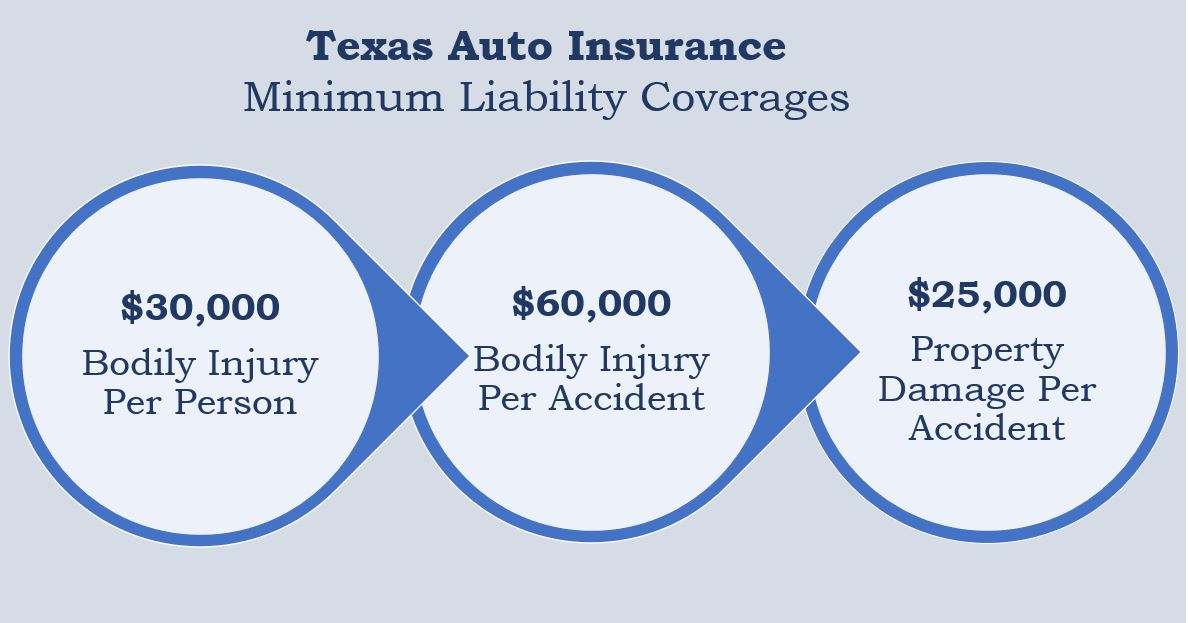

Understanding Texas’s “30/60/25” Rule: The Basics of Liability

At the heart of Texas’s car insurance regulations lies the concept of liability coverage, mandated by state law to protect other drivers and their property in an accident where you are at fault. This is often referred to as the “30/60/25” rule, a crucial set of numbers that every driver in the state must understand. This minimum requirement ensures that anyone operating a vehicle on Texas roads can financially cover potential damages or injuries they might cause. While these numbers represent the legal floor, for many, particularly those leading an active travel lifestyle or settling into a new home, they are merely a starting point for adequate protection.

Deciphering Bodily Injury Liability (BIL)

The “30/60” in the “30/60/25” rule pertains to Bodily Injury Liability (BIL). This coverage is designed to pay for the medical expenses, lost wages, and pain and suffering of individuals injured in an accident you cause.

- $30,000 per person: This is the maximum amount your insurance company will pay for injuries to any single individual involved in an accident that you are responsible for. Imagine you are driving through Houston and accidentally cause a minor fender bender with another vehicle. If the other driver sustains injuries requiring medical attention, your BIL would cover up to $30,000 of their related costs.

- $60,000 per accident: This is the total maximum amount your insurance company will pay for all bodily injuries in a single accident, regardless of how many people were injured. So, if your accident near the historic Alamo in San Antonio involved three injured parties, your insurance would pay a combined total of up to $60,000 for their medical bills, with no single person receiving more than $30,000.

For travelers exploring Texas on a road trip, having sufficient BIL is not just a legal obligation but a practical necessity. An accident, even a minor one, can quickly escalate into significant financial strain if medical costs exceed your coverage limits. This is especially true given the rising costs of healthcare. For new residents, securing adequate BIL is a foundational step in financial planning, safeguarding their assets and future in their new Texas home. Consider the peace of mind that comes from knowing you’re protected, whether navigating the bustling streets of Dallas or cruising through the serene landscapes near Big Bend National Park.

Property Damage Liability (PDL) Explained

The final number in the “30/60/25” rule, $25,000, represents the minimum requirement for Property Damage Liability (PDL). This coverage is essential for covering the costs of damage to another person’s property if you are found at fault for an accident. This property can include their vehicle, but it can also extend to other types of property like fences, buildings, or even road signs.

Imagine you are driving near a popular attraction in Galveston and, due to a momentary lapse, you rear-end another car, causing substantial damage. Your PDL would cover up to $25,000 to repair or replace that vehicle. What if the accident causes damage to a nearby storefront or a landmark sign? The same principle applies.

In a state as large and developed as Texas, where vehicles range from compact cars to luxury SUVs and commercial trucks, the cost of repairing or replacing a damaged vehicle can easily exceed the $25,000 minimum. For travelers renting a car to explore the diverse regions of Texas, understanding this limit is crucial. While the rental company might offer basic coverage, relying solely on the state minimum might leave you exposed to significant out-of-pocket expenses if you damage a newer or more expensive vehicle. Similarly, for new residents establishing their roots, a low PDL limit could jeopardize their financial stability should they be involved in an accident that causes extensive damage to another party’s valuable property. It’s a critical component of responsible driving that directly impacts your overall lifestyle and financial health within the state.

Beyond the Minimum: Protecting Your Texas Adventure and Lifestyle

While the 30/60/25 liability coverage is the legal minimum in Texas, it’s crucial to understand that “minimum” rarely equates to “adequate” when it comes to true financial protection. For anyone living, working, or extensively traveling in Texas, especially given the state’s vast distances and varied driving conditions, considering additional coverages is a wise investment in peace of mind and financial security. These supplementary policies go beyond protecting others and actively safeguard your own vehicle, well-being, and assets, ensuring your Texas adventure or new lifestyle remains unburdened by unforeseen automotive misfortunes.

Essential Additional Coverages for Peace of Mind

Expanding your insurance portfolio beyond basic liability can make a profound difference in the event of an accident or unexpected incident.

- Collision Coverage: This is perhaps one of the most vital additions for anyone who values their vehicle. Collision coverage pays for damage to your own car resulting from an impact with another vehicle or object, or even if you roll over. If you’re planning a scenic road trip through the Texas Hill Country, taking your own car or a rental, this coverage ensures that if you hit a deer or have a solo accident on a winding country road, your repair costs are covered, minus your deductible. For those who frequently stay at different hotels or explore various landmarks, the risk of scrapes or minor collisions in parking lots is always present, making collision coverage incredibly relevant.

- Comprehensive Coverage: Often paired with collision, comprehensive coverage protects your vehicle from non-collision-related damage. This includes events like theft (a concern in any major city like Houston or Dallas), vandalism, fire, natural disasters (hailstorms are common in Texas), and even damage from falling objects or encounters with animals. If your car is parked at a resort in Corpus Christi and is damaged by a severe storm, or if you discover a break-in after a day exploring Fort Worth‘s cultural district, comprehensive coverage provides a financial safety net. It’s especially valuable for newer vehicles or those with high market value, preserving your investment and travel freedom.

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: Despite strict laws, not all drivers on Texas roads carry adequate insurance, or any at all. UM/UIM coverage protects you if you’re involved in an accident with a driver who has no insurance or insufficient insurance to cover your medical bills and vehicle repairs. This is a critical layer of protection, particularly in a state with a large and diverse population where financial circumstances can vary widely. It ensures that your travel plans or daily routines aren’t derailed by someone else’s lack of responsibility.

- Personal Injury Protection (PIP) and Medical Payments (MedPay): These coverages help pay for medical expenses for you and your passengers, regardless of who was at fault for the accident. PIP typically covers medical bills, lost wages, and essential services, while MedPay focuses solely on medical costs. While Texas law requires insurers to offer PIP, you can reject it in writing. However, for those concerned about unexpected medical costs during a trip or as part of their daily life, accepting or adding this coverage provides an important safety net, complementing your existing health insurance and ensuring immediate accident-related medical needs are addressed without significant out-of-pocket stress.

Factors Influencing Your Insurance Premium in the Lone Star State

Understanding the minimum requirements is one thing; navigating the costs associated with car insurance in Texas is another. Several factors contribute to your premium, directly impacting your budget and lifestyle.

- Driving Record: Your history as a driver is perhaps the most significant determinant. A clean record with no accidents or traffic violations translates to lower premiums. Conversely, a history of speeding tickets or at-fault accidents will likely result in higher costs, reflecting a higher perceived risk to the insurer. This can significantly impact a traveler’s budget or a new resident’s monthly expenses.

- Vehicle Type: The make, model, year, and safety features of your car play a substantial role. Sports cars and luxury vehicles, or those with high repair costs, generally incur higher premiums. Vehicles equipped with advanced safety features might qualify for discounts. If you’re renting a car for a Texas tour, the type of vehicle you choose will influence the insurance add-ons you might need or consider. For residents, this is a key factor when purchasing a vehicle, balancing desired lifestyle with ongoing costs.

- Location within Texas: Where you live or frequently drive within Texas can affect your rates. Urban areas like Houston, Dallas, or Austin generally have higher rates due to increased traffic congestion, higher accident rates, and greater risk of theft or vandalism compared to more rural communities. For those considering moving, researching insurance costs based on specific neighborhoods or cities is a smart financial planning step.

- Age and Driving Experience: Younger, less experienced drivers typically face higher premiums due to statistical data indicating a greater risk of accidents. As drivers gain more experience and maintain a clean record, their rates tend to decrease.

- Credit History: In Texas, as in many other states, insurance companies often use a credit-based insurance score to help determine premiums. A strong credit history can lead to lower rates, reflecting financial responsibility.

- Deductibles: The deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in for collision and comprehensive claims. Choosing a higher deductible typically lowers your premium, but means you’ll pay more upfront in the event of a claim. This is a crucial financial decision that balances immediate savings with potential future costs, influencing both travel budgets and household financial management.

Navigating Texas Roads: Insurance for Travelers and Newcomers

Texas’s expansive road network beckons adventurers and offers new beginnings for many. Whether you’re visiting for a short stint to experience the vibrant culture of Austin or making a permanent move to a charming Texas town, understanding how car insurance integrates with your plans is vital. The approach to coverage can differ significantly for a tourist renting a vehicle versus a new resident establishing roots and registering their own car. Ensuring you have the correct and adequate insurance prevents legal headaches and financial burdens, allowing you to focus on enjoying all that the state has to offer, from its bustling cities to its serene natural wonders.

Renting a Car in Texas: What You Need to Know

For the legions of travelers exploring Texas’s attractions, from the NASA Space Center Houston to the expansive Big Bend National Park, a rental car often provides the ultimate freedom. However, the question of insurance for a rental vehicle can be complex.

- Rental Car Company Insurance: When you pick up a rental car at Dallas Fort Worth International Airport or any other major hub, the rental company will offer various insurance products. These typically include a Loss Damage Waiver (LDW) or Collision Damage Waiver (CDW), which covers damage to the rental car itself, and supplemental liability insurance, which extends the basic liability provided by the rental company (which is often the state minimum). While these options are convenient, they can be expensive.

- Personal Auto Insurance Policy: Many personal auto insurance policies extend coverage to rental cars. It’s crucial to check with your existing insurer before your trip. Your collision and comprehensive coverage might transfer to the rental vehicle, and your personal liability limits would also apply. This can save you a significant amount on daily rental car insurance fees. For example, if you live in El Paso and travel to San Antonio for a vacation, your existing Texas policy may cover your rental.

- Credit Card Benefits: Many premium credit cards offer rental car insurance benefits, typically covering damage or theft of the rental vehicle (similar to collision/comprehensive). These benefits are usually secondary, meaning they kick in after your personal insurance pays out, but some offer primary coverage. Always verify the specifics with your credit card issuer before you travel, as requirements can vary (e.g., you often must decline the rental company’s LDW).

- Specific Advice for Tourists: When visiting popular tourist destinations like the beaches of Galveston or the historic sites of San Antonio, ensure your rental car coverage is robust enough for typical tourist activities and potential scenarios. For example, if you plan to drive off-road in designated areas, check if your insurance covers that activity. Understand that the state minimum liability in Texas (30/60/25) applies to rental vehicles as well, but this bare minimum may not be sufficient protection against substantial claims. A quick call to your personal insurer or credit card company before reserving your car can provide immense peace of mind and potential savings, allowing you to fully immerse yourself in the Texas experience without undue financial worry.

Moving to Texas: Securing Your Ride

Relocating to Texas opens up a world of new experiences, from discovering local culture and cuisine to finding the perfect accommodation. A significant part of this transition involves ensuring your vehicle complies with state laws.

- Transferring Policies vs. New Policies: If you’re moving from another state, your existing car insurance policy will likely not transfer directly to Texas. You’ll need to obtain a new Texas auto insurance policy. It’s wise to start this process before your move, or immediately upon arrival, to ensure continuous coverage. Insurance companies consider local factors, including accident rates and theft statistics in your new Texas zip code, to determine your premiums. For instance, moving to a bustling city like Houston from a rural area might see a change in your rates.

- Registering Your Vehicle: Once you establish residency in Texas (typically within 30 days of moving), you must register your vehicle with the Texas Department of Motor Vehicles (DMV). Proof of current Texas liability insurance is a prerequisite for vehicle registration and obtaining Texas license plates. You’ll also need to get your vehicle inspected by an authorized Texas inspection station.

- Adapting to Local Laws and Lifestyle: Beyond the legal minimums, consider how your new Texas lifestyle will influence your insurance needs. If your new accommodation is in a high-traffic area, or if you plan frequent road trips to explore landmarks across the state, opting for higher liability limits and additional coverages like collision and comprehensive insurance becomes even more pertinent. This proactive approach not only keeps you compliant with the law but also provides robust financial protection tailored to your new life in the “Lone Star State.” It integrates seamlessly with the broader aspects of settling in, like finding suitable housing, understanding local customs, and exploring the vast array of activities Texas has to offer.

Drive Smart, Live Fully in Texas

Navigating the roads of Texas, whether for a fleeting vacation or a permanent relocation, is an experience rich with possibilities. From the vibrant nightlife of Austin to the serene beauty of the Gulf Coast in Corpus Christi, the freedom of driving allows you to embrace every facet of this diverse state. However, that freedom comes with a significant responsibility: ensuring you are adequately insured.

The minimum car insurance required in Texas, the “30/60/25” rule, serves as a fundamental baseline. It guarantees that, at the very least, you have liability coverage to protect other individuals and their property in an accident where you are at fault. For travelers renting a vehicle, or new residents moving their life to the Lone Star State, this minimum is a non-negotiable legal requirement for driving on public roads.

Yet, as we’ve explored, meeting the minimum doesn’t always mean achieving optimal protection. For true peace of mind and robust financial security, especially given the potential costs associated with accidents, medical bills, and vehicle repairs, considering additional coverages like collision, comprehensive, uninsured/underinsured motorist protection, and personal injury protection is highly advisable. These supplementary policies safeguard your own assets, health, and vehicle, preventing minor mishaps from escalating into major financial crises that could disrupt your travel plans or new lifestyle.

Ultimately, understanding and securing the right car insurance in Texas is more than just adhering to a legal mandate; it’s a critical component of responsible travel and sustainable living. It empowers you to explore Texas confidently, knowing that you are prepared for unforeseen circumstances, allowing you to focus on discovering charming local hotels, experiencing unique tourism activities, visiting iconic landmarks, and enjoying the rich lifestyle that the state proudly offers. Drive smart, stay protected, and live fully in the heart of Texas.