Navigating the intricacies of real estate transactions in Texas can feel like exploring a new continent, brimming with unique customs and, often, unexpected expenses. One of the most frequent questions that arises, much like planning a dream vacation, is who ultimately shoulders the financial responsibility for certain fees. In Texas, the question of “Who Pays Closing Costs?” is not a simple one-size-fits-all answer, but rather a dynamic interplay between buyer and seller, influenced by negotiation, local customs, and the type of transaction.

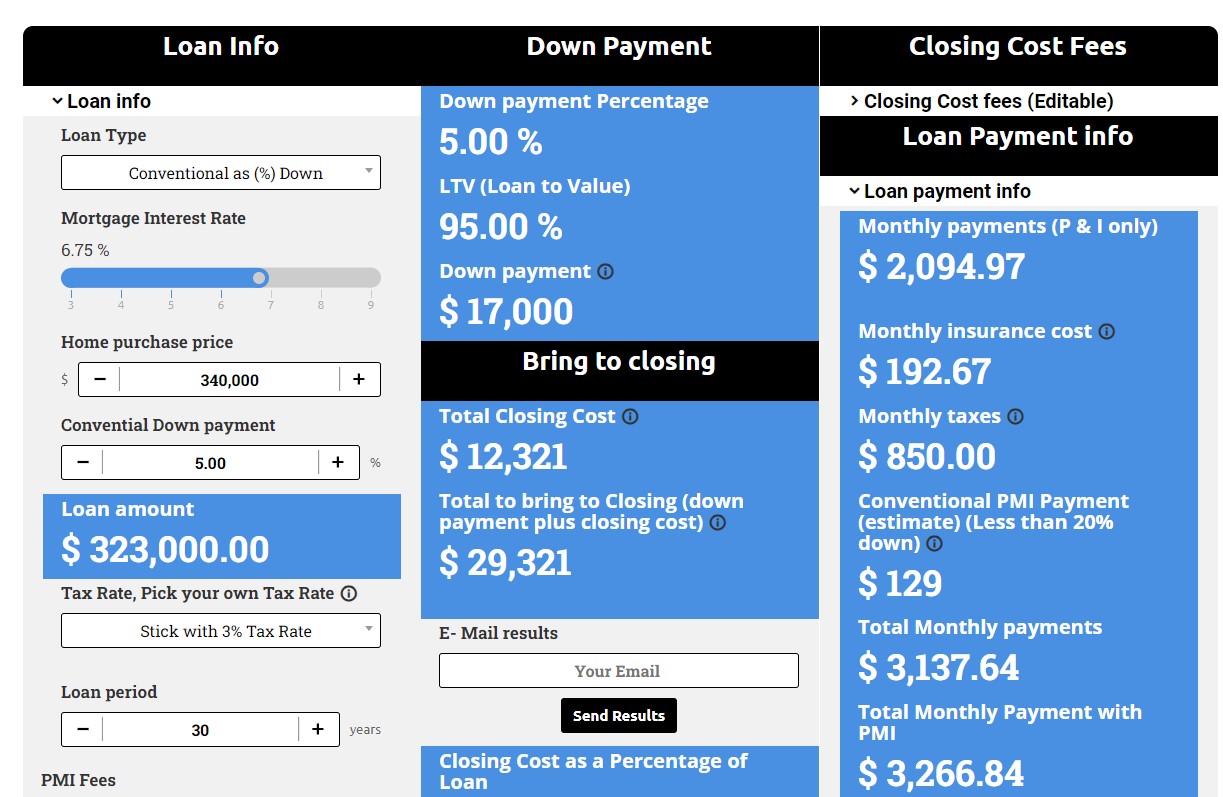

Closing costs are the sum of various fees and expenses incurred by both the buyer and the seller during the closing of a real estate transaction. These costs are separate from the down payment and the loan principal. They typically encompass a range of services and administrative tasks essential to transferring ownership of a property, from title insurance and appraisal fees to recording fees and real estate agent commissions. Understanding these costs is crucial for budgeting and avoiding surprises, much like understanding the true cost of that all-inclusive resort package or the hidden fees for adventure tours.

While Texas has some general practices, the specifics of who pays what can vary. The overarching principle is that these costs are negotiable. However, established customs in the Lone Star State often lean towards certain parties covering specific expenses. For instance, it’s a common practice for sellers to cover a larger portion of the closing costs than buyers. This is often factored into the initial listing price of the property. Buyers, on the other hand, typically cover costs directly related to securing their financing and the actual transfer of ownership.

The Buyer’s Burden: Securing the Dream Home

When you embark on the journey of purchasing a home in Texas, several closing costs will fall squarely on your shoulders as the buyer. These expenses are largely tied to the financing you secure to make the purchase possible and the essential due diligence required to ensure a sound investment. Think of these as the necessary steps in booking your flights and arranging your accommodation for a memorable trip; they are non-negotiable for the journey to commence.

Loan-Related Expenses

The majority of a buyer’s closing costs in Texas are directly associated with obtaining a mortgage. Lenders, understandably, want to ensure the loan is secure and that their investment is protected.

- Loan Origination Fees: This is a fee charged by the lender for processing the mortgage application. It can be a flat fee or a percentage of the loan amount. It’s akin to the booking fee you might pay for a premium travel package.

- Appraisal Fee: Before approving a loan, lenders require an independent appraisal to determine the market value of the property. This ensures the loan amount does not exceed the property’s worth.

- Credit Report Fee: Lenders pull your credit report to assess your creditworthiness. This fee covers the cost of obtaining your credit history.

- Discount Points: If you choose to pay points, which are essentially prepaid interest, to lower your interest rate over the life of the loan, this is a significant buyer closing cost.

- Private Mortgage Insurance (PMI) or FHA Mortgage Insurance Premium (MIP): If your down payment is less than 20% of the home’s purchase price, lenders will typically require PMI. For FHA loans, MIP is mandatory. These protect the lender in case you default on the loan.

- Flood Certification Fee: This fee determines if the property is located in a flood zone, which might necessitate flood insurance.

- Title Insurance (Lender’s Policy): This policy protects the lender against any undiscovered title defects or liens on the property that could jeopardize their investment.

Ownership Transfer and Legal Fees

Beyond financing, buyers are also responsible for costs directly related to taking legal ownership of the property.

- Escrow Fee (Buyer’s Portion): An escrow company or attorney acts as a neutral third party, holding funds and documents until all conditions of the sale are met. The buyer typically pays a portion of this fee.

- Recording Fees: When the deed is transferred and the mortgage is recorded with the county clerk, there are fees associated with this official registration.

- Title Search Fee: This fee covers the cost of searching public records to ensure the seller has clear title to the property and that there are no outstanding liens or encumbrances.

- Home Inspection Fee: While not always a closing cost required by the lender, a home inspection is a critical step for buyers to identify any potential issues with the property before finalizing the purchase. This is a wise investment for any homeowner, much like opting for a guided tour to fully appreciate a historical landmark.

- Survey Fee: In some cases, a survey may be required to verify property boundaries.

The Seller’s Side of the Ledger: Transferring Ownership

Sellers in Texas also incur significant closing costs, primarily related to the sale of their property and the transfer of clear title to the buyer. These costs are often the largest single expense in the transaction and are frequently a point of negotiation. For sellers, these costs are akin to the fees associated with preparing a property for an international tour – ensuring everything is in order for the next visitor.

Real Estate Commissions

Perhaps the most substantial closing cost for sellers in Texas is the real estate agent’s commission. This is typically a percentage of the final sale price, split between the buyer’s agent and the seller’s agent. This commission compensates the agents for their services in marketing the property, negotiating the sale, and guiding both parties through the closing process.

Title and Escrow Services

Sellers also contribute to the costs associated with ensuring a clean title transfer and the smooth operation of the escrow process.

- Title Insurance (Owner’s Policy): While the lender requires a lender’s policy (paid by the buyer), it is customary in Texas for the seller to pay for the owner’s title insurance policy. This policy protects the buyer against any title defects that may arise after the purchase.

- Title Search Fee (Seller’s Portion): The seller often covers the cost of the initial title search that confirms their ownership and identifies any existing liens that need to be cleared before the sale.

- Escrow Fee (Seller’s Portion): As mentioned earlier, the escrow fee is typically split, and the seller pays their allocated portion.

- Attorney Fees: If the seller utilizes an attorney for the transaction, their fees will be part of the closing costs. This is common in Texas, especially for more complex transactions.

Property-Related Expenses

Several other expenses are typically borne by the seller at closing.

- Property Taxes: Sellers are responsible for paying their portion of property taxes up to the closing date. Any prepaid taxes will be prorated.

- HOA Dues and Transfer Fees: If the property is part of a Homeowners Association (HOA), the seller will be responsible for any outstanding dues and often for the transfer fees associated with changing ownership in the HOA records.

- Transfer Taxes (if applicable): While Texas does not have a statewide transfer tax, some local jurisdictions may impose them. These are usually paid by the seller.

- Outstanding Mortgage Payoff: The seller is responsible for paying off any existing mortgage balance on the property.

- Repairs and Seller Concessions: If the seller agrees to make repairs or offer seller concessions (e.g., contributing to the buyer’s closing costs), these amounts are also settled at closing.

Negotiation is Key: Customizing Your Closing Costs

In Texas, the “Who Pays Closing Costs?” question is not rigidly defined. The most significant factor influencing the allocation of these costs is negotiation. Real estate transactions are dynamic, and both buyers and sellers can leverage their positions to shift some of these expenses. Understanding the typical distribution allows parties to enter negotiations from an informed standpoint.

Factors Influencing Negotiation

- Market Conditions: In a seller’s market, where demand for homes is high, sellers are less likely to agree to cover many buyer closing costs. Conversely, in a buyer’s market, buyers may have more leverage to request seller contributions.

- Offer Price: The initial offer price often sets the stage for closing cost negotiations. A buyer might offer a slightly lower price if they anticipate paying more closing costs, or a higher price if they are requesting the seller cover a larger portion.

- Contingencies: The number and type of contingencies in an offer can influence negotiations. For instance, a buyer’s willingness to waive certain inspection contingencies might be traded for seller concessions on closing costs.

- Type of Loan: Different loan types can have varying closing cost implications. For example, FHA loans often have specific requirements regarding who pays certain fees.

- Local Customs: While general principles apply, specific neighborhoods or even cities within Texas might have very localized customs regarding closing cost allocations that real estate agents are well aware of.

Common Negotiation Scenarios

- Seller Concessions: A common negotiation tactic is for the seller to agree to pay a portion of the buyer’s closing costs. This can be a specified dollar amount or a percentage of the sale price. This is particularly helpful for buyers who may have limited cash for down payments and closing costs combined.

- Shared Costs: In some cases, certain costs like the survey or title insurance might be split between the buyer and seller.

- “As-Is” Sales: When a property is sold “as-is,” it usually means the seller is not willing to make repairs. In such scenarios, buyers might try to negotiate for the seller to contribute more to their closing costs to offset the risk.

Ultimately, the closing cost allocation is an agreement reached between the buyer and seller, documented in the purchase agreement. It’s wise to work with an experienced real estate agent and a reputable title company or real estate attorney in Texas to understand all the associated costs and to navigate the negotiation process effectively. Just as a well-planned itinerary ensures a smooth travel experience, a clear understanding and agreement on closing costs pave the way for a successful real estate transaction.