For many, the mention of Florida conjures images of sun-drenched beaches, vibrant cities like Miami and Orlando, and a lifestyle characterized by leisure and warmth. It’s a premier destination for travelers seeking diverse experiences, from the thrilling theme parks of Central Florida to the tranquil natural beauty of the Everglades or the historic charm of Key West. The state is also a magnet for those looking to invest in a second home, a vacation rental, or even make a permanent move, drawn by the promise of year-round sunshine and a relaxed pace of life. However, beneath the allure of the Sunshine State lies a critical consideration for homeowners, potential buyers, and property investors alike: the cost and complexities of homeowners insurance.

Understanding how much homeowners insurance costs in Florida isn’t just about crunching numbers; it’s about grasping a fundamental aspect of the Florida lifestyle and the financial realities of property ownership in a unique and dynamic environment. Unlike many other states, Florida’s geographical location, climate, and specific legal landscape significantly impact insurance premiums, often making them among the highest in the United States. For anyone considering a move, purchasing a vacation property, or simply navigating the responsibilities of homeownership in this beautiful state, a comprehensive understanding of insurance costs is paramount. It influences everything from long-term accommodation budgets to the viability of a real estate investment, shaping the overall financial landscape of living or visiting the state.

Understanding the Florida Homeowners Insurance Landscape

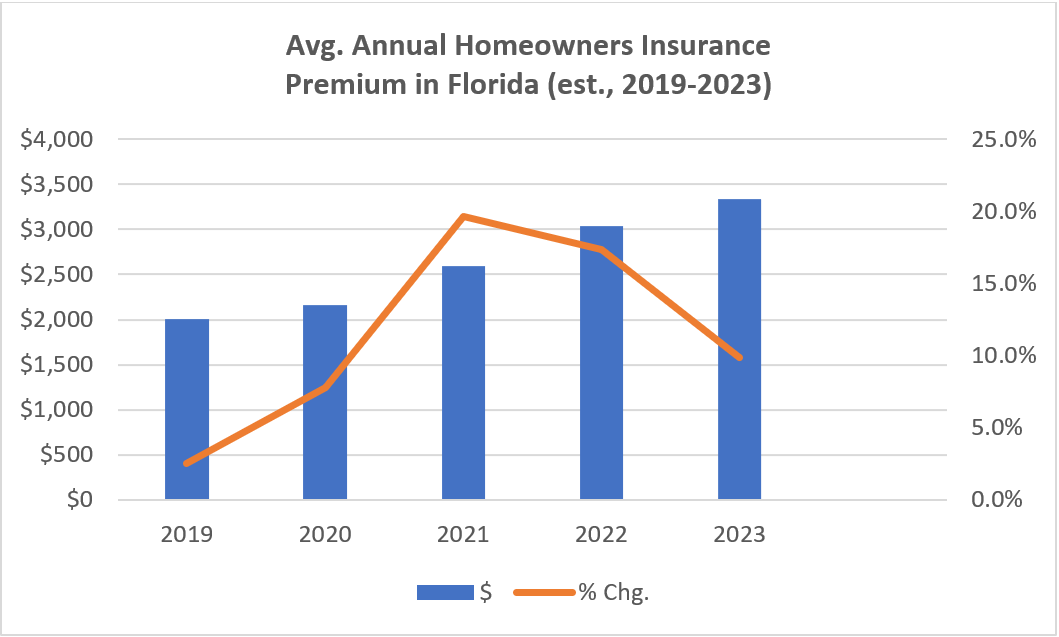

The cost of homeowners insurance in Florida can be a significant surprise for those accustomed to rates in other parts of the United States. While the national average for homeowners insurance hovers around $1,700 per year, Florida homeowners often face premiums that are two, three, or even four times that amount. This dramatic difference is not arbitrary; it’s the result of a confluence of factors unique to the state, affecting everything from property values to the types of coverage available. For individuals planning a long-term stay, contemplating a move, or even evaluating the financial feasibility of owning a vacation property that might also serve as a short-term rental, comprehending these underlying influences is key. It’s an integral part of budgeting for a Florida lifestyle, whether it’s in the bustling metropolis of Tampa or a serene coastal community near Naples.

Key Factors Influencing Premiums in the Sunshine State

Several critical elements contribute to the elevated and often fluctuating cost of homeowners insurance in Florida:

- Hurricane Risk: This is arguably the most dominant factor. Florida’s extensive coastline, both along the Gulf Coast and Atlantic Coast, places it directly in the path of tropical storms and hurricanes. The frequency and intensity of these events, as exemplified by recent destructive storms like Hurricane Ian, lead to massive property damage claims, which insurance companies must factor into their rates.

- Proximity to the Coast: Homes closer to the coast face higher wind and flood risks, directly translating into higher premiums. A property just a few miles inland might have significantly lower rates than an identical one right on the beach, even within the same city like Sarasota or Fort Lauderdale.

- Age and Construction of the Home: Older homes, particularly those built before modern building codes (e.g., pre-2002 hurricane mitigation standards), are generally more vulnerable to storm damage. Insurers often charge more for these properties or require specific upgrades. Conversely, newer homes with wind-resistant features, fortified roofs, and impact-resistant windows may qualify for significant discounts.

- Roof Age and Condition: In Florida, the age and condition of a roof are paramount. Given the relentless sun, humidity, and potential for hurricane-force winds, roofs degrade faster. Many insurers have strict rules regarding roof age, often refusing to cover homes with roofs over 15-20 years old without a full replacement.

- Claims History: Both the homeowner’s personal claims history and the claims history of the property itself can impact rates. A home that has had multiple claims filed against it in the past will likely be more expensive to insure.

- Local Repair Costs: The cost of labor and materials for home repairs in Florida, especially after a widespread natural disaster, can be high, further driving up insurance payouts and, consequently, premiums.

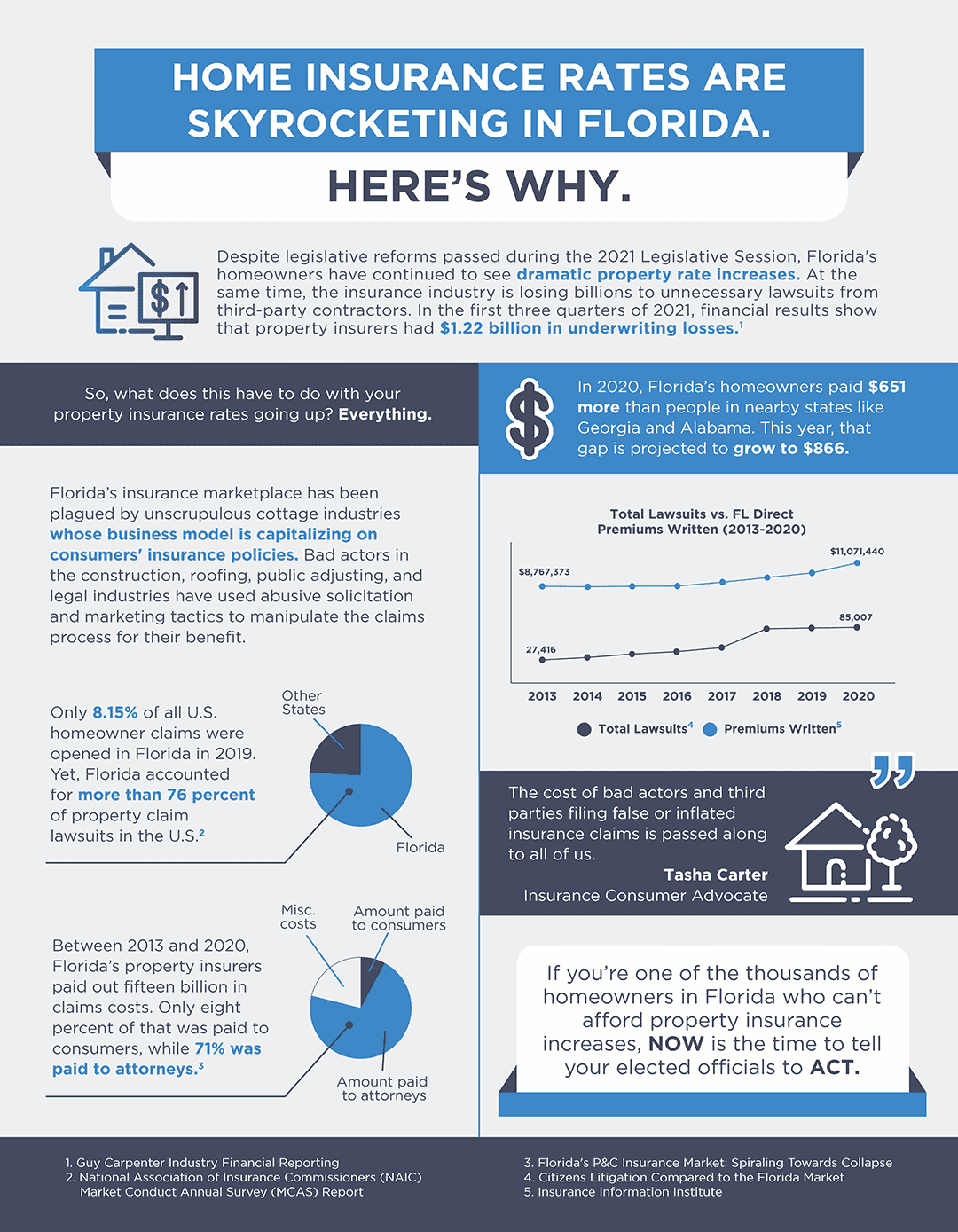

- Litigation Environment: Florida has faced challenges with insurance fraud and excessive litigation related to property damage claims, particularly for roofs. This has led many insurers to pull out of the state or drastically increase rates to offset their increased risk and legal expenses.

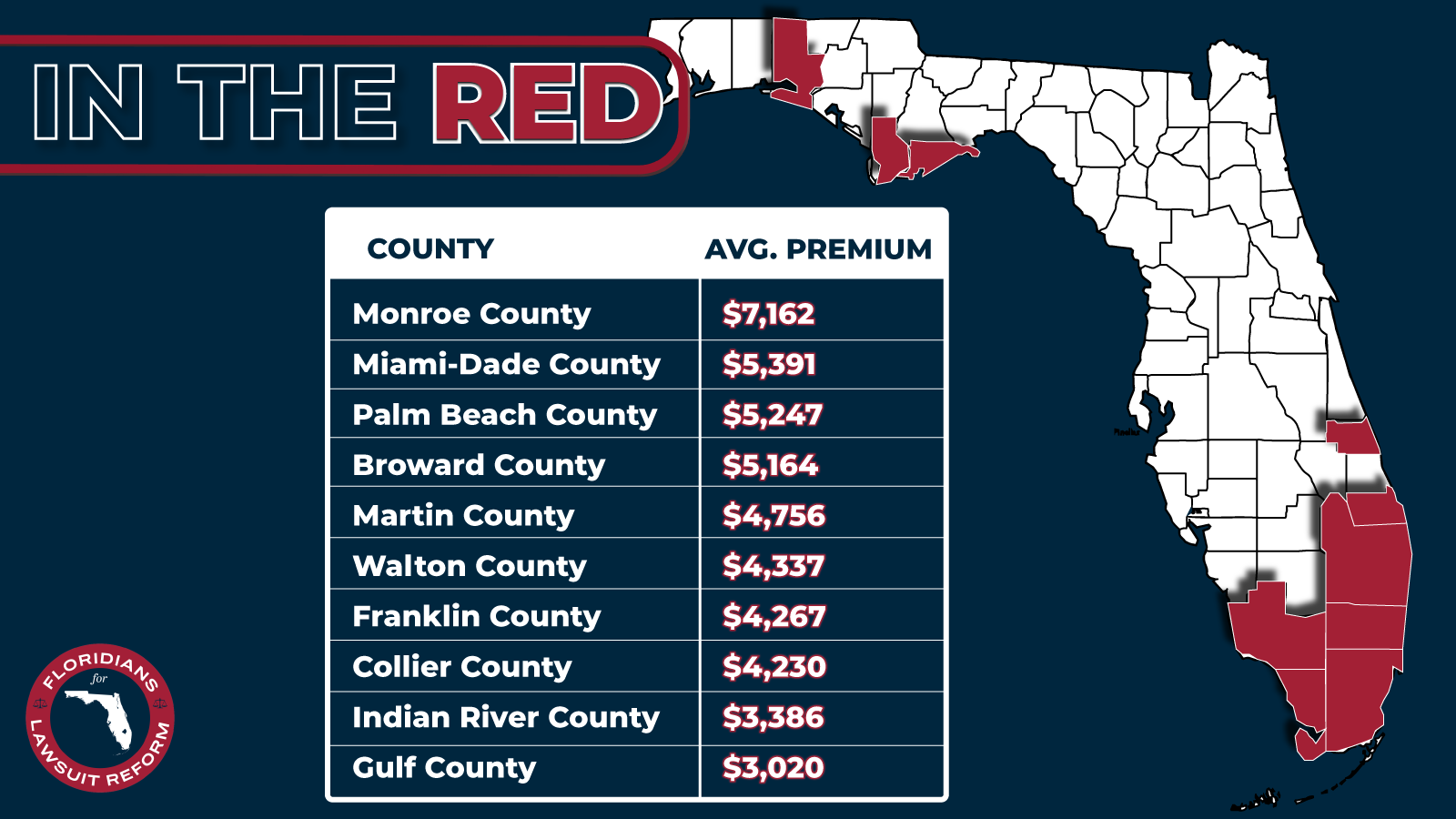

Average Costs and Regional Variations

While it’s challenging to provide a precise average due to the numerous variables, the statewide average for homeowners insurance in Florida can often range from $3,000 to over $6,000 per year, with many homeowners paying significantly more, especially in high-risk coastal zones.

Regional variations are substantial:

- Coastal Areas (e.g., Miami, Fort Lauderdale, Naples, the Florida Panhandle): These regions typically see the highest premiums due to their direct exposure to hurricanes and storm surge. Homes here might easily exceed $5,000 to $10,000 annually, and even more for larger or luxury properties.

- Inland Areas (e.g., Orlando, Gainesville, Jacksonville): While not immune to hurricane impacts (especially wind and heavy rain), these areas generally experience lower premiums than coastal zones. Averages here might fall closer to the $2,500 to $4,500 range, though still higher than national averages.

- South Florida: Often faces the highest rates due to its hurricane exposure and dense population.

- North Florida: While still vulnerable, sometimes sees slightly lower rates than South Florida if not directly on the coast, but this can vary greatly.

It’s crucial for prospective homeowners to obtain multiple quotes tailored to their specific property and location to get an accurate picture of the costs. This research is just as important as evaluating property taxes or maintenance costs when considering a long-term stay or investment in a Florida home.

Navigating the Challenges: What Makes Florida Unique?

The insurance market in Florida is often described as volatile and challenging, a direct consequence of the state’s unique geographical and legal environment. For anyone considering buying a vacation property in Florida or relocating to enjoy the state’s vibrant tourism and lifestyle, understanding these intricacies is not merely academic; it’s a practical necessity that can profoundly impact financial planning and peace of mind. The dynamic nature of the insurance landscape means that what was true last year might not be true today, requiring continuous vigilance and adaptation from homeowners.

The Impact of Natural Disasters and Climate

Florida‘s subtropical climate, while a major draw for tourism and a desired lifestyle, is also its Achilles’ heel when it comes to insurance. The state is uniquely vulnerable to a range of natural disasters, primarily:

- Hurricanes and Tropical Storms: As previously mentioned, Florida experiences the highest number of direct hurricane landfalls in the United States. These storms bring devastating winds, torrential rains, and storm surge, capable of causing catastrophic damage to homes, infrastructure, and personal property. Historical events like Hurricane Andrew in 1992 and more recent storms like Hurricane Ian have resulted in billions of dollars in insured losses, shaking the very foundation of the insurance market.

- Flooding: Beyond storm surge, heavy rainfall often leads to widespread inland flooding, which is typically not covered by a standard homeowners policy. This necessitates separate flood insurance, usually through the National Flood Insurance Program (NFIP), adding another layer of cost and complexity.

- Sinkholes: Florida’s limestone bedrock and abundant groundwater make it prone to sinkhole activity, particularly in areas like Central Florida. While basic homeowners policies may offer some limited coverage for catastrophic ground collapse, comprehensive sinkhole coverage often requires an additional endorsement, further increasing costs.

The increasing frequency and intensity of these events, potentially linked to climate change, mean that insurers face higher risks and greater payouts. This leads them to either raise premiums dramatically, limit coverage options, or, in some cases, withdraw from the Florida market altogether. This situation directly affects individuals looking for a tranquil retirement in Jacksonville or those managing a portfolio of vacation rentals near Disney World.

The Evolving Insurance Market and Its Effects on Residents and Visitors

The dynamic and often turbulent Florida insurance market has a ripple effect on anyone with a stake in the state’s real estate.

- Shrinking Private Market: In recent years, numerous private insurance companies have either stopped writing new policies in Florida, non-renewed existing customers, or even gone insolvent. This significantly reduces competition and options for homeowners, driving up prices among the remaining carriers.

- Reliance on Citizens Property Insurance Corporation: As private insurers retreat, more and more Florida homeowners are forced to turn to Citizens Property Insurance Corporation, the state-backed insurer of last resort. While Citizens offers a lifeline, its role as the primary insurer for a large segment of the population can pose risks to the state’s finances, and its policies may be less comprehensive or more expensive than a robust private market would offer.

- Legislative Reforms: The Florida Legislature has passed several significant reforms in an attempt to stabilize the market, curb litigation abuse, and attract more private insurers. These reforms aim to reduce fraud, limit attorney fees, and streamline the claims process. While the long-term effects are still unfolding, these changes reflect the urgent need to make insurance more available and affordable.

- Impact on Real Estate Decisions: For those considering a purchase, the high and unpredictable cost of insurance can be a deal-breaker. It’s not uncommon for insurance quotes to add hundreds, even thousands, of dollars to a monthly mortgage payment, making some properties financially unfeasible. This is particularly relevant for those planning to buy a second home or a property for long-term accommodation that might otherwise seem affordable based on the listing price.

- Due Diligence is Crucial: Potential buyers must perform extensive due diligence on insurance before making an offer. This includes getting actual quotes for the specific property, understanding its wind mitigation features, and checking its flood zone designation. Relying solely on estimates can lead to severe budget shortfalls.

Understanding these challenges is not about deterring people from enjoying all that Florida has to offer, but rather about equipping them with the knowledge to navigate its unique property landscape effectively. It ensures that the dream of a Florida lifestyle or a profitable tourism venture remains a sustainable reality.

Types of Coverage and Essential Considerations for Florida Homes

When exploring homeowners insurance in Florida, it’s crucial to understand that not all policies are created equal, and some essential protections are often excluded from standard coverage. For both residents and those considering a long-term stay or an investment in a vacation rental, this knowledge forms the bedrock of responsible property ownership and contributes to a stress-free Florida lifestyle. Properly understanding your coverage means you can fully enjoy the state’s attractions, from the beaches of Clearwater to the nightlife of South Beach, knowing your most significant asset is protected.

Standard Policies and Additional Protections

A typical homeowners insurance policy (often an HO-3 policy) in Florida generally provides several core coverages:

- Dwelling Coverage: Protects the physical structure of your home, including the roof, walls, and foundation, against covered perils. Given Florida’s weather, ensuring adequate dwelling coverage for full replacement cost is paramount.

- Other Structures Coverage: Covers detached structures on your property, such as a garage, shed, or fence.

- Personal Property Coverage: Protects your belongings inside your home, from furniture to electronics, against theft or damage from covered perils.

- Loss of Use (Additional Living Expenses): If your home becomes uninhabitable due to a covered loss, this coverage helps pay for temporary housing, food, and other living expenses while your home is being repaired. This is particularly important after a hurricane, when repairs can take months.

- Personal Liability: Provides financial protection if someone is injured on your property and you are found legally responsible. This is vital for owners of vacation rentals, where guests are frequent.

- Medical Payments: Covers medical expenses for guests injured on your property, regardless of fault, up to a certain limit.

However, in Florida, there are critical exclusions and additional coverages to consider:

- Windstorm Coverage: While standard policies typically include wind coverage, in many coastal or high-risk areas, wind damage (especially from hurricanes) may be subject to a separate, higher deductible (often 2% to 10% of the dwelling coverage amount). In some very high-risk zones, windstorm coverage might even need to be purchased from a separate insurer, like Citizens Property Insurance Corporation.

- Flood Insurance: As mentioned, standard homeowners insurance does not cover flood damage. This is a separate policy, primarily offered through the National Flood Insurance Program (NFIP). Given Florida’s susceptibility to both coastal and inland flooding, flood insurance is highly recommended, and often required by lenders, even outside of designated flood zones.

- Sinkhole Coverage: Standard policies usually only cover “catastrophic ground collapse,” which is a very high bar to meet. To protect against less severe but still damaging sinkhole activity, a separate sinkhole endorsement is often necessary, particularly in sinkhole-prone areas.

- Loss Assessment Coverage: If you live in a condominium or homeowner association (HOA) community, this coverage protects you if the association levies a special assessment for damages to common areas that exceed the HOA’s master policy limits.

- Ordinance or Law Coverage: This is crucial in Florida. After a significant event, building codes may have changed, requiring more expensive repairs or demolition of undamaged portions of your home. This coverage helps pay for the increased costs to bring your home up to current building codes.

Tips for Securing Affordable Homeowners Insurance

While “affordable” is relative in Florida, there are strategies homeowners can employ to mitigate costs:

- Shop Around Extensively: Get quotes from multiple insurance providers. The rates can vary wildly between companies. Don’t just rely on online quotes; speak to independent agents who can access policies from various carriers, including smaller regional ones.

- Focus on Wind Mitigation: Invest in home improvements that make your home more resistant to wind damage. This includes reinforced garage doors, hurricane shutters or impact-resistant windows, roof-to-wall attachments, and a reinforced roof deck. A wind mitigation inspection can identify these features and often lead to substantial discounts.

- Increase Your Deductible: Opting for a higher deductible, especially for your hurricane deductible, will lower your annual premium. However, ensure you have sufficient savings to cover this deductible if a claim arises.

- Maintain a Good Credit Score: Insurers in Florida often use credit-based insurance scores to help determine premiums. A higher credit score can translate to lower rates.

- Bundle Policies: If possible, bundle your homeowners insurance with other policies, such as auto insurance, with the same provider for multi-policy discounts.

- Review Your Policy Annually: Don’t let your policy renew without reviewing it. Market conditions change, and new discounts may become available. Your circumstances might also change, warranting adjustments to your coverage.

- Consider the Age of Your Roof: A newer roof (especially one installed to current building codes) will generally yield lower premiums. If your roof is old, replacing it might not only protect your home better but also significantly reduce your insurance costs.

By diligently applying these strategies and understanding the nuances of the Florida insurance market, homeowners can better manage their costs and secure the necessary protection for their cherished properties, ensuring their enjoyment of the Sunshine State remains unburdened by unforeseen financial surprises.

Homeowners Insurance and Your Florida Lifestyle: A Broader Perspective

Beyond the immediate financial burden, the cost and availability of homeowners insurance in Florida have a profound impact on lifestyle decisions, real estate trends, and the overall appeal of the state for tourism and long-term accommodation. For those drawn to Florida for its unparalleled travel experiences, its array of hotels and resorts, and its promise of a vibrant lifestyle, understanding this critical aspect of property ownership is essential. It influences everything from where you might choose to live to the viability of investing in the booming vacation rental market.

Investing in Vacation Rentals and Second Homes

Florida is a prime location for investing in vacation rentals and second homes, particularly in popular tourist destinations like Orlando, Miami, and the various coastal towns. Owners often seek to capitalize on the constant influx of tourists by offering unique accommodation options beyond traditional hotels. However, the insurance implications for such properties are significantly more complex and expensive:

- Higher Premiums for Non-Owner Occupied Properties: Insurance companies view properties that are not owner-occupied, especially those used for short-term rentals, as higher risk. There’s a greater chance of liability claims from guests, and potentially less vigilance against small issues becoming larger problems. As a result, premiums for vacation rentals or investment properties are typically higher than for primary residences.

- Specific Coverage Needs: Standard homeowners policies often have exclusions for commercial activities like short-term rentals. Owners need to ensure they have appropriate coverage, which might include a landlord policy or a specialized short-term rental policy that includes comprehensive liability coverage, loss of income protection, and coverage for contents owned by the landlord. This is crucial for protecting the investment and maintaining profitability.

- Navigating Local Regulations: Beyond insurance, owners of vacation rentals must also contend with evolving local regulations, zoning laws, and licensing requirements, which vary significantly from city to city. For instance, operating a short-term rental in Miami Beach might have entirely different rules and costs than in St. Petersburg.

- Impact on Profitability: The high cost of specialized insurance, combined with property taxes, HOA fees, and maintenance, can significantly eat into the potential profits of a vacation rental. Prospective investors must factor these costs accurately into their financial projections to ensure the venture remains viable. For those dreaming of a luxury travel experience for their guests, these fundamental costs cannot be overlooked.

Peace of Mind for Long-Term Stays and Relocation

For individuals and families considering a permanent move to Florida or a prolonged stay to enjoy its lifestyle, the insurance landscape directly impacts their quality of life and financial stability:

- Budgeting for the True Cost of Living: Understanding and budgeting for realistic insurance costs is as important as considering housing prices, utility bills, and other living expenses. An underestimate can lead to significant financial strain and diminish the enjoyment of the Florida lifestyle.

- Property Selection: Insurance costs can influence where prospective residents choose to buy. A dream home on the beach in Key West might come with an insurance bill that makes it unaffordable, pushing buyers towards inland communities or properties with superior hurricane-mitigation features. This choice impacts access to specific attractions, local culture, and overall daily experiences.

- The Psychological Impact of Risk: Living in a hurricane-prone state with a volatile insurance market can create anxiety for homeowners. Knowing you have robust and reliable coverage, even if expensive, provides essential peace of mind, allowing residents to fully immerse themselves in the rich experiences Florida offers, from exploring historical landmarks to participating in local activities.

- Maintaining and Upgrading Homes: The incentive to upgrade homes with features like impact-resistant windows or a stronger roof is not just about personal safety; it’s also about reducing insurance premiums. This means that home maintenance in Florida often has an added financial dimension tied directly to insurance costs, influencing decisions about property improvements and long-term upkeep.

In conclusion, while Florida offers an unparalleled quality of life, rich travel opportunities, and diverse accommodation options, the cost and complexities of homeowners insurance are an integral part of its unique landscape. Navigating this environment effectively requires thorough research, proactive planning, and a deep understanding of the factors at play. By doing so, individuals can ensure their Florida dream remains a sustainable and enjoyable reality, allowing them to fully embrace the adventures and relaxation that the Sunshine State promises.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.