Unlike many states that employ a progressive income tax system, where higher earners pay a larger percentage of their income in taxes, [Colorado] stands out with its unique flat tax rate. This distinct approach simplifies the tax process for many, but it still has nuances that residents, part-year residents, and even some non-residents need to understand. Beyond income tax, [Colorado]’s broader tax structure – encompassing sales tax, property tax, and specific industry-related taxes – contributes to its economy, funding everything from infrastructure to public services that enhance both resident life and the visitor experience. This article aims to demystify [Colorado] state income tax, examining its core principles, who is subject to it, and how it fits into the larger financial picture of this enchanting state, all while keeping in mind the perspectives of travelers, potential residents, and those seeking to immerse themselves in [Colorado]’s lifestyle.

Understanding Colorado’s Unique Flat Tax System

[Colorado]’s approach to state income tax is a cornerstone of its financial policy, and it’s particularly noteworthy for its simplicity compared to many other [United States] jurisdictions. While many states implement a tiered system where tax rates increase with income, [Colorado] has long adhered to a flat tax rate. This means that, regardless of your income level, all taxable income is subject to the same percentage rate. This system is often lauded for its transparency and ease of understanding, yet its implications for various income brackets and the state’s revenue generation are subjects of ongoing discussion. For anyone considering the cost of living in [Denver] or evaluating the financial viability of a long-term stay in [Fort Collins], grasping this fundamental aspect is key.The consistency of the flat tax rate offers a predictable financial environment for both individuals and businesses, which can be particularly appealing for entrepreneurs or those looking to invest in [Colorado]’s burgeoning tourism and technology sectors. However, it’s essential to remember that while the state income tax rate is flat, other taxes and financial obligations can vary significantly by county or municipality, influencing the overall financial landscape of different [Colorado] destinations. This often includes local sales taxes, which can impact the cost of goods and services, and property taxes, which are a major consideration for homeowners or those renting in specific areas.

The Basics of the Colorado Income Tax Rate

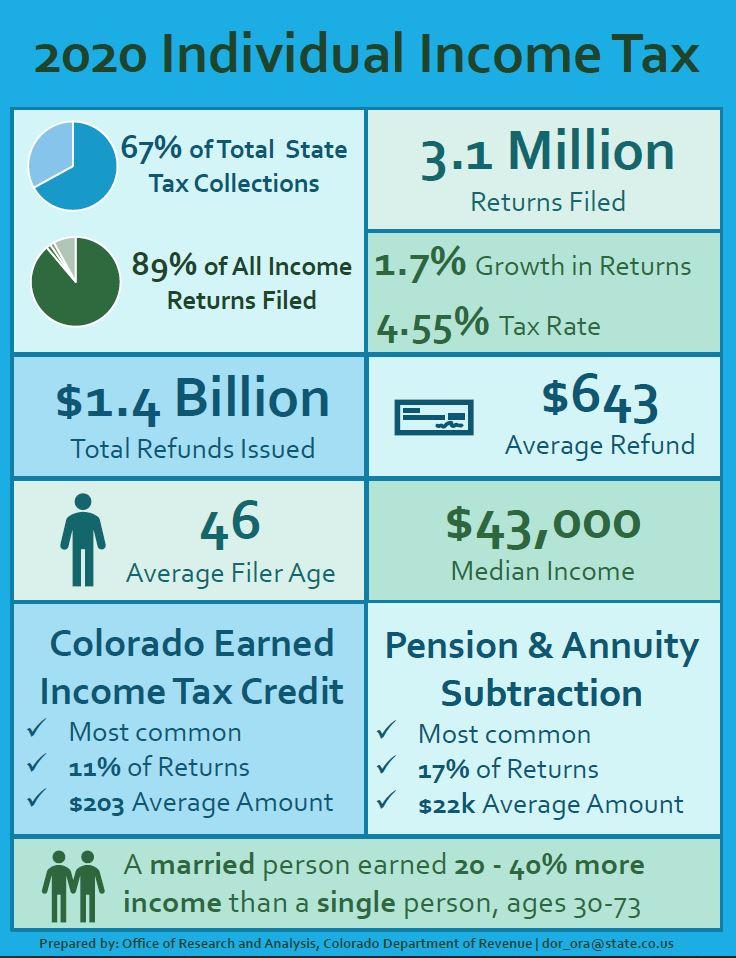

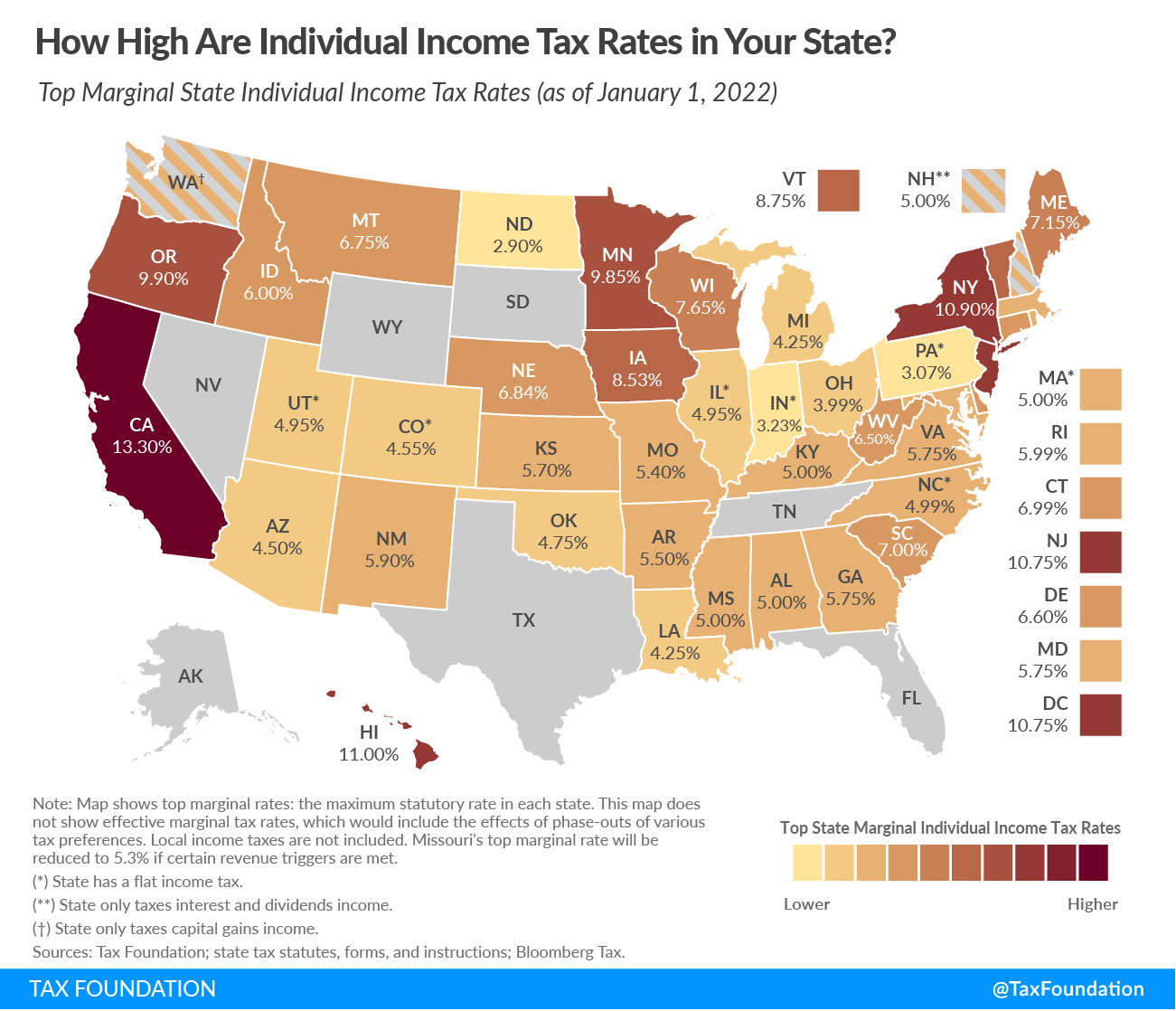

At the heart of [Colorado]’s income tax system is its flat rate. As of recent periods, this rate has typically hovered around the low to mid-4% range, applying uniformly to all income subject to state taxation. This consistency is a significant departure from the progressive tax structures found in many other states, where higher income brackets face incrementally higher tax percentages. For instance, if the rate is 4.40%, every dollar of taxable income—whether it’s the first dollar or the millionth—is taxed at that same 4.40%. This fixed percentage simplifies tax calculations for individuals and businesses operating within the state.

This flat rate applies to wages, salaries, business income, investment income, and most other forms of income earned by [Colorado] residents or income sourced from [Colorado] for non-residents. While the rate itself is flat, the calculation of taxable income involves several steps, including adjustments, deductions, and exemptions, which can reduce the amount of income ultimately subject to the state tax. Understanding these elements is crucial for accurate tax planning and ensures that individuals and entities are meeting their obligations while also taking advantage of any available benefits. The [Colorado Department of Revenue] is the primary authority for up-to-date information on the current flat tax rate and all associated regulations, making it an invaluable resource for both new and long-term residents.

Who Needs to File a Colorado Income Tax Return?

The obligation to file a [Colorado] income tax return extends beyond just full-time residents. Understanding who is required to file is critical, especially for the diverse demographic that interacts with the [Centennial State] – from seasonal workers at ski resorts to digital nomads enjoying the mountain lifestyle, and even those who own vacation properties.

Generally, you must file a [Colorado] income tax return if you are:

- A full-year resident of [Colorado]: If your permanent home (domicile) was in [Colorado] for the entire tax year, you are considered a full-year resident and must report all your income, regardless of where it was earned, to the state.

- A part-year resident of [Colorado]: If you moved into or out of [Colorado] during the tax year, you are a part-year resident. You will typically be taxed on all income received while you were a [Colorado] resident and on any income sourced from [Colorado] during the portion of the year you were a non-resident. This is a common scenario for those relocating for work or retirement, affecting financial planning around accommodation and lifestyle changes.

- A non-resident with [Colorado]-sourced income: Even if you do not live in [Colorado], if you earned income from sources within the state, you generally must file a [Colorado] income tax return. This includes income from a [Colorado] business, rental income from [Colorado] property (a significant consideration for those investing in vacation rentals or apartments), or wages for work performed within [Colorado] (relevant for remote workers whose company is based in the state, or those traveling for temporary contracts). For example, a non-resident who owns a rental property in [Breckenridge] would need to report the income generated from that property to the state.

- Required to file a federal income tax return and you have gross income from [Colorado] sources: Even if your total income is below the federal filing threshold, if you have [Colorado]-sourced income, you might still need to file a state return.

For travelers, this means if you perform work remotely for a [Colorado]-based company while staying in a hotel or apartment in [Denver], your income could be considered [Colorado]-sourced. Similarly, if you derive income from an investment property in [Colorado] while residing elsewhere, that income will likely be subject to [Colorado] state income tax. The complexities for part-year residents and non-residents often revolve around properly allocating income between [Colorado] and other states, making careful record-keeping and potentially professional tax advice invaluable.

Navigating Taxable Income and Key Deductions for Colorado Residents and Visitors

Understanding the flat tax rate is just the first step; the next crucial element is knowing what income is actually taxable and what deductions and credits are available to reduce that taxable amount. For individuals and families planning a move to [Colorado], or even those managing investment properties or businesses within the state, these details can significantly impact their overall financial picture. From the wages earned in [Colorado]’s bustling tourism sector to the rental income from a vacation home near the [Rocky Mountains National Park], various income streams are subject to taxation, but the state also provides avenues for reducing that liability.

The interplay of taxable income and available deductions is particularly relevant for those exploring different lifestyles in [Colorado]. Whether you’re a high-earning professional working in [Denver]’s tech scene, a retiree enjoying the mild climate of [Colorado Springs], or a family taking advantage of the state’s family-friendly attractions, understanding these tax components helps in budgeting and financial forecasting. It impacts everything from the cost of daily living to the profitability of long-term investments in accommodation or local businesses.

What Constitutes Taxable Income in Colorado?

In [Colorado], taxable income generally aligns with the federal definition of adjusted gross income (AGI), with certain state-specific modifications. This means that most types of income that are taxable at the federal level are also taxable by [Colorado]. Common sources of taxable income include:

- Wages, Salaries, and Tips: This is the most straightforward category, encompassing income from employment within [Colorado], whether full-time, part-time, or seasonal work often found in tourist destinations like [Aspen] or [Vail].

- Business Income: Profits from sole proprietorships, partnerships, S corporations, and other business entities are generally taxable. This is a significant factor for entrepreneurs setting up businesses in [Colorado] or remote workers operating as independent contractors.

- Rental Income: Income derived from real estate properties located in [Colorado], such as apartments, vacation homes, or commercial spaces, is taxable. This is particularly relevant for investors in [Colorado]’s thriving accommodation market, whether through short-term rentals in popular destinations or long-term leases in cities like [Boulder].

- Interest and Dividends: Income earned from savings accounts, bonds, stocks, and other investments is typically taxable.

- Capital Gains: Profits from the sale of assets, such as real estate or stocks, are generally included in taxable income. Given [Colorado]’s dynamic real estate market, capital gains from property sales can be substantial.

- Retirement Income: While some states offer exemptions for certain types of retirement income, [Colorado] generally taxes pension and annuity income, though some deductions may apply for eligible seniors.

- Gambling and Lottery Winnings: Winnings from sources within [Colorado] are considered taxable income.

It’s important to note that while the starting point is often federal AGI, [Colorado] has specific additions and subtractions that modify this figure to arrive at the state’s taxable income. For instance, certain municipal bond interest might be exempt at the federal level but taxable by [Colorado], or vice versa for specific [Colorado] bond interest. Keeping track of these state-specific adjustments is crucial for accurate filing.

Common Deductions and Credits Affecting Your Colorado Tax Bill

While [Colorado] has a flat tax rate, various deductions and credits can significantly reduce your taxable income, thereby lowering your overall tax liability. These provisions are designed to provide financial relief for different taxpayer situations, aligning with the state’s efforts to support residents and stimulate its economy. Understanding and utilizing these benefits is a key aspect of smart financial planning, especially for those new to the state or managing diverse income streams.

Key Deductions and Credits include:

- Standard Deduction vs. Itemized Deductions: Taxpayers can choose between taking a standard deduction or itemizing their deductions. The [Colorado] standard deduction amount changes annually and is generally tied to federal guidelines, offering a straightforward reduction for many taxpayers. Itemized deductions, on the other hand, allow individuals to deduct specific expenses like mortgage interest, state and local taxes (SALT cap applies federally), and charitable contributions, potentially offering greater savings for those with substantial qualifying expenses, particularly homeowners in areas with high property values.

- Property Tax/Rent/Heat Credit: This valuable credit is available to eligible low-income seniors and individuals with disabilities. It provides a refund for a portion of the property taxes paid (or rent paid, which is deemed to include property tax) or heating expenses. This is particularly helpful for managing the cost of accommodation, especially for vulnerable populations in [Colorado].

- Child Care Expenses Credit: Families incurring child care expenses may be eligible for a credit, which can significantly alleviate the financial burden of raising children in [Colorado], making family trips and long-term stays more affordable.

- Enterprise Zone Credits: [Colorado] has designated “Enterprise Zones” in certain economically distressed areas to encourage business development and job creation. Businesses and individuals investing or operating within these zones may qualify for various tax credits, which can be a draw for entrepreneurs considering new ventures in [Colorado].

- Conservation Easement Credit: For those passionate about preserving [Colorado]’s natural beauty, donating a conservation easement can provide a substantial tax credit, aligning with the state’s commitment to protecting its landscapes and landmarks.

- Pension and Annuity Subtraction: Eligible seniors may be able to subtract a certain amount of pension and annuity income from their taxable income, providing financial relief for retirees choosing [Colorado] for their golden years.

- Federal Tax Deduction: A unique feature in [Colorado] is the ability to deduct a portion of the federal income tax paid from your [Colorado] taxable income. This deduction further reduces the state income tax burden for many residents.

Navigating these deductions and credits requires careful record-keeping and an understanding of eligibility criteria. For many, consulting with a tax professional familiar with [Colorado] tax law is a wise investment, especially when dealing with complex income situations such as those from business ventures, rental properties, or significant investments, or when transitioning residency.

The Broader Tax Landscape: Beyond Income Tax in the Centennial State

While state income tax is a significant component of [Colorado]’s financial framework, it’s far from the only tax influencing the cost of living, travel, and business operations in the [Centennial State]. For visitors and potential residents alike, understanding the broader tax landscape, including sales tax, local levies, and property taxes, is essential for a comprehensive financial picture. These taxes play a crucial role in funding local amenities, maintaining public services, and shaping the economic viability of various [Colorado] destinations, impacting everything from the price of a souvenir in [Denver] to the long-term investment in a vacation rental.

The combination of different tax types means that the overall tax burden can vary considerably depending on where you live, what you buy, and what kind of lifestyle you lead in [Colorado]. For example, the total sales tax rate you pay will depend on the city and county, while property taxes are influenced by local assessments and mill levies. These variations underscore the importance of looking beyond just the income tax rate when planning a trip, considering accommodation options, or evaluating a move to [Colorado].

Sales Tax and Local Levies: What Travelers and Consumers Should Know

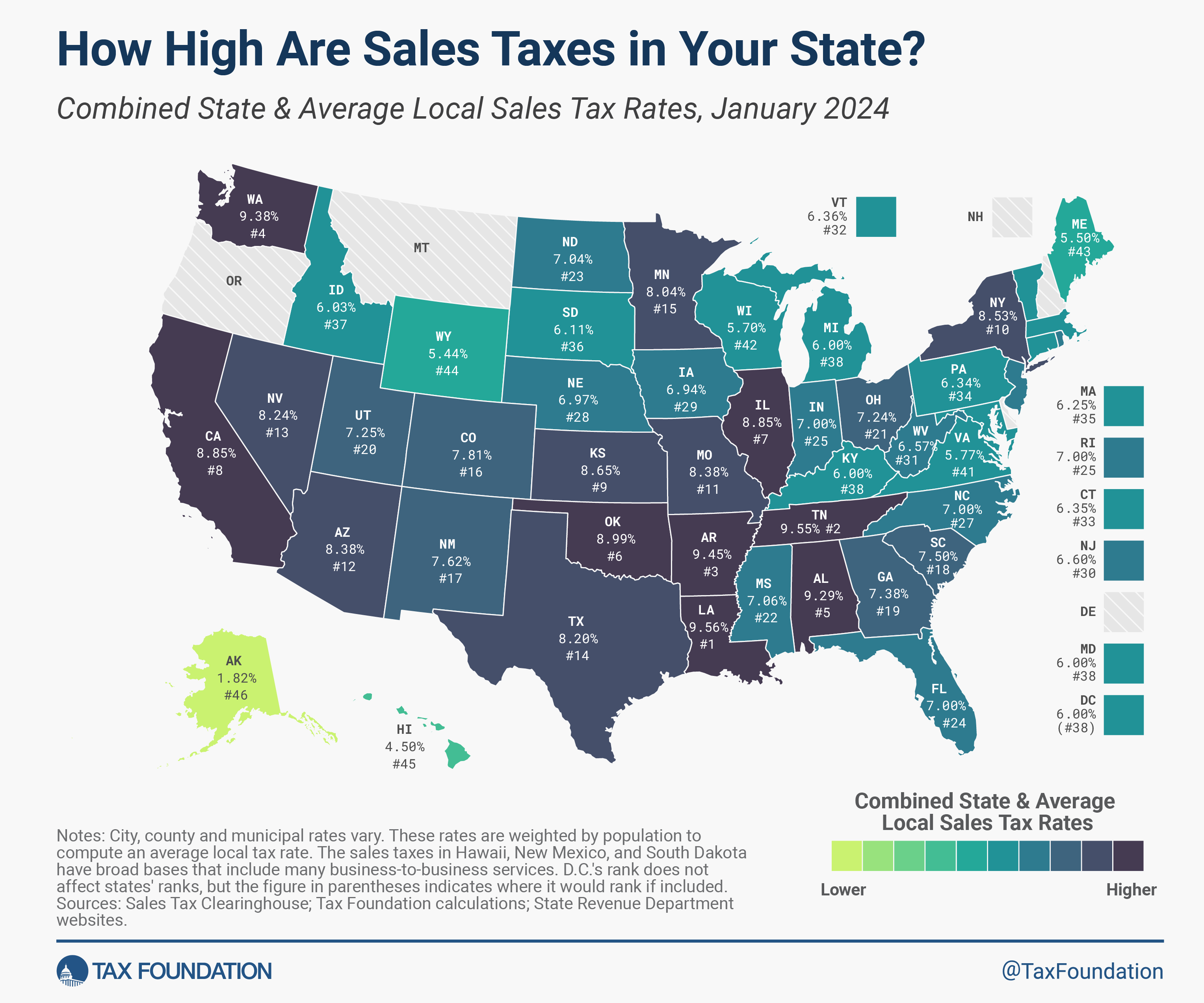

For anyone traveling through [Colorado] or engaging in consumer activities, sales tax is an immediate and tangible part of nearly every transaction. Unlike the state’s flat income tax, sales tax rates are far more dynamic, varying significantly by jurisdiction. [Colorado] imposes a statewide sales tax, but cities, counties, and special districts can levy additional sales taxes, leading to a patchwork of rates across the state. This means that buying a souvenir in [Aspen], dining in [Boulder], or purchasing groceries in [Colorado Springs] could incur different total sales tax percentages.

- State Sales Tax: [Colorado] has a relatively low statewide sales tax rate compared to many other states. However, this is just the base.

- Local Sales Taxes: Cities and counties have the authority to add their own sales taxes. For instance, a major city like [Denver] will have a higher combined sales tax rate than a rural area due to additional city and county levies. These local taxes are critical for funding municipal services, local attractions, and community infrastructure, directly enhancing the visitor experience.

- Special District Taxes: Many areas also have special district taxes that fund specific projects or services, such as transit authorities or cultural districts. These can add further complexity to the sales tax rate.

- What’s Taxed: Generally, sales tax applies to most retail sales of tangible personal property. Services are typically not taxed unless specifically enumerated by law. Prepared food, alcoholic beverages, and lodging are almost always subject to sales tax, which is a key consideration for tourism and hotel expenses.

- Tourism Impact: For tourists, sales tax directly impacts the cost of accommodations (hotels, suites, apartments), restaurant meals, entertainment, and retail purchases. When budgeting for a trip to [Colorado], it’s wise to factor in these varying sales tax rates, as they can add up, particularly in popular tourist destinations where local sales taxes tend to be higher to support local tourism infrastructure.

Understanding these localized sales tax rates is vital for managing a travel budget or assessing the true cost of goods and services in different parts of [Colorado], ensuring a seamless and financially predictable experience.

Property Taxes and Their Impact on Colorado’s Real Estate Market

Property taxes are another critical component of [Colorado]’s tax structure, particularly for homeowners, real estate investors, and those evaluating long-term accommodation options. While not directly impacting most short-term travelers, property taxes significantly influence the cost of housing, rental rates, and the overall economic landscape of local communities. They are the primary funding source for local services like schools, libraries, and emergency services, directly contributing to the quality of life and attractiveness of [Colorado]’s cities and towns.

- Assessment and Valuation: In [Colorado], property taxes are based on the assessed value of real estate. County assessors determine property values, which are typically a percentage of the actual market value. Property values in [Colorado] can vary dramatically, from the high-end luxury properties in [Aspen] and [Vail] to more modest homes in suburban areas, directly influencing the property tax bill.

- Mill Levies: The actual tax rate applied to the assessed value is determined by local taxing authorities (counties, cities, school districts, fire districts, etc.) through what are called “mill levies.” A mill levy represents the amount of tax per $1,000 of assessed value. Since multiple taxing authorities can levy taxes on a single property, the combined mill levy can vary significantly from one location to another, even within the same county.

- Impact on Homeowners and Renters: For homeowners, property taxes are a recurring expense that needs to be factored into their budget. For renters, property taxes indirectly affect rent prices, as landlords typically incorporate these costs into their rental rates. This means that living in areas with higher property taxes, such as desirable neighborhoods in [Denver] or scenic mountain towns, generally translates to higher rental costs.

- Real Estate Investment: For those looking to invest in [Colorado]’s real estate market, perhaps acquiring an apartment for long-term rental or a villa for short-term tourism accommodation, understanding local property tax rates is paramount. High property taxes can erode rental yields or increase the holding costs of investment properties, making thorough due diligence crucial.

- Gallagher Amendment (Historically): While the [Gallagher Amendment] was repealed by [Colorado] voters in 2020, its historical impact shaped the state’s property tax landscape by limiting the residential assessment rate. Its repeal has led to ongoing discussions and potential shifts in property tax burdens, underscoring the dynamic nature of tax policy and its importance for real estate planning.

In summary, property taxes, while complex, are a fundamental aspect of [Colorado]’s financial fabric, influencing everything from housing affordability to local economic development. For anyone considering a permanent move, investing in real estate, or even planning an extended stay that involves renting, a grasp of these taxes is indispensable.

Planning Your Colorado Stay or Move: Income Tax Considerations for a Seamless Experience

Whether you’re enchanted by the idea of remote work from a cozy mountain cabin, envisioning a business venture amidst [Colorado]’s vibrant economy, or simply planning an extended exploration of its natural wonders, understanding the nuances of state income tax is key to a seamless and financially sound experience. The “lifestyle” aspect of [Colorado] living—be it luxury travel, budget adventures, family trips, or extended business stays—is invariably linked to financial planning, and income tax sits at the core of this. For digital nomads, entrepreneurs, and property owners, specific considerations come into play, influencing decisions about residency, business structure, and investment strategies.

[Colorado]’s blend of outdoor recreation, cultural attractions, and economic opportunities makes it a magnet for diverse populations. However, successfully navigating the state’s offerings, both personally and professionally, requires an awareness of the tax implications. This section delves into the specific income tax considerations for those whose relationship with [Colorado] extends beyond a typical short-term tourist visit, aiming to provide insights for a more informed and worry-free engagement with the [Centennial State].For Remote Workers and Digital Nomads: Establishing Residency and Tax Implications

The rise of remote work has made [Colorado] an increasingly popular destination for digital nomads and individuals seeking a better work-life balance amidst stunning natural backdrops. However, working remotely from [Colorado] or establishing a temporary base carries specific income tax implications related to residency that can often be overlooked.

- Defining Residency: For tax purposes, “residency” is not always straightforward. If you spend a significant portion of the year in [Colorado] (generally more than 183 days), or if your primary home is considered to be in [Colorado], you may be deemed a [Colorado] resident for tax purposes, even if you maintain ties to another state. This means all your worldwide income could become subject to [Colorado]’s flat income tax rate.

- Part-Year Residency: If you move to [Colorado] mid-year, you’ll be a part-year resident. This requires careful tracking of income earned during your residency period versus income earned elsewhere, and potentially filing tax returns in both [Colorado] and your previous state of residence.

- Non-Resident with [Colorado]-Sourced Income: Even if you maintain residency elsewhere, if you perform work physically within [Colorado] for any period (e.g., attending a conference, working on a temporary project, or even taking an extended working vacation), the income earned during that time could be considered [Colorado]-sourced and thus taxable by the state. This is especially relevant for self-employed digital nomads who might generate income while staying in a [Colorado] hotel or rental apartment.

- “Convenience of the Employer” Rule (Less common in [Colorado] but good to be aware of in other states): Some states have rules where income earned by a remote worker whose employer is in that state is taxable there, even if the employee lives elsewhere, if the work is performed remotely for the convenience of the employee. While [Colorado] doesn’t typically apply this rule aggressively for out-of-state residents, it’s worth understanding the potential for income to be sourced to [Colorado] if the employer is based there.

- Documentation and Record-Keeping: To avoid potential issues, remote workers and digital nomads should meticulously document their physical presence, income sources, and residency status. This includes keeping records of travel dates, rental agreements, utility bills, and proof of residency in other states if applicable.

Understanding these nuances is crucial for enjoying the [Colorado] lifestyle without unexpected tax burdens. It’s often advisable for digital nomads with complex situations to consult with a tax professional experienced in multi-state taxation to ensure compliance and optimize their tax strategy.

Business and Investment Income: A Guide for Entrepreneurs and Property Owners

[Colorado]’s robust economy and growing tourism sector present numerous opportunities for entrepreneurs and property owners. From starting a new business in [Denver] to investing in vacation rentals in mountain towns, these ventures come with specific income tax considerations that are vital for profitability and compliance.- Business Structures and Income Tax: The type of business entity you choose (sole proprietorship, partnership, LLC, S corporation, C corporation) has direct implications for how business income is taxed in [Colorado].

- Pass-Through Entities (Sole Proprietorships, Partnerships, S-Corps, LLCs taxed as such): For these entities, business profits “pass through” directly to the owners’ personal income tax returns and are then taxed at [Colorado]’s flat individual income tax rate. This is common for many small businesses, independent contractors, and those operating short-term rental properties.

- C Corporations: C corporations are taxed at the corporate level by [Colorado] (which also has a flat corporate income tax rate, often mirroring the individual rate), and then shareholders are taxed again on dividends (double taxation).

- Rental Property Income: Investing in [Colorado] real estate, whether for long-term rentals or short-term vacation accommodation, generates taxable income. This income is subject to [Colorado]’s flat income tax rate.

- Deductions for Rental Properties: Property owners can deduct various expenses related to their rental properties, including mortgage interest, property taxes, insurance, repairs, depreciation, and management fees. Maximizing these deductions is crucial for optimizing the profitability of a rental investment.

- Vacation Rentals (e.g., Airbnb, VRBO): Income from short-term vacation rentals is treated similarly to other rental income. However, if a property is rented for fewer than 14 days in a year, the income might be tax-free at the federal level, though [Colorado] law could have specific reporting requirements. For longer periods, it’s considered business income, and hosts must track income and expenses diligently.

- Sales Tax for Businesses: Businesses selling tangible goods or certain services in [Colorado] are responsible for collecting and remitting sales tax. This is particularly relevant for retail establishments, restaurants, and hotels (which collect lodging taxes). Entrepreneurs must ensure they are properly registered with the [Colorado Department of Revenue] and understand the varying local sales tax rates applicable to their operations.

- Withholding and Estimated Taxes: Self-employed individuals and those with significant investment or rental income are generally required to pay estimated income taxes throughout the year to cover their [Colorado] tax liability, similar to federal requirements. Failure to do so can result in penalties.

- Seeking Professional Advice: Given the complexities of business and investment taxation, especially with varying local regulations and potential multi-state implications, entrepreneurs and property owners in [Colorado] are strongly encouraged to consult with a [Colorado]-based tax accountant or financial advisor. This ensures compliance, maximizes legitimate deductions, and supports sound financial planning for their ventures in the [Centennial State].

In conclusion, while [Colorado]’s flat income tax rate offers a degree of simplicity, its broader tax landscape is layered with specific considerations for various individuals and entities. Whether you’re planning a visit, a move, or a new business endeavor, a comprehensive understanding of these tax principles will undoubtedly enhance your experience in this remarkable state.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.