Embarking on a journey to purchase property, whether for a permanent residence, a vacation retreat, or a strategic investment, is an exciting prospect. For many, the allure of the Lone Star State – with its vast landscapes, booming economy, diverse culture, and captivating cities – makes it a top destination for such endeavors. However, just as planning an unforgettable trip involves understanding all the associated expenses, so too does buying real estate. Beyond the sticker price of a home, there’s a crucial financial layer that often surprises first-time buyers and even seasoned investors: closing costs.

These are the various fees and charges incurred at the end of a real estate transaction, beyond the down payment. For those considering an extended stay, relocation, or acquiring an investment property like a short-term rental or a luxury villa in a vibrant Texan locale, comprehending these costs is paramount to budgeting effectively and ensuring a smooth transition into ownership. From the lively streets of Austin to the sprawling metropolis of Dallas, the energetic hub of Houston, or the historic charm of San Antonio, each region of Texas offers unique opportunities, but the fundamentals of closing costs remain a constant, requiring careful consideration. This comprehensive guide will demystify the intricacies of closing costs in Texas, providing clarity for anyone looking to make this dynamic state their next home or investment haven.

Understanding the Landscape of Closing Costs in Texas

When you’re planning a grand adventure or considering a long-term accommodation solution, budgeting is key. Similarly, when it comes to acquiring property in Texas, understanding the full financial picture is crucial. Closing costs represent the administrative and legal fees associated with transferring ownership of a property from the seller to the buyer. They are distinct from the down payment and the principal amount of the loan, and they are typically paid at the “closing” or “settlement” meeting. Without a clear grasp of these figures, a buyer might find themselves unexpectedly short on funds, potentially delaying or even jeopardizing their dream of owning a piece of the Lone Star State.

For individuals and families drawn to Texas for its burgeoning job markets, world-class educational institutions, diverse cultural experiences, or simply a change of scenery, real estate represents more than just a transaction; it’s an entry point into a new lifestyle. Investors, on the other hand, might eye a property in a popular tourist destination like South Padre Island or the Hill Country as a potential vacation rental or a boutique hotel conversion. In either scenario, the financial implications of closing costs can significantly impact the overall profitability and affordability of the venture. Unlike some states where closing costs might be more predictable, Texas has its own unique blend of fees and customs, making it essential to delve into the specifics. These costs are not arbitrary; they cover the services of various professionals involved in the transaction, from lenders and title companies to attorneys and appraisers, all working to ensure the legality and security of your property acquisition.

The Texan Appeal: Why Consider a Home Here?

Texas is more than just a geographical location; it’s a vibrant destination that offers a compelling blend of opportunities and attractions, making it an ideal place for both short-term visits and long-term stays. For travelers seeking diverse experiences, Texas delivers everything from the natural wonders of Big Bend National Park to the historical richness of the Alamo and the bustling cultural scenes of its major cities. Austin, known as the “Live Music Capital of the World,” draws visitors and new residents alike with its eclectic vibe, thriving tech industry, and vibrant culinary scene. Dallas and Houston stand as economic powerhouses, boasting impressive skylines, world-class museums, and diverse communities. Houston is also home to the NASA Johnson Space Center, a major landmark that attracts tourists from around the globe. Meanwhile, San Antonio enchants with its Spanish colonial missions, the iconic Alamo, and the picturesque Riverwalk, offering a unique blend of history and leisure.

The state’s appealing tax structure, including no state income tax, further enhances its attractiveness for those looking to relocate or invest in property, whether it’s a primary residence, a vacation home, or a property destined for short-term rentals. The steady growth of tourism along the Gulf Coast in areas like Galveston and Corpus Christi also creates lucrative opportunities for accommodation providers and real estate investors. Understanding closing costs isn’t just about budgeting; it’s about confidently entering a market that promises significant lifestyle and financial rewards. Whether you’re drawn to urban luxury, serene rural living in the Hill Country, or a beachfront escape, Texas offers a diverse portfolio of properties to suit every taste and ambition, making the investment in understanding its real estate processes well worth the effort.

Deconstructing the Costs: What Makes Up Closing Costs in Texas?

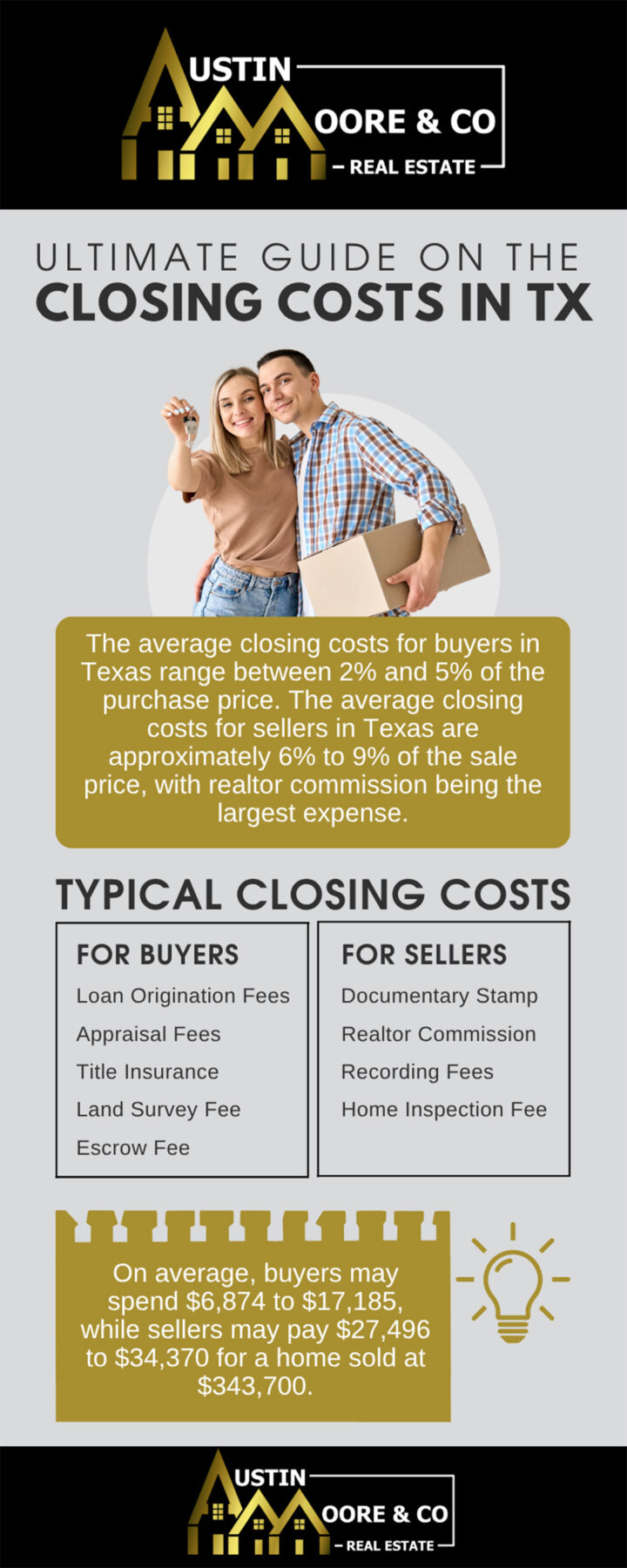

Closing costs are not a single fee but a collection of charges from various entities involved in the home buying process. These costs typically range from 2% to 5% of the loan amount, though this can vary significantly based on factors like the loan type, property value, and specific location within Texas. To truly prepare for your real estate venture, whether it’s for a permanent residence or a new addition to your portfolio of accommodation options, it’s vital to understand the common categories of fees you’ll encounter.

Lender-Related Fees

These fees are directly tied to the mortgage loan you obtain and compensate the lender for their services in processing and underwriting your loan.

- Loan Origination Fee: This is a charge for the administrative costs of processing your loan. It can be a flat fee or a percentage of the loan amount, typically ranging from 0.5% to 1.5%. This fee covers the lender’s overhead in setting up the loan.

- Underwriting Fee: This fee covers the cost of evaluating your loan application and determining whether you qualify for the loan. The underwriter assesses your creditworthiness, income, and the property’s value.

- Appraisal Fee: Before a lender can approve a mortgage, they require an independent appraisal of the property to ensure its value is at least equal to the loan amount. This protects the lender from lending more than the property is worth. Fees can range from $400 to $600 in Texas, varying by property size and location.

- Credit Report Fee: The lender pulls your credit report(s) to assess your credit history and score, which impacts your eligibility and interest rate. This is usually a small fee, around $20-$50.

- Flood Certification Fee: If the property is located in or near a designated flood zone, lenders are required to determine this. This fee covers the cost of obtaining a flood zone determination from a third party. While small, it’s a necessary check in areas prone to flooding, particularly near the Gulf Coast.

Title and Escrow Fees

These fees ensure that the property’s title is clear and that the transaction proceeds smoothly and legally.

- Title Search Fee: A title company conducts a thorough search of public records to ensure there are no liens, unpaid taxes, lawsuits, or other claims against the property that could complicate ownership. This is crucial for securing a clear title.

- Title Insurance (Owner’s and Lender’s): This is perhaps one of the most significant closing costs in Texas.

- Owner’s Title Insurance: Protects the buyer from any challenges to the property’s title that may arise after closing, such as errors in public records, forged documents, or undisclosed heirs. In Texas, the seller typically pays for the owner’s title policy, which is a significant saving for the buyer compared to many other states where the buyer covers this.

- Lender’s Title Insurance: This policy protects the lender’s interest in the property should a title defect arise. The buyer usually pays for this, as it’s a requirement for most mortgage loans. The cost is often based on the loan amount.

- Escrow/Settlement Fees: The escrow or closing agent (often the title company in Texas) handles all the paperwork, funds, and ensures all conditions of the sale are met. This fee compensates them for managing the closing process.

- Recording Fees: These are fees paid to the county or local government to officially record the new deed and mortgage documents in the public records, formally establishing your ownership.

Property Taxes and Insurance

These are ongoing costs associated with property ownership, but some are paid upfront at closing.

- Prorated Property Taxes: At closing, you’ll typically reimburse the seller for any property taxes they have pre-paid for the current year, or you will pay taxes for the remaining portion of the year. Property taxes in Texas can be quite high compared to other states, making this an important consideration.

- Homeowner’s Insurance Premium: Lenders require you to have a homeowner’s insurance policy in place at closing. You’ll usually pay the first year’s premium upfront. Depending on your location, you might also need additional coverage like windstorm insurance for coastal areas like Galveston or flood insurance, especially if you’re looking at properties along the Gulf Coast or in specific flood plains.

- Escrow Setup/Pre-Paid Items: Lenders often require buyers to establish an escrow account for future property taxes and homeowner’s insurance premiums. At closing, you might need to deposit several months’ worth of these payments into this account to get it started.

Other Potential Costs

Depending on the specific transaction, other fees may arise.

- Survey Fee: While not always required, a survey may be necessary to confirm property lines and ensure there are no encroachments. In Texas, if there is an existing survey and the seller can provide an affidavit confirming no changes to the property, a new survey might not be needed. However, if no recent survey exists or if the lender or title company requires a new one, this can add $400 to $800 to your costs.

- Attorney Fees: While attorneys are not mandatory for real estate closings in Texas (the title company often handles the closing), buyers or sellers may choose to hire their own legal counsel. If you do, their fees will be part of your closing costs. This is more common in complex transactions, such as commercial properties or luxury estates.

- Home Inspection Fee: Although typically paid outside of closing, a home inspection is highly recommended to identify any structural or mechanical issues with the property. While not a closing cost, it’s a critical expense in the home-buying process, usually ranging from $300 to $600.

- HOA Fees: If you’re purchasing a property in a community with a Homeowners Association (HOA), you may be required to pay an initial HOA setup fee or several months of dues upfront at closing. This is common for condos, townhouses, and many planned communities that offer shared amenities similar to those found in resorts or hotels.

Navigating the Numbers: Average Closing Costs in the Lone Star State

The question “How much is the closing cost in Texas?” doesn’t have a single, fixed answer, much like the cost of a vacation can vary wildly based on your destination and chosen accommodations. However, we can provide a realistic range and insights into the factors that influence these numbers. On average, buyers in Texas can expect to pay between 2% and 5% of the loan amount in closing costs. This general estimate places Texas in a middle-to-lower range compared to some other states like New York or California, primarily because sellers traditionally cover the owner’s title insurance policy, which is a substantial expense.

For instance, on a $300,000 home with a loan amount of $240,000 (assuming a 20% down payment), closing costs could range from $4,800 to $12,000. It’s important to remember that this range is influenced by several variables:

- Loan Amount and Type: Larger loans naturally lead to higher fees when those fees are calculated as a percentage. Government-backed loans like FHA, VA, or USDA loans can sometimes have different fee structures or offer opportunities for seller concessions that impact the buyer’s out-of-pocket costs.

- Property Location: Real estate values and local fees can vary significantly from one Texan city to another. Closing costs might be slightly higher in competitive markets like Austin or Dallas compared to more rural areas, due to higher property values and potentially more complex transactions.

- Lender and Service Providers: Different lenders have varying origination and underwriting fees. Similarly, title companies and other service providers (like appraisers) have their own fee schedules. Shopping around can make a difference.

- Negotiations: The allocation of closing costs between buyer and seller is often a point of negotiation. While sellers typically pay for the owner’s title policy in Texas, other fees can be shifted depending on market conditions and the negotiating power of each party. For example, if you’re buying a vacation rental in a highly sought-after destination, you might have less leverage to ask for seller concessions.

It’s crucial to distinguish between what the buyer typically pays and what the seller usually covers. In Texas, the buyer generally pays:

- Loan origination and underwriting fees

- Appraisal and credit report fees

- Lender’s title insurance

- Survey fee (if a new one is required)

- Pre-paid property taxes and homeowner’s insurance

- Recording fees

- Escrow fees (often split with the seller)

The seller typically pays:

- Owner’s title insurance

- Real estate agent commissions (for both buyer and seller agents)

- Any existing mortgage payoff and related fees

- Prorated property taxes up to the closing date

An important document to familiarize yourself with is the Loan Estimate (LE), which your lender is required to provide within three business days of applying for a mortgage. This document provides a good-faith estimate of all your loan terms and closing costs. Shortly before closing, you’ll receive a Closing Disclosure (CD), which itemizes all actual charges and credits for both buyer and seller. Comparing the LE to the CD is critical to ensure there are no unexpected fees, allowing you to finalize your budgeting for your new accommodation in Texas.

Savvy Strategies: Reducing Your Closing Costs in Texas

Just as smart travelers seek out deals on flights and hotels to maximize their budget, proactive home buyers can employ several strategies to minimize their closing costs in Texas. Reducing these upfront expenses can significantly lighten the financial load, making your new home or investment property more accessible.

- Negotiate with the Seller for Credits: This is often the most impactful strategy. In a buyer’s market, or if the seller is motivated, you can ask the seller to pay for a portion of your closing costs. This is often referred to as “seller credits” or “seller concessions.” For example, you might negotiate for the seller to pay 2-3% of your closing costs, which can represent thousands of dollars in savings. The feasibility of this depends heavily on market conditions and the specifics of the property – a unique luxury villa might command less negotiation flexibility than a standard suburban home.

- Shop Around for Lenders and Service Providers: Just like you’d compare prices for different resorts or long-term apartment rentals, compare Loan Estimates from multiple lenders. While loan origination fees are typically fixed by the lender, other fees, such as appraisal or title services, might be open to negotiation or vary significantly between providers. You have the right to shop for some third-party services, such as title companies, survey companies, and home insurance providers. Even a few hundred dollars saved on each service can add up.

- Timing Your Closing Date: The day of the month you close can impact prorated property taxes and interest payments. Closing at the end of the month often means you’ll pay less prepaid interest at closing, as mortgage interest is paid in arrears (for the previous month). While this doesn’t reduce total costs over the life of the loan, it reduces the cash needed upfront.

- Ask for Lender Credits: In some cases, lenders might offer “lender credits” to help cover closing costs. However, these often come at the expense of a slightly higher interest rate over the life of the loan. You’ll need to weigh whether the upfront savings outweigh the increased long-term interest payments. This can be a good option if you are certain you will refinance or sell the property within a few years, or if upfront liquidity is a major concern.

- Utilize Loan Programs with Lower Fees: Certain loan types, such as VA loans for eligible veterans, have restrictions on what fees can be charged to the borrower, potentially reducing closing costs. FHA and USDA loans can also have different fee structures or allow for more seller concessions than conventional loans. Explore these options if you qualify.

- Review the Loan Estimate and Closing Disclosure Meticulously: Always compare your initial Loan Estimate (LE) to the final Closing Disclosure (CD). These documents detail all fees. Look for any discrepancies or unexpected charges. You have the right to ask for explanations for any fees you don’t understand. Identifying and questioning erroneous charges before closing can save you money and prevent unnecessary stress.

By being informed and proactive, you can significantly influence the final amount you pay in closing costs, making your journey into Texas homeownership or real estate investment a smoother and more financially manageable experience. Whether you’re settling down for a new life chapter or expanding your portfolio of luxury travel accommodations, understanding these financial nuances is key to a successful venture in the Lone Star State.

In conclusion, understanding “How Much Is The Closing Cost In Texas?” is an indispensable part of preparing for property ownership in this dynamic state. Just as discerning travelers plan every detail of their itineraries, from attractions to accommodation, future Texas homeowners and investors must factor in these crucial expenses. By deconstructing the various fees, understanding average costs, and implementing savvy reduction strategies, you can navigate the complexities of real estate transactions with confidence. This knowledge empowers you to budget accurately, negotiate effectively, and ultimately secure your piece of Texas, whether it’s a bustling city apartment, a serene Hill Country retreat, or a prime investment property, ensuring your entry into the Lone Star State is as seamless and rewarding as possible.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.