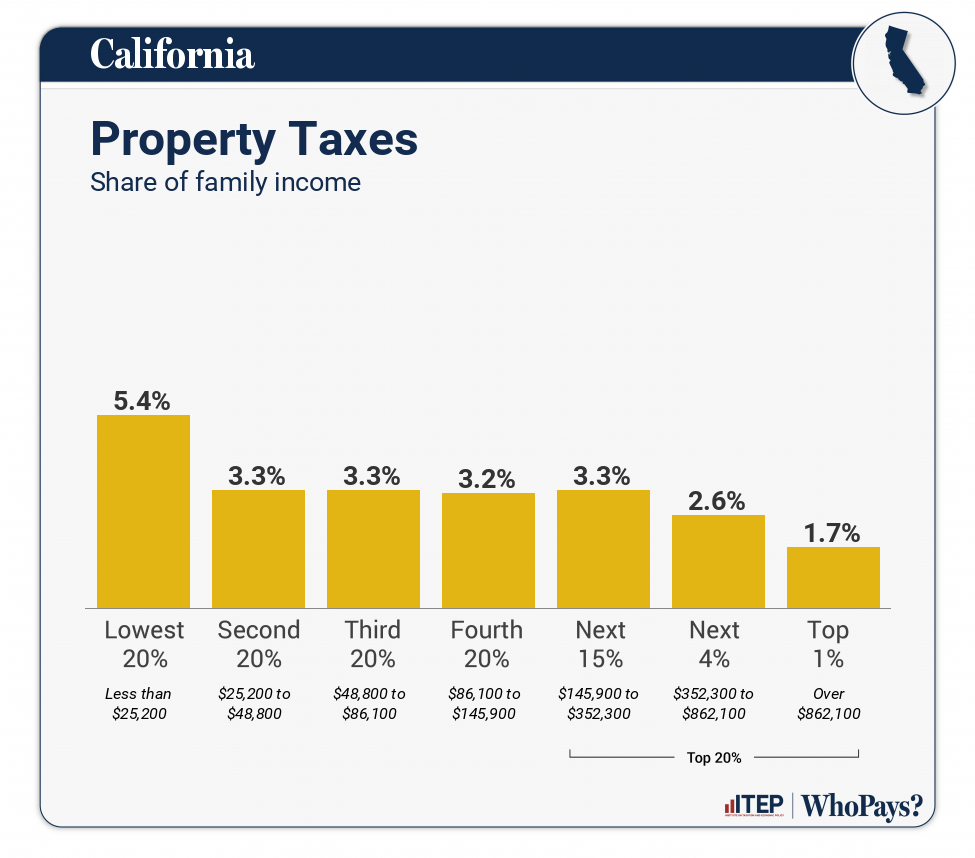

While the allure of California often conjures images of sun-drenched beaches, iconic theme parks, and the glitz of Hollywood, a significant aspect of property ownership in the Golden State that potential residents and investors need to understand is its property tax system. Far from being a simple, uniform fee, California property taxes are governed by a unique set of rules, primarily shaped by Proposition 13. This landmark legislation, passed in 1978, has profoundly impacted how property taxes are calculated and levied across the state, making it crucial to grasp the nuances before embarking on any property ventures, whether for a luxurious vacation home, a business investment, or a long-term rental property.

Understanding California‘s property tax landscape is essential for anyone considering purchasing real estate, from individual homeowners to large-scale developers. It influences not only the ongoing cost of ownership but also the financial feasibility of various lifestyle choices, including luxury travel destinations that might double as investment properties, or the budgeting for extended family trips that involve acquiring a temporary base. For those delving into the tourism sector, perhaps by investing in hotels or apartments for short-term rentals, a clear comprehension of these tax obligations is paramount. This article aims to demystify California property taxes, breaking down the core principles and explaining how they might affect your financial planning.

The Cornerstone: Proposition 13 and Its Impact

At the heart of California‘s property tax system lies Proposition 13. This initiative fundamentally altered how assessed values and tax rates are determined, creating a system that is notably different from many other states. Its primary tenets are twofold: the limitation of property tax rates and the restriction on annual assessment increases.

Assessed Value: The Base for Taxation

Under Proposition 13, the assessed value of a property is generally fixed at its market value as of March 1, 1975, or its sale price at the time of a subsequent purchase. This means that if you purchase a property today, its assessed value for tax purposes will be based on your purchase price. However, this initial assessed value is subject to strict limitations on how much it can increase each year.

Annual Assessment Limitations

One of the most significant aspects of Proposition 13 is its cap on annual increases to the assessed value. The assessed value of a property can only increase by a maximum of 2% per year, or by the rate of inflation, whichever is lower. This has a profound effect on long-term property owners, as their tax burden often remains significantly lower than that of newer buyers, even if the market value of their property has soared far beyond their assessed value. For instance, a property purchased in Beverly Hills in the 1980s might have an assessed value that is a fraction of its current market worth.

The Tax Rate: A Standardized Levy

Proposition 13 also standardized the property tax rate. The maximum property tax rate is set at 1% of the assessed value. This 1% rate is then applied to the property’s assessed value to calculate the annual property tax bill. However, this 1% is not a rigid ceiling for all taxes. It forms the base, and additional local taxes, often approved by voters for specific purposes like funding schools or local infrastructure, can be added on top of this base rate. These additional levies are known as “special assessments” and can vary significantly from one city to another.

Special Assessments and Bond Measures

While the 1% base rate is a constant, property owners in California may encounter additional charges. These often stem from voter-approved bond measures or special districts that provide specific services. For example, a city might have a special assessment to fund its local fire department or improve its park systems. These are levied based on benefits received or the parcel’s size and can increase the effective tax rate. Navigating these can be complex, and understanding the specific levies in a particular county or city is crucial. For those considering long-term stay accommodations or investing in resorts, these additional costs can accumulate.

How Property Taxes Are Calculated: A Practical Example

To illustrate how property taxes are calculated in California, let’s consider a hypothetical scenario.

Scenario: Purchasing a Home in Los Angeles

Imagine you purchase a property in Los Angeles for $1,000,000.

-

Initial Assessed Value: Your initial assessed value will be $1,000,000, reflecting your purchase price.

-

Annual Tax Calculation (Year 1): With the standard 1% property tax rate, your property tax for the first year would be:

$1,000,000 (Assessed Value) * 0.01 (Tax Rate) = $10,000 -

Annual Tax Calculation (Year 2): Assuming the assessed value increases by the maximum 2% allowed by Proposition 13, your new assessed value would be:

$1,000,000 * 1.02 = $1,020,000

Your property tax for the second year would be:

$1,020,000 (Assessed Value) * 0.01 (Tax Rate) = $10,200

This example highlights the impact of Proposition 13 on newer buyers. Their taxes are directly tied to market fluctuations at the time of purchase and are subject to modest annual increases.

The “Rollover” Effect for Long-Term Owners

Contrast this with a property purchased decades ago for a much lower price. Let’s say a similar property was purchased in Los Angeles in the 1980s for $100,000. If it has been owned continuously by the same family and has seen its assessed value increase by a modest 2% annually, its current assessed value could still be significantly lower than its current market value of $1,000,000.

For instance, after 40 years, a $100,000 assessed value with 2% annual increases would be roughly:

$100,000 * (1.02)^40 approx $220,804

The property tax on this long-held property would then be:

$220,804 (Assessed Value) * 0.01 (Tax Rate) = $2,208.04

This stark difference illustrates why California is often perceived as having a favorable property tax environment for long-term residents and owners, while newer buyers face higher immediate tax burdens. This can influence decisions related to budget travel within the state, as lower property tax bills for established residents can free up funds for other lifestyle expenses.

Factors Influencing Your Property Tax Bill

While Proposition 13 provides the foundational framework, several other factors can influence the final property tax bill you receive in California. Understanding these can help you anticipate and manage your expenses.

Property Location and Local Levies

The specific city or county where your property is located plays a crucial role. As mentioned, local voter-approved measures can add special assessments to the base 1% tax rate. These can range from small amounts to significant additions, depending on the services funded and the voters’ approval. For example, a city with excellent public schools and extensive park systems might have higher special assessments than a more rural area. This is particularly relevant for those considering family trips or investing in local culture and attractions, as the amenities often funded by these taxes contribute to the overall appeal of a destination.

Property Type and Usage

The type of property and its intended use can also have an indirect impact. While the tax calculation method generally remains the same, the purchase price of different property types—be it a suite in a downtown hotel, a sprawling resort in Palm Springs, or a modest apartment for long-term stay—will vary considerably, directly affecting the initial assessed value and subsequent tax payments. Investors in the accommodation sector, looking at reviews and comparison of properties, will need to factor in the tax implications for commercial versus residential properties, although Proposition 13‘s core principles apply to both.

Changes in Ownership and New Construction

Any change in ownership, such as a sale or transfer of property, triggers a reassessment of the property’s value to its current market value at the time of the transfer. This is often referred to as a “reassessment event.” Similarly, new construction on a property will be assessed at its market value, and this new value will then be subject to the annual 2% increase limit. This is a critical consideration for developers or those planning renovations, as it can lead to a significant jump in property taxes. For instance, adding a new wing to a villa or constructing a new landmark hotel would necessitate a reassessment.

Exemptions and Reductions

Certain exemptions and reductions are available that can lower your property tax bill. The most common is the homeowner’s exemption, which reduces the taxable value of a principal residence by $7,000. This means that if your property’s assessed value is $500,000, the homeowner’s exemption would effectively reduce your taxable value to $493,000. Other exemptions may be available for disabled veterans or seniors, though these often have specific eligibility requirements. Investigating these potential reductions is a wise step for any property owner in California.

Proposition 19 and Its Nuances

It’s important to note that Proposition 13 has seen some modifications and clarifications over the years. Proposition 19, passed in November 2020, introduced significant changes, particularly concerning property tax portability for seniors, individuals with severe disabilities, and victims of wildfires. It allows eligible individuals to transfer their existing assessed property values to a new home of equal or lesser value, anywhere in California, or even to a more expensive home with an adjustment to the new tax assessment. This change aims to provide more flexibility for these specific groups, allowing them to relocate without facing a drastic property tax increase. The nuances of Proposition 19 can be complex, and it’s advisable to consult with the county assessor’s office for detailed information on eligibility and application procedures, especially if you are considering downsizing or relocating for lifestyle reasons.

In conclusion, while the prospect of owning property in California is exciting, a thorough understanding of its property tax system, primarily governed by Proposition 13, is indispensable. From the initial assessment based on purchase price to the limitations on annual increases and the potential for local special assessments, each element plays a role in the final tax burden. By familiarizing yourself with these factors, you can make informed decisions, whether you’re planning a dream vacation home, investing in accommodation, or simply seeking to understand the financial landscape of this vibrant state.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.