The question of whether residents of Puerto Rico pay U.S. federal income taxes is a complex one, often shrouded in misunderstanding and fueled by the island’s unique political status. As a territory of the United States, Puerto Rico holds a distinct position within the American sphere, leading to a tax system that differs significantly from that of mainland states. This article aims to demystify these tax obligations, exploring who pays, who doesn’t, and the underlying reasons for these distinctions, while also touching upon how this impacts travel and lifestyle on this vibrant Caribbean island.

Understanding the tax landscape in Puerto Rico is crucial for anyone considering visiting, investing in, or relocating to the island. For travelers, it can influence perceptions of cost and affordability. For those contemplating a longer stay, or even a permanent move, it’s a fundamental aspect of financial planning. We’ll delve into the nuances of U.S. federal income tax, Puerto Rico income tax, and other tax considerations, providing clarity for residents and visitors alike.

The Tax Puzzle: Federal vs. Territorial Obligations

The core of the tax question lies in the distinction between U.S. federal income tax and Puerto Rico income tax. While Puerto Rico is indeed a territory of the United States, its residents are not subject to the same federal income tax laws as citizens living in the fifty states. This is a key differentiator that often causes confusion.

Who Pays U.S. Federal Income Tax in Puerto Rico?

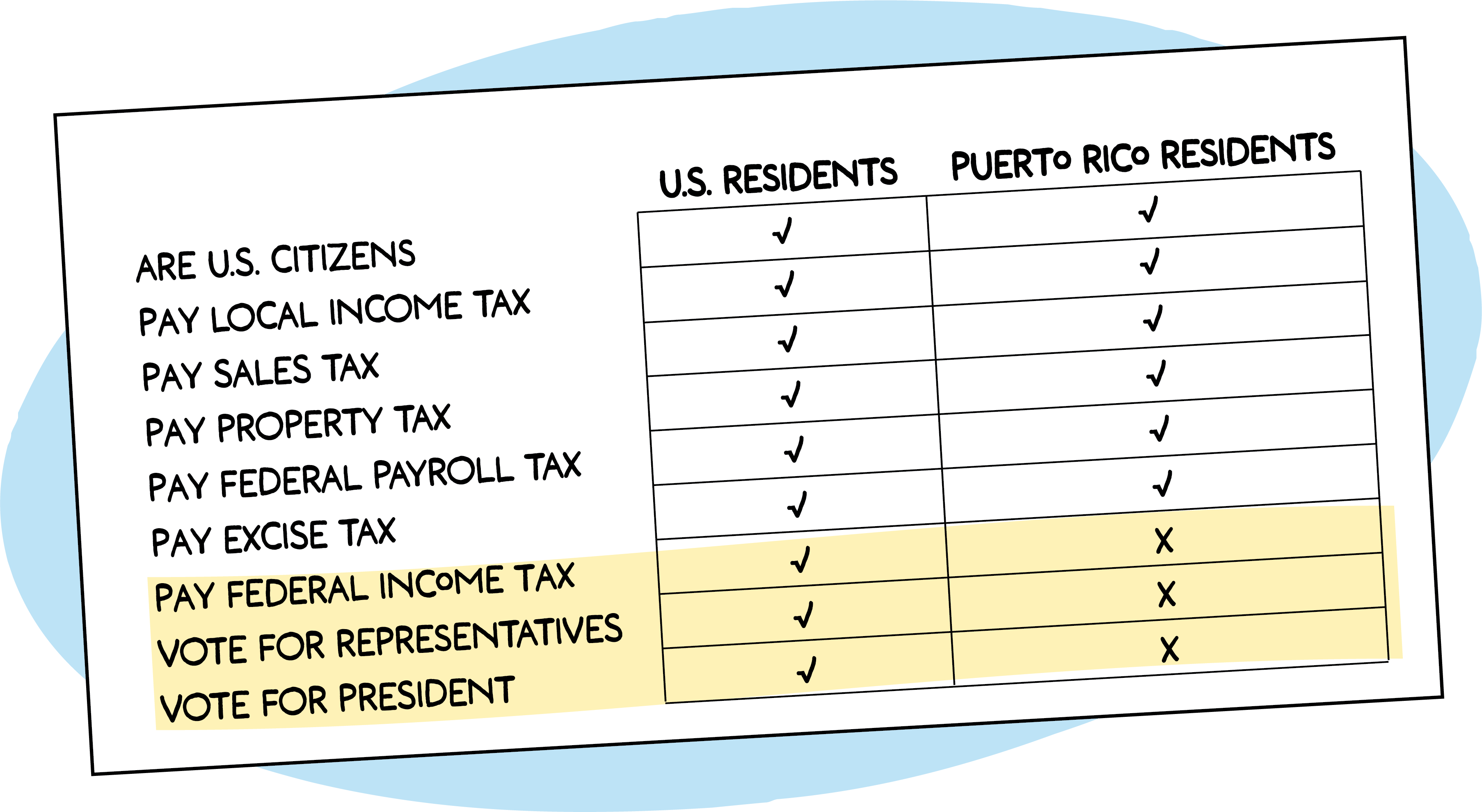

Generally, most residents of Puerto Rico do not pay U.S. federal income taxes on income earned within Puerto Rico. This exemption stems from Section 933 of the Internal Revenue Code, which states that income derived from sources within Puerto Rico by individuals who are bona fide residents of Puerto Rico is excluded from their gross income for federal tax purposes.

However, there are important exceptions and nuances to this rule:

- Non-Resident U.S. Citizens: U.S. citizens who reside in Puerto Rico but are not considered bona fide residents (for example, those who maintain domicile in a state and only reside in Puerto Rico temporarily) may still be subject to U.S. federal income tax on their worldwide income.

- Income from U.S. Sources: If a Puerto Rico resident earns income from sources outside of Puerto Rico – for instance, from investments in mainland U.S. stocks or from business activities conducted on the mainland – that income may be subject to U.S. federal income tax.

- Federal Payroll Taxes: While U.S. federal income taxes are often waived, Puerto Rico residents are generally subject to federal payroll taxes, such as Social Security and Medicare taxes. Employers and employees both contribute to these programs, just as they would in any U.S. state.

- Other Federal Taxes: Certain other federal taxes may still apply, depending on the specific circumstances. For example, if an individual has significant business dealings or investments that cross territorial lines, or if they are subject to specific federal excise taxes, these would still be levied.

The concept of “bona fide residency” is crucial. To be considered a bona fide resident of Puerto Rico for tax purposes, an individual must meet certain criteria, generally including establishing a permanent home on the island and not having a closer connection to any other place. The Internal Revenue Service (IRS) has specific guidelines for determining bona fide residency, which can involve factors like the duration of stay, intent to remain, and economic ties.

The Puerto Rico Income Tax System

In lieu of paying U.S. federal income taxes on their local income, residents of Puerto Rico are subject to the Puerto Rico income tax system. This system is administered by the Puerto Rico Department of Treasury (Departamento de Hacienda). The tax rates and rules are distinct from those of the U.S. mainland and can vary over time.

- Local Tax Rates: Puerto Rico has its own income tax brackets and rates, which apply to income earned by its residents. These rates have historically been progressive, meaning higher earners pay a larger percentage of their income in taxes.

- Tax Incentives: Puerto Rico has actively used tax incentives to attract businesses and investment. Notably, Act 20 (now superseded by Act 60) offered significant tax reductions for companies engaged in export services, while Act 22 (also now part of Act 60) provided substantial tax exemptions for new residents who invest in Puerto Rico. These acts have been instrumental in shaping the island’s economic landscape and attracting a segment of the lifestyle and business travel crowd.

- Filing Requirements: Residents of Puerto Rico must file annual income tax returns with the Puerto Rico Department of Treasury, reporting their income and calculating their tax liability according to local laws.

For individuals who relocate to Puerto Rico and qualify for tax incentives, the tax implications can be very favorable. For example, under Act 60 (which consolidated Act 20 and Act 22), qualifying businesses can benefit from a flat corporate tax rate of 4% on eligible income, and qualifying new residents can enjoy a 0% tax rate on passive income like interest, dividends, and capital gains for a period of 15 years, provided they meet certain investment and residency requirements. This has led to an influx of entrepreneurs, digital nomads, and individuals seeking a more tax-advantageous lifestyle, impacting the luxury travel and lifestyle segments of tourism.

Tax Implications for Travelers and Tourists

For the vast majority of tourists visiting Puerto Rico, the tax question is a non-issue. Visitors typically do not pay U.S. federal income taxes or Puerto Rico income taxes on their travel expenses or on any income they might incidentally earn while on vacation. The tax regulations are primarily concerned with the residency status of individuals.

However, there are a few indirect ways taxes can influence a tourist’s experience:

- Hotel Occupancy Taxes: Hotels and other accommodations in Puerto Rico typically levy an occupancy tax, which is a form of local tax added to the room rate. This tax goes towards funding various tourism initiatives and local services. The rates can vary, so it’s always advisable to check the total cost when booking.

- Sales Tax (IVU): Puerto Rico has a sales and use tax (Impuesto sobre Ventas y Uso, or IVU) that applies to most goods and services, similar to sales tax in U.S. states. The standard rate is 11.5%, with a 7% rate for groceries and medications. This tax is factored into the price of many purchases, from souvenirs to dining experiences.

- Impact on Local Economy: The tax structure, including the incentives aimed at attracting businesses and investment, has a broader impact on the Puerto Rico economy. This can influence the availability and cost of services, the development of attractions, and the overall cost of living and travel on the island. For instance, the growth in luxury resorts and high-end dining establishments can be partly attributed to tax incentives that have encouraged investment.

When planning a trip, understanding these local taxes is part of budgeting. While you won’t be filing income tax returns, these embedded taxes are part of the overall cost of experiencing Puerto Rico. The allure of destinations like Old San Juan with its historic architecture, the natural beauty of the El Yunque National Forest, and the vibrant culture of cities like Ponce are all supported, in part, by these tax revenues.

Long-Term Stays and Relocation: Navigating the Tax Landscape

For individuals considering a longer stay, be it for extended vacation, remote work, or permanent relocation, understanding the tax implications becomes paramount. This is where the distinction between being a tourist and becoming a resident truly matters.

Establishing Bona Fide Residency

As previously mentioned, the key to benefiting from the U.S. federal income tax exemption on Puerto Rico-sourced income is establishing bona fide residency. The IRS provides guidelines, but generally, it involves demonstrating a clear intent to reside permanently on the island. This can include:

- Physical Presence: Spending a significant amount of time in Puerto Rico.

- Home Ownership or Rental: Establishing a primary residence on the island.

- Economic Ties: Shifting your economic activities and financial interests to Puerto Rico.

- Driver’s License and Voter Registration: Obtaining a Puerto Rico driver’s license and registering to vote locally can be strong indicators.

- Severing Ties with the Mainland: Demonstrating a clear break from your previous state of residence, such as selling property, closing bank accounts, or terminating leases.

The Appeal of Tax Incentives for New Residents

The tax incentives offered under Act 60 have been a major draw for individuals seeking to relocate and reduce their tax burden. These incentives, particularly the 0% tax on passive income for new residents and the attractive corporate tax rates for businesses, have fueled a boom in certain sectors. This has led to a diversification of the tourism market, with more emphasis on luxury accommodations, high-end experiences, and lifestyle-oriented travel.

Travelers interested in these incentives might find themselves exploring areas with new developments, upscale resorts like the Dorado Beach, a Ritz-Carlton Reserve, and boutique hotels catering to a discerning clientele. The emphasis shifts from purely sightseeing to experiencing a particular lifestyle.

Tax Obligations for Businesses and Investors

For businesses operating in Puerto Rico, understanding the tax regime is crucial. While the U.S. federal income tax on locally sourced income is generally exempt for bona fide residents, businesses are subject to Puerto Rico income tax. However, the competitive corporate tax rates and incentives under Act 60 make Puerto Rico an attractive location for businesses, particularly those involved in export services, manufacturing, and technology.

Investors also need to be aware of the tax implications. While new residents might benefit from a 0% tax on passive income, understanding the specifics of capital gains, dividends, and interest income is essential for tax planning. Consulting with tax professionals who specialize in Puerto Rico tax law is highly recommended for anyone considering relocation or significant investment.

In conclusion, the question of whether Puerto Rico residents pay U.S. federal income taxes is answered with a qualified “no” for most bona fide residents on their Puerto Rico-sourced income. However, the island has its own robust tax system, and federal payroll taxes still apply. For tourists, the primary tax considerations are local occupancy taxes and sales tax. For those contemplating a longer-term commitment, understanding the intricacies of residency and the island’s unique tax incentive programs is vital for financial planning and maximizing the benefits of living in this dynamic U.S. territory. From the bustling streets of San Juan to the serene beaches of Vieques, Puerto Rico offers a rich tapestry of experiences, and a clear understanding of its tax landscape is an essential part of appreciating all it has to offer.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.