Florida, the Sunshine State, is a magnet for travelers, dreamers, and those seeking a vibrant lifestyle. From the enchanting theme parks of Orlando to the sun-kissed beaches of Miami, the historic charm of St. Augustine, and the serene beauty of the Florida Keys, this state offers an unparalleled array of destinations and attractions. For many, experiencing Florida to its fullest means having the freedom of the open road – a car to explore hidden gems, drive along scenic coastal routes, or simply commute between your chosen accommodations, be it a luxurious resort, a cozy villa, or a budget-friendly apartment.

Whether you’re planning a short-term family trip to Walt Disney World Resort, a long-term snowbird escape to Sarasota, or contemplating a permanent move to cities like Tampa or Jacksonville, the question of car insurance inevitably arises. It’s not just a technicality; it’s a crucial aspect of responsible travel and an essential component of navigating the state’s unique legal landscape. Understanding Florida’s car insurance requirements isn’t just about avoiding legal woes; it’s about protecting yourself, your loved ones, and your travel investments, ensuring peace of mind as you embark on your Florida adventures. This comprehensive guide aims to demystify the intricacies of car insurance in Florida, providing clarity for every type of traveler and resident, ensuring your journey through this captivating state is as smooth and carefree as possible.

Navigating Florida’s Roads: Why Car Insurance Isn’t Just a Suggestion

The allure of Florida’s diverse landscapes and vibrant culture often means hitting the road is a necessity. From exploring the thrilling rides at Universal Orlando Resort to discovering the natural wonders of Everglades National Park, a vehicle offers unparalleled flexibility. However, this freedom comes with responsibility, and in Florida, that responsibility is legally enshrined in its car insurance laws. Unlike some other states, car insurance here isn’t merely recommended; it’s a mandatory requirement, deeply integrated into the state’s no-fault system. Understanding these foundational requirements is the first step towards ensuring your compliance and safeguarding your travel experiences or long-term stay.

The Legal Mandate: Florida’s No-Fault System

Florida operates under a “no-fault” car insurance system, a framework designed to streamline the process of medical payments and prevent lengthy legal battles after minor accidents. This system mandates that regardless of who is at fault for an accident, each driver’s own insurance company pays for their medical expenses and lost wages up to a certain limit. This doesn’t mean fault is irrelevant for all aspects of an accident, but it significantly changes how initial medical costs are handled.

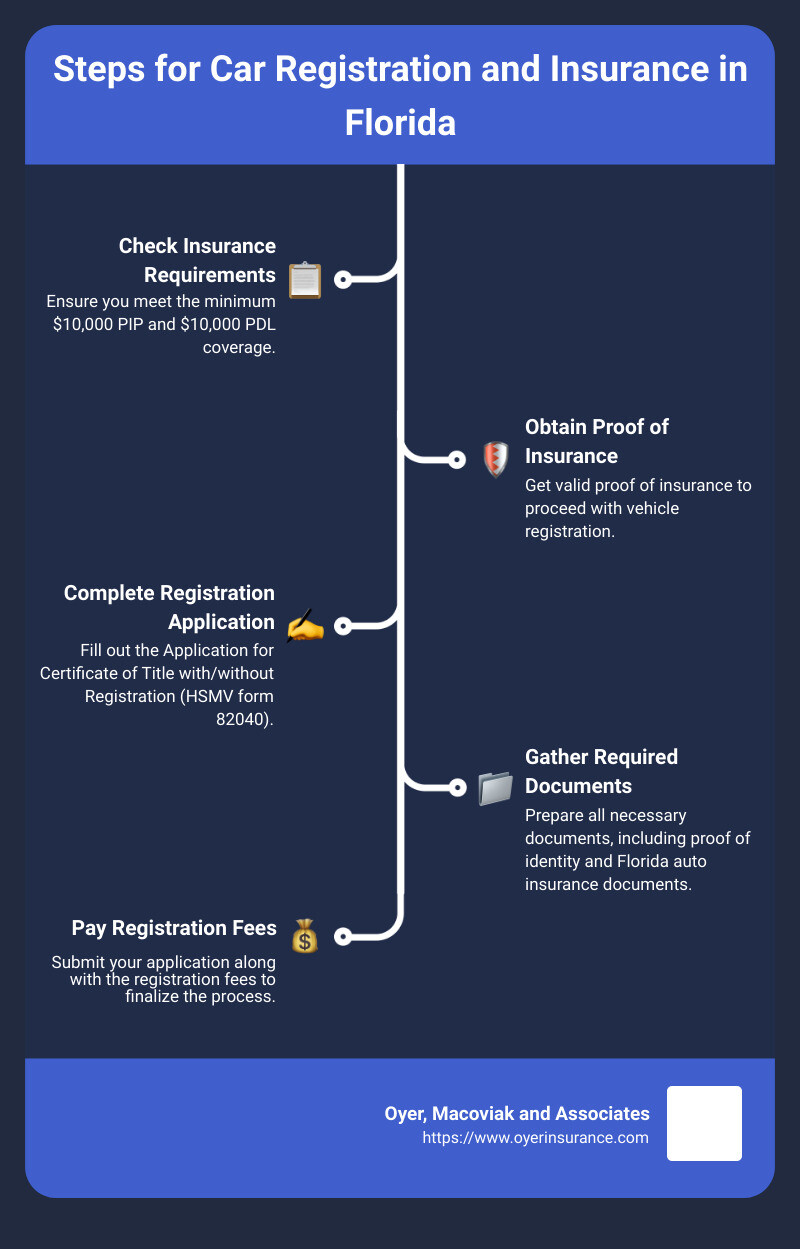

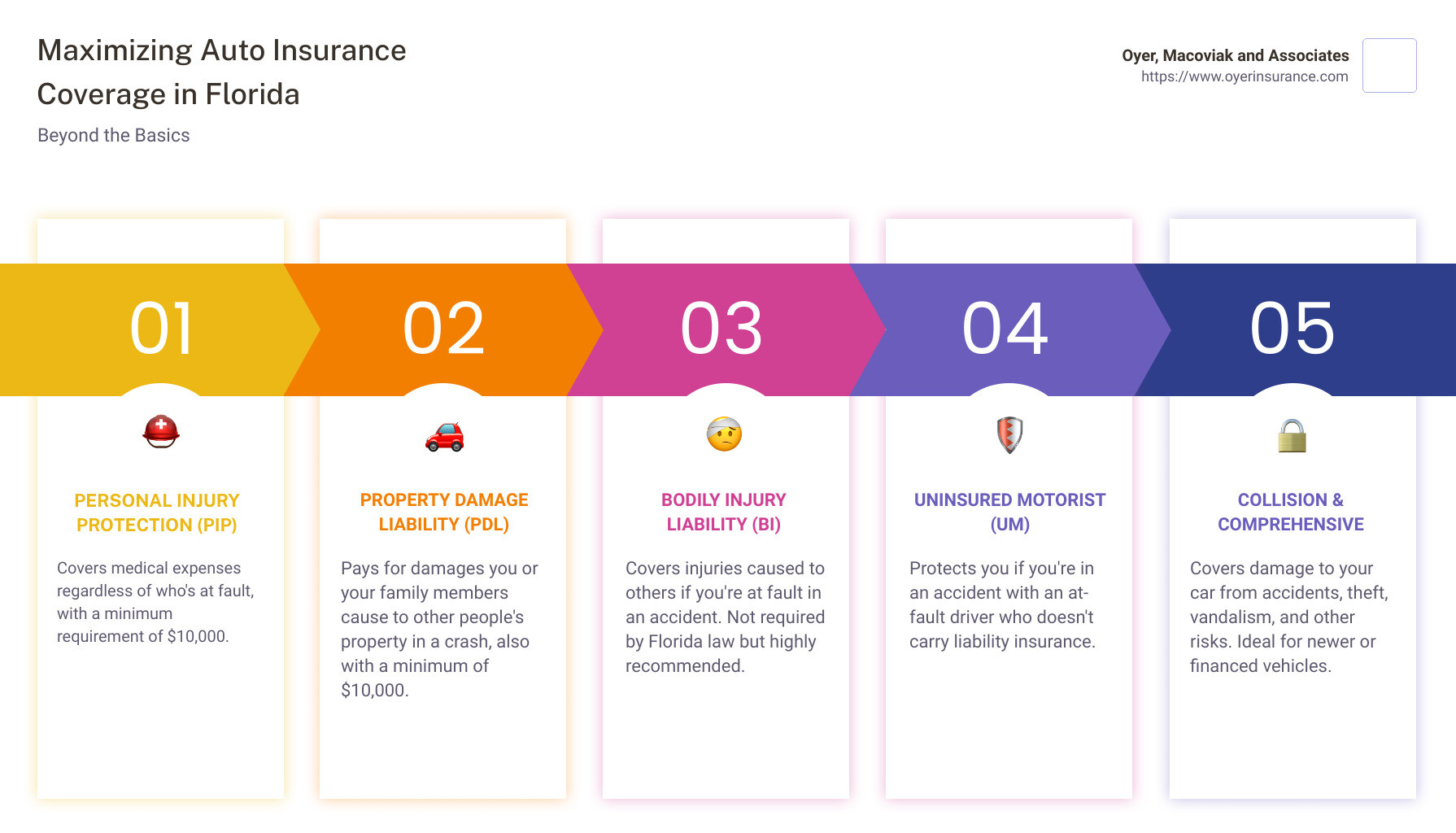

The cornerstone of Florida’s no-fault system is the Personal Injury Protection (PIP) coverage. This is a crucial component of your policy that every registered vehicle in Florida must carry.

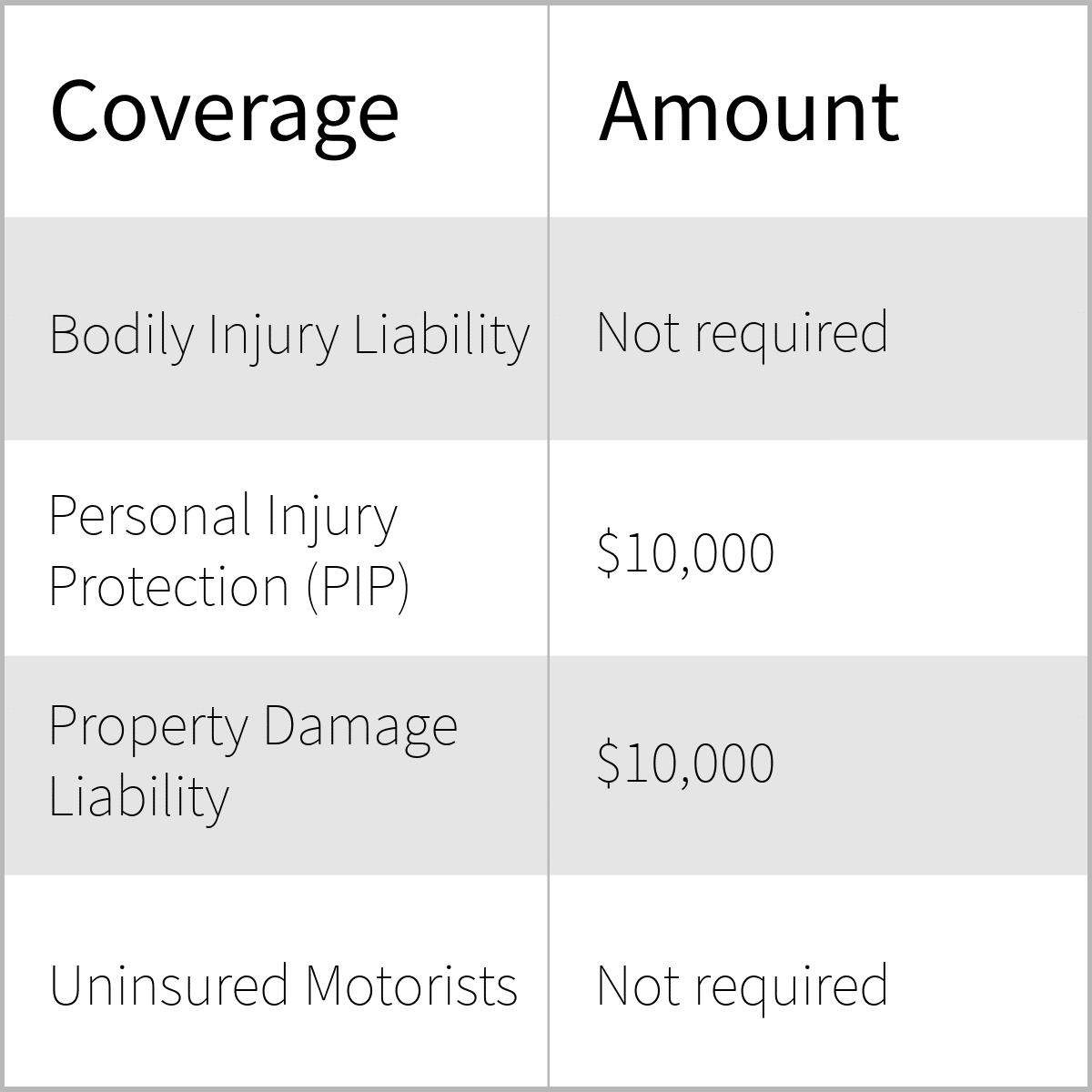

- Personal Injury Protection (PIP): Florida law requires all registered vehicle owners to carry a minimum of $10,000 in PIP coverage. This coverage is designed to pay 80% of your medical expenses, 60% of lost wages, and 100% of replacement services (like hiring someone to perform tasks you normally would) up to your policy limit, regardless of who caused the accident. This protection extends not only to you as the policyholder but also to relatives living in your household, certain passengers, and even pedestrians or cyclists if they are hit by your insured vehicle. For travelers, this means that even if you’re just visiting and involved in an accident, your PIP coverage (or that of the vehicle you’re in) will be the primary payer for initial medical costs.

- Property Damage Liability (PDL): In addition to PIP, Florida law also mandates a minimum of $10,000 in Property Damage Liability (PDL) coverage. This coverage pays for damage you cause to another person’s property, such as their vehicle, fences, or other structures, in an accident where you are at fault. While it doesn’t cover your own vehicle’s damage, it’s vital for protecting you from the financial burden of repairing someone else’s property.

These two components, PIP and PDL, form the absolute minimum legal requirement for any vehicle registered and operated in Florida. Failing to meet these requirements can lead to severe penalties, including fines, suspension of your driver’s license and vehicle registration, and even impoundment of your vehicle. For anyone considering an extended stay, purchasing a vehicle, or simply renting one, understanding and securing these basic coverages is non-negotiable.

Beyond the Basics: Recommended Coverage for Peace of Mind

While PIP and PDL are the legal minimums, relying solely on them can leave you dangerously exposed to significant financial risks, especially in a state with high traffic volumes and frequent tourist activity. For a truly worry-free travel or living experience in Florida, considering additional types of coverage is highly advisable. These supplementary coverages are designed to protect you from more substantial financial liabilities and losses that can arise from accidents or other unforeseen events.

- Bodily Injury Liability (BIL): This is perhaps the most critical additional coverage to consider. While PIP covers your medical expenses, BIL pays for medical expenses, lost wages, and pain and suffering of others if you are at fault for an accident. Florida does not legally require BIL, which might seem counterintuitive. However, without it, you are personally responsible for these costs, which can quickly escalate into hundreds of thousands of dollars in severe accidents. Imagine a luxury travel experience turning into a financial nightmare – BIL is your shield.

- Uninsured/Underinsured Motorist (UM/UIM): Given that BIL is not mandatory, Florida unfortunately has a significant number of uninsured drivers. UM/UIM coverage protects you if you are hit by a driver who either has no insurance or insufficient insurance to cover your damages. This coverage steps in to pay for your medical bills and lost wages when the at-fault driver cannot. It’s an invaluable layer of protection, particularly when exploring popular tourist destinations like Key West or the bustling streets of Fort Lauderdale.

- Collision Coverage: This pays for damages to your own vehicle resulting from a collision with another vehicle or object, regardless of who is at fault. If you’ve invested in a nice rental car for your trip or own a vehicle you value, collision coverage is essential. Without it, you’d be solely responsible for repair or replacement costs for your car after an accident.

- Comprehensive Coverage: Often paired with collision, comprehensive coverage protects your vehicle from non-collision-related incidents. This includes damage from theft, vandalism, fire, natural disasters (a crucial consideration in hurricane-prone Florida), falling objects, or even hitting an animal. For those enjoying the outdoor lifestyle or staying in different types of accommodation, from urban hotels to secluded villas, this offers protection against a wide array of potential misfortunes.

Investing in these additional coverages is a prudent decision for anyone planning to drive in Florida. They transform your car insurance from a mere legal compliance into a robust financial safety net, ensuring that your focus remains on enjoying the state’s beautiful destinations and enriching experiences rather than worrying about potential financial calamities.

Car Insurance for Every Florida Adventure

Florida’s appeal is vast and varied, attracting a diverse demographic from short-term tourists to long-term residents and business travelers. Each group navigates the state with unique needs, and understanding how car insurance applies to these different scenarios is key to a smooth and enjoyable experience. Whether you’re renting a car for a week-long vacation, spending several months as a snowbird, or relocating permanently, the approach to securing adequate insurance will differ significantly.

Tourists and Rental Cars: What You Need to Know

For the millions of tourists flocking to Florida’s attractions like Busch Gardens Tampa Bay, the Kennedy Space Center Visitor Complex, or the pristine sands of Clearwater Beach, renting a car is often the most convenient way to explore. The question of rental car insurance can be confusing, as various options are presented at the rental counter.

- Rental Car Company Insurance: When you pick up your rental car, you’ll likely be offered several types of coverage:

- Loss Damage Waiver (LDW) or Collision Damage Waiver (CDW): This waives your financial responsibility for damage to the rental car itself due to collision, theft, or vandalism. It’s essentially collision and comprehensive coverage for the rental.

- Liability Insurance: This provides additional bodily injury and property damage liability coverage beyond the state minimums (which the rental company typically provides with the car, as it’s legally required for them).

- Personal Accident Insurance (PAI): Similar to PIP, this covers medical expenses and accidental death for you and your passengers.

- Personal Effects Coverage (PEC): This covers your personal belongings if they are stolen from or damaged in the rental car.

- Personal Auto Policy Extension: Many personal car insurance policies (especially those from major national providers) extend coverage to rental cars, at least for collision and comprehensive. However, the extent of liability coverage extension can vary, and it might not fully cover all aspects, such as “loss of use” fees charged by rental companies. Always check with your own insurer before traveling.

- Credit Card Benefits: A significant number of premium credit cards offer secondary (or sometimes primary) collision damage waiver coverage for rental cars when you use that card to pay for the rental. This can be a great money-saver, but it’s crucial to understand the terms and limitations, including types of vehicles covered, rental duration, and whether it’s primary or secondary coverage (meaning it kicks in after your personal insurance).

For short-term visitors, especially those on family trips or budget travel, thoroughly reviewing these options and understanding what you already have (through personal policies or credit cards) can save you considerable expense and provide appropriate protection as you navigate from your hotel suite to the nearest attractions, or from a secluded villa to a popular local eatery. Don’t let the excitement of exploring Epcot or South Beach overshadow the importance of securing your ride.

Snowbirds and Long-Term Stays: Establishing Residency and Vehicle Registration

Florida welcomes countless “snowbirds” and other visitors who opt for extended stays, often for several months in destinations like Naples, Destin, or the vibrant communities around St. Petersburg. If your stay extends beyond 90 days, or if you establish certain ties to Florida (like getting a driver’s license or registering to vote), you might be considered a resident for vehicle registration and insurance purposes. This has significant implications:

- Florida Vehicle Registration: If you become a Florida resident, you are typically required to register your vehicle in the state within a certain timeframe (usually 10-30 days, depending on the specific circumstances). To register your vehicle, you must have Florida-compliant car insurance, meaning a policy from an insurance company licensed to do business in Florida that meets the state’s minimum PIP and PDL requirements.

- Transferring Out-of-State Policies: Your out-of-state policy, even if it meets Florida’s minimums, will likely not be sufficient once you establish residency and need to register your car in Florida. You’ll need to obtain a new policy from a Florida-licensed insurer. Many national carriers operate in Florida, so your current provider might be able to help you transition. This is an important consideration for accommodation planning, especially if you’re comparing long-term stay options or even purchasing a villa.

For those enjoying a long-term stay, whether it’s luxury travel or a budget-conscious extended vacation, understanding when you cross the residency threshold and the subsequent requirements for vehicle registration and insurance is paramount to avoid legal complications and ensure continuous coverage.

New Florida Residents: Your Guide to Local Compliance

Moving to Florida permanently, whether for career opportunities in Gainesville or to enjoy the serene coastal lifestyle of Amelia Island, involves several administrative steps, and car insurance is high on that list.

- Florida Driver’s License: If you become a resident, you’ll need to obtain a Florida driver’s license within 30 days of establishing residency.

- Vehicle Registration and Titling: As discussed for long-term stays, your out-of-state vehicle must be registered and titled in Florida. This requires proof of Florida-compliant insurance.

- Obtaining a Florida-Specific Policy: The most straightforward way to ensure compliance is to secure a car insurance policy from a company licensed to operate in Florida. It’s advisable to start shopping for quotes before you move, as rates can vary significantly based on your new Florida address, your driving history, and the type of vehicle you drive. Local culture often involves driving everywhere, so integrating quickly into the state’s regulatory framework for vehicles is a key tip for new arrivals.

For new residents, integrating into the local transport ecosystem means understanding these requirements upfront. This ensures not only legal compliance but also consistent protection as you settle into your new lifestyle, explore new landmarks like the Dali Museum in St. Petersburg, or visit family-friendly attractions like LEGOLAND Florida Resort.

The Financial and Legal Repercussions of Driving Uninsured

The temptation to forego car insurance might seem like a way to save money, particularly for budget travelers or those trying to minimize expenses during a long-term stay. However, the short-term savings are profoundly outweighed by the severe financial and legal repercussions that come with driving uninsured in Florida. These consequences can swiftly turn a dream vacation or a new life chapter into a nightmare, impacting your travel plans, financial stability, and even your freedom.

- Penalties for Non-Compliance: Florida takes its mandatory insurance laws seriously. If you’re caught driving without the minimum PIP and PDL coverage, the penalties are immediate and significant. Your driver’s license and vehicle registration will be suspended for a minimum of one year. To reinstate them, you’ll have to pay a hefty reinstatement fee (which increases for subsequent offenses) and provide proof of continuous Florida insurance for at least three years. If you’re involved in an accident while uninsured, the suspensions can be even longer, and you might also face additional fines. For a tourist, this could mean an abrupt end to your travel experience, leaving you stranded or facing exorbitant travel changes. For a new resident, it’s a rocky start to building a life in the state.

- The High Cost of Accidents Without Adequate Coverage: Beyond legal penalties, the financial fallout from an accident while uninsured can be catastrophic.

- Medical Bills: If you are injured, your PIP coverage is supposed to cover 80% of your medical bills up to $10,000. Without it, you are personally responsible for 100% of these costs. Even minor injuries can result in thousands of dollars in medical expenses, let alone serious ones requiring surgery or extended care.

- Property Damage: If you cause damage to another person’s vehicle or property, your PDL coverage is there to protect you. Without it, you would have to pay out of pocket for all repairs or replacement costs. A minor fender-bender could still cost thousands, and damage to a luxury car or extensive property can quickly run into tens of thousands of dollars.

- Lawsuits: If you are at fault for an accident and cause significant injuries to others, and you lack Bodily Injury Liability (BIL) coverage, you can be personally sued for those damages. This includes their medical expenses, lost wages, and pain and suffering. Judgments in such lawsuits can easily exceed hundreds of thousands or even millions of dollars. Without insurance, your personal assets – savings, property, future earnings – are all at risk. This could severely impact your ability to enjoy future travel, secure accommodation, or maintain your desired lifestyle.

- Your Own Vehicle Damage: If you don’t have Collision or Comprehensive coverage, any damage to your own vehicle, whether from an accident, theft, or natural disaster, will be entirely your financial responsibility. Repairing or replacing a vehicle can be a major unexpected expense, capable of derailing any carefully planned budget travel or long-term stay.

Driving uninsured in Florida is a gamble with incredibly high stakes. It’s a risk that far outweighs any perceived savings. For anyone visiting, living, or working in Florida, securing appropriate car insurance isn’t just a legal obligation; it’s a fundamental aspect of financial prudence and personal responsibility, ensuring that your time in the Sunshine State remains joyous and unburdened by preventable financial crises.

Smart Choices for Your Florida Journey: Securing the Right Coverage

Navigating the vibrant landscapes of Florida, from the historical streets of Key West to the sprawling attractions of Orlando, is an experience best enjoyed with complete peace of mind. Securing the right car insurance is a crucial step in achieving this, allowing you to focus on the destinations, experiences, and lifestyle Florida offers rather than lingering worries about potential mishaps. Making smart choices when it comes to your policy involves understanding your needs, comparing options, and staying informed.

- Finding Reputable Insurers: When seeking car insurance in Florida, whether for a rental, a newly purchased vehicle, or a registered resident’s car, it’s essential to choose a reputable insurer licensed to operate in the state. Many national carriers have a strong presence in Florida, alongside numerous regional and local companies. Look for insurers with positive customer reviews, strong financial ratings, and a track record of reliable claims service. Websites that offer comparison quotes can be a useful tool, but always follow up with direct inquiries to fully understand policy details and customer service offerings. For those considering long-term stays or permanent relocation, developing a relationship with a local insurance agent can also provide invaluable personalized advice tailored to Florida’s unique conditions and your specific needs, whether it’s for luxury travel or budget-conscious living.

- Factors Influencing Premiums in Florida: Car insurance premiums in Florida can vary widely due to several factors, reflecting the state’s diverse geography, population density, and unique environmental risks. Understanding these factors can help you make informed decisions:

- Location: Where you live or regularly drive in Florida significantly impacts your rates. Densely populated areas with higher traffic volumes and greater risk of theft, such as Miami or parts of Fort Lauderdale, often have higher premiums than more rural areas or calmer coastal towns like Sanibel Island. Even within cities like Tampa or Jacksonville, specific zip codes can influence rates.

- Driving Record: Your driving history is paramount. A clean record with no accidents or moving violations will generally secure lower rates. Conversely, a history of tickets or at-fault accidents will lead to higher premiums.

- Vehicle Type: The make, model, year, and safety features of your vehicle all play a role. More expensive cars, sports cars, and those with higher theft rates often cost more to insure. Vehicles with advanced safety features may qualify for discounts.

- Coverage Levels and Deductibles: Choosing higher liability limits and additional coverages like Uninsured/Underinsured Motorist, Collision, and Comprehensive will increase your premium. However, higher deductibles (the amount you pay out-of-pocket before your insurance kicks in) can lower your premium. It’s a balance between monthly cost and potential out-of-pocket expenses in an accident.

- Demographics: Factors like age, gender, and marital status can also influence rates, though their impact is often less significant than location or driving history.

- Credit Score: In Florida, insurers are allowed to use a credit-based insurance score as one factor in determining premiums. A higher score often indicates lower risk and can lead to better rates.

- Comparing Quotes and Understanding Policy Details: Don’t settle for the first quote you receive. Obtain quotes from multiple insurers to compare coverage options, limits, deductibles, and prices. Online comparison tools are a good starting point, but always verify details directly with an agent or the insurer’s website. Pay close attention to the fine print of each policy. Understand what is covered, what is excluded, and the specific conditions under which your coverage applies. Ask about available discounts, such as multi-policy discounts (if you bundle home or renters insurance), safe driver discounts, good student discounts, or discounts for certain vehicle safety features.

Securing the right car insurance isn’t just about ticking a box; it’s about protecting your travel investment and ensuring your Florida lifestyle is as enjoyable and stress-free as possible. Whether you’re commuting to a business stay in West Palm Beach, taking the family to Magic Kingdom, enjoying the local culture and food scene in Gainesville, or simply cruising along Siesta Key Beach, comprehensive and compliant car insurance is your ticket to a truly unforgettable experience. It enhances your freedom to explore famous places, discover hidden attractions, and fully immerse yourself in all the activities Florida has to offer, without the looming worry of unforeseen financial liabilities.

In conclusion, the question “Do you need car insurance in Florida?” has a resounding answer: Yes, unequivocally. Whether you are a fleeting tourist exploring the vibrant attractions, a snowbird enjoying an extended stay, or a new resident establishing roots, understanding and adhering to Florida’s car insurance laws is not merely a legal obligation but a cornerstone of responsible travel and living. From the mandatory PIP and PDL to the highly recommended liability and comprehensive coverages, each layer of protection contributes to a safer, more secure experience in the Sunshine State. By making informed choices, securing adequate coverage, and staying compliant, you ensure that your journey through Florida remains filled with delightful experiences and cherished memories, free from the unexpected burdens that can arise from being uninsured. Drive safely, stay insured, and let the adventures begin!

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.