Navigating the intricacies of estate planning and wealth transfer can feel like charting an unfamiliar territory, especially when you’re considering the financial implications for beneficiaries. For many, a crucial question arises: “Does Arizona have an inheritance tax?” This query is particularly relevant for those with ties to the Grand Canyon State, whether they are residents, own property there, or anticipate receiving assets from an estate situated in Arizona. Understanding the state’s tax landscape is vital for proper planning and to avoid any unwelcome surprises for those who inherit.

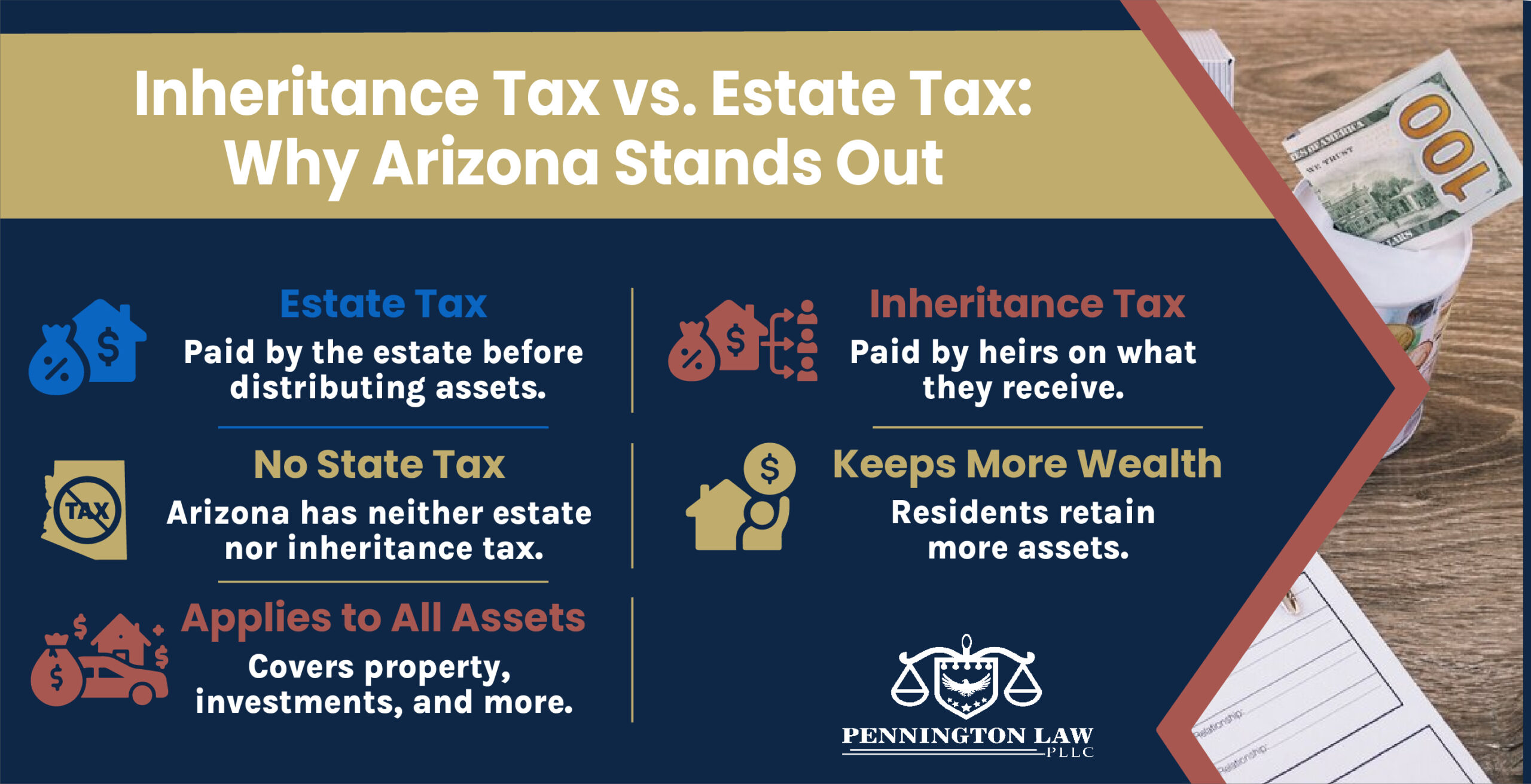

At its core, an inheritance tax is a tax levied on the recipient of an inherited asset, meaning the beneficiaries are the ones responsible for paying the tax. This is distinct from an estate tax, which is a tax on the deceased person’s estate itself, typically paid before assets are distributed to heirs. Many states in the United States have abolished inheritance taxes, but a few still maintain them. This has led to considerable confusion and the need for clarity, especially for individuals whose life experiences span multiple states or who have investments and properties across different jurisdictions.

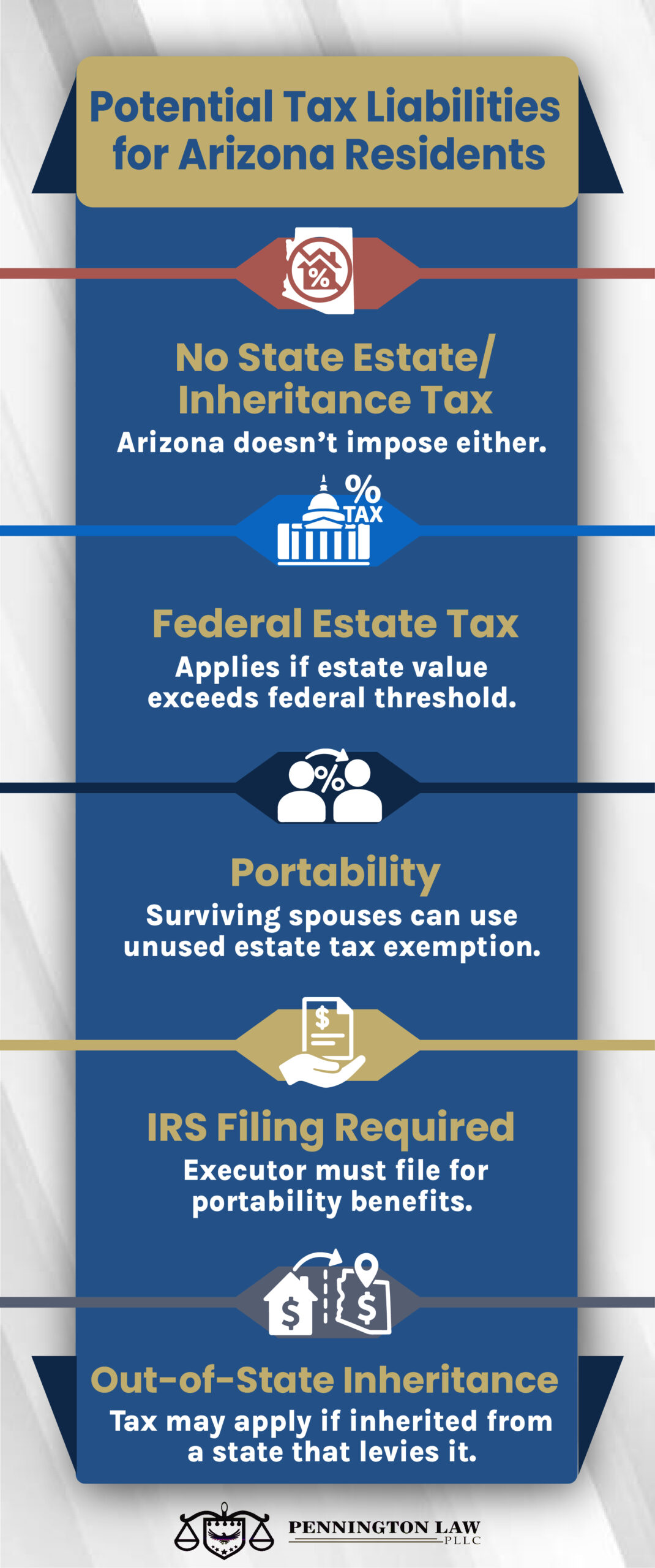

The good news for those with connections to Arizona is that the state does not currently impose an inheritance tax. This means that when someone passes away and their assets are distributed to their heirs in Arizona, those heirs will not be required to pay a tax to the state based on the value of the inheritance they receive. This is a significant factor that can simplify estate planning for residents and those who plan to leave assets within the state.

However, it’s crucial to understand that the absence of an inheritance tax in Arizona does not mean there are no tax implications whatsoever concerning inherited wealth. There are other federal and state considerations that can come into play, and it’s wise to be aware of them. These can include federal estate taxes, capital gains taxes on appreciated assets, and property taxes.

Understanding the Absence of an Inheritance Tax in Arizona

Arizona’s stance on inheritance taxes is a clear one: it does not have one. This policy has been in place for some time, making it a predictable aspect of estate planning for individuals living in or with assets in the state. The primary beneficiaries of this policy are the heirs and beneficiaries who will receive assets from an estate. They can inherit without the additional burden of a state-specific tax levied on the value of the assets they receive.

This absence of an inheritance tax can be particularly attractive for individuals planning their estates, especially when compared to states that do have such taxes. For instance, if someone lives in a state with a high inheritance tax and owns property in Arizona, they might consider structuring their assets or domicile in a way that leverages Arizona’s tax-friendly environment for their beneficiaries. This strategic planning can potentially save heirs a considerable amount of money.

Why No Inheritance Tax?

The decision by a state to implement or forgo an inheritance tax is often a reflection of its broader fiscal policies, economic development goals, and political landscape. States that do not have an inheritance tax often aim to attract wealth, encourage investment, and provide a more favorable environment for businesses and residents. They might rely on other forms of taxation, such as income tax, sales tax, or property tax, to fund state services.

Arizona has historically adopted a pro-business and pro-growth economic strategy. The absence of an inheritance tax can be seen as another element contributing to this strategy, by making it more appealing for individuals to retire, invest, and pass on their wealth within the state. It simplifies the process of wealth transfer and reduces potential friction for those who are already navigating the emotional and logistical challenges of estate settlement.

The absence of an inheritance tax doesn’t mean that the estate is entirely free from any tax considerations. Federal laws and other state laws can still apply. It’s important to distinguish between inheritance tax and estate tax. While Arizona does not have an inheritance tax, the federal government does have an estate tax, though it applies only to very large estates.

Federal Estate Tax and Other Considerations

While Arizona spares beneficiaries from paying an inheritance tax, it’s essential to be aware of federal estate taxes and other potential financial implications that can arise when inheriting assets. These are not specific to Arizona but are part of the broader tax framework in the United States.

Federal Estate Tax

The Internal Revenue Service (IRS) imposes a federal estate tax on the transfer of a deceased person’s estate. However, this tax has a very high exemption amount. For 2023, the federal estate tax exemption was $12.06 million per individual, and for 2024, it is $13.61 million per individual. This means that only very wealthy individuals whose estates exceed these substantial thresholds would be subject to federal estate taxes. For the vast majority of estates, federal estate taxes will not be a concern, regardless of whether they are located in Arizona or any other state.

If an estate does exceed the federal exemption amount, the tax is levied on the value of the estate above that threshold. The estate tax is paid by the estate itself, not directly by the beneficiaries. So, even if federal estate tax is applicable, the beneficiaries would receive the assets after the tax has been paid by the executor or administrator of the estate.

Capital Gains Tax

Another important consideration for beneficiaries is capital gains tax. If an inherited asset, such as stocks, bonds, or real estate, has appreciated in value since it was purchased by the deceased, the beneficiaries may be subject to capital gains tax when they eventually sell that asset.

However, there is a significant benefit known as the “step-up in basis” rule. When a person inherits an asset, its cost basis is typically “stepped up” to its fair market value at the time of the decedent’s death. This means that if a beneficiary sells the asset shortly after inheriting it, they will likely owe capital gains tax only on any appreciation that occurs after they inherit it, rather than on the entire appreciation that occurred during the original owner’s lifetime. This rule can significantly reduce or even eliminate capital gains tax liability for beneficiaries who sell inherited assets relatively quickly.

For example, if a parent bought real estate in Scottsdale for $100,000 many years ago, and its fair market value at the time of their death is $500,000, the beneficiary’s cost basis becomes $500,000. If the beneficiary then sells the property for $510,000, they would only owe capital gains tax on the $10,000 profit. Without the step-up in basis, they would have owed capital gains tax on the $400,000 appreciation.

Property Taxes

While not an inheritance tax, property taxes are a recurring cost that beneficiaries who inherit real estate will need to manage. Property taxes are levied by local governments based on the assessed value of the property. The rates and assessment methods vary by county and municipality within Arizona. Therefore, anyone inheriting property in Arizona should budget for these ongoing tax obligations.

Estate Planning and Professional Advice

The absence of an inheritance tax in Arizona simplifies one aspect of estate planning, but it doesn’t eliminate the need for careful consideration and professional guidance. Estate planning is a multifaceted process that involves more than just tax implications. It includes ensuring your assets are distributed according to your wishes, minimizing potential probate complications, and providing for your loved ones.

Wills and Trusts

Having a properly drafted will is fundamental to any estate plan. A will clearly outlines who should inherit your assets, who will be responsible for managing your estate (the executor), and who will care for minor children, if applicable. Without a will, state laws of intestacy will determine how your assets are distributed, which may not align with your intentions.

For more complex estates or to avoid probate altogether, a trust can be a valuable tool. Assets placed in a trust can be distributed to beneficiaries according to the terms of the trust agreement, often more quickly and privately than through the probate process. Trusts can also offer additional benefits, such as asset protection and control over how and when beneficiaries receive their inheritance.

Working with Professionals

Given the complexities of estate law and tax regulations, it is highly advisable to consult with qualified professionals. An estate planning attorney can help you draft wills, trusts, and other legal documents tailored to your specific circumstances and goals. They can also advise on strategies to minimize estate taxes, both federal and any state-level considerations, even though Arizona does not have an inheritance tax.

Furthermore, a financial advisor or certified public accountant (CPA) can provide valuable insights into the financial aspects of your estate. They can help you understand the potential tax implications of your assets, plan for capital gains taxes on appreciated assets, and ensure that your beneficiaries are prepared for any financial responsibilities, such as property taxes.

What About Other States?

It is important to remember that if you own property or have assets in other states, the inheritance or estate tax laws of those states could still apply. For example, if you are an Arizona resident but own a vacation home in New York or California, your beneficiaries might be subject to estate or inheritance taxes in those states, depending on their specific laws. This highlights the importance of a comprehensive estate plan that considers all your holdings, regardless of your primary residence.

In conclusion, while Arizona does not impose an inheritance tax, making it a favorable state for beneficiaries, it is crucial to understand the broader financial and legal landscape of estate planning. Federal estate taxes, capital gains taxes, property taxes, and the laws of other states where assets may be held all play a role. Consulting with legal and financial professionals is the most effective way to ensure that your estate plan is robust, minimizes tax burdens for your heirs, and honors your wishes for the distribution of your wealth. This proactive approach will provide peace of mind for you and a smoother, less financially burdensome transition for your loved ones.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.