California, often heralded as the Golden State, beckons with its captivating blend of sun-drenched beaches, towering redwood forests, vibrant cultural hubs, and an unparalleled lifestyle. For many contemplating retirement, the allure of spending their golden years amidst this picturesque setting is undeniable. Imagine waking up to the gentle Pacific breeze in Santa Barbara, exploring the historic vineyards of Napa Valley and Sonoma Valley, or enjoying world-class dining and entertainment in Los Angeles or San Francisco. However, the dream of a California retirement often comes with a crucial question: how will it impact my finances, particularly my Social Security benefits?

Understanding the tax landscape is a paramount concern for anyone planning a long-term stay, a move, or even an extended vacation that might transition into retirement in the United States. Financial considerations are a core part of the lifestyle planning that goes into choosing a retirement destination, whether it’s for luxury travel, a budget-conscious relocation, or family visits. This article delves into the specifics of California’s tax policies regarding Social Security and other retirement income, helping you paint a clearer picture of what to expect when considering the Golden State for your golden years.

Unpacking California’s Stance on Retirement Income

The first and most pressing question for many retirees is whether their hard-earned Social Security benefits will be subject to state taxes in California. The answer to this specific query often brings a sigh of relief to prospective residents.

The Good News for Social Security Recipients

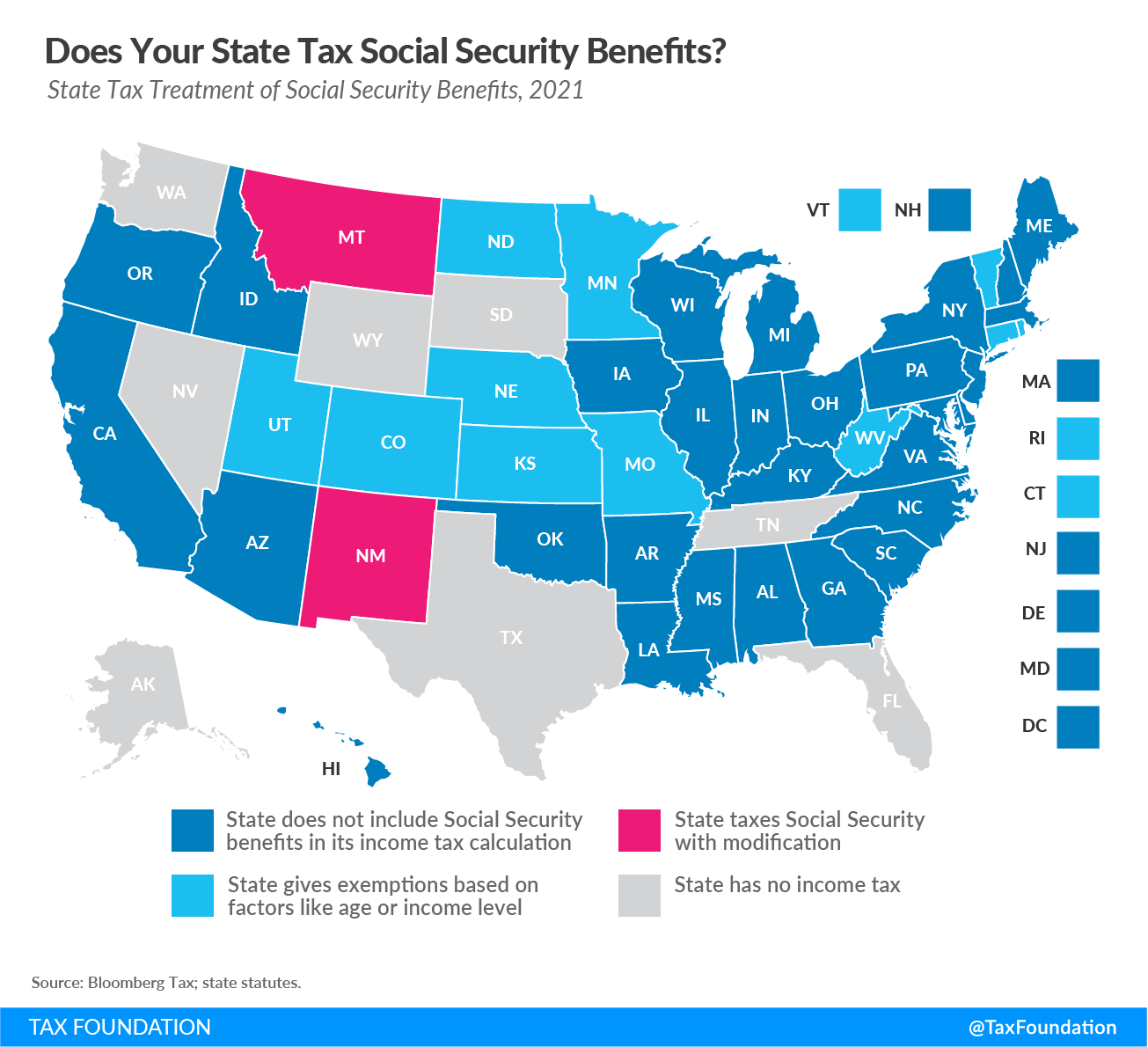

Let’s cut directly to the chase: California does NOT tax Social Security benefits. This is a significant piece of good news for retirees who rely on these payments as a cornerstone of their financial security. Unlike some other states that might tax a portion of Social Security income based on federal adjusted gross income thresholds, California completely exempts these benefits from state income tax. This means that if you’re receiving Social Security payments, that portion of your retirement income will remain untouched by the state’s tax collectors, allowing you to allocate more funds towards enjoying the myriad attractions and experiences California has to offer, from exploring Yosemite National Park to indulging in the culinary delights of San Francisco. This policy makes California a more appealing destination for those for whom Social Security forms a substantial part of their retirement budget, offering peace of mind regarding this particular income stream. It’s an important consideration when evaluating the overall financial viability of a move to the Golden State, especially when juxtaposed with the state’s reputation for higher costs in other areas.

Beyond Social Security: Other Retirement Income Considerations

While California’s stance on Social Security is favorable, it’s crucial for retirees to understand how the state taxes other forms of retirement income. The overall picture of your retirement finances will be influenced by how your pensions, 401(k)s, IRAs, and other investments are treated. In California, income from private and public pensions, as well as distributions from 401(k)s, IRAs, and other retirement savings plans, are generally considered taxable income. These sources are subject to the state’s progressive income tax rates, which can be among the highest in the nation.

This means that while your Social Security is safe, a significant portion of your other retirement income could be taxed at a substantial rate, depending on your total annual income. For individuals with robust pension plans or large investment portfolios, this can have a considerable impact on their disposable income. Furthermore, capital gains from investments are also subject to California’s income tax, which can be a factor for retirees who plan to sell assets or manage an active investment portfolio. Therefore, a comprehensive financial plan for retirement in California must carefully account for the taxation of all income streams beyond Social Security. Understanding these nuances is vital for anyone assessing the financial implications of long-term accommodation or a permanent move, allowing them to budget effectively for daily expenses, travel, and leisure activities throughout the Golden State.

The Broader Financial Picture: Understanding California’s Tax Landscape

Moving beyond specific retirement income, a complete understanding of California’s tax environment is essential for anyone considering a move or extended stay. The state’s financial landscape is multifaceted, encompassing income tax, property tax, and sales tax, all of which contribute to the overall cost of living.

High Income Tax Rates and Their Impact

California is renowned for its progressive income tax system, meaning that higher earners pay a larger percentage of their income in taxes. The state’s top marginal income tax rate is among the highest in the United States, reaching up to 13.3% for the highest income brackets. While this might not directly affect those solely reliant on Social Security, it significantly impacts retirees with substantial pension income, investment earnings, or other taxable income. For instance, a retiree with a high pension from a former employer could find a considerable portion of that income going towards state taxes, regardless of their age. This progressive structure also applies to capital gains, making it a crucial consideration for those planning to sell assets during retirement. The impact of these rates extends beyond mere numbers; it affects lifestyle choices, from the type of accommodation one can afford to the frequency of travel and leisure activities. A higher tax burden on other income streams means less discretionary spending, which could necessitate adjustments to a desired lifestyle, whether it involves luxury travel or simply enjoying local attractions like Disneyland or the Hollywood Walk of Fame. Thorough financial planning, often involving a financial advisor, is critical to navigating these income tax implications effectively and ensuring a comfortable retirement in the Golden State.

Property Taxes and Housing Costs: A Major Factor

Perhaps one of the most significant financial considerations for retirees in California is the cost of housing and the associated property taxes. California’s real estate market is notoriously expensive, with median home prices in desirable areas like San Francisco, Los Angeles, San Diego, Orange County, and Palo Alto often far exceeding the national average. This high cost of entry can be a formidable barrier for new retirees looking to purchase a home.

However, California does have a unique system for property taxes, largely governed by Proposition 13, enacted in 1978. Proposition 13 limits property taxes to 1% of the assessed value at the time of purchase, plus a maximum annual increase of 2% (or the inflation rate, whichever is lower). This means that long-term residents who purchased their homes decades ago often pay remarkably low property taxes compared to the current market value. For new buyers, however, the property tax will be based on the much higher current purchase price, which can result in substantial annual tax bills. This disparity creates a complex landscape for retirees. Those already owning homes in California can enjoy relatively stable and low property tax burdens, a major financial advantage. Newcomers, on the other hand, must factor in potentially very high property tax payments on top of the steep purchase prices. This makes researching specific locations and understanding property tax implications crucial when evaluating accommodation options, whether it’s a luxurious villa in Beverly Hills or a more modest home in the Central Valley. The cost of accommodation is often the largest single expense, directly impacting one’s overall retirement budget and ability to enjoy other aspects of the California lifestyle.

Sales Tax and Other Levies

Beyond income and property taxes, retirees in California must also consider sales tax and various other levies that contribute to the overall cost of living. California has one of the highest statewide sales tax rates in the United States, currently at 7.25%. However, local jurisdictions can add their own district sales taxes, pushing the combined rate in some cities to over 10%. This means that nearly every purchase, from groceries (excluding most unprepared food) to clothing, entertainment, and personal services, will incur this additional cost. For retirees on a fixed income, these recurring expenses can subtly but significantly impact their monthly budget.

Furthermore, California imposes other taxes and fees that, while not as prominent as income or property taxes, still add to the financial burden. These include high gas taxes, which impact transportation costs, especially important for exploring vast distances like driving the Pacific Coast Highway or visiting national parks. Vehicle registration fees are also notable. While these individual taxes might seem small, their cumulative effect can be substantial over the course of a year, influencing everything from daily errands to travel plans and overall tourism experiences. Therefore, when evaluating the financial feasibility of retirement in California, it’s important to account for these “hidden” costs alongside the more significant income and property tax considerations, ensuring a realistic budget that supports your desired lifestyle.

Weighing the Golden State’s Appeal for Retirees

Despite the financial complexities, the magnetic pull of California remains incredibly strong for retirees. The state offers an unparalleled blend of natural beauty, cultural richness, and lifestyle opportunities that many find irresistible, making the financial trade-offs seem worthwhile.

The Allure of California’s Lifestyle and Attractions

The undeniable appeal of California for retirees lies in its incredibly diverse and vibrant lifestyle, coupled with world-class attractions and natural beauty. The climate itself is a major draw, with year-round sunshine in many regions like Palm Springs and San Diego, allowing for an active outdoor lifestyle well into one’s golden years. Imagine hiking in the Sierra Nevada Mountains, golfing year-round, or enjoying beach strolls along the Malibu coast.

Beyond the climate, California boasts an incredible array of tourist attractions and landmarks. Nature lovers can explore the majestic sequoias of Redwood National Park, the stark beauty of Death Valley, or the serene waters of Lake Tahoe. Cultural enthusiasts will find an abundance of museums, theaters, and culinary experiences in cities like Los Angeles, San Francisco, and Sacramento. From wine tasting in Napa Valley to whale watching off Monterey, the opportunities for travel and unique experiences are endless. Many communities offer excellent healthcare facilities and a robust social infrastructure catering to seniors. The chance to live a healthy, active, and culturally enriched retirement, surrounded by stunning landscapes and diverse communities, is often the compelling factor that sways retirees towards the Golden State, making the potential financial hurdles seem less daunting when balanced against such a rich lifestyle.

Navigating the High Cost of Living

While the lifestyle benefits are immense, the reality of California’s high cost of living remains a significant hurdle for many retirees. Beyond taxes, virtually everything from housing and utilities to groceries and transportation can be more expensive than in other parts of the United States. This elevated cost impacts not just big-ticket items like accommodation but also daily expenses and the overall budget for travel and leisure.

Navigating this reality requires careful planning and, for some, strategic compromises. One common strategy is to consider regions outside the major metropolitan areas. While San Francisco, Los Angeles, and Silicon Valley are notoriously expensive, areas like Riverside, San Bernardino, or parts of the Central Valley offer more affordable housing options, albeit often with different climates and access to amenities. Retirees might also consider downsizing their living space, opting for apartments or condos over single-family homes, or even exploring long-term stay options in areas with a lower cost of living. Budgeting diligently for all expenses, including sales tax on everyday purchases and higher gas prices for exploring landmarks like the Golden Gate Bridge or Big Sur, becomes paramount. It’s about weighing the trade-offs: the dream lifestyle might require a more disciplined financial approach or a willingness to explore lesser-known, more budget-friendly destinations within the state, ensuring that the Golden State dream remains achievable without financial strain.

Making an Informed Decision: Is California Right for Your Retirement?

Deciding whether to retire in California is a deeply personal choice, intertwined with financial realities and lifestyle aspirations. There’s no one-size-fits-all answer, but understanding the complete picture, particularly around taxation and cost of living, is fundamental.

The good news is clear: your Social Security benefits will not be taxed by the state of California. This is a significant advantage that can alleviate some financial pressure. However, this positive aspect must be balanced against the state’s high income tax rates on other retirement income (like pensions and 401(k) distributions), the potentially substantial property taxes for new homeowners, and the generally elevated cost of living across various sectors.

For those who prioritize an active, diverse, and culturally rich lifestyle amidst stunning natural beauty, and who have the financial means to navigate the higher costs, California can be an idyllic retirement destination. The opportunities for travel, exploration of famous places from Carmel-by-the-Sea to Ventura County, and engagement in a vibrant community are unparalleled.

Conversely, for retirees whose primary concern is maximizing their retirement savings and minimizing tax burdens, or those with more modest incomes, the financial hurdles in California might outweigh the lifestyle benefits. It’s crucial to perform a detailed personal financial analysis, considering all income sources, potential expenditures, and specific regional costs within the state. Consulting with a financial advisor specializing in retirement planning can provide invaluable insights tailored to your unique situation. They can help you model different scenarios, identify potential tax savings, and strategize for a sustainable retirement.

Ultimately, retiring in California means making a conscious trade-off. It’s about weighing the exceptional quality of life, the diverse attractions, and the year-round opportunities for tourism and leisure against the financial demands of living in one of the most dynamic, yet expensive, states in the United States. With careful planning and a clear understanding of the tax landscape, the dream of a Golden State retirement can indeed become a vibrant reality.