Embarking on a journey, whether it’s for a luxurious escape to a Caribbean resort, an adventurous trek through the national parks of the United States, or a business trip to London, brings with it a thrill of anticipation. However, amidst the excitement of planning your itinerary, booking your flights, and reserving your ideal accommodation, a crucial question often lingers in the minds of savvy travelers: “Does my renters insurance cover me when I’m staying in a hotel?”

This seemingly straightforward question delves into the intricacies of insurance policies, travel safeguards, and the distinctions between protecting your home and securing your journey. For those who prioritize peace of mind, understanding the scope of your existing renters insurance policy in a travel context is paramount. While renters insurance is designed to protect your belongings and liability within your primary residence, its coverage doesn’t simply disappear the moment you step out the door. However, its application in a temporary accommodation like a hotel, a charming Airbnb apartment, or a serene villa is often nuanced, limited, and can be a source of confusion.

This comprehensive guide aims to unravel these complexities, explaining precisely what your renters insurance might cover while you’re away from home, what it definitely won’t, and why a multi-faceted approach to travel protection, potentially including dedicated travel insurance and credit card benefits, is often the wisest course of action for any traveler. From safeguarding your personal belongings against theft in a Paris hotel room to understanding your liability if an unforeseen accident occurs at a resort in Hawaii, we’ll explore every angle to ensure your travels are as secure as they are memorable.

Understanding the Fundamentals of Renters Insurance

Before we can determine how renters insurance applies to your travels, it’s essential to grasp its core components and what it typically safeguards within your everyday life. Renters insurance, often an affordable yet vital policy for anyone renting a home or apartment, primarily offers three main categories of coverage: personal property, liability, and additional living expenses.

Personal Property Coverage (Contents Coverage)

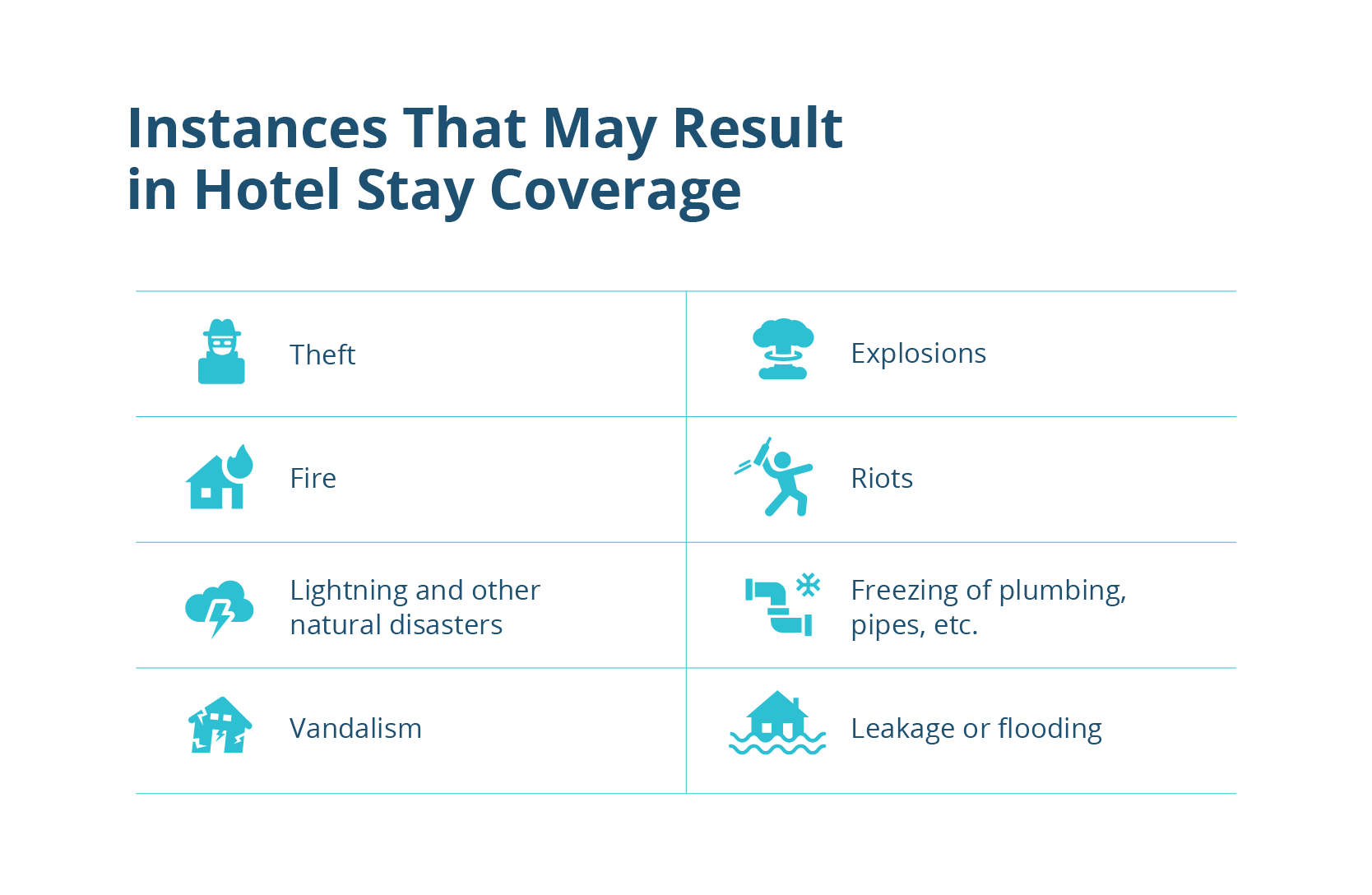

This is arguably the most recognized aspect of renters insurance. Personal property coverage, sometimes referred to as “contents coverage,” is designed to protect your belongings from a wide array of perils such as theft, fire, smoke, vandalism, and certain types of water damage. It covers items like furniture, electronics, clothing, jewelry, and other personal possessions that would be costly to replace. When you consider the cumulative value of everything you own, from your smartphone and laptop to your wardrobe and kitchenware, it quickly becomes clear why this coverage is indispensable. Most policies offer either actual cash value (depreciated value) or replacement cost value coverage, with the latter paying out enough to buy new replacements for damaged or stolen items. The level of protection you choose, alongside your deductible, will dictate your premium and how much you’d receive in a claim.

Liability Coverage

Beyond protecting your possessions, renters insurance also provides crucial liability coverage. This protects you financially if you are found responsible for causing bodily injury to another person or damage to someone else’s property, whether at your rented home or sometimes even away from it. For instance, if a guest slips and falls in your apartment, or if your pet bites someone, your liability coverage can help cover legal fees, medical expenses, and settlement costs up to your policy limits. This safeguard extends to accidental damage you might inflict on the property you rent, protecting you from potentially ruinous out-of-pocket expenses. It’s a vital safety net that many renters overlook but is incredibly important for comprehensive protection.

Additional Living Expenses (ALE)

The third primary component is Additional Living Expenses (ALE) coverage, also known as “loss of use” coverage. This critical safeguard comes into play if your rented home becomes uninhabitable due to a covered peril, such as a fire or a severe storm. ALE covers the necessary increase in living expenses incurred while your home is being repaired or rebuilt. This can include the cost of a temporary apartment, a hotel stay, meals eaten out, and other essential expenses that exceed your normal spending. It ensures you have a place to stay and the means to live comfortably during a challenging period, preventing financial hardship on top of the distress of home damage. However, it’s important to note that ALE is specifically tied to the uninhabitability of your primary residence, a distinction that becomes critical when discussing travel.

Renters Insurance on the Road: How it Applies to Your Hotel Stay

Now that we understand the foundations of renters insurance, let’s explore how these coverages might extend their protective umbrella when you’re away from your primary residence, specifically during a hotel stay or while exploring a vibrant city like New York City. The good news is that certain aspects of your renters insurance policy do offer protection beyond your four walls, but with specific limitations and conditions.

Protecting Your Valuables Away From Home

One of the most valuable features for travelers is the “off-premises” personal property coverage. Most standard renters insurance policies include a provision that extends your personal property coverage to items you take with you on vacation, whether you’re staying at a Hilton resort, a cozy bed and breakfast in the countryside, or a budget-friendly hostel. This means that if your laptop is stolen from your hotel room in Tokyo, your camera bag goes missing from your rental car while touring the Grand Canyon, or your designer luggage is pilfered from a locker at a Rome train station, your renters insurance could provide reimbursement.

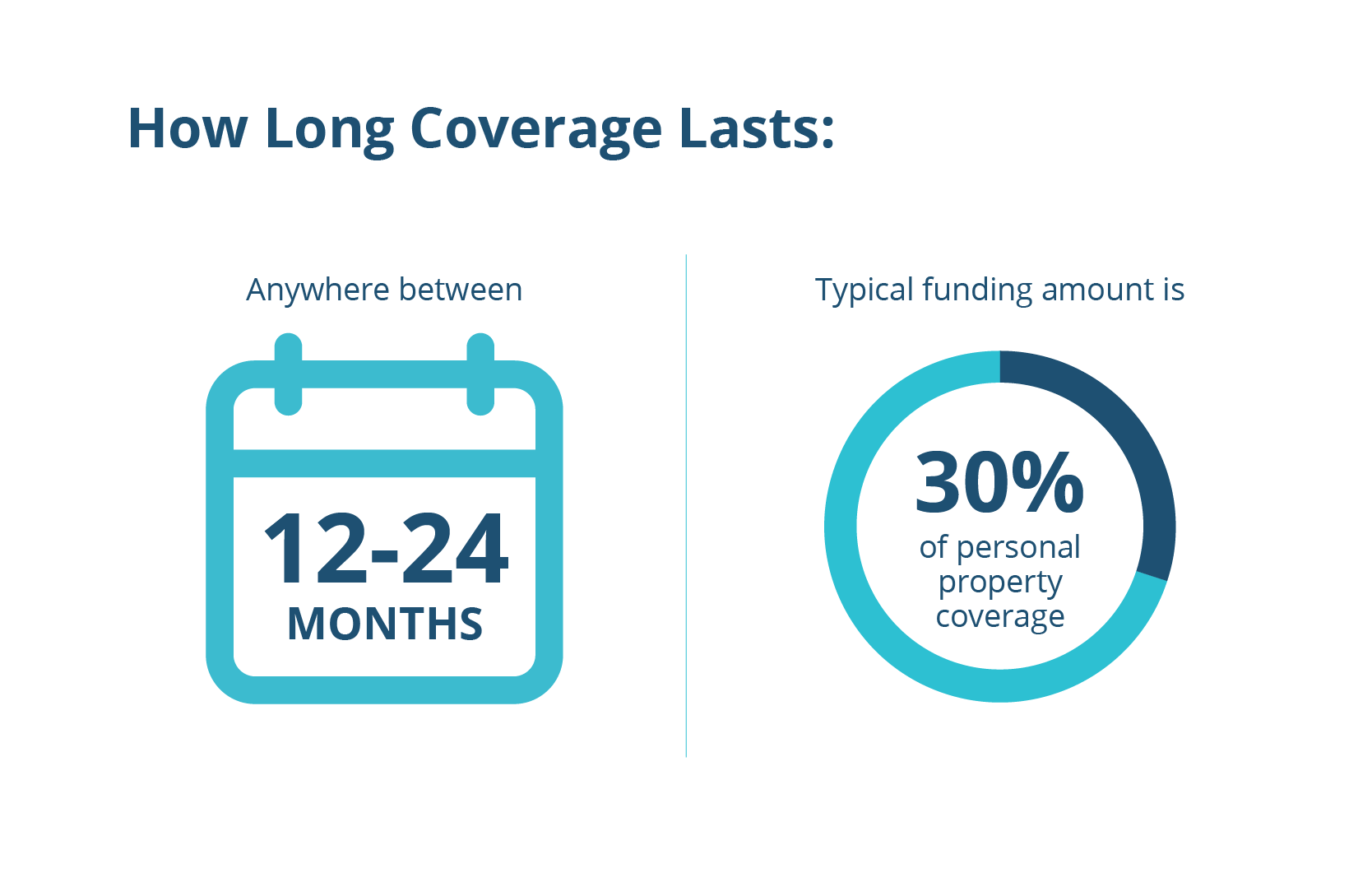

However, there are crucial caveats. Typically, off-premises coverage is limited to a percentage of your total personal property coverage, often around 10% to 20%. So, if you have $30,000 in personal property coverage, only $3,000 to $6,000 might apply to items stolen or damaged while you’re traveling. Furthermore, high-value items like expensive jewelry, fine art, or specialized electronics often have sub-limits within your policy, meaning they might only be covered up to a certain amount (e.g., $1,500 for jewelry) unless you have them specifically “scheduled” or “endorsed” onto your policy with additional coverage. Deductibles also apply, meaning you’ll need to pay that initial amount out of pocket before your insurance kicks in. It’s also vital to understand that this coverage usually protects against specified perils, like theft or fire, but typically not against simple loss or mysterious disappearance (e.g., leaving your phone on a park bench).

Navigating Liability in Temporary Accommodations

Your personal liability coverage from your renters insurance policy also often extends beyond your primary residence, offering a layer of protection during your travels. This means that if you accidentally cause damage to your hotel room — for example, if you spill red wine on the carpet, break a valuable vase, or even accidentally start a small fire (though hopefully never!) — your liability coverage might help pay for the repair or replacement costs. Similarly, if you accidentally injure another guest at your resort, say by tripping them in the lobby or spilling hot coffee on them at breakfast, your policy could assist with their medical expenses and any potential legal fees, up to your coverage limits.

This extension of liability is a significant benefit, providing a safety net against unforeseen accidents that could otherwise lead to substantial out-of-pocket expenses. However, just like with personal property, there are limits to this coverage. Intentional acts are never covered, and there might be exclusions for certain types of activities or property. It’s always wise to review your policy documents or contact your insurance provider to fully understand the scope of your liability coverage when traveling, especially if you plan on participating in activities that could carry higher risks.

The Limitations of ALE for Travel

This is where a common misconception arises. While Additional Living Expenses (ALE) coverage is a cornerstone of renters insurance, it is generally not applicable to travel disruptions, even if you find yourself staying in a hotel. ALE is specifically designed to cover the costs incurred when your primary residence becomes uninhabitable due to a covered loss (e.g., a fire or flood at your apartment forces you out). It pays for temporary accommodation and increased living expenses while your home is being repaired.

It does not cover:

- Expenses if your flight is delayed or canceled, forcing an unexpected hotel stay.

- Costs if you miss a cruise departure due to unforeseen circumstances.

- Accommodation expenses due to a natural disaster occurring at your travel destination (unless it directly caused damage to your home).

- Any other travel-related inconvenience that disrupts your trip but doesn’t affect the habitability of your primary residence.

For these types of travel-related disruptions, a dedicated travel insurance policy or certain credit card benefits are the appropriate solutions, which we will explore next. This distinction is crucial for travelers to understand, as relying on ALE for travel disruptions will almost certainly lead to disappointment.

When Renters Insurance Falls Short: Exploring Broader Travel Protections

While renters insurance offers some valuable peace of mind regarding your personal property and liability away from home, it’s crucial to acknowledge its limitations as a travel protection tool. For comprehensive coverage against the myriad of unforeseen events that can derail a trip, dedicated travel insurance and the often-overlooked benefits of credit cards come into play.

Comprehensive Travel Insurance: A Dedicated Solution

For most travelers, especially those embarking on significant or international trips, a standalone travel insurance policy is the most robust and appropriate solution. Travel insurance is specifically designed to address the unique risks associated with being away from home, covering a much broader spectrum of scenarios that renters insurance simply doesn’t touch.

Key benefits of travel insurance include:

- Trip Cancellation and Interruption: Reimburses non-refundable expenses if your trip is canceled or cut short due to covered reasons like illness, injury, natural disaster at your destination, or a family emergency. This is particularly valuable for expensive trips to destinations like the Maldives or a European tour across Italy and France.

- Medical Emergencies: Covers emergency medical and dental expenses incurred during your trip. This is critically important, as your domestic health insurance often provides very limited or no coverage outside your home country, and even within the United States, unforeseen medical issues can be incredibly costly. It can also cover emergency medical evacuation, which can run into tens of thousands of dollars.

- Travel Delays: Provides reimbursement for unexpected accommodation, meals, and transportation if your flight or other common carrier is delayed for a covered reason and a specified duration.

- Lost, Damaged, or Delayed Baggage: Offers much more comprehensive coverage for your luggage and its contents than renters insurance, especially when the airline is at fault. It can help replace essential items quickly while you wait for your bags, or provide a payout if they are permanently lost.

- Rental Car Coverage: Many policies include primary or secondary coverage for damage to a rental vehicle.

- Emergency Assistance: Provides 24/7 access to assistance services for travel emergencies, from rebooking flights to locating medical facilities.

Whether you’re planning a budget-friendly backpacking adventure or a luxury cruise, travel insurance can be tailored to your specific needs, offering protection for medical emergencies, adventure sports, or even “cancel for any reason” options for ultimate flexibility. For travelers exploring destinations that require specialized guides or activities, such as a safari in Kenya or a dive trip to the Great Barrier Reef, this dedicated protection is indispensable.

The Hidden Benefits of Credit Card Travel Protections

Many premium credit cards offer a surprising array of travel benefits that can complement or even stand in for some aspects of travel insurance. These perks are often overlooked but can provide significant value, especially for frequent travelers or those on business trips.

Common credit card travel benefits include:

- Trip Cancellation/Interruption Insurance: Similar to travel insurance, this can reimburse non-refundable travel expenses if your trip is disrupted due to a covered event, provided you booked the trip using that card.

- Lost/Delayed Baggage Coverage: If your luggage is lost or delayed by a common carrier, many cards will provide reimbursement for essential items you need to purchase.

- Rental Car Insurance (Collision Damage Waiver): Many credit cards offer secondary (or sometimes primary) coverage for collision and theft of a rental vehicle. This can save you money by allowing you to decline the rental car company’s expensive insurance.

- Travel Accident Insurance: Provides coverage for accidental death or dismemberment during a trip booked with the card.

- Travel Delay Reimbursement: Covers expenses like meals and lodging if your flight is significantly delayed.

- Concierge Services: While not insurance, these services can be invaluable for finding last-minute restaurant reservations in Paris or securing tickets to a popular show in Las Vegas.

It’s crucial to remember that credit card benefits often come with specific terms, conditions, and coverage limits. They typically only apply when the entire trip or a significant portion of it is paid for with that particular card. Always check with your credit card issuer to understand the exact details of your benefits before relying on them for your travel protection. For a family trip to Disneyland or a solo journey to explore ancient landmarks like the Colosseum in Rome, these benefits can provide a valuable safety net.

Specific Exclusions and Gaps

Even with renters insurance, travel insurance, and credit card benefits, it’s important to be aware that certain events or items might still fall into coverage gaps.

- High-Value Items: While renters insurance offers some off-premises coverage, extremely valuable items like rare art, high-end electronics, or heirloom jewelry often require specific endorsements or separate policies (e.g., a personal articles floater) to be fully protected, especially when traveling.

- Negligence: No insurance policy will cover losses due to gross negligence (e.g., leaving your valuables openly displayed in an unlocked car or hotel room).

- Certain Activities: Adventure sports like skydiving, bungee jumping, or extreme skiing may be excluded from standard travel insurance policies and definitely from renters insurance. Specialized adventure travel insurance is needed for these activities.

- Pre-Existing Conditions: Some medical exclusions might apply to pre-existing conditions unless a waiver is purchased or specific criteria are met.

- Acts of War/Terrorism: Most standard policies have exclusions for acts of war or terrorism, though some specialized travel insurance might offer limited coverage.

Understanding these potential gaps is key to making informed decisions about your overall travel protection strategy.

Practical Steps and Smart Strategies for Insured Travel

Navigating the world of insurance can seem daunting, but with a few proactive steps, you can significantly enhance your travel security and enjoy your experiences with greater peace of mind. Whether you’re planning a long-term stay abroad, a quick weekend getaway, or a business trip, a thoughtful approach to your coverage is essential.

Review Your Policy Before You Go

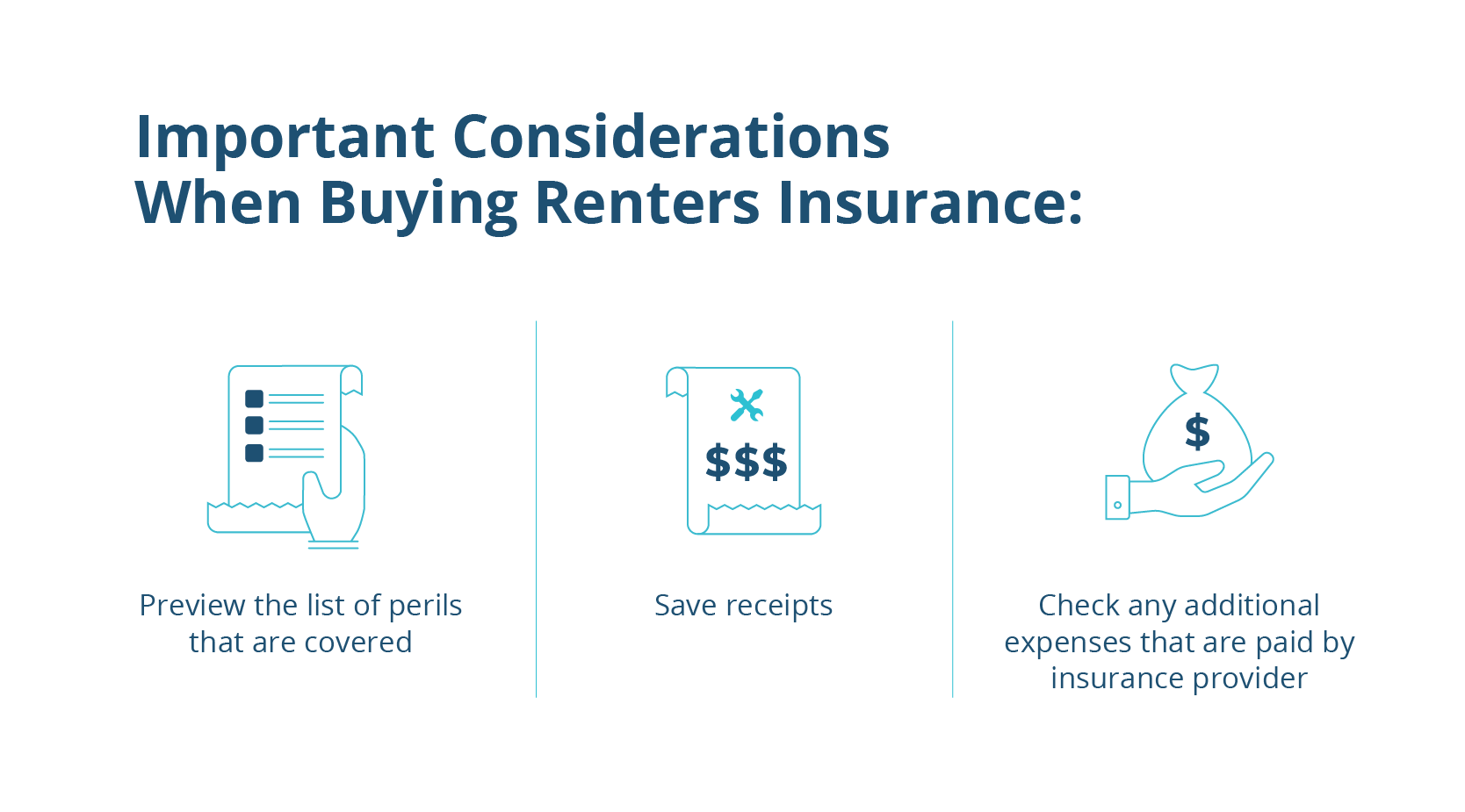

The single most important step you can take is to thoroughly review your existing renters insurance policy before embarking on any trip. Don’t assume anything.

- Contact Your Insurer: Call your insurance agent or company directly. Explain your travel plans, including your destination (e.g., Japan, Germany), the type of accommodation (hotel, serviced apartment), the duration of your trip, and any particularly valuable items you’ll be taking.

- Understand Off-Premises Limits: Ask about the specific percentage or dollar limit for personal property coverage away from your home.

- Inquire About Deductibles: Know your deductible amount, as a small claim might not exceed it, making filing a claim impractical.

- Clarify Exclusions: Ask about any specific exclusions that might apply to travel or certain types of property.

- Consider Endorsements: If you’re bringing high-value items, ask about scheduling them on your policy with a “personal articles floater” for more robust, specific coverage, often with no deductible.

- Keep a Copy of Your Policy: Have access to your policy details, including your policy number and claims contact information, while you’re traveling.

This pre-trip check-up can reveal crucial information and help you decide if additional coverage is needed.

Documenting and Making a Claim

Should the unfortunate happen while you’re traveling, proper documentation and prompt action are vital for a successful insurance claim.

- Report Incidents Immediately: For theft, damage to your hotel room, or personal injury, report the incident to the hotel management, local police (if theft or significant damage occurred), or the relevant authorities as soon as possible. Obtain a written report or case number.

- Document Everything: Take photos or videos of damaged items, the scene of an accident, or any signs of forced entry. Keep receipts for stolen items, or any new purchases made to replace essentials.

- Gather Contact Information: For liability claims, collect contact details from any witnesses or involved parties.

- Contact Your Insurer Promptly: Notify your renters insurance provider as soon as you can. They will guide you through the claims process and inform you of the necessary documentation. Be prepared to provide all reports, photos, and itemized lists of losses.

Diligence in these steps can significantly streamline your claim and increase your chances of fair reimbursement.

Choosing the Right Coverage Mix

The ideal approach to insured travel often involves a strategic combination of your existing renters insurance, dedicated travel insurance, and leveraging your credit card benefits.

- For Everyday Travel: For shorter, less expensive domestic trips where you’re not carrying many high-value items, your renters insurance might offer sufficient protection for personal property theft and liability. Your credit card might cover rental cars or minor delays.

- For Significant or International Travel: For longer journeys, international trips, or adventures involving significant financial investment, a comprehensive travel insurance policy is highly recommended. It fills the crucial gaps in medical coverage, trip cancellation, and extensive baggage protection that renters insurance does not provide.

- For High-Value Items: If you routinely travel with expensive cameras, laptops, or jewelry, consider scheduling these items on your renters policy, or even obtaining a separate specialized policy, regardless of your other travel plans.

- For Adventure Travel: If your lifestyle involves extreme sports or high-risk activities, ensure your travel insurance explicitly covers these specific pursuits, as standard policies often exclude them.

By carefully assessing your travel plans, understanding the value of your belongings, and considering potential risks, you can craft a personalized insurance strategy that provides optimal protection for every journey. Whether you’re exploring the cultural richness of Vietnam or simply enjoying a tranquil beach vacation, being prepared allows you to focus on the experience rather than worrying about the unexpected.

In conclusion, while renters insurance offers a valuable, albeit limited, safety net for your personal property and liability when you’re staying in a hotel or traveling, it is not a comprehensive travel insurance solution. It provides a foundational layer of protection for theft or damage to your belongings away from home, and for personal liability, but critically falls short on covering trip cancellations, medical emergencies abroad, travel delays, or extensive lost luggage scenarios. For true peace of mind and robust financial protection against the myriad of potential disruptions that can occur during travel, a dedicated travel insurance policy, often supplemented by the hidden benefits of your premium credit cards, is highly recommended. Always review your policies, understand their limitations, and make informed decisions to ensure your adventures, wherever they may lead, are secure and worry-free.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.