Embarking on the journey of homeownership in the Lone Star State is an exciting prospect, brimming with the promise of spacious living and a vibrant lifestyle. Whether you’re dreaming of a sprawling ranch in the Hill Country, a modern condo in the heart of Dallas, or a charming bungalow in Austin, the path to owning your piece of Texas is paved with exciting possibilities. However, alongside the thrill of finding your perfect abode comes the often-overlooked but crucial aspect of closing costs. These are the fees and expenses incurred by both the buyer and the seller during the final stages of a real estate transaction. Understanding these costs is paramount to budgeting accurately and avoiding unwelcome surprises as you approach the finish line of your home purchase.

While the dream of owning a home in Texas is tangible, the financial realities of closing the deal require careful consideration. Unlike some other states where closing costs are largely standardized, Texas presents a landscape where these expenses can fluctuate. This variation is influenced by a multitude of factors, from the specific property and its location to the chosen lenders and title companies. This comprehensive guide aims to demystify the world of Texas closing costs, providing you with the insights needed to navigate this essential part of the homebuying process with confidence. We’ll break down the typical components, explore the variables that impact the total, and offer tips for managing these expenses, ensuring your Texas homeownership dream becomes a smooth and well-prepared reality.

Deconstructing the Components of Texas Closing Costs

Closing costs in Texas are not a single, monolithic fee but rather a collection of various charges that add up to the final sum due at the time of sale. These costs are typically divided between the buyer and the seller, although the exact allocation can sometimes be a point of negotiation. For buyers, these costs represent a significant upfront investment beyond the down payment and purchase price, while sellers also incur a set of expenses that reduce their net proceeds from the sale. Understanding each component is key to comprehending the overall financial picture.

Buyer’s Closing Costs: The Investment Beyond the Down Payment

As a buyer, your closing costs will likely encompass a broader range of expenses, reflecting the services and protections you receive as the new owner. These fees are essential for transferring ownership, securing your financing, and ensuring the property is free and clear of any encumbrances.

Loan-Related Fees

- Loan Origination Fee: This is a fee charged by your mortgage lender for processing and underwriting your loan. It’s typically a percentage of the loan amount, often ranging from 0.5% to 1%. The specific amount can vary significantly between lenders, so comparing offers is crucial.

- Appraisal Fee: Lenders require an appraisal to determine the fair market value of the property. This ensures the loan amount is not higher than the home’s worth. The cost of an appraisal usually falls between $300 and $500, depending on the property’s size and location.

- Credit Report Fee: Your lender will pull your credit report to assess your financial history and creditworthiness. This fee is generally modest, usually around $30 to $50.

- Flood Certification Fee: If the property is located in a flood zone, a flood certification fee is required to determine if flood insurance will be necessary. This fee is typically under $25.

- Discount Points: Some buyers opt to pay “points” upfront to lower their interest rate over the life of the loan. One point is equal to 1% of the loan amount. This is an optional expense, driven by individual financial goals and market conditions.

- Private Mortgage Insurance (PMI) or FHA Mortgage Insurance Premium (MIP): If your down payment is less than 20% of the home’s purchase price, you’ll likely need to pay PMI (for conventional loans) or MIP (for FHA loans). This protects the lender in case you default on the loan. The cost varies based on your credit score and down payment percentage.

Title and Escrow Fees

- Title Search Fee: This fee covers the cost of researching public records to ensure the seller has clear title to the property and there are no outstanding liens, claims, or encumbrances.

- Title Insurance: You’ll be required to purchase a lender’s title insurance policy to protect the lender. You’ll also have the option to purchase an owner’s title insurance policy, which protects you, the buyer, for as long as you own the home. These policies are a one-time fee paid at closing.

- Escrow Fees: The escrow company acts as a neutral third party, holding funds and documents until all conditions of the sale are met. Their fee covers their services in managing the closing process. This fee is often split between the buyer and seller.

- Recording Fees: These fees are charged by the county government to officially record the new deed and mortgage in public records.

Other Buyer Expenses

- Homeowners Insurance: Lenders require you to have homeowners insurance in place before closing. You’ll typically pay the first year’s premium upfront.

- Property Taxes: You will likely need to pay a pro-rated portion of the current year’s property taxes, as well as deposit funds into an escrow account to cover future tax payments.

- Prepaid Interest: You’ll pay per diem interest from the closing date until the end of the month in which you close.

- HOA Dues (if applicable): If the property is part of a Homeowners Association, you may need to pay pro-rated dues and potentially an initial capital contribution fee.

Seller’s Closing Costs: Preparing for the Sale

Sellers also have a set of closing costs that reduce their net profit from the sale. These are often related to transferring ownership and clearing any existing obligations on the property.

Real Estate Agent Commissions

- Real Estate Agent Commissions: This is typically the largest closing cost for sellers, usually ranging from 5% to 6% of the sale price, which is then split between the buyer’s and seller’s agents. This is a significant expense and a key factor in the seller’s net proceeds.

Title and Escrow Fees

- Title Search and Title Insurance: While buyers pay for lender’s title insurance, sellers often pay for their portion of the title search and may contribute to or pay for the owner’s title insurance policy, depending on local customs and negotiation.

- Escrow Fees: Similar to buyers, sellers will pay a portion of the escrow company’s fees for their role in facilitating the transaction.

- Recording Fees: Sellers may incur fees for releasing existing liens or recording documents related to the sale.

Other Seller Expenses

- Outstanding Mortgage Payoff: The seller must pay off any remaining balance on their current mortgage.

- Property Taxes: Pro-rated property taxes up to the closing date are typically paid by the seller.

- HOA Dues: Sellers will pay their share of HOA dues up to the closing date.

- Survey Fee (sometimes): In some transactions, a new survey of the property may be required, which the seller might be responsible for.

- Termite Inspection and Repairs: Depending on the contract and local practice, sellers may need to pay for a termite inspection and any necessary repairs.

- Attorney Fees: While not always required, some sellers choose to hire an attorney to review contracts and ensure their interests are protected.

Factors Influencing the Total Cost of Closing in Texas

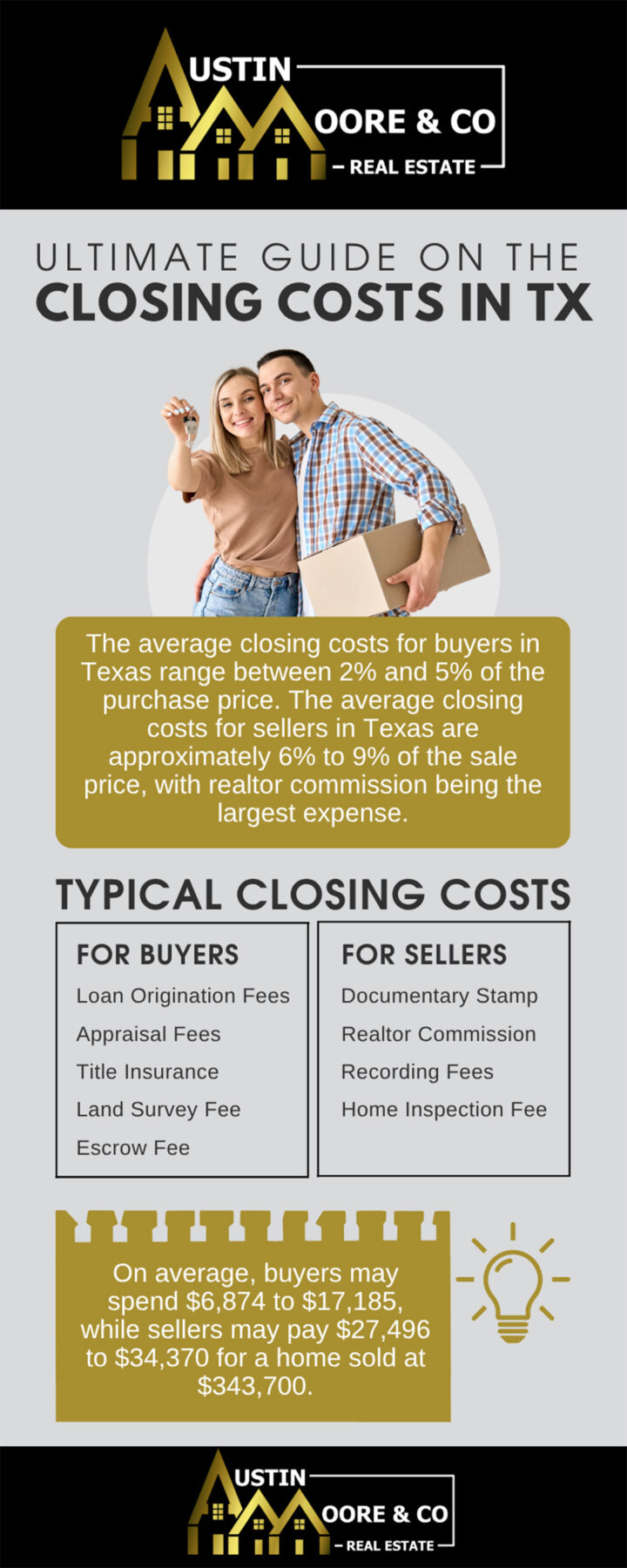

The total closing costs in Texas can be a significant figure, often estimated to be between 2% and 5% of the loan amount or purchase price for buyers, and a similar or slightly higher percentage for sellers when factoring in agent commissions. However, this is a broad estimate, and the actual amount can be influenced by numerous variables, making each transaction unique.

Location, Location, Location: County and City Specific Fees

The specific county and city where the property is located play a crucial role in determining closing costs. Each county in Texas has its own set of recording fees, transfer taxes (though Texas doesn’t have a statewide transfer tax on real estate, some municipalities may have specific fees), and other administrative charges. For instance, closing costs in a bustling metropolitan area like Houston or San Antonio might differ from those in a smaller town in West Texas. Understanding the local fee structure is essential for accurate budgeting.

The Role of Lender and Title Company Choice

Your choice of mortgage lender and title company can also impact your closing costs. Different lenders may have varying origination fees, underwriting charges, and processing fees. Similarly, title companies can have different fee structures for their title search, title insurance, and escrow services. It’s wise to shop around and compare quotes from multiple lenders and title companies to find the most competitive rates. Many buyers opt for a title company that is well-versed in Texas real estate laws and practices, ensuring a smooth transaction, but always inquire about their fee breakdown.

The Nature of the Transaction: New Construction vs. Resale

The type of property you’re purchasing can also affect closing costs. For example, buying a new construction home might involve different fees compared to purchasing a resale property. Builders may have preferred lenders or title companies, which could influence the fees you encounter. Additionally, new construction often involves deposits for utilities and builder-specific warranties that might not be present in a resale transaction.

Negotiating Power and Contingencies

The terms of your purchase agreement can also influence who pays for what. While certain costs are standard, many closing costs are negotiable. For instance, a buyer might negotiate for the seller to cover a portion of their closing costs, especially if they are facing budget constraints or if the market is favorable to buyers. Contingencies, such as a financing contingency or an inspection contingency, can also indirectly impact closing costs if they lead to renegotiations or extended closing periods, potentially incurring additional fees.

Strategies for Managing and Reducing Closing Costs in Texas

While closing costs are an inevitable part of buying a home, there are several strategies buyers and sellers can employ to manage and potentially reduce these expenses. Proactive planning and informed decision-making are key to a more financially manageable closing.

Smart Shopping and Comparison

- Lender Comparison: As mentioned, obtain loan estimates from at least three different lenders. Compare not only interest rates but also origination fees, points, and other lender-specific charges. A small difference in fees can add up to thousands of dollars over the life of the loan.

- Title Company Comparison: Get quotes from several reputable title companies. While they all perform similar services, their pricing can vary. Ensure they are licensed and experienced in Texas real estate.

- Insurance Quotes: Shop for homeowners insurance well in advance of closing. You might find significant savings by comparing policies from different insurance providers.

Negotiation Tactics

- Seller Concessions: Don’t hesitate to negotiate for seller concessions, especially in a buyer’s market. Requesting the seller to pay a portion of your closing costs can significantly reduce your upfront financial burden. This is particularly effective if you’re making a strong offer on a property that has been on the market for a while.

- Reviewing Fees: Carefully review the closing disclosure statement and the settlement statement. Question any fees that seem unusually high or unclear. Sometimes, errors can occur, or there might be opportunities to negotiate the price of certain services.

Strategic Financial Planning

- Budgeting for the Unexpected: Always aim to have a buffer in your budget for closing costs. Unexpected expenses can arise, and being prepared will prevent undue stress.

- Understanding Loan Options: Some loan programs might offer assistance with closing costs, or you might be able to roll certain closing costs into your loan. Discuss these options with your lender to see if they align with your financial situation.

- Prioritizing Owner’s Title Insurance: While often an optional expense for buyers, owner’s title insurance is a valuable investment that protects your equity. Weigh the upfront cost against the potential long-term risk.

By arming yourself with knowledge and employing these strategies, you can navigate the landscape of Texas closing costs with greater confidence, ensuring that your journey to homeownership is as financially sound as it is exciting. This understanding will allow you to fully appreciate your new Texas home, whether it’s a luxurious resort-style property in a planned community or a charming historic home in a quaint Texas town.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.