Navigating the vast and often unpredictable landscape of Texas can be an unforgettable experience. From the vibrant energy of Austin‘s live music scene to the historic charm of San Antonio and the sprawling ranches of the Hill Country, there’s a wealth of attractions and experiences to discover. When planning your travel itinerary, securing the right accommodation is paramount, whether you’re seeking luxurious resorts, cozy apartments, or expansive villas. However, amidst the excitement of exploring local culture, savoring delicious food, and embarking on thrilling activities, it’s crucial to consider an often-overlooked aspect of preparedness: flood insurance.

While the primary focus of your tourism ventures might be on iconic landmarks like the Alamo or the natural beauty of Big Bend National Park, understanding the financial implications of flood damage is a vital component of responsible lifestyle choices, especially for Texas residents and property owners. This guide delves into the world of flood insurance in Texas, aiming to demystify its costs and the factors that influence them, ensuring your peace of mind, whether you’re enjoying a family trip or a budget travel adventure.

Understanding Flood Risks in Texas

Texas, with its diverse geography, faces a significant flood risk. The state’s long coastline along the Gulf of Mexico is susceptible to hurricane-driven storm surges and heavy rainfall. Inland, major rivers and tributaries can overflow their banks after intense storms, affecting communities far from the coast. Even in areas that don’t typically experience flooding, sudden and severe weather events can lead to unexpected inundation.

Coastal Flooding and Hurricanes

The Texas Gulf Coast is a prime example of an area vulnerable to coastal flooding. Cities like Galveston, Corpus Christi, and Houston are on the front lines of potential storm surges from hurricanes. These powerful storms can bring not only strong winds but also massive amounts of water that can inundate coastal communities, causing widespread damage to homes and businesses. The history of Texas is punctuated by devastating hurricanes, such as Hurricane Ike and Hurricane Harvey, which serve as stark reminders of the destructive potential of these weather phenomena. For those living or investing in property in these coastal regions, flood insurance is not just a recommendation; it’s a necessity. The frequency and intensity of tropical storms and hurricanes can influence premiums, as insurers assess the likelihood of such events impacting a property.

Inland Flooding and River Systems

Beyond the coast, Texas‘s extensive river systems present another significant flood risk. Major rivers like the Brazos River, Colorado River, and Trinity River can experience dramatic rises in water levels following prolonged periods of heavy rainfall, often exacerbated by slow-moving weather systems. Communities situated near these rivers, and even those in low-lying areas downstream, can be severely affected by flash floods and riverine flooding. The Hill Country, known for its picturesque landscapes and charming towns like Fredericksburg, can also experience flash floods in its canyons and creek beds during intense thunderstorms. Understanding the specific flood zones and historical flooding patterns in your particular area of Texas is crucial when assessing your flood risk and the potential cost of insurance.

The National Flood Insurance Program (NFIP)

In the United States, flood insurance is primarily offered through the National Flood Insurance Program (NFIP), managed by the Federal Emergency Management Agency (FEMA). While private flood insurance options are becoming more prevalent, the NFIP remains the dominant provider. Properties located in high-risk flood zones (identified on FEMA‘s Flood Insurance Rate Maps, or FIRMs) that are federally backed mortgages are typically required to carry flood insurance. This requirement aims to protect lenders and homeowners from the devastating financial consequences of flood damage. The NFIP sets the framework for how flood insurance is priced and what it covers, influencing the cost for most policyholders in Texas.

Factors Influencing Flood Insurance Costs in Texas

The cost of flood insurance in Texas is not a one-size-fits-all figure. Several key factors contribute to the premium an individual or business will pay. These variables allow insurers to assess the specific risk associated with a particular property and set a premium that reflects that risk.

Property Location and Flood Zone Designation

Perhaps the most significant factor determining flood insurance cost is the property’s location and its designated flood zone. FEMA categorizes areas into different flood risk zones. Properties in Special Flood Hazard Areas (SFHAs), designated as Zone A or Zone V, face a higher risk of flooding and therefore will generally have higher insurance premiums. Zone V areas, typically coastal areas subject to high-velocity wave action, are considered the highest risk. Conversely, properties in lower-risk zones (like Zones C or X) will typically have lower premiums. It’s essential to consult FEMA‘s FIRMs to determine your property’s flood zone designation. This information is publicly available and can be accessed through FEMA‘s website or local planning departments.

Elevation of the Property

Within a given flood zone, the elevation of a property relative to the Base Flood Elevation (BFE) is a critical determinant of cost. The BFE is the anticipated elevation to which floodwater will rise during a 100-year flood event. Properties built at or above the BFE are at a lower risk of experiencing flooding and will typically command lower premiums. Conversely, homes situated below the BFE, particularly those with basements or on lower ground, will face higher insurance costs. Elevation certificates, often completed by a licensed surveyor, provide definitive proof of a property’s elevation and are crucial for accurate flood insurance underwriting.

Type of Coverage and Deductible

The amount of coverage you choose and the deductible you opt for significantly impact your premium. Flood insurance policies typically offer coverage for the building structure and its contents. The more extensive the coverage you select (i.e., higher dwelling coverage limits and contents coverage), the higher your premium will be. Similarly, choosing a lower deductible will result in a higher annual premium, as you’ll be responsible for less of the repair costs out-of-pocket in the event of a flood. Conversely, opting for a higher deductible will reduce your annual premium, but it means you’ll pay more upfront if a claim is filed. Most NFIP policies have a maximum dwelling coverage of $250,000 and contents coverage of $100,000, with higher limits potentially available through private insurers.

Building Characteristics and Age

The characteristics of the building itself also play a role in flood insurance pricing. For example, the type of foundation (e.g., slab, crawl space, raised foundation) can affect flood risk. Properties with basements are generally considered at higher risk. The age of the building can also be a factor, especially if it was built before current flood-resistant building codes were in place. Insurers may also consider the materials used in construction and whether flood mitigation measures, such as elevating utilities or installing backflow valves, have been implemented.

Year of Community’s Flood Map Adoption

The year a community’s flood map was adopted can also influence flood insurance rates. Communities that have adopted and are actively participating in the NFIP‘s Community Rating System (CRS) may offer discounts on flood insurance premiums to their residents. The CRS program encourages communities to implement floodplain management activities that go above and beyond the minimum NFIP requirements, leading to reduced flood risk and savings for policyholders.

Obtaining Flood Insurance Quotes in Texas

Securing flood insurance in Texas involves a few key steps to ensure you get the most accurate pricing and appropriate coverage for your needs. Whether you’re a homeowner in Dallas, a business owner in Houston, or a vacation rental owner in the Texas Hill Country, the process is largely similar.

Working with Insurance Agents

The most common way to obtain flood insurance in Texas is through an insurance agent. Agents licensed to sell flood insurance can help you navigate the options, understand your policy, and find the best coverage for your situation. For NFIP policies, agents will help you complete the necessary applications and submit them to the NFIP‘s servicing agent. They can also guide you through the process of obtaining an elevation certificate if one is needed. Many agents represent multiple insurance companies, allowing them to compare quotes for both NFIP policies and private flood insurance options, potentially offering more competitive pricing and broader coverage.

Understanding NFIP vs. Private Flood Insurance

While the NFIP is the primary source of flood insurance, private flood insurance is increasingly available in Texas. Private policies may offer higher coverage limits than the NFIP, potentially cover additional items (like temporary housing or loss of use), and may have more flexible terms. However, NFIP policies are standardized, ensuring a baseline level of protection and accessibility. It’s advisable to compare quotes and coverage details from both NFIP-backed policies and private insurers to determine the best fit for your individual circumstances and budget. Some private insurers may even offer discounts for properties that have implemented specific mitigation measures.

Average Costs and What to Expect

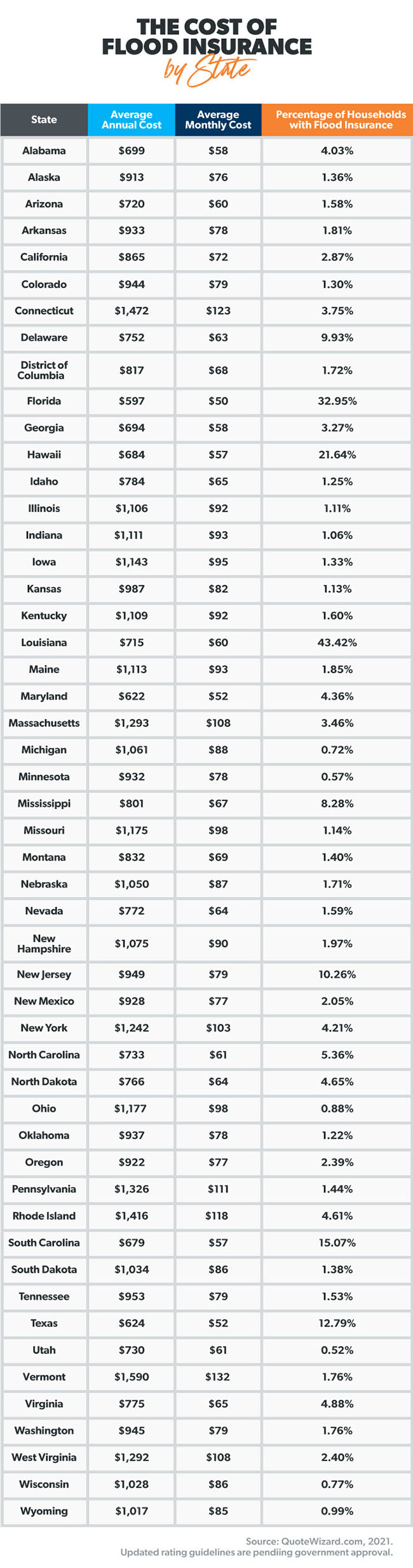

Pinpointing an exact “average” cost for flood insurance in Texas is challenging due to the multitude of influencing factors. However, national averages for NFIP policies often hover around $700-$800 per year. In Texas, this can range from a few hundred dollars for properties in low-risk areas with high elevations to several thousand dollars for homes in high-risk coastal zones or with significant flood history. It’s crucial to get personalized quotes based on your specific property details. Websites and tools are available to estimate flood risk, but a formal quote from an insurance provider will be the most accurate. Remember that flood insurance is typically an annual premium, and the cost is in addition to your standard homeowner’s insurance policy.

Factors Affecting Affordability

Several external factors can also influence the affordability of flood insurance in Texas. Government initiatives aimed at reducing flood risk through improved infrastructure, updated building codes, and floodplain management can lead to lower premiums over time. Conversely, an increase in the frequency or severity of flood events due to climate change could potentially lead to rising insurance costs nationwide. For Texas residents, staying informed about local and state initiatives related to flood mitigation and preparedness can be beneficial. For instance, participating in community programs that aim to reduce flood damage can sometimes translate into insurance savings.

In conclusion, while the allure of Texas‘s diverse landscapes, vibrant cities like Houston and Dallas, and unique cultural offerings is undeniable, ensuring your travel plans and property investments are protected from the potential threat of flooding is a prudent step. By understanding the factors that influence flood insurance costs and diligently obtaining quotes, you can secure the peace of mind needed to fully enjoy everything the Lone Star State has to offer. Whether you’re planning a luxury travel getaway, a budget travel exploration, or simply securing your home, flood insurance is an integral part of responsible lifestyle planning in Texas.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.