California has long captivated imaginations worldwide, drawing in those seeking its unique blend of stunning natural beauty, vibrant culture, and unparalleled lifestyle opportunities. From the sun-drenched beaches of Malibu to the majestic peaks surrounding Lake Tahoe, and the bustling urban centers of Los Angeles and San Francisco, the Golden State offers an incredibly diverse range of places to call home. Whether you’re considering a permanent move, investing in a vacation property, or simply exploring the possibilities of long-term accommodation beyond temporary hotel stays, understanding the intricacies of homeownership here is crucial. And central to that understanding, especially in a state known for both its allure and its distinct challenges, is the cost of home insurance.

Home insurance in California isn’t just a financial safeguard; it’s a fundamental aspect of securing your lifestyle and investment against unforeseen circumstances. While the dream of a California home is often romanticized, the practicalities, particularly concerning insurance premiums, can be complex. This guide delves into the various factors that determine how much you’ll pay, offering insights for both prospective homeowners and those already enjoying the California dream. It’s an essential read for anyone navigating the path to homeownership in one of the world’s most desired destinations.

Understanding California’s Home Insurance Landscape

California’s unique geography and climate, while contributing to its allure as a premier travel and tourism hub, also present specific challenges for homeowners and, consequently, for insurance providers. Unlike many other states, the Golden State faces a higher propensity for certain natural events, which directly impacts the risk assessments and premium calculations for insurers.

Key Factors Influencing Premiums

Several variables come into play when an insurance company calculates your home insurance premium in California. Understanding these can help you anticipate costs and potentially find ways to mitigate them:

- Location, Location, Location: This is perhaps the most significant factor. Homes in areas prone to wildfires, earthquakes, or coastal flooding will invariably have higher premiums. A property nestled in the hills of Santa Barbara, for instance, might face different risks and thus different rates than one in the heart of Sacramento. Proximity to emergency services, such as fire stations and hydrants, also plays a role.

- Home Characteristics: The age of your home, its construction materials (e.g., wood frame versus stucco or brick), its size, and even the type of roof all affect your premium. Older homes may be more expensive to insure due to outdated wiring or plumbing, while homes built with fire-resistant materials might qualify for discounts.

- Claims History: Both your personal claims history and the claims history of the property itself can influence rates. A history of frequent claims, whether yours or a previous owner’s, signals higher risk to insurers.

- Credit Score: In many states, including California, insurers use credit-based insurance scores to help predict the likelihood of future claims. A higher credit score can often lead to lower premiums.

- Coverage Amount and Deductible: The more coverage you purchase (e.g., higher dwelling coverage, more personal property coverage), the higher your premium will be. Conversely, choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) can lower your premium, but means greater immediate expenses if you file a claim.

- Additional Riders or Endorsements: Basic home insurance policies often don’t cover everything. If you add coverage for specific risks like identity theft, valuable art, or home businesses, your premium will increase.

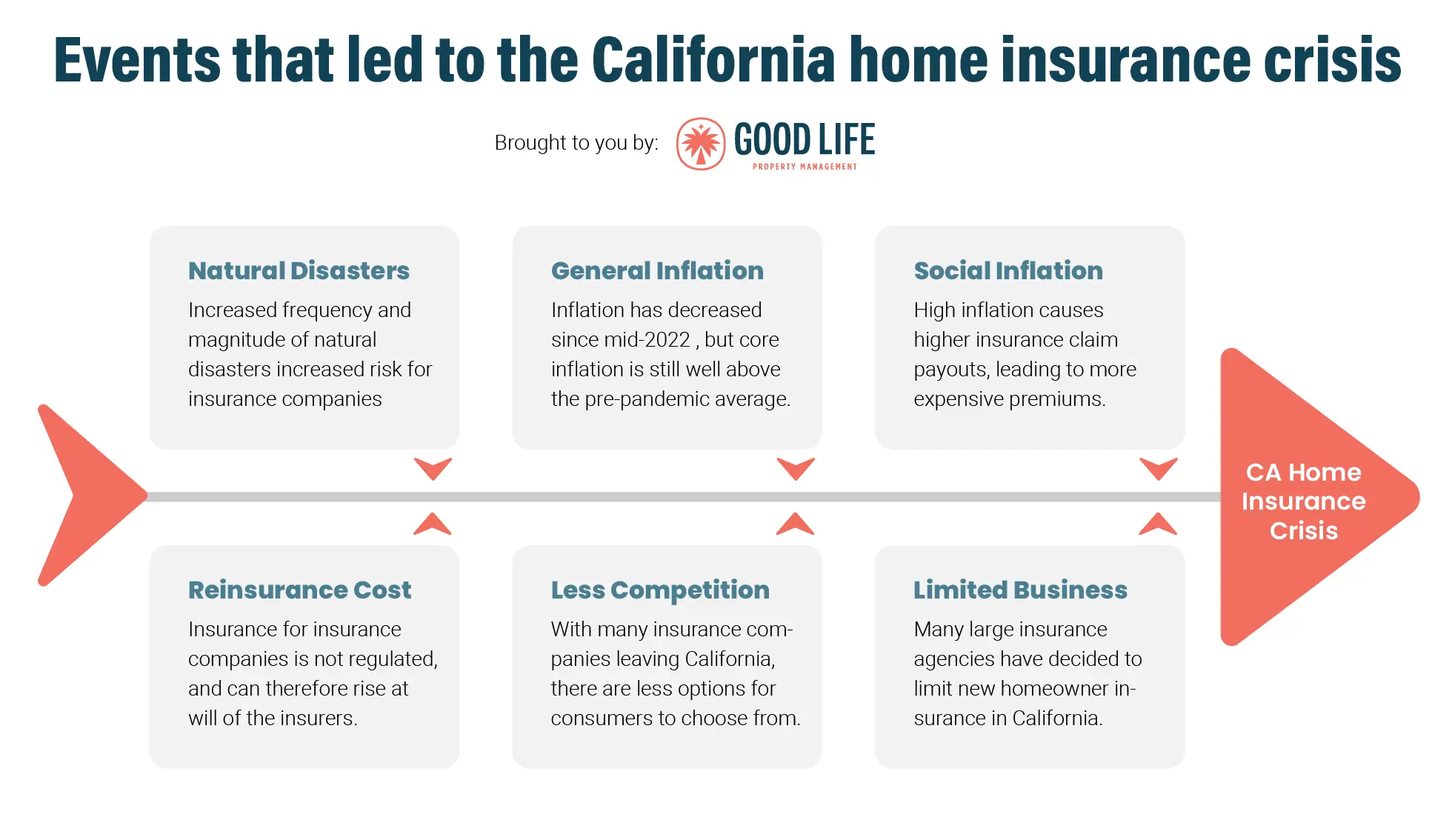

The Impact of Natural Disasters

California’s stunning natural beauty is undeniable, making it a dream for travelers and residents alike. However, this beauty comes with a caveat: a heightened risk of natural disasters. Wildfires and earthquakes, in particular, are defining features of the California landscape and significantly impact the availability and cost of home insurance.

The increasing frequency and intensity of wildfires, especially in areas bordering wildlands (the “wildland-urban interface”), have led some insurers to pull back from offering coverage in high-risk zones. For homeowners in these areas, finding comprehensive coverage can be a challenge, sometimes requiring them to turn to the California FAIR Plan, an insurer of last resort. Earthquakes, while less frequent, pose a significant threat, and standard home insurance policies do not cover earthquake damage. This requires a separate policy, typically from the California Earthquake Authority (CEA) or private insurers, adding another layer to the cost calculation for a true California lifestyle of security.

Other risks, such as mudslides (often following wildfires) and floods (especially in low-lying or coastal areas), also require special consideration. Flood insurance, like earthquake coverage, is usually purchased separately through the National Flood Insurance Program (NFIP) or private providers. These additional coverages, while optional for some, are virtually essential for others, making home insurance a multi-layered financial commitment in the Golden State.

Average Costs and Regional Variations

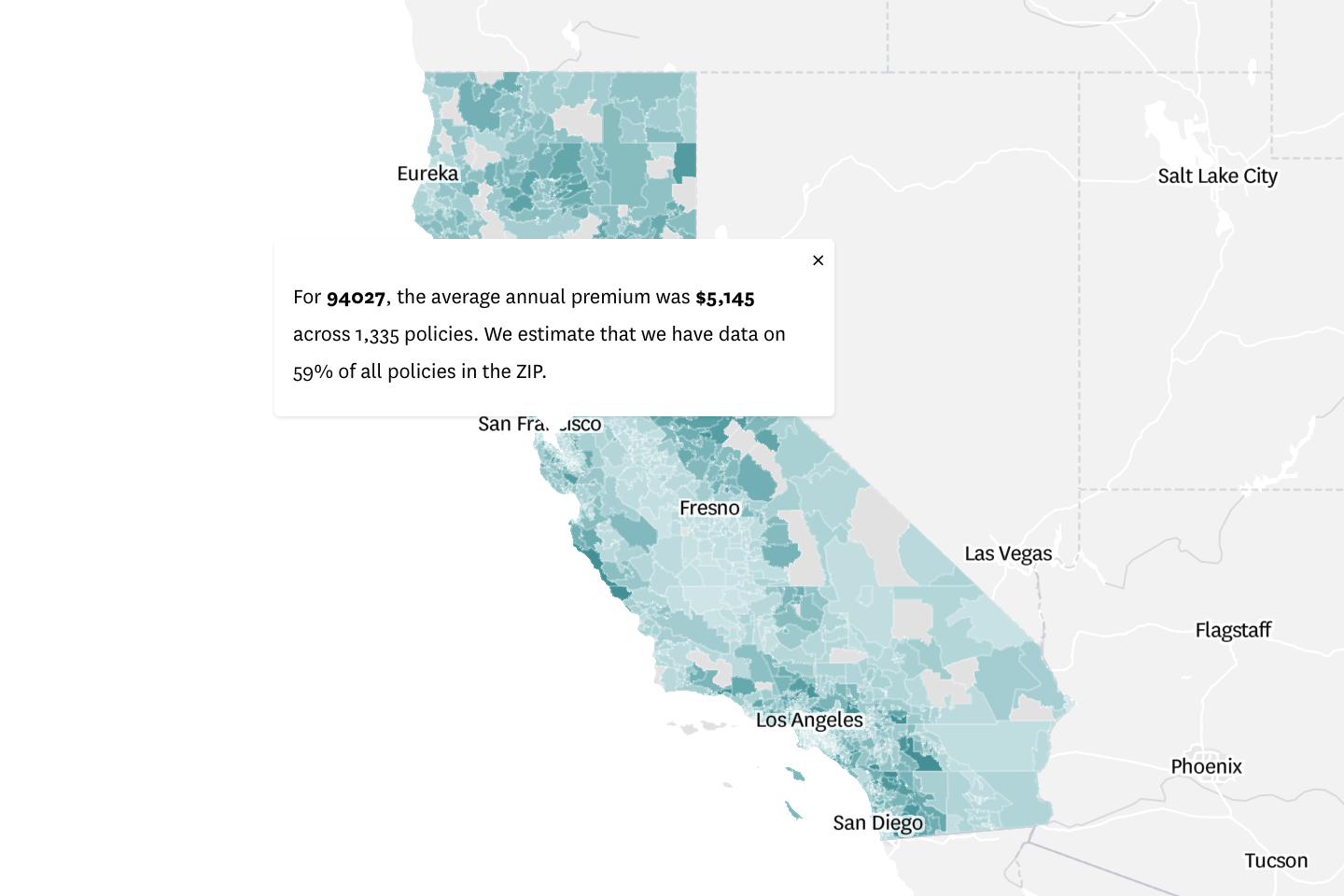

Understanding the factors that influence home insurance is one thing; grasping the actual financial outlay is another. The cost of home insurance in California can vary dramatically, not just year-to-year, but also from one region to another, reflecting the diverse risks and property values across the state.

Breaking Down the Numbers

While exact figures fluctuate based on market conditions, individual property specifics, and policy choices, the average annual cost of home insurance in California generally falls within a broad range. For a standard homeowners policy (HO-3), which covers the dwelling, personal property, liability, and additional living expenses, you might expect to pay anywhere from $1,000 to $2,500 per year, or even more in high-risk areas. This range is a broad estimate and can be significantly impacted by the factors discussed earlier, such as the age of your home, its replacement cost, and your chosen deductible.

It’s crucial to remember that this average often excludes additional coverages like earthquake and flood insurance, which can add hundreds, if not thousands, of dollars annually to your total insurance expenditure. For example, a basic earthquake policy might start around $500-$1,000 per year, but could climb much higher depending on your home’s location, construction, and value. This makes it vital for anyone planning a long-term stay or considering a home purchase to budget comprehensively for their total accommodation costs.

Why Location Matters: From San Francisco to San Diego

The sheer size and geographical diversity of California mean that home insurance costs are far from uniform. The premium for a home overlooking the iconic Golden Gate Bridge in San Francisco will likely differ significantly from a property in the wine country of Napa Valley or a desert retreat near Palm Springs.

- Coastal Regions ([Los Angeles], [San Diego], [Santa Barbara]): Homes along the coast often command higher property values, which means higher dwelling coverage limits and thus higher premiums. They also face unique risks like coastal erosion and potential flooding, making flood insurance a common necessity. The beautiful seaside community of Malibu, for instance, combines high property values with wildfire risk in its hills and potential coastal issues, leading to some of the state’s highest premiums. Even a stay at a luxurious beachfront Pacific Coast Grand Hotel offers a glimpse into the desirability and associated costs of coastal living.

- Urban Centers ([Los Angeles], [San Francisco], [Sacramento]): While typically having good access to emergency services, urban areas often have higher population densities and sometimes older housing stock. They also bear a higher risk of theft and vandalism, which influences premiums. Earthquakes are a concern statewide, but the concentration of infrastructure in cities like San Francisco and Los Angeles means potential for widespread damage.

- Wildland-Urban Interface (e.g., foothill communities, parts of [Orange County]): These areas, often near forests or open spaces, offer a desirable lifestyle close to nature but are at the highest risk for wildfires. Insurers may charge significantly more, or even decline coverage, pushing homeowners to the FAIR Plan. Places near famous landmarks like Yosemite National Park or Sequoia National Park can fall into this category, requiring careful insurance planning even for a quaint Sierra Nevada Lodge in the vicinity.

- Inland Valleys and Desert Regions (e.g., Central Valley, [Death Valley National Park] area, [Palm Springs]): These areas generally experience fewer wildfires than the foothills and less flood risk than the coast. Premiums might be relatively lower compared to high-risk zones, though specific localized risks still apply. A resort like Desert Oasis Spa in a more arid region might have different insurance considerations than one on the coast.

Understanding these regional differences is vital for anyone dreaming of their own slice of the California dream, ensuring that the financial realities align with their chosen lifestyle and destination.

Navigating Specific Insurance Needs

The standard HO-3 policy, while comprehensive for many perils, often falls short in California due to the state’s unique geological and environmental characteristics. Homeowners must be proactive in assessing their specific risks and exploring additional coverage options to truly protect their investment and lifestyle.

Wildfire and Earthquake Coverage

These two perils are perhaps the most critical considerations for California homeowners:

- Wildfire Coverage: While basic home insurance policies typically include some coverage for fire damage, the increasing severity of California wildfires has complicated matters. In high-risk areas, insurers may restrict coverage, charge exorbitant premiums, or even refuse to renew policies. If you’re in a wildfire-prone zone, understanding your policy’s specifics regarding fire is paramount. If traditional insurance is unavailable, the California FAIR Plan acts as a safety net, offering basic fire-only coverage, though it often needs to be supplemented by a “Difference in Conditions” (DIC) policy from a private insurer to provide broader protection for other perils. This dual approach can be more costly and complex than a single comprehensive policy.

- Earthquake Coverage: As mentioned, standard policies do not cover earthquake damage. Given California’s seismic activity, obtaining earthquake insurance is a significant decision for most homeowners. The California Earthquake Authority (CEA) is the largest provider of earthquake insurance in the state, offering policies that cover dwelling, personal property, and additional living expenses. Private insurers also offer earthquake coverage. Premiums depend on your location (proximity to fault lines), home’s construction, and deductible choice. Earthquake deductibles are often high, typically ranging from 5% to 25% of the dwelling coverage amount, meaning you’d pay a substantial sum out-of-pocket before coverage kicks in. For those settling into a Hollywood Hills Villas with its iconic views, this coverage is often a non-negotiable expense.

Additional Protections for Your California Home

Beyond the major perils, other types of coverage can provide peace of mind and protect your California accommodation:

- Flood Insurance: Not included in standard home insurance, flood insurance is essential for homes in designated flood zones. It covers damage from rising water, which can occur from heavy rains, overflowing rivers, or coastal storms. This is especially important for properties near popular attractions or low-lying areas, and areas like Big Sur can experience mudslides after heavy rains. Flood insurance is typically purchased through the National Flood Insurance Program (NFIP) or private carriers.

- Landslide and Mudslide Coverage: Often linked to heavy rainfall on scorched earth after wildfires, mudslides and landslides are typically excluded from standard policies. Some insurers may offer limited coverage as an endorsement, but comprehensive coverage can be difficult to obtain.

- Sewer Backup/Water Backup: This endorsement covers damage from water backing up through sewers or drains. It’s a relatively inexpensive add-on that can save thousands in repair costs.

- Valuables and Collections: If you own expensive jewelry, art, or other high-value items, your standard personal property coverage limits might not be sufficient. A “floater” or “endorsement” can provide specific, higher coverage for these items, crucial for a truly luxurious lifestyle.

- Identity Theft Protection: A growing concern, identity theft coverage can help with the costs and recovery efforts if your identity is stolen.

Considering these specific needs is an integral part of making an informed decision about homeownership in California, ensuring that your investment and your chosen lifestyle are adequately protected against the state’s unique challenges.

Strategies for Reducing Your Home Insurance Costs

While home insurance in California can seem dauntingly expensive, there are proactive steps you can take to mitigate costs without compromising on essential protection. These strategies are not just about saving money; they’re about making your home a safer and more resilient part of your chosen lifestyle.

Discounts and Bundling Opportunities

Many insurers offer a variety of discounts that can significantly reduce your annual premiums:

- Bundling Policies: One of the most common and effective ways to save is to bundle your home insurance with other policies, such as auto insurance. Many major providers, from those offering Travel insurance to those specializing in Accommodation protection, incentivize customers to keep all their policies under one roof. For example, if you’re staying at The Golden State Resort and considering a longer stay, researching combined home and auto plans can lead to substantial savings.

- Safety and Security Features: Installing approved security systems, smoke detectors, carbon monoxide detectors, deadbolt locks, and even sprinkler systems can qualify you for discounts. Insurers view these as measures that reduce the likelihood of claims due to theft or fire.

- Home Updates and Renovation Discounts: Modernizing your home’s systems (electrical, plumbing, HVAC, roofing) can not only improve its safety and efficiency but also lead to lower premiums, as newer systems are less prone to issues.

- Non-Smoker Discount: Some insurers offer a discount if all residents in the household are non-smokers, reducing the risk of fire.

- Loyalty Discounts: Staying with the same insurer for an extended period can sometimes earn you a loyalty discount.

- Higher Deductible: As mentioned earlier, opting for a higher deductible will lower your premium. Just ensure you have the financial capacity to cover that deductible if you need to file a claim.

- Claims-Free Discount: If you haven’t filed a claim for a certain period, some insurers will reward you with a discount.

Always inquire about all available discounts when obtaining quotes. A little research can go a long way in making your California dream more affordable.

Proactive Home Hardening Measures

Beyond discounts, directly reducing your home’s vulnerability to California’s specific risks can make your property more appealing to insurers and potentially lower your premiums, particularly in wildfire-prone areas. These measures contribute to a more secure and sustainable lifestyle.

- Wildfire Hardening: For homes in high-risk zones, implementing “defensible space” guidelines is critical. This involves clearing vegetation around your home, using fire-resistant landscaping, replacing wood shake roofs with fire-resistant materials, installing ember-resistant vents, and using fire-rated doors and windows. Websites like the California Department of Forestry and Fire Protection (CAL FIRE) provide extensive guides on how to harden your home. Some insurers offer discounts or are more willing to provide coverage if these measures are in place.

- Earthquake Retrofitting: For older homes, especially those built before 1979, earthquake retrofitting can significantly reduce damage during a seismic event. This often involves bolting the house to its foundation (“cripple wall bracing”) or strengthening the foundation. While an upfront investment, retrofitting can lead to substantial discounts on earthquake insurance and, more importantly, can protect your home from catastrophic damage. Many local programs or state initiatives, sometimes highlighted in tourism information for historical landmarks, offer grants or rebates for retrofitting.

- Flood Mitigation: If your home is in a flood-prone area, measures like elevating your home, installing backwater valves, or ensuring proper drainage can reduce your flood risk and potentially lower flood insurance premiums.

- Regular Maintenance: Keeping your home well-maintained—addressing leaks promptly, cleaning gutters, and regularly inspecting your roof—can prevent small issues from becoming expensive claims. This proactive approach supports a worry-free lifestyle.

Making Informed Decisions for Your California Lifestyle

Navigating the complexities of home insurance in California is a crucial step towards realizing or maintaining your desired lifestyle in the Golden State. Whether you’re drawn to the allure of Hollywood and its iconic Universal Studios Hollywood, the family fun of Disneyland, or the serene beauty captured from the Griffith Observatory, securing your home is foundational. The state’s unique blend of natural splendor and inherent risks means that a “one-size-fits-all” approach to insurance simply won’t suffice.

The key to finding the right coverage at a reasonable price lies in thorough research and diligent comparison. Don’t settle for the first quote you receive. Reach out to multiple insurance providers, including both major national carriers and local independent agents who specialize in the California market. They can offer tailored advice and help you navigate the nuances of specific regional risks, from the brushfire dangers near Big Sur to the seismic activity prevalent across the state.

Carefully review each policy’s coverage limits, deductibles, exclusions, and endorsements. Understand what is and isn’t covered, especially concerning wildfires, earthquakes, and floods. Ask specific questions about how your home’s unique characteristics and location impact your premiums. For instance, a beautiful Ocean Breeze Suites style home might have specific coastal considerations, while a Wine Country Inn in Napa Valley could face different, localized concerns.

Homeownership in California is an investment in a dream, a commitment to a particular way of life. By taking the time to understand the nuances of home insurance, exploring all available discounts, and implementing proactive hardening measures, you can protect that investment and ensure that your California lifestyle remains secure and enjoyable for years to come. It’s about building a future, not just finding a place to stay.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.