California, a land of sun-kissed beaches, towering redwoods, vibrant cities, and diverse landscapes, is a dream destination for many travelers and a coveted place to call home. From the bustling streets of Los Angeles and the iconic vistas of San Francisco to the serene wine country of Napa Valley and the majestic beauty of Lake Tahoe, the Golden State offers an unparalleled lifestyle. However, for those considering a long-term stay, investing in a vacation rental, or even making the ultimate commitment of purchasing property here, a crucial question arises: “How much is house insurance in California?”

Understanding the nuances of homeowner’s insurance in California is essential, not just for property owners but also for anyone contemplating extended accommodation options. It’s an integral part of protecting your investment and ensuring peace of mind, allowing you to fully embrace the California lifestyle without undue financial worry. This guide delves into the factors influencing insurance costs, average premiums, and strategies to navigate the unique insurance landscape of this iconic state, weaving in insights relevant to travel, tourism, and lifestyle enthusiasts.

Understanding Homeowner’s Insurance in the Golden State

Homeowner’s insurance in California isn’t just a legal requirement for most mortgage holders; it’s a vital safeguard for your most significant asset. Whether you’re a long-time resident, a recent transplant, or an investor eyeing the lucrative vacation rental market in destinations like Palm Springs or near the Disneyland Resort, understanding your policy’s components is paramount.

A standard homeowner’s insurance policy typically covers several key areas:

- Dwelling Coverage: This protects the physical structure of your home, including the roof, walls, and foundation, against perils like fire, windstorms, and vandalism. In a state prone to natural disasters, this is particularly critical.

- Personal Property Coverage: This covers your belongings inside the home, such as furniture, electronics, clothing, and other valuables. It often includes coverage for items even when they are not on your property, a boon for frequent travelers.

- Liability Coverage: This protects you financially if someone is injured on your property or if you accidentally cause damage to someone else’s property. This is especially relevant if you entertain guests or operate a short-term rental.

- Additional Living Expenses (ALE): Should your home become uninhabitable due to a covered loss, ALE covers costs like hotel stays, meals, and other necessary expenses while your home is being repaired. For those who frequently host, or who themselves rely on their home as a base for their travel adventures, this can be an invaluable safety net.

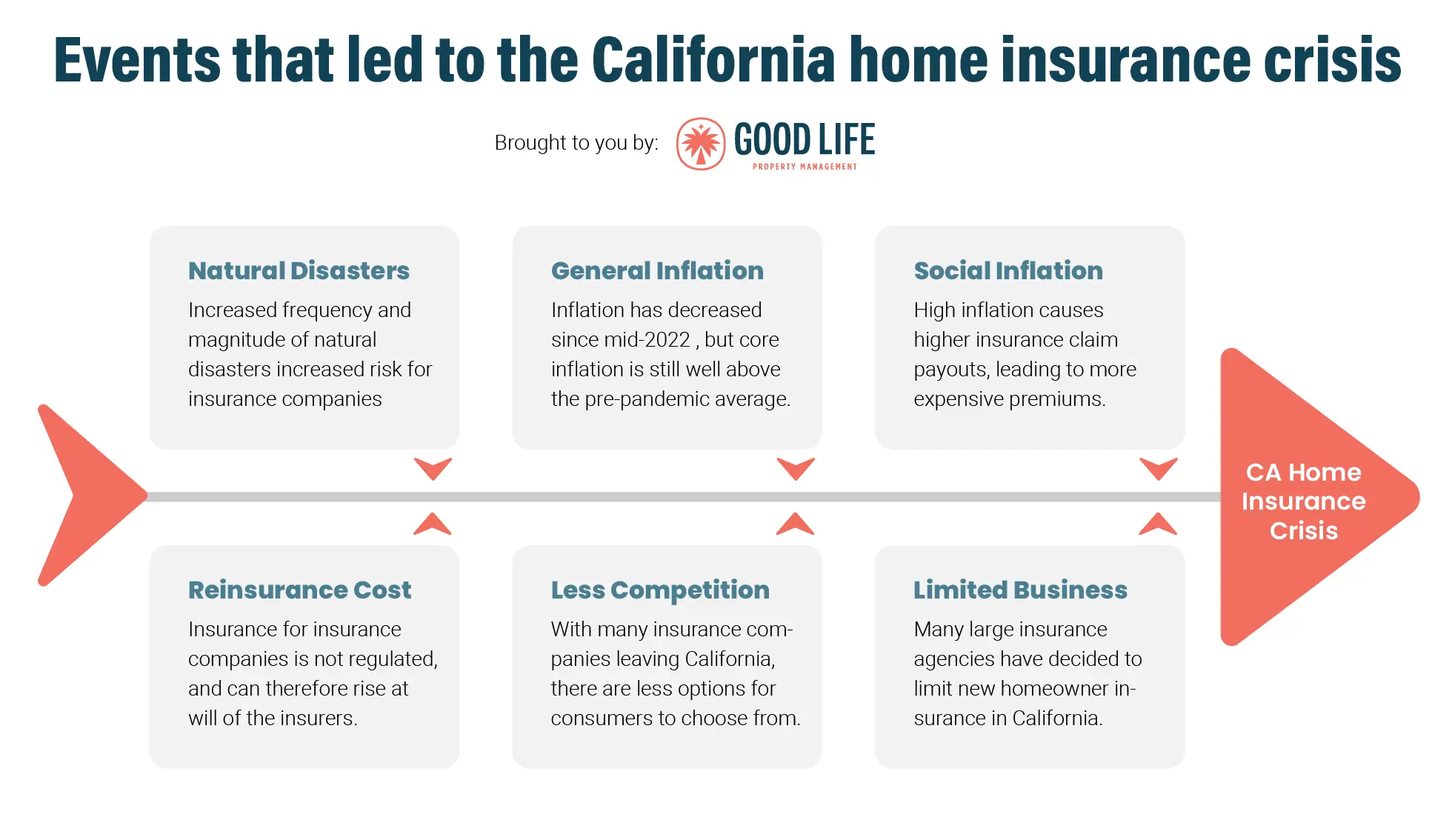

What makes California’s insurance landscape distinct are its inherent natural risks. The state is renowned for its stunning geography, but this beauty comes with challenges like wildfires, earthquakes, and, in some areas, floods. While standard policies cover many perils, specific endorsements or separate policies are often necessary for these California-specific risks, directly impacting the overall cost of protecting your home and your chosen lifestyle.

Factors Influencing Insurance Premiums in California

The cost of house insurance in California is far from uniform. It’s a complex calculation influenced by a myriad of factors, making it crucial for any prospective homeowner or long-term renter to delve into the specifics. These elements directly relate to the value, location, and inherent risks associated with your chosen accommodation in the Golden State.

Location, Location, Location

Perhaps no factor impacts California home insurance premiums more significantly than where your property is situated. The state’s diverse topography means risks vary wildly from one region to another.

- Coastal Areas: Homes along the Pacific Ocean in places like Malibu or Santa Barbara may face higher risks of coastal erosion and, in some cases, flood damage, requiring additional flood insurance.

- Wildfire-Prone Zones: Many desirable California destinations, including parts of the Sierra Nevada Mountains, the Hollywood Hills near Los Angeles, and rural areas around Redding and Chico, are in high-risk wildfire areas. Insuring properties here can be significantly more expensive, with some homeowners even struggling to find traditional coverage.

- Earthquake Zones: While no part of California is entirely free from earthquake risk, proximity to major fault lines, particularly in urban centers like San Francisco, San Jose (part of Silicon Valley), and Orange County, will influence the need and cost for earthquake insurance.

- Urban vs. Rural: Generally, densely populated urban areas might have different risk profiles for theft or vandalism compared to sprawling rural properties. However, rural properties are often more exposed to natural elements.

Your chosen location for a permanent residence or a vacation getaway directly dictates a significant portion of your insurance outlay.

Property Characteristics and Value

The specifics of your home itself play a crucial role in premium calculations.

- Reconstruction Cost: Insurers are primarily concerned with the cost to rebuild your home, not its market value. Larger, more complex homes, especially those with custom features often found in luxury travel accommodations, will naturally cost more to insure.

- Age and Construction Materials: Older homes, particularly historic properties or those built with materials less resistant to modern hazards, may command higher premiums. Newer homes built with fire-resistant materials or up-to-date seismic retrofitting can often qualify for discounts.

- Safety Features: Modern plumbing, electrical systems, alarm systems, smart home technology, and even features like fire sprinklers can help reduce premiums by mitigating risks.

- Roof Condition: The age and material of your roof are critical, as it’s often the first line of defense against weather.

For those investing in California real estate as part of their lifestyle or for potential tourism income, these characteristics are key considerations when evaluating both the property and its associated costs.

Coverage Levels and Deductibles

The choices you make regarding your policy’s specifics also directly impact your premiums.

- Higher Coverage Limits: Opting for higher dwelling, personal property, or liability limits will increase your premium, offering greater protection for expensive homes or valuable possessions common in a luxury lifestyle.

- Lower Deductibles: A deductible is the amount you pay out-of-pocket before your insurance kicks in. Choosing a lower deductible means the insurance company pays more for smaller claims, so your premium will be higher. Conversely, a higher deductible typically leads to a lower premium. Finding the right balance depends on your financial comfort level and risk tolerance.

Natural Disaster Risks

As touched upon earlier, California’s unique geological and climatic conditions make natural disaster risks a paramount factor.

- Wildfire Risk: This is arguably the most impactful factor currently. As climate patterns shift, more areas, including popular destinations like Pasadena and parts of San Diego County, are being reclassified as high or very high wildfire risk zones. This can lead to non-renewal of policies by traditional insurers, forcing homeowners to seek coverage from the more expensive California Fair Access to Insurance Requirements (FAIR) Plan or the surplus lines market.

- Earthquake Risk: While earthquake insurance is almost always a separate policy, the underlying risk influences the overall cost of living and insuring property in California.

- Flood Risk: While less pervasive than fire or earthquake, properties in flood zones, such as those near rivers in the Central Valley or low-lying coastal areas, will require separate flood insurance, usually through the National Flood Insurance Program (NFIP).

These specific risks add layers of complexity and cost to securing adequate accommodation insurance in the state, making it a critical aspect of financial planning for any homeowner or long-term visitor.

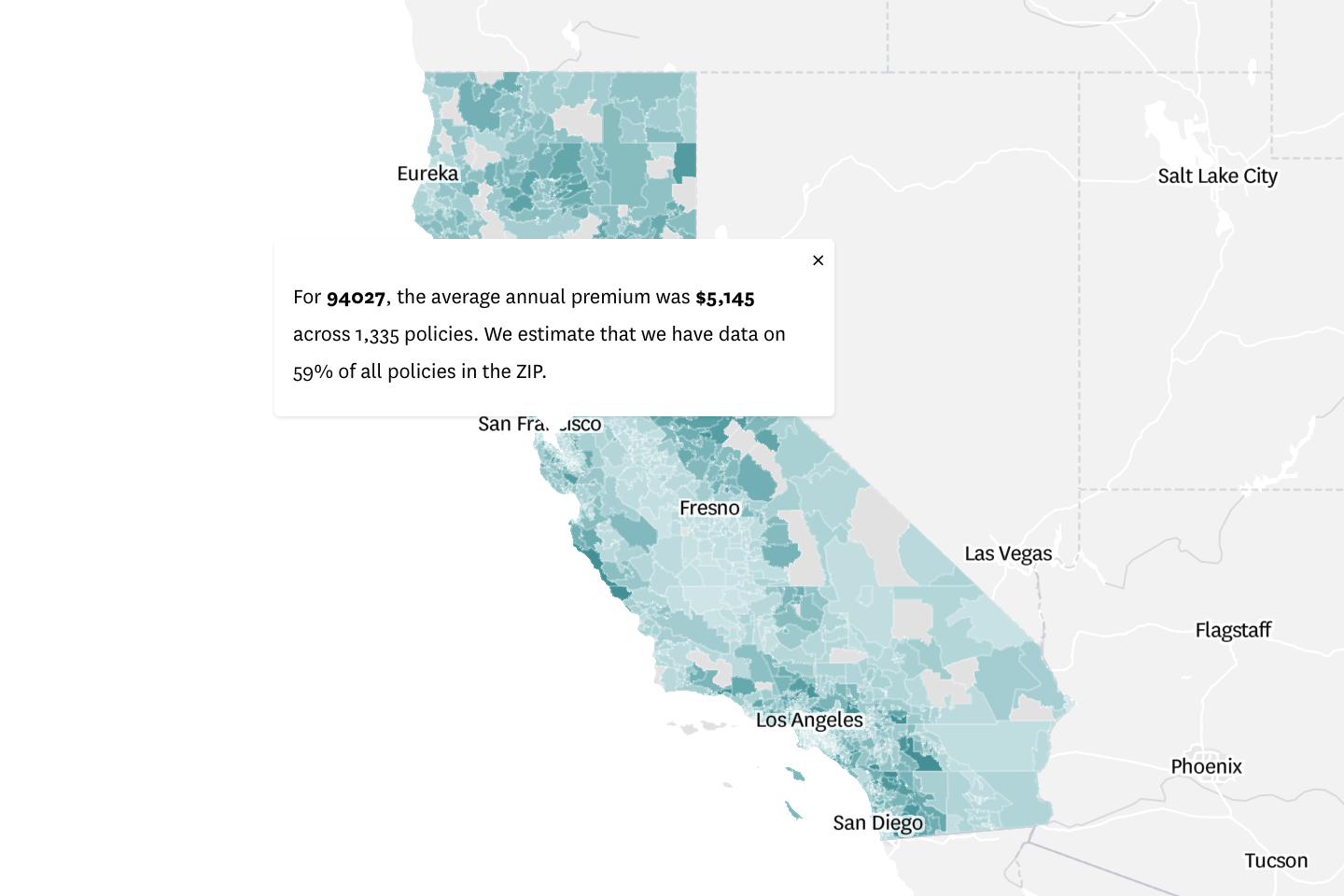

Average Costs and Variances Across California

Determining an exact average cost for house insurance in California can be misleading due to the extreme variances discussed above. However, general estimates suggest that a standard homeowner’s policy might range anywhere from $1,000 to $3,000 annually. This figure can significantly increase, however, when additional policies for specific perils like wildfires or earthquakes are included.

Consider these rough regional variations:

- Inland Empire/Central Valley: Generally, areas like Sacramento or parts of the Central Valley might see lower base premiums than coastal regions, assuming they are not in a high wildfire or flood zone.

- Los Angeles/Orange County: Urban and suburban areas here can have moderate base premiums, but costs can skyrocket in desirable wildfire-prone communities like Malibu or the Hollywood Hills.

- San Francisco Bay Area: While earthquake risk is prominent, base homeowner’s insurance might be competitive, but adding earthquake coverage will increase the overall spend.

- Wildfire Interface Zones: Areas bordering wildlands, regardless of their specific location (e.g., parts of Napa Valley, regions near Yosemite National Park, or Sequoia National Park, mountain communities near Lake Tahoe or Joshua Tree National Park), often face the highest premiums and the greatest challenges in securing traditional coverage. It’s not uncommon for annual costs in these areas to exceed $5,000, $10,000, or even more, especially when relying on the FAIR Plan and supplemental coverage.

These costs are a crucial component of the overall financial picture for anyone considering living or investing in California, whether for a permanent residence, a vacation home, or an income-generating rental for tourism. It impacts everything from property affordability to the feasibility of a chosen lifestyle.

Beyond Standard Homeowner’s: Special Considerations for California Properties

For many California homeowners, a standard policy simply isn’t enough. The state’s unique risks necessitate additional, often separate, insurance coverages that are critical for complete protection and peace of mind. These considerations are vital for securing your investment, especially if you’re venturing into the accommodation market for travelers or exploring different lifestyle options within the state.

Wildfire Insurance

Given the increasing frequency and intensity of wildfires, particularly across recent years, wildfire insurance has become a paramount concern for many in California. While standard homeowner’s policies often include some fire coverage, this can be limited, especially in high-risk areas. Many traditional insurers are pulling back from offering comprehensive coverage in these zones, leading to a reliance on alternative options:

- California FAIR Plan: This is a state-mandated program providing basic fire coverage to properties that cannot obtain insurance in the voluntary market. It’s often a last resort and typically covers only fire, vandalism, and limited other perils, meaning homeowners usually need to purchase a “Difference in Conditions” (DIC) policy from a separate insurer to cover other standard homeowner’s risks like liability and theft.

- Surplus Lines Market: This consists of non-admitted insurers who offer coverage for higher-risk properties at higher prices. They are not regulated by the state in the same way as admitted carriers, offering more flexibility but often at a greater cost.

Understanding your wildfire risk, especially if your property is near popular landmarks or attractions that border wildlands like the Golden Gate Bridge Park area or Big Sur, is non-negotiable.

Earthquake Insurance

Earthquakes are a fact of life in California, and standard homeowner’s insurance explicitly excludes earthquake damage. For comprehensive protection, a separate earthquake policy is essential. These policies are often offered by the California Earthquake Authority (CEA) or by private insurers.

- High Deductibles: Earthquake policies typically come with very high deductibles, often 10% to 25% of the dwelling coverage, meaning you’d pay a substantial amount out-of-pocket before coverage kicks in.

- Cost Variation: Premiums vary based on your home’s age, construction, location relative to fault lines, and the policy’s deductible and coverage limits. For example, a home in a seismic hot zone like San Francisco will have different rates than one in a less active area.

For anyone committed to the California lifestyle, especially those with a long-term investment, earthquake insurance is a prudent, if often costly, consideration.

Flood Insurance

While not as widespread a concern as fire or earthquake, flood risk is a reality for properties located in designated flood plains, near rivers, or along the coast. Standard homeowner’s insurance does not cover flood damage. Flood insurance is typically purchased through the National Flood Insurance Program (NFIP), though some private flood insurance options are becoming available. This is particularly relevant for properties in low-lying areas or those impacted by storm surges.

Vacation Rentals and Investment Properties

For those who see their California property as more than just a home—perhaps a lucrative venture in the tourism or accommodation sector—specific insurance considerations apply. If you plan to rent out your property on platforms like Airbnb or VRBO, a standard homeowner’s policy is likely insufficient.

- Landlord Policy (Dwelling Fire): This covers the dwelling and provides liability for landlords, but typically less coverage for personal property.

- Specific Short-Term Rental Insurance: Some insurers offer specialized policies designed for short-term vacation rentals, addressing the unique risks associated with frequent guest turnover, such as increased liability and potential property damage.

- Commercial Coverage: For properties that operate more like a business (e.g., a multi-unit property or a very active rental), commercial property insurance may be required.

Protecting your investment in the thriving California tourism market means ensuring your insurance policy accurately reflects how the property is used, safeguarding your lifestyle and financial stability.

Smart Strategies for Managing Insurance Costs in California

Navigating the complexities and costs of house insurance in California can seem daunting, but several smart strategies can help homeowners manage their premiums while maintaining adequate protection. These tips are valuable for anyone embracing the California lifestyle, whether as a permanent resident or an investor in the state’s vibrant accommodation sector.

- Shop Around Aggressively: This is perhaps the most crucial step. Insurance rates vary significantly between carriers. Obtain quotes from multiple insurers – both national and regional providers – and don’t forget to explore options within the surplus lines market if you’re in a high-risk area. Using independent insurance agents who work with multiple carriers can simplify this process.

- Bundle Policies: Many insurance companies offer discounts if you bundle multiple policies, such as your home and auto insurance. If you have a car in California, inquiring about bundling options for your home and vehicle can lead to substantial savings.

- Increase Your Deductible: As mentioned earlier, opting for a higher deductible will lower your annual premium. Just ensure you have sufficient funds set aside to cover that deductible should you need to file a claim. This is a common strategy for individuals focused on budget travel in their finances, extending to their home expenses.

- Improve Home Safety and Resilience: Investing in home improvements that mitigate risks can often lead to discounts.

- Wildfire Hardening: For homes in wildfire-prone areas, measures like creating defensible space, using fire-resistant landscaping, installing fire-resistant roofing and siding, and upgrading to dual-pane windows can make a significant difference. Some insurers offer specific wildfire mitigation credits.

- Seismic Retrofitting: For earthquake-prone areas, retrofitting an older home to make it more resistant to seismic activity can potentially lower earthquake insurance premiums or at least make your home more insurable.

- Security Systems: Installing a monitored home security system, smoke detectors, and carbon monoxide detectors can earn you discounts.

- Smart Home Technology: Leak detection systems and smart fire alarms can prevent costly claims and demonstrate a proactive approach to home maintenance.

- Maintain a Good Credit Score: In California, like many other states, insurers often use credit-based insurance scores to help determine premiums. A higher credit score can translate into lower insurance costs, reflecting a responsible financial lifestyle.

- Regularly Review Your Policy: Life changes, and so do your insurance needs. Review your policy annually with your agent. Ensure your coverage limits are appropriate for the current cost of rebuilding your home and replacing your belongings. You might discover opportunities to adjust coverage or apply for new discounts.

- Understand Your Risks and Coverage: Don’t just pay the bill; understand what you’re paying for. Knowing the specifics of your policy, including what’s covered and what’s excluded (especially concerning natural disasters), empowers you to make informed decisions and fill any gaps in coverage.

By proactively employing these strategies, homeowners and property investors in California can better manage their insurance expenses, ensuring their valuable assets are protected without overspending. This diligence contributes to a more secure and enjoyable California lifestyle, whether you’re living in a cozy bungalow in San Diego or managing a luxury villa for travelers near the Universal Studios Hollywood theme park.

In conclusion, understanding “How Much Is House Insurance In California?” is far more complex than a simple number. It’s a nuanced calculation influenced by location, property specifics, chosen coverage, and the unique natural risks inherent to the Golden State. For anyone seeking to embrace the vibrant California lifestyle, whether as a permanent resident, a vacation homeowner, or an investor in the lucrative tourism market, comprehensive and appropriate home insurance is not just an expense; it’s an indispensable investment in peace of mind. By diligently researching, comparing options, and understanding the specific needs of your property, you can secure the right protection, allowing you to fully enjoy all the incredible experiences California has to offer, free from undue financial worry related to your accommodation.