California, often referred to as the Golden State, beckons with its diverse landscapes, vibrant cities, and unparalleled lifestyle. From the sun-kissed beaches of San Diego to the tech hubs of Silicon Valley and the wine country allure of Napa Valley, it’s a dream destination for many – not just for travel, but for living, investing, and establishing a long-term base. Whether you’re considering purchasing a vacation home in Palm Springs, an investment property in Los Angeles, or simply curious about the economic landscape that underpins the region’s appeal, understanding property taxes in California is paramount. This intricate system can significantly impact your financial planning, whether you’re a prospective homeowner, a real estate investor, or even just a traveler observing the local economy. Delving into the nuances of California’s property tax structure reveals a unique framework shaped by historical legislation, local funding needs, and the ever-evolving real estate market.

Unpacking California’s Property Tax Framework

The property tax system in California is distinctly different from many other states, primarily due to a landmark piece of legislation. This system directly affects everything from the cost of accommodation for tourists to the viability of long-term investments for those considering a lifestyle change in this popular state.

The Bedrock: Proposition 13 and its Legacy

At the heart of California’s property tax structure lies Proposition 13, a voter-approved initiative passed in 1978. Its impact cannot be overstated, as it fundamentally altered how property values are assessed and taxed. Prior to Proposition 13, property taxes were subject to significant annual increases, leading to widespread public outcry. The initiative introduced two key provisions that continue to define the system today. Firstly, it capped the maximum ad valorem tax on real property at 1% of its full cash value. This means that, for most properties, the base property tax rate is around 1% of its purchase price or the value at which it was last officially reassessed. Secondly, and perhaps even more significantly, Proposition 13 limited the annual increase in assessed value to a maximum of 2% or the rate of inflation, whichever is lower. This provision offers long-term property owners a substantial protection against soaring property tax bills, especially in areas with rapidly appreciating real estate markets like San Francisco or Orange County. However, it also means that new buyers inherit a property with a freshly assessed value, often resulting in a significantly higher tax bill compared to their long-term neighbors. This dynamic creates a distinct financial consideration for anyone looking to invest in a vacation property, relocate for work, or consider a retirement home in the Golden State.

The Calculation: Base Rate, Assessed Value, and Annual Adjustments

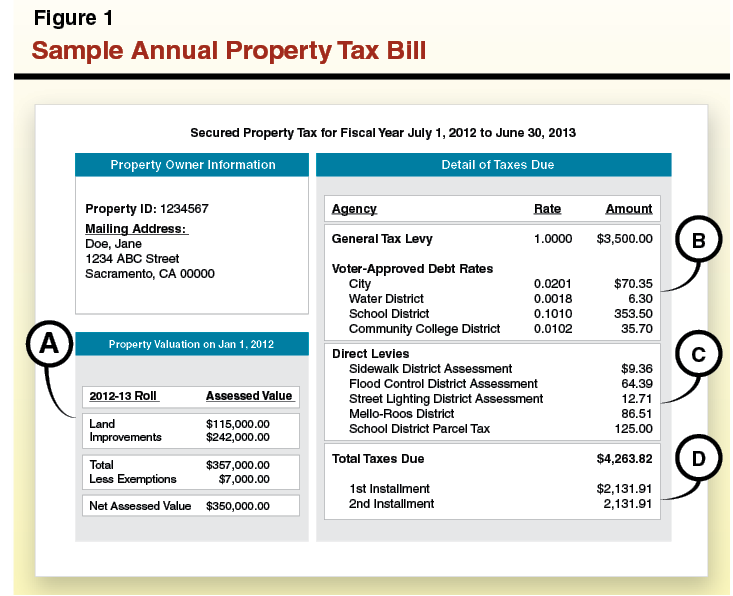

So, how is your property tax bill actually calculated in California? It begins with the assessed value of your property. For newly purchased properties, this is typically the purchase price. For existing properties, it’s the 1975 market value adjusted annually by no more than 2% or the consumer price index, whichever is lower, until a change in ownership or new construction occurs. Once the assessed value is established, the base tax rate of 1% is applied. However, this isn’t the final figure. Various locally approved bonds and special assessments are added on top of this 1% base. These additional levies fund specific local services and infrastructure projects, such as schools, parks, libraries, police, and fire departments. These can include school bonds, infrastructure improvements, or Mello-Roos Community Facilities Districts, which we will explore further. As a result, the “effective” property tax rate, encompassing the 1% base and all additional local assessments, can range from approximately 1.1% to 1.5% or even higher, depending on the specific location within California. For someone considering a long-term stay or purchasing a rental property, understanding these local variations is crucial for accurate financial forecasting.

Factors Shaping Your Property Tax Bill Across California

The cost of property tax in California isn’t a uniform figure across the entire state. A multitude of factors contribute to the final amount you’ll pay, ranging from geographical location and property type to specific local funding initiatives. These variations are particularly important for travelers exploring long-term accommodation options, investors seeking rental income, or individuals considering a lifestyle move to the Golden State.

The Geographic Divide: Urban vs. Rural & Desirable Locales

One of the most significant determinants of your property tax bill, beyond the foundational rules of Proposition 13, is the property’s location. While the base 1% tax rate applies statewide, the “full cash value” (which serves as the assessed value for new purchases) varies dramatically across California’s diverse regions. Properties in highly desirable urban centers and popular tourist destinations naturally command higher prices, leading to higher assessed values and consequently, larger tax bills. For instance, a luxury condominium in San Francisco or a beachfront home in Malibu will have a significantly higher assessed value than a comparable-sized property in a more rural or less demand-driven area of the Central Valley.

Consider the contrast between a property in bustling Los Angeles County, home to attractions like Hollywood and Santa Monica, and a home in a quieter northern California county. The sheer market demand, proximity to world-class landmarks, and concentration of amenities drive property values up in places like Beverly Hills, Laguna Beach, or near the vibrant Gaslamp Quarter in San Diego. This isn’t just about the initial purchase price, but also about the cumulative impact of that higher base value on the 1% tax, even with Proposition 13’s protections. For those dreaming of a vacation rental near Disneyland or a long-term stay overlooking Lake Tahoe, understanding these localized value dynamics is crucial for budgeting their overall cost of ownership. The prestige and desirability associated with certain locations, often highlighted in travel guides and lifestyle blogs, directly translate into higher property valuations and thus, higher tax obligations.

Beyond the Base: Special Assessments and Mello-Roos Districts

While Proposition 13 limits the general property tax rate, it does allow for additional property-based fees and special assessments. These are levied by local governments and agencies to fund specific services or infrastructure projects that benefit the properties within a defined geographic area. Common examples include assessments for schools, parks, libraries, public safety, street lighting, storm drains, and even local transportation improvements. These additional levies are typically fixed amounts or a percentage of the assessed value, added on top of the 1% base tax.

Perhaps the most significant of these are Mello-Roos Community Facilities Districts. Established under the Mello-Roos Community Facilities Act of 1982, these districts allow local governments to finance public improvements and services in developing areas where traditional funding sources are insufficient. If you purchase a new home, particularly in master-planned communities across areas like Orange County, the Inland Empire, or growing suburbs around San Diego and Los Angeles, there’s a good chance it might be within a Mello-Roos district. These taxes fund items such as new roads, schools, utility systems, and sometimes even police and fire services. Mello-Roos taxes can be substantial and can remain in effect for many years, often adding thousands of dollars annually to a property tax bill. Unlike the base property tax, Mello-Roos taxes can sometimes increase by more than 2% per year, or they might be a flat amount indexed to inflation, depending on the bond’s terms. Prospective buyers, especially those looking at newer developments for residential use or as vacation rentals, must diligently inquire about the presence and cost of Mello-Roos assessments, as they can significantly impact the overall cost of ownership and thus, the viability of an investment.

Property Tax Considerations for Travelers, Investors, and Long-Term Stays

For those captivated by California’s allure, property taxes extend beyond a mere civic duty; they become a critical component of travel budgeting, investment strategy, and lifestyle planning. From a temporary visitor pondering the cost of their vacation to a seasoned investor eyeing a portfolio expansion, the property tax landscape in the Golden State has far-reaching implications.

Investing in a California Dream: Vacation Homes and Rental Properties

Many individuals are drawn to California not just to visit, but to own a piece of it. Whether it’s a chic bungalow in Palm Springs for weekend getaways, a coastal retreat in Santa Barbara, or a rental unit near popular attractions like Universal Studios Hollywood, the dream of owning a vacation home or investment property is compelling. However, property taxes are a foundational cost that must be meticulously factored into any financial model. For an investment property, the annual property tax directly impacts the net operating income and, consequently, the return on investment. A higher property tax bill means less profit from rental income, potentially influencing rental rates and the overall competitiveness of the property in the market.

For those purchasing a second home for personal use and occasional rentals, the property tax adds a significant fixed cost, regardless of how often the property is occupied or rented out. Consider a luxury villa in Napa Valley or a cabin near Yosemite National Park; the property tax, combined with maintenance, insurance, and HOA fees, can represent a substantial annual expense. New buyers, especially, should be aware that their property taxes will be based on the current market value (their purchase price), which can be considerably higher than what long-term residents pay for similar properties due to Proposition 13’s protections. This dynamic is a crucial differentiator when evaluating the long-term financial commitment of owning property in a high-demand area. Prudent investors and future vacation homeowners will conduct thorough due diligence on estimated property taxes, including any special assessments or Mello-Roos fees, to ensure their California dream doesn’t become a financial burden.

The Indirect Impact on Tourism and Accommodation Costs

While tourists rarely directly pay property taxes, the system in California has an indirect but tangible impact on the cost of travel and accommodation. Hotels, resorts, and vacation rental operators (like those running Airbnb properties) are all subject to property taxes on their commercial or residential holdings. These taxes represent a significant overhead cost for businesses in the hospitality sector. Naturally, these costs are passed on to the consumer in the form of higher room rates, rental fees, and other charges.

In popular destinations such as San Francisco, where commercial property values are exceptionally high, hotels face substantial property tax bills. This contributes to San Francisco’s reputation as one of the most expensive cities for accommodation in the United States. Similarly, luxury resorts in Carmel-by-the-Sea or boutique hotels near iconic landmarks like the Golden Gate Bridge or Hearst Castle factor their property tax burden into their pricing strategies. For travelers planning extended stays or looking for budget-friendly options, understanding that property taxes indirectly influence prices can help in comparing costs across different regions or types of accommodation. A smaller, family-run guesthouse in a less glamorous but charming town might have a lower property tax burden than a Grand Hyatt Hotel in downtown Los Angeles, allowing them to offer more competitive rates. This intricate link demonstrates how local fiscal policies can subtly shape the economic landscape experienced by every visitor to California.

Navigating Exemptions and Resources for Property Owners

While California’s property tax system can seem complex, particularly with its Proposition 13 rules and various assessments, there are pathways for eligible property owners to reduce their tax burden. Understanding these exemptions and knowing where to find reliable information is crucial for maximizing your investment or managing the costs of your California lifestyle.

Key Exemptions and Tax Relief Programs

For homeowners residing in their primary residence, the Homeowner’s Exemption is the most common form of tax relief. This exemption reduces the assessed value of a primary residence by $7,000, which translates to a saving of approximately $70 to $80 on the annual property tax bill, depending on the local combined tax rate. While this may seem modest, it’s a consistent saving for owner-occupiers. To claim this, homeowners must file an application with their county assessor’s office.

Beyond the Homeowner’s Exemption, California offers several other programs, primarily targeted at specific demographics or circumstances:

- Senior Citizen Property Tax Postponement Program: This allows eligible seniors (aged 62 or older, blind, or disabled) with limited household income to postpone payment of property taxes on their primary residence. The state then places a lien on the property, and the taxes become due when the property is sold, changes ownership, or the homeowner moves.

- Disabled Veterans’ Exemption: Eligible disabled veterans and their unremarried spouses may receive a significant reduction in their assessed property value, potentially leading to substantial tax savings. The amount of the exemption varies based on the veteran’s disability rating and income.

- Intercounty Base Value Transfer: Under certain conditions (Proposition 60/90 and Proposition 19), homeowners over 55, or those severely disabled, can transfer the Proposition 13 protected assessed value of their primary residence to a replacement home of equal or lesser value anywhere in the state. This is particularly relevant for seniors looking to downsize or move closer to family while retaining their low property tax base.

Understanding eligibility requirements and application procedures for these programs can provide considerable financial relief, making long-term residency or investment in California more manageable.

Staying Informed: Essential Resources for California Property Owners

Navigating the intricacies of property tax requires reliable information. The primary resource for any property owner or prospective buyer in California is the County Assessor’s Office in the county where the property is located. Each county maintains its own records, assessment rolls, and processes exemption applications. Their websites typically offer property search tools to look up assessed values and tax bills, detailed information on exemptions, and contact information for questions. For broader understanding of the state’s tax laws, the California State Board of Equalization (BOE) website provides comprehensive resources, publications, and guidance on property tax laws and regulations. Consulting a qualified real estate agent or a tax professional specializing in California real estate is also highly recommended, especially when considering a major purchase or investment property, to ensure all relevant tax implications are thoroughly understood and accounted for.

In conclusion, property tax in California is a multifaceted system, deeply influenced by Proposition 13 and local assessments. While it can be a significant cost for homeowners and investors, especially in high-value areas like Los Angeles and San Francisco, understanding its components and available exemptions is key to successful financial planning in the Golden State. For travelers, recognizing its indirect impact on accommodation costs helps shed light on the economic realities of visiting one of the world’s most desirable destinations.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.