For anyone considering a move or extended stay in the vibrant Texas, understanding renters insurance is crucial. Beyond finding the perfect rental, this often-overlooked safeguard protects your belongings and financial well-being, offering peace of mind as you settle into the Lone Star State. Whether in Houston, Dallas, Austin, or San Antonio, costs vary, but the value is consistently high. This guide explores what renters insurance entails in Texas, factors influencing its price, and how to secure optimal coverage.

Understanding Renters Insurance in the Lone Star State

Renters insurance, often a lease requirement and always a smart choice, protects you and your possessions from unforeseen circumstances. Unlike homeowner’s insurance, which covers the dwelling’s structure, renters insurance focuses on what’s inside your rented space and your personal liability. For those who frequently travel or lead a mobile lifestyle, this coverage is particularly critical, safeguarding valuable electronics, travel souvenirs, or essential business equipment that accompany extended stays or relocations.

A typical renters insurance policy in Texas offers three primary types of coverage:

- Personal Property Coverage: This protects your belongings against specified perils such as fire, smoke, theft, vandalism, certain types of water damage (e.g., burst pipes, not floods), and severe weather like windstorms or hail – a significant consideration in Texas. Whether your camera gear, wardrobe, or documents are damaged or stolen, this coverage helps replace them. Policies typically offer Actual Cash Value (depreciated value) or Replacement Cost Value (new replacement cost), with the latter offering superior protection for a slightly higher premium.

- Personal Liability Coverage: This component protects you financially if you’re found legally responsible for bodily injury or property damage to someone else within your rental or anywhere globally. For instance, if a guest slips in your Austin apartment or your pet causes injury, liability coverage can help cover medical expenses, legal fees, and potential settlements.

- Additional Living Expenses (ALE) Coverage: Also known as Loss of Use coverage, ALE is invaluable if a covered loss (like a fire) renders your home uninhabitable. It helps cover temporary housing (e.g., a hotel suite), meals, and other increased living costs while your rental is repaired or you find a new one, preventing significant disruption, especially for travelers in temporary accommodation.

Understanding these foundational elements highlights why renters insurance is an indispensable part of living in or exploring Texas.

Factors Influencing Renters Insurance Costs Across Texas

The cost of renters insurance in Texas is not fixed but dynamically calculated by various factors. These elements determine your annual premium, from your chosen location to your coverage level. For those new to the state or considering a move, understanding these variables helps in making informed decisions and potentially lowering rates.

Geographic Variations: City to City

Location is a primary determinant of renters insurance premiums. Texas’s vastness means risks vary dramatically by region.

- Urban vs. Rural: Premiums in densely populated urban centers like Houston or Dallas may be slightly higher due to increased crime rates (theft, vandalism) compared to rural areas. However, this varies by specific zip code.

- Weather Risks: Texas is no stranger to severe weather. Areas along the Gulf Coast face hurricane risks, while North Texas sees frequent hailstorms and tornadoes. Insurers factor these localized weather patterns into pricing, alongside building specifics and proximity to known flood zones (note: flood insurance is separate).

Personal Coverage Choices and Deductibles

Your policy choices directly impact its cost.

- Coverage Limits: Higher personal property coverage (e.g., $50,000 vs. $30,000) or liability limits (e.g., $300,000 vs. $100,000) will increase your premium.

- Deductible: This is your out-of-pocket payment before insurance kicks in. A higher deductible (e.g., $1,000 instead of $500) lowers your annual premium, but ensure you can afford it in an emergency.

- Endorsements and Riders: For particularly valuable items like high-end jewelry or specialized photography equipment, standard policies might not suffice. Adding specific endorsements or “riders” increases your premium but provides dedicated, higher coverage.

Your Personal Profile: Credit, Claims, and More

Insurers also assess individual risk factors.

- Credit Score: In Texas, insurers use a credit-based insurance score to gauge financial responsibility. A higher credit score typically translates to lower rates, as statistically, individuals with better credit are less likely to file claims.

- Claims History: Multiple past claims may classify you as a higher risk, leading to elevated premiums. A clean claims history often results in more favorable rates.

- Type of Dwelling: The age, construction type, and safety features of your rental unit influence rates. A modern apartment with fire suppression and controlled access might qualify for lower rates than an older home lacking such features.

- Pet Ownership: While not always impacting the base premium directly, certain dog breeds might be excluded from liability coverage or require an additional endorsement due to higher perceived risk.

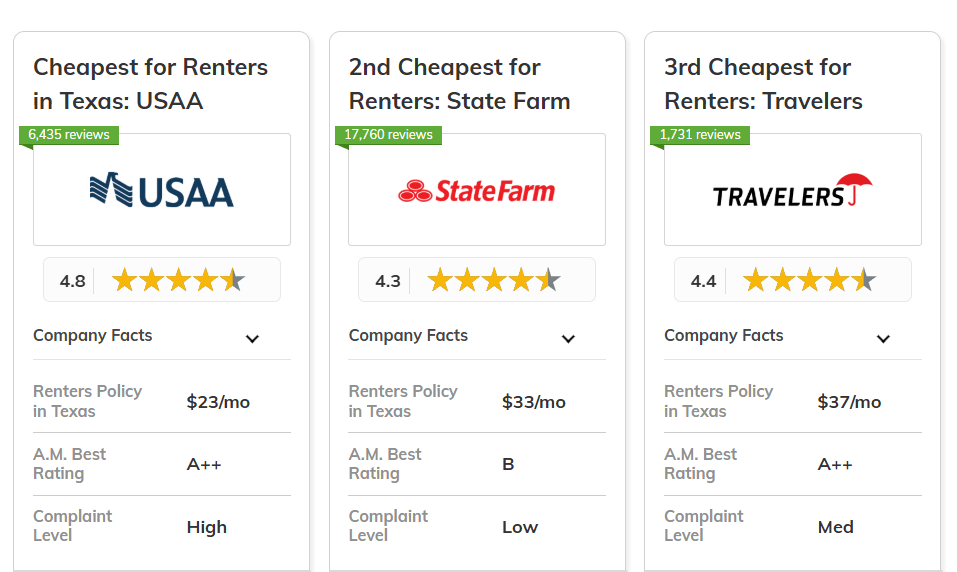

Average Renters Insurance Costs in Major Texas Cities

While precise costs are individualized, general estimates can provide a useful benchmark for budgeting, especially if you’re exploring long-term accommodation options in Texas’s prominent urban centers.

A Snapshot of Urban Centers

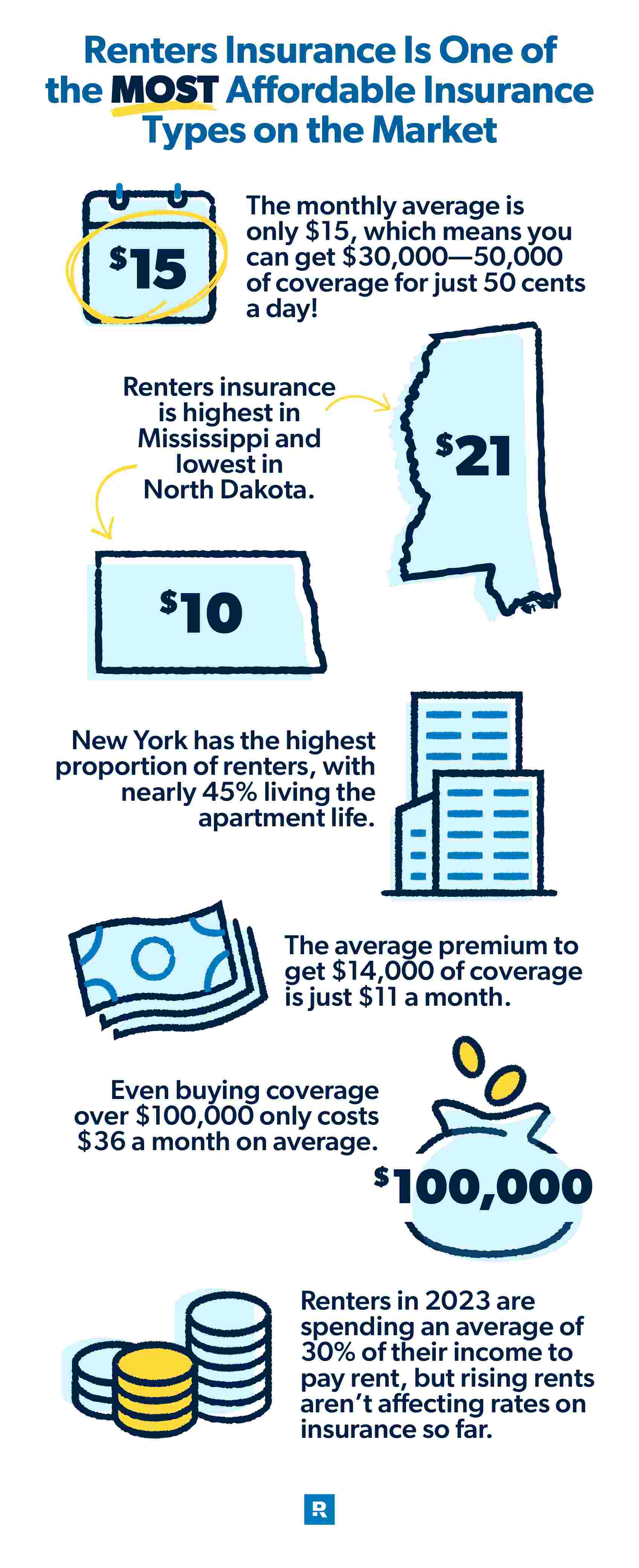

Renters insurance in Texas is generally affordable, often ranging from $150 to $250 per year for a standard policy with $20,000-$30,000 in personal property coverage and $100,000 in liability. This translates to roughly $12 to $20 per month – a small price for substantial protection.

Here’s a look at specific cities:

- Houston: As the largest city, Houston’s unique risks—from higher crime rates to hurricane threats from the Gulf Coast—often lead to premiums at the higher end, typically $180 – $280 annually. This coverage is essential for those basing here to explore attractions like Space Center Houston.

- Dallas: The economic powerhouse of North Texas, Dallas experiences severe weather like hailstorms and tornadoes. Its urban environment also contributes to varying crime rates. Renters might expect to pay $170 – $270 per year. For those relocating for business or enjoying the Dallas Arts District, securing renters insurance is a smart move.

- Austin: Known for its vibrant culture and tech scene, Austin generally sees moderate average premiums, around $150 – $240 annually. While not immune to storms, it’s less prone to direct hurricane impacts than Houston or the extreme hail of North Texas.

- San Antonio: Rich in history and home to the iconic Riverwalk, San Antonio often has a lower cost of living, reflected in its renters insurance rates, typically $140 – $230.

- Fort Worth: Often considered Dallas’s neighbor, Fort Worth shares similar weather but can offer slightly lower rates depending on the neighborhood, usually $160 – $250 annually.

- El Paso: In West Texas with a desert climate, El Paso generally experiences fewer severe weather events. This often leads to some of the lowest renters insurance rates in Texas, potentially around $130 – $200 per year.

- Plano: This prosperous Dallas suburb often has lower crime rates and well-maintained properties, contributing to competitive premiums, likely $160 – $240.

Always obtain multiple personalized quotes to get the most accurate cost estimate for your situation.

Smart Strategies to Save on Your Texas Renters Insurance

While renters insurance is already an affordable protection, several strategies can further reduce your premium without compromising essential coverage. These tips are especially useful for budget-conscious travelers planning extended stays or anyone optimizing lifestyle expenses in Texas.

Bundling and Discounts: Maximizing Your Savings

Many insurers offer attractive discounts.

- Bundle Policies: One of the most effective ways to save is to “bundle” renters insurance with another policy, typically auto insurance. Inquire if your current auto provider offers renters insurance and a multi-policy discount. Major insurers like State Farm, Allstate, Geico, Progressive, Farmers, and USAA are known for such bundles, often saving 10-20% on combined premiums.

- Home Security Discounts: Installing safety features like smoke detectors, carbon monoxide detectors, deadbolt locks, or a full home security system can qualify you for discounts.

- Claim-Free Discount: A clean claims history often leads to lower premiums.

- Non-Smoker Discount: Some providers offer discounts for non-smokers due to reduced fire risk.

- Paid-in-Full Discount: Paying your annual premium upfront instead of monthly can often earn a discount.

Adjusting Coverage and Deductibles Wisely

Fine-tuning your policy specifics can also lead to savings.

- Review Personal Property Value: Take a realistic inventory of your belongings. Avoid over-insuring items you no longer own or under-insuring valuable new acquisitions. Aim for Replacement Cost Value coverage, but adjust the total amount to accurately reflect your current possessions.

- Increase Your Deductible: Opting for a higher deductible (e.g., $1,000 or $2,500) will lower your premium. Ensure you have sufficient emergency funds to cover this higher deductible if you need to file a claim.

- Avoid Unnecessary Endorsements: Only add endorsements for items not adequately covered by your base policy or that you truly own. Regularly review your policy to ensure it matches your current needs.

Regular Reviews and Comparison Shopping

The insurance market is competitive and rates change.

- Shop Around Annually: Don’t settle for the first quote. Obtain quotes from at least three to five providers, as rates can vary significantly for the same coverage.

- Review Your Policy Annually: Your life and insurance needs change. Annually review your policy with your agent, considering new acquisitions, changes in living situation, or improved credit score.

Beyond the Basics: Renters Insurance for the Modern Traveler & Resident

In a state as expansive and diverse as Texas, where travel experiences range from exploring the vast wilderness of Big Bend National Park and Guadalupe Mountains National Park to savoring the culinary delights of South Padre Island or the historic depth of San Antonio’s Riverwalk, the concept of ‘home’ can be fluid. For many, Texas is a temporary residence for business, a long-term base for exploring regional attractions, or a new lifestyle chapter. Renters insurance plays a vital, often understated, role in supporting this modern lifestyle.

Consider the digital nomad or business professional who calls an apartment in Austin or Dallas home for several months. Their livelihood depends on laptops, cameras, and portable electronics, essential for work or passion. A standard renters policy typically covers these items not just within the rented dwelling but also when temporarily away from home, anywhere in the world. This means if your camera gear is stolen from a locked car during a weekend trip to Big Bend National Park, your renters insurance might still offer protection. This extended coverage provides invaluable peace of mind, allowing you to focus on adventures and work without constant worry.

Furthermore, for those embracing long-term travel, perhaps in a serviced apartment or extended-stay rental while exploring Texas, renters insurance ensures a stable foundation. It protects against the unexpected, safeguarding personal property investment and offering liability protection in unfamiliar environments. Whether you’re a student making a temporary move, a family on an extended vacation exploring various Texas landmarks, or an individual embarking on a new career, renters insurance is an affordable necessity that complements the adventurous spirit of exploring a new place.

It aligns perfectly with a lifestyle focused on experiences rather than anxieties. Knowing your financial liability is covered and personal items are protected means you can fully immerse yourself in local culture, explore every attraction, and enjoy every destination without the underlying stress of potential loss or unexpected expenses. In essence, renters insurance is not merely a policy; it’s an enabler of freedom and security, allowing you to truly embrace your Texas journey, whether short-term exploration or long-term residency.

By understanding the cost drivers and leveraging smart saving strategies, you can secure robust protection for your home and belongings, ensuring your Texas experience is as smooth and worry-free as possible. It’s a small monthly investment for substantial security, allowing you to fully enjoy the rich culture, diverse landscapes, and vibrant cities of the Lone Star State.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.