New York – a name that conjures images of towering skyscrapers, bustling avenues, iconic landmarks, and a vibrant cultural tapestry. Whether you dream of a long-term stay in a Manhattan apartment, a thrilling adventure exploring the diverse neighborhoods of Brooklyn and Queens, or a strategic business visit to the United States‘ financial capital, the allure of the Empire State is undeniable. From the historic grandeur of the Statue of Liberty to the artistic wonders of the Metropolitan Museum of Art and the tranquil beauty of Central Park, New York offers an unparalleled lifestyle and an endless list of experiences.

However, amidst the excitement of planning your travel, accommodation, and activities, one crucial aspect often gets overlooked: health insurance. In the United States, healthcare costs can be extraordinarily high, and an unexpected illness or injury can quickly turn an dream trip or relocation into a financial nightmare. For anyone considering an extended stay, moving to, or even just visiting New York for a significant period, understanding how to navigate the private health insurance market is not just recommended, it’s essential. This comprehensive guide aims to demystify the process, ensuring you can enjoy all that New York has to offer with peace of mind.

Understanding New York’s Healthcare Landscape for Travelers and Residents

The healthcare system in the United States is complex, and New York State operates within its unique regulatory framework, influenced by federal policies. For both transient visitors and new residents, grasping the fundamentals is the first step toward securing adequate coverage. The sheer volume of world-class hospitals and medical facilities in New York City is impressive, but access to these services without proper insurance can be prohibitively expensive.

The Importance of Private Health Insurance in the Big Apple

Imagine strolling through Times Square, enjoying a Broadway show, or taking in the panoramic views from the Empire State Building, only to be struck by a sudden illness or accident. Without health insurance, even a routine doctor’s visit can cost hundreds of dollars, while an emergency room visit or a hospital stay could easily run into thousands or even tens of thousands. For international travelers, short-term travel insurance policies might offer some emergency coverage, but they often come with limitations on pre-existing conditions, duration of stay, and the types of treatments covered. They are rarely sufficient for those planning to reside in New York for several months or longer, or for individuals needing ongoing medical care.

Private health insurance, on the other hand, provides a robust safety net. It covers a wide range of medical services, from preventive care and specialist visits to prescription medications and hospitalization. This comprehensive coverage is critical for anyone hoping to truly immerse themselves in the New York lifestyle without the constant worry of potential medical debt. It’s an investment in your well-being, allowing you to focus on discovering charming Greenwich Village cafes, exploring the vibrant arts scene, or advancing your career, knowing that your health needs are covered.

Key Healthcare Regulations and Mandates in New York

The healthcare landscape in New York State is significantly shaped by the federal Affordable Care Act (ACA), often referred to as Obamacare. The ACA introduced mandates for individuals to have health insurance, established health insurance marketplaces, and implemented consumer protections like preventing insurers from denying coverage due to pre-existing conditions. For residents of New York, the primary avenue for purchasing individual and family health insurance is the New York State of Health (NYSoH) Marketplace. This online platform allows individuals and small businesses to compare health plans, determine eligibility for financial assistance, and enroll in coverage.

Eligibility for plans through the New York State of Health typically requires legal residency in New York State and citizenship or a qualifying immigration status. This means that temporary visitors, tourists, or those on certain non-immigrant visas might not be eligible for all plans or subsidies offered on the Marketplace. However, even if not eligible for subsidies, individuals can often still purchase plans directly from private insurers or through the Marketplace at full price. Understanding these eligibility nuances is crucial, especially for expats, digital nomads, or students planning an extended stay in New York. It’s also important to note the annual “Open Enrollment Period,” typically in the fall, when most individuals can sign up for new plans or change existing ones. Special Enrollment Periods exist outside this window for those experiencing qualifying life events, such as moving to New York, getting married, or having a child.

Navigating Your Options: Types of Private Health Insurance Plans

Once you understand the ‘why,’ the next step is to tackle the ‘what’ and ‘how.’ The private health insurance market in New York offers a variety of plan types, each with different structures, benefits, and cost implications. Choosing the right plan involves understanding these distinctions and aligning them with your personal health needs, lifestyle, and budget.

Different Plan Structures: HMOs, PPOs, EPOs, and POS Plans

The alphabet soup of health insurance plans can be daunting, but understanding the basic differences is key to making an informed decision:

- HMO (Health Maintenance Organization): These plans typically require you to choose a Primary Care Provider (PCP) within the plan’s network. Your PCP then acts as a gatekeeper, referring you to specialists when needed. HMOs often have lower monthly premiums and out-of-pocket costs but offer less flexibility, as out-of-network care is generally not covered, except in emergencies. This structure might be suitable for those who prefer a coordinated approach to care and don’t anticipate needing frequent specialist visits outside a specific network.

- PPO (Preferred Provider Organization): PPO plans offer more flexibility. You don’t usually need a PCP referral to see a specialist, and you can see doctors and hospitals both in and out of the plan’s network. However, staying within the network will result in lower costs. PPOs typically have higher premiums than HMOs but appeal to individuals who value choice and flexibility, perhaps those who travel frequently within the United States or have specific preferred doctors.

- EPO (Exclusive Provider Organization): EPOs are similar to PPOs in that you don’t need a PCP referral to see a specialist, but they are “exclusive” – meaning they generally won’t cover out-of-network care, similar to an HMO. They can be a good middle ground, offering a wider choice of specialists without referrals, but still requiring you to stay within their network to avoid high costs.

- POS (Point of Service): POS plans combine elements of both HMOs and PPOs. You often choose a PCP who then refers you to specialists within the network. However, you also have the option to go out of network for care, though you will pay more for it. This offers a balance between managed care and flexibility.

For someone relocating to New York City, especially if they haven’t established a local doctor, the flexibility of a PPO or EPO might be appealing, allowing them to explore various providers. For budget-conscious individuals or those happy to have their care coordinated, an HMO could be a cost-effective option.

Understanding Key Insurance Terms: Premiums, Deductibles, Copayments, and Coinsurance

Beyond the plan structure, several financial terms dictate your out-of-pocket expenses:

- Premium: This is the fixed amount you pay monthly (or annually) to keep your health insurance coverage active, regardless of whether you use medical services. It’s like a subscription fee.

- Deductible: This is the amount you must pay out of your own pocket for covered medical services before your insurance plan starts to pay. For example, if you have a $2,000 deductible, you pay the first $2,000 in medical costs each year before your insurer contributes. Once met, your plan begins to pay for a percentage of your medical bills.

- Copayment (Copay): This is a fixed amount you pay for a covered healthcare service after you’ve met your deductible. For instance, a $30 copay for a doctor’s visit or a $15 copay for a prescription.

- Coinsurance: This is your share of the cost for a covered health service, calculated as a percentage (e.g., 20%) of the allowed amount for the service, after you’ve met your deductible. If your coinsurance is 20% and the allowed amount for a service is $100, you’d pay $20.

Understanding how these elements interact is crucial for managing your healthcare budget. A plan with a lower premium often comes with a higher deductible, and vice-versa. Travelers or new residents who are generally healthy might opt for a higher deductible plan to keep premiums low, while those with ongoing medical needs might prefer a plan with a higher premium but lower deductible and out-of-pocket maximum.

Special Considerations for Expats, Digital Nomads, and Long-Term Visitors

For individuals whose primary purpose in New York is temporary residency, work on specific visas, or remote work as a digital nomad, the standard New York State of Health Marketplace options might not always be the best fit or even accessible.

- International Health Insurance: Many international insurance providers offer plans specifically designed for expats or global citizens. These plans can provide coverage not only in New York but also internationally, which is ideal for those with a truly nomadic lifestyle or who frequently travel outside the United States. These plans can often be more flexible regarding enrollment periods and eligibility requirements than domestic ACA-compliant plans.

- Travel Medical Insurance (Long-Term): While distinct from comprehensive health insurance, long-term travel medical insurance can be a suitable option for stays from a few months up to a year or two. These plans are designed to cover unexpected medical emergencies, accidents, and sometimes acute onset of pre-existing conditions. They usually don’t cover routine care or preventive services but are essential for catastrophic events. When exploring New York’s vast offerings, from the historic Brooklyn Bridge to the vibrant markets, having this safety net is invaluable.

- Student Health Plans: If you’re coming to New York for academic purposes, your educational institution likely offers a student health insurance plan or requires you to have adequate coverage. These plans are often comprehensive and tailored to the needs of students, including access to campus health services.

Always scrutinize the policy details, especially the geographic scope of coverage, limitations, exclusions, and emergency evacuation clauses, which can be particularly relevant for international individuals.

The Step-by-Step Guide to Purchasing Private Health Insurance in New York

With a foundational understanding of the New York healthcare system and available plan types, you’re ready to embark on the purchasing journey. This process involves careful assessment, diligent research, and informed decision-making to secure the best coverage for your unique situation.

Assessing Your Needs and Budget

Before diving into plan comparisons, take an honest inventory of your healthcare needs and financial capabilities.

- Duration of Stay: Are you planning a short-term visit (less than 6 months), a medium-term relocation (6 months to 2 years), or a permanent move? This significantly impacts the type of plan you should consider.

- Health Status: Are you generally healthy with no pre-existing conditions, or do you have chronic conditions that require ongoing medication or specialist care? Consider your age, lifestyle, and any planned medical procedures.

- Desired Level of Coverage: Do you need comprehensive coverage for all eventualities, or are you primarily looking for catastrophic coverage in case of emergencies?

- Provider Preferences: Do you have specific doctors or hospitals you wish to use? Remember, New York City is home to world-renowned medical centers, but ensuring your plan covers them is critical.

- Financial Situation: How much can you comfortably afford for monthly premiums? What is your comfort level with potential out-of-pocket costs (deductibles, copays, coinsurance) if you need medical care? Balance lower premiums with higher out-of-pocket risks. Your budget for luxury travel or long-term accommodation might need to account for health insurance costs.

By honestly evaluating these factors, you can narrow down your options and avoid paying for unnecessary coverage while ensuring you’re not underinsured. This self-assessment is as important as choosing the right hotel in Manhattan or deciding on a budget for exploring Wall Street and Rockefeller Center.

Where to Shop: The New York State of Health Marketplace and Private Brokers

For most eligible residents and those with qualifying immigration statuses, the New York State of Health (NYSoH) Marketplace is the primary resource. It provides a centralized platform to:

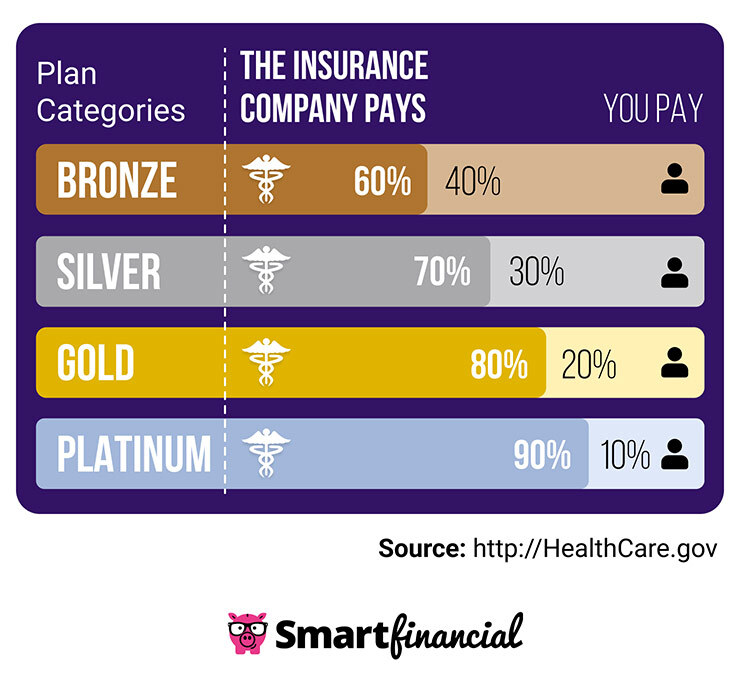

- Compare Plans: View various plans from different insurers, categorized by metal tiers (Bronze, Silver, Gold, Platinum) which indicate the percentage of costs the plan covers.

- Check for Financial Assistance: Determine if you qualify for tax credits (subsidies) that can significantly reduce your monthly premiums, or for Medicaid/Child Health Plus.

- Enroll: Directly enroll in a chosen plan during Open Enrollment or a Special Enrollment Period.

For individuals not eligible for NYSoH, or for those seeking specialized international plans, private insurance companies and brokers are invaluable resources.

- Direct from Insurers: Major insurance carriers operate in New York and offer plans directly. This might be suitable if you know exactly which company and plan you want.

- Insurance Brokers/Agents: Licensed brokers specialize in navigating the complex insurance market. They can assess your needs, compare plans from multiple providers (including international options), explain intricate policy details, and help you enroll. They are especially helpful for expats, non-residents, or those with unique healthcare requirements, as they can find plans outside the standard Marketplace offerings. Their services are typically free to you, as they are compensated by the insurance companies.

Remember to conduct your search during the Open Enrollment Period if possible, unless you qualify for a Special Enrollment Period due to a life event like moving to New York or a change in visa status.

What to Look For in a Plan: Provider Networks, Benefits, and Customer Service

As you compare plans, keep these critical factors in mind:

- Provider Networks: Crucially, check if your preferred doctors, specialists, or hospitals are “in-network.” Out-of-network care, especially with HMOs and EPOs, can be very costly. If you have specific medical needs, ensure the plan’s network includes relevant specialists or facilities. Use the insurer’s online provider directory.

- Covered Benefits: Review the Summary of Benefits and Coverage (SBC) for each plan. It outlines what services are covered (e.g., preventive care, prescriptions, mental health, maternity, emergency services) and what isn’t. Pay attention to coverage for specific activities if you plan on adventure tourism or particular sports.

- Out-of-Pocket Maximum: This is the most you’ll have to pay for covered services in a plan year. Once you hit this limit, your insurance pays 100% of covered costs. A lower out-of-pocket maximum provides greater financial protection against catastrophic medical events.

- Prescription Drug Coverage: If you take regular medications, check the plan’s formulary (list of covered drugs) and the associated costs (tiers).

- Customer Service and Reputation: Research the insurer’s reputation for customer service, claims processing, and ease of communication. Reading reviews from other policyholders can provide valuable insights. A responsive and helpful customer service team can make a significant difference, especially if you’re new to the United States healthcare system.

Tips for a Seamless Healthcare Experience in New York

Securing private health insurance is a vital first step, but a seamless healthcare experience in New York also involves understanding how to utilize your plan effectively and maintain your well-being while immersing yourself in the vibrant local culture.

Maximizing Your Insurance Benefits While Exploring New York

- Know Your Plan Inside Out: Once enrolled, thoroughly read your policy documents. Understand your deductible, copays, coinsurance, and the process for filing claims. Keep your insurance card handy at all times.

- Primary Care Provider (PCP): If your plan requires one (like an HMO), choose a PCP shortly after arriving. They will be your first point of contact for non-emergency medical needs and referrals.

- Urgent Care vs. Emergency Room: For non-life-threatening conditions (e.g., severe cold, minor cuts, sprains), an urgent care center is usually a much more cost-effective and time-efficient option than a hospital emergency room. New York City has numerous urgent care facilities. Use the emergency room only for true emergencies.

- Telehealth Services: Many plans offer telehealth or telemedicine services, allowing you to consult with a doctor remotely via phone or video call for minor issues. This can be incredibly convenient when you’re busy exploring Fifth Avenue or taking a ferry to Ellis Island.

- Preventive Care: Most ACA-compliant plans cover preventive services (e.g., annual physicals, screenings, vaccinations) at no extra cost. Utilize these benefits to maintain your health.

Staying Healthy and Enjoying Your Time in the Empire State

New York is a city of endless possibilities, offering incredible experiences from the culinary delights of Chelsea Market to the thrill rides of Coney Island. However, the fast-paced urban environment can also take a toll.

- Maintain a Healthy Lifestyle: Take advantage of New York’s many parks for exercise, explore the diverse food scene for nutritious options, and prioritize sleep amidst the constant activity.

- Be Prepared for Seasons: New York experiences distinct seasons. Be ready for hot summers, cold winters, and the associated health considerations (e.g., flu season, allergies).

- Stay Hydrated: Especially when walking extensively, whether through the financial district to see One World Trade Center or exploring a museum, ensure you drink enough water.

- Mind Your Mental Health: Adjusting to a new city, especially one as intense as New York, can be stressful. Many insurance plans offer mental health benefits; don’t hesitate to use them if needed.

Having robust health insurance frees you from worry, allowing you to fully embrace the New York experience, whether that’s enjoying the luxury of a Manhattan resort or venturing out to the scenic Hudson Valley or Long Island for a day trip. It ensures that an unexpected stumble on a cobblestone street in The Bronx or a sudden illness during a visit to Staten Island doesn’t derail your adventure or lead to financial hardship.

In conclusion, securing private health insurance in New York is an indispensable part of planning any extended stay, relocation, or even a substantial trip to the state. While the process may seem intricate, understanding the landscape, your options, and the practical steps involved will empower you to make an informed decision. With the right coverage in place, you can confidently explore all the breathtaking landmarks, immerse yourself in the vibrant culture, and savor the unforgettable lifestyle that New York offers, knowing that your health and financial well-being are protected. From the bustling streets of New York City to the serene landscapes of the Adirondacks, the picturesque Finger Lakes, the charming Catskill Mountains, or even a visit to the majestic Niagara Falls, peace of mind is the ultimate travel companion.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.