Navigating the complexities of business regulations can often feel like embarking on an unexpected journey, far removed from the exciting explorations of new destinations or the luxurious comfort of a well-appointed suite. Yet, for businesses operating within the Lone Star State, understanding and fulfilling their franchise tax obligations is a crucial aspect of maintaining operational integrity. While the typical traveler might be focused on booking the perfect villa in Tuscany or discovering the vibrant local culture of Marrakech, business owners in Texas must dedicate attention to the intricacies of state taxation. This guide aims to demystify the process of filing franchise tax in Texas, ensuring compliance and peace of mind, much like having a reliable travel guide for an unfamiliar city.

The Texas franchise tax is a unique business privilege tax imposed on entities for the privilege of doing business in Texas. It is not a sales tax or an income tax. Instead, it’s based on the taxable margin of a business. For many, this concept can seem as daunting as deciphering a foreign transportation system or planning a multi-city itinerary. However, by breaking down the process into manageable steps, much like planning an extended stay in a new city, businesses can effectively manage this requirement.

Understanding Texas Franchise Tax Fundamentals

Before delving into the procedural aspects of filing, it’s essential to grasp the core principles of the Texas franchise tax. This foundational knowledge will illuminate why certain steps are necessary and what factors influence your filing obligations. Think of it as understanding the local customs and etiquette before arriving in a new country to ensure a smooth and respectful experience.

What is the Texas Franchise Tax?

At its heart, the Texas franchise tax is a tax on the privilege of doing business in Texas. It applies to all entities, including corporations, limited liability companies (LLCs), partnerships, and professional services limited liability companies (PSLLCs), that have a legal or “nexus” presence in Texas. This nexus can be established through various means, such as having employees, property, or making sales in the state. The tax is levied on the entity’s “taxable margin,” which is essentially a portion of its gross receipts after certain deductions.

Unlike an income tax, which is based on net profit, the franchise tax considers a business’s revenue and certain allowable deductions. This distinction is critical for accurate calculation and filing. For instance, a business might have a high revenue but still owe little to no franchise tax if its allowable deductions significantly reduce its taxable margin. Understanding these nuances is akin to understanding the difference between booking a budget hostel and a luxury resort; the underlying need for accommodation is the same, but the financial and experiential outcomes vary greatly.

Who is Subject to the Texas Franchise Tax?

Generally, any entity formed in Texas or “doing business” in Texas is subject to the franchise tax. This broad definition covers a wide range of business structures. However, there are specific thresholds and exemptions that can relieve certain businesses of their filing burden.

Nexus: The concept of “nexus” is paramount. An entity establishes nexus in Texas if it has sufficient physical presence or economic activity within the state. This can include:

- Having employees in Texas.

- Owning or leasing property in Texas.

- Conducting business through representatives (agents or solicitors) in Texas.

- Generating revenue from sales into Texas.

Exemptions: Texas offers several exemptions from the franchise tax. The most common is the “no tax due” threshold. If an entity’s total revenue is below a certain amount (which is adjusted annually), it may be excused from paying franchise tax, although it might still be required to file a “No Tax Due Report.” Other exemptions exist for specific industries or types of entities, such as certain non-profit organizations. Identifying these exemptions is like finding a hidden gem attraction on a travel itinerary – it can significantly simplify your journey.

Key Concepts: Gross Receipts and Taxable Margin

The calculation of the franchise tax revolves around two primary concepts: gross receipts and taxable margin.

Gross Receipts: This refers to all revenue generated by the business from all sources, with some specific exclusions. For example, certain taxes collected on behalf of another entity may not be included in gross receipts. Understanding what constitutes gross receipts is the first step in calculating your tax liability.

Taxable Margin: This is the figure on which the franchise tax is actually calculated. It is derived by subtracting allowable deductions from your total gross receipts. Texas law provides for several deductions, including:

- Compensation Deduction: A portion of the compensation paid to employees.

- Cost of Goods Sold (COGS) Deduction: Similar to income tax, this deduction applies to businesses that sell tangible goods.

- Specific Industry Deductions: Certain industries have unique deductions available.

The choice of which deduction method to use can significantly impact the final tax amount. Businesses can elect to compute their taxable margin using one of two methods: the “cost of goods sold” method or the “compensation” method. Each method has its own set of rules and complexities, and selecting the most advantageous one is a crucial strategic decision. This is comparable to choosing between different accommodation options; a budget motel might be sufficient for a short stay, while a family trip might necessitate a larger villa with more amenities.

The Franchise Tax Filing Process: Step-by-Step

Once you understand the fundamental principles, the next step is to navigate the actual filing process. This can be likened to following a detailed itinerary, ensuring each leg of your journey is accounted for. The Texas Comptroller of Public Accounts is the state agency responsible for administering the franchise tax.

Filing Requirements and Deadlines

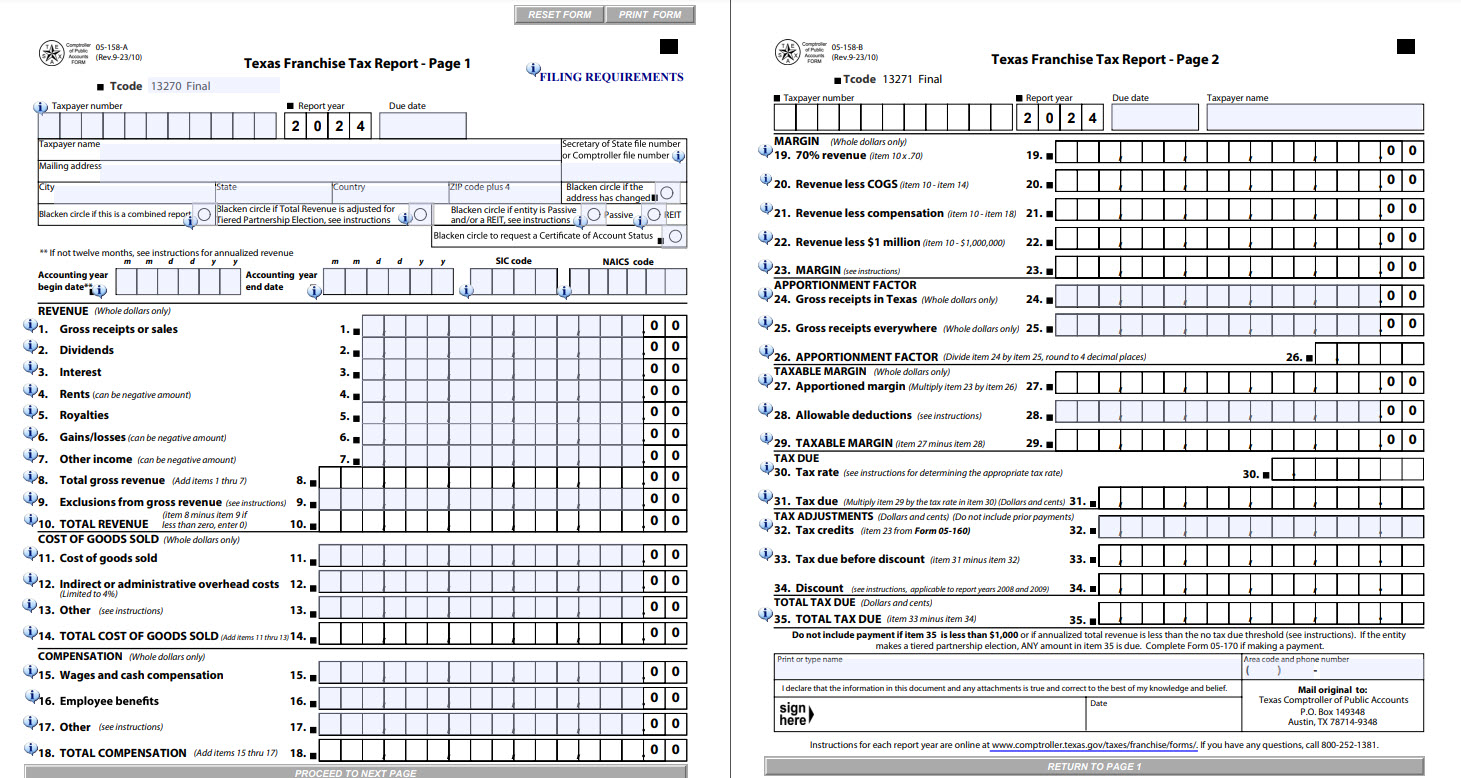

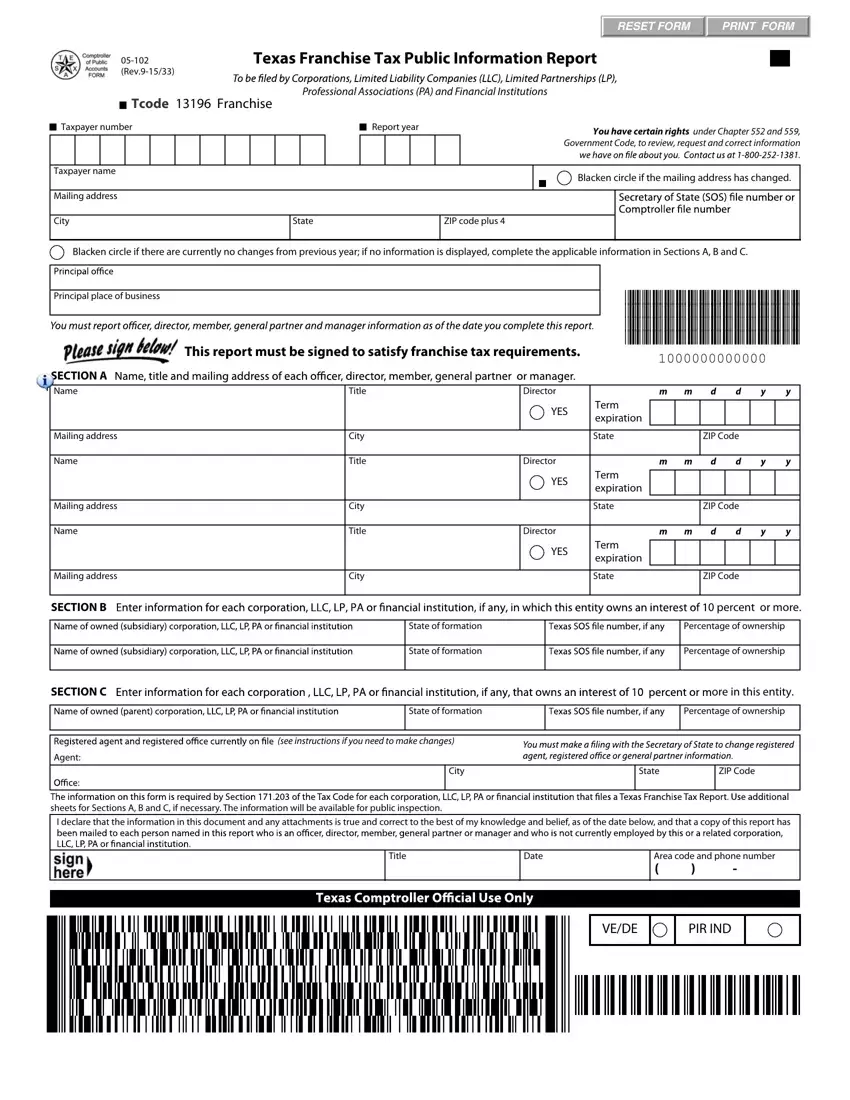

The primary form for reporting franchise tax is the Franchise Tax Report (Form 05-102, Franchise Tax Public Information Report). This report must be filed annually.

Key Deadlines:

- May 15th: The due date for most entities.

- October 15th: For entities with a fiscal year ending on December 31st, their reports are due on the 15th day of the fifth month following the close of their fiscal year. However, for the purpose of this guide, we will primarily focus on the May 15th deadline for simplicity.

Filing Methods:

- Online Filing: The Comptroller’s website offers an online filing system that is generally the preferred and most efficient method for submitting franchise tax reports. This is akin to using a mobile app to book your next hotel, offering convenience and instant confirmation.

- Mail: While less common, paper forms can be mailed to the Comptroller’s office. However, online filing is strongly encouraged to avoid potential delays.

Information Needed: To accurately complete the franchise tax report, businesses will need to gather specific financial information, including:

- Total revenue for the reporting period.

- Detailed breakdown of revenue sources.

- Information on compensation paid to employees.

- Cost of goods sold (if applicable).

- Details of any business activities conducted in Texas.

- Information for the Public Information Report, which requires details about the entity’s ownership structure and officers.

Extensions: If an entity needs more time to file, an extension can be requested. Typically, an automatic six-month extension is granted if the filer pays at least 90% of their estimated tax liability by the original due date. This is a helpful buffer, much like having a flexible cancellation policy on a flight or hotel booking.

Calculating Your Franchise Tax Liability

The calculation of the franchise tax can be complex, and seeking professional guidance is often recommended. However, understanding the general steps is beneficial.

- Determine Total Revenue: Identify all sources of gross receipts for the fiscal period.

- Apply Allowable Deductions: Subtract the eligible deductions (e.g., compensation, COGS) to arrive at the taxable margin. The Comptroller provides detailed instructions and worksheets to assist with this process.

- Apply Tax Rate: The franchise tax rate is applied to the calculated taxable margin. The rates vary depending on the entity’s total revenue and whether it is a sole proprietorship, partnership, or corporation. For businesses with revenue above certain thresholds, the tax rate is a percentage of their taxable margin.

- Check for “No Tax Due” Threshold: If the total revenue is below the established threshold, the entity may not owe any tax, but must still file the report.

Example: Imagine a small business in Austin that generates $500,000 in total revenue and has $300,000 in eligible compensation expenses. If the “no tax due” threshold is $1.23 million, this business is not exempt based on revenue. However, if the compensation deduction allows for the full compensation to be deducted, and other deductions bring the taxable margin to zero, then no tax would be owed, even though the report must be filed. This scenario is similar to planning a trip on a tight budget; you still need to plan and account for expenses, even if you aim to spend very little.

The Public Information Report

A critical component of the franchise tax filing is the Public Information Report. This report requires businesses to disclose information about their ownership structure and key individuals, such as officers, directors, partners, or managers. This transparency is a mandatory part of the filing process, regardless of whether tax is owed. It serves a similar purpose to providing detailed traveler information when booking a multi-person tour; it ensures all relevant parties are accounted for.

Seeking Assistance and Avoiding Common Pitfalls

Navigating tax regulations can be challenging, and like planning a complex travel itinerary that includes multiple flights and hotel bookings in different countries, seeking expert advice can save time and prevent costly mistakes.

When to Seek Professional Help

The Texas franchise tax system is intricate, with numerous nuances and exceptions. For many businesses, especially those with complex financial structures or significant operations in Texas, engaging a qualified tax professional is highly advisable.

- Complex Financial Structures: If your business has multiple revenue streams, significant intercompany transactions, or operations across different states, a tax advisor can help ensure accurate reporting.

- Uncertainty About Deductions: Determining which deductions are applicable and how to calculate them can be confusing. A professional can clarify these issues.

- First-Time Filers: For businesses new to Texas or new to filing franchise tax, professional guidance is invaluable.

- Audits or Inquiries: If the Comptroller’s office contacts you regarding your franchise tax filing, a tax professional can assist in responding to their inquiries.

Professionals can provide services ranging from basic tax preparation to more comprehensive tax planning and consulting. Their expertise can help identify potential tax savings opportunities and ensure compliance, much like a seasoned travel agent can curate the perfect, stress-free vacation.

Common Mistakes to Avoid

Even with careful attention, businesses can fall into common traps when filing their Texas franchise tax. Being aware of these pitfalls can help you steer clear of them.

- Missing the Filing Deadline: Late filings can result in penalties and interest. Filing electronically well before the deadline is the safest approach.

- Incorrectly Calculating Gross Receipts or Deductions: Errors in these calculations can lead to underpayment or overpayment of taxes. Meticulous record-keeping is essential.

- Failing to File a “No Tax Due” Report: Even if no tax is owed, the report must be filed. Failure to do so can be treated as a non-filing, incurring penalties.

- Incomplete Public Information Report: Omitting required information on the Public Information Report can lead to penalties.

- Not Understanding Nexus: Businesses that are not physically located in Texas might still have a nexus and be subject to the tax. Understanding the state’s nexus rules is crucial.

- Ignoring Tax Law Changes: Franchise tax laws and thresholds are subject to change. Staying informed about updates from the Texas Comptroller is important.

By taking a proactive and informed approach, businesses can successfully manage their Texas franchise tax obligations. This diligent attention to detail, much like planning every aspect of a memorable journey from booking a charming boutique hotel in Paris to discovering the best local eateries in Rome, ensures a smooth and compliant experience, allowing business owners to focus on growth and success.