Understanding the intricacies of taxation is a fundamental aspect of managing one’s finances, especially when dealing with significant assets. In the diverse and dynamic landscape of California, a state renowned for its breathtaking natural beauty, innovative industries, and vibrant lifestyle, capital gains tax stands as a crucial financial consideration for residents, investors, and anyone contemplating the sale of valuable property. From the bustling metropolises of Los Angeles and San Francisco to the serene vineyards of Napa Valley and the sun-drenched resorts of Palm Springs, the appreciation of assets—be they real estate, stocks, or cherished collectibles—is a common phenomenon. However, with that appreciation often comes a tax liability that demands careful planning and a thorough understanding of state and federal regulations.

This article aims to demystify capital gains tax within the Golden State, explaining what it is, how it applies specifically in California, and why its unique structure makes it a particularly important factor for those who call this iconic state home or choose to invest here. For individuals engaged in the travel and tourism sectors, managing accommodation properties, or simply enjoying the luxurious lifestyle that California affords, grasping these tax implications is not just a matter of compliance but a key component of sound financial strategy. Whether you’re selling a primary residence, divesting from an investment property in a coveted tourist destination, or offloading a portfolio of stocks that have soared in value, the capital gains tax in California will undoubtedly play a significant role in your net proceeds.

Understanding Capital Gains: The Basics

At its core, a capital gain is the profit one makes from the sale of a capital asset. While this concept seems straightforward, its application and taxation can be quite complex, especially when considering both federal and state regulations. In California, understanding these foundational elements is the first step toward navigating your tax obligations effectively.

What is a Capital Gain?

A capital gain arises when you sell a capital asset for more than you paid for it. Conversely, if you sell an asset for less than your purchase price, you incur a capital loss. Capital assets encompass a wide array of property, including:

- Real Estate: This is often the most significant asset for many individuals, whether it’s a primary residence, a vacation home, a rental property in San Diego, or commercial real estate. Given California’s robust property market, capital gains from real estate sales are a prevalent issue.

- Stocks and Bonds: Investments in publicly traded companies or government securities.

- Mutual Funds and Exchange-Traded Funds (ETFs): These investment vehicles are popular among both seasoned and novice investors.

- Collectibles: Items such as art, antiques, coins, stamps, jewelry, and even rare memorabilia. The vibrant arts scene and antique markets in California mean many residents might hold such assets.

- Other Personal Property: While less common for significant gains, items like boats, expensive cars, or other luxury goods can also be considered capital assets.

The “gain” is calculated by subtracting your cost basis from the sale price. Your cost basis generally includes the original purchase price plus any commissions, fees, and the cost of capital improvements. For instance, if you bought a charming bungalow in Santa Monica for $500,000 and spent $50,000 on renovations, your basis is $550,000. If you later sell it for $900,000, your capital gain is $350,000.

Capital gains are further categorized into two types:

- Short-Term Capital Gains: These are profits from assets held for one year or less.

- Long-Term Capital Gains: These are profits from assets held for more than one year.

This distinction is critically important at the federal level, where long-term gains often receive preferential tax treatment. However, as we’ll explore, California’s approach differs significantly.

Federal vs. California Capital Gains Tax

Understanding the interplay between federal and state tax laws is paramount. The United States federal government taxes capital gains based on whether they are short-term or long-term. Short-term capital gains are taxed at your ordinary income tax rates, while long-term capital gains often enjoy lower, preferential rates (0%, 15%, or 20%, depending on your income bracket). This federal distinction incentivizes long-term investment.

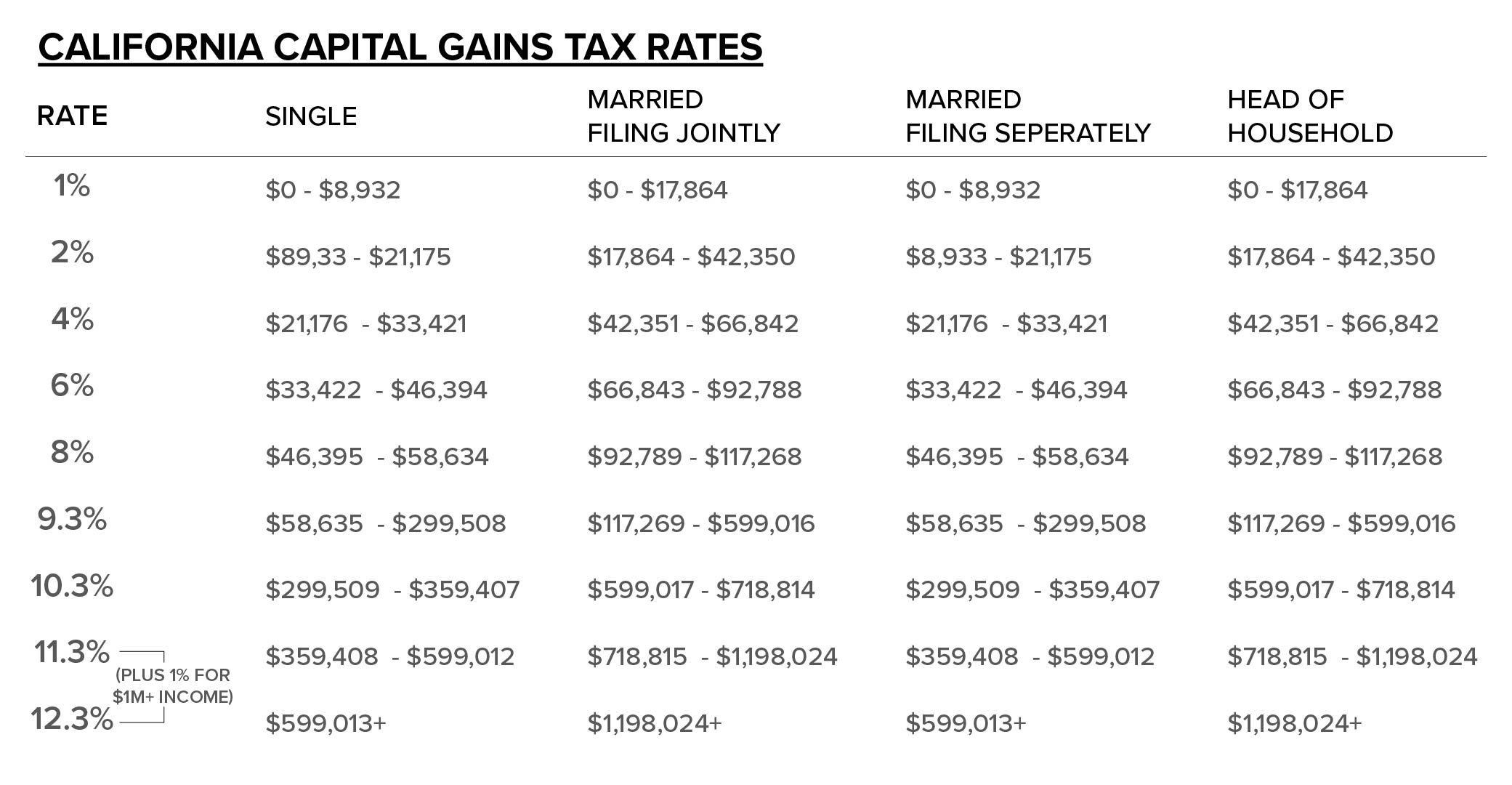

California, however, adopts a different philosophy. The state does not have a separate, lower tax rate for long-term capital gains. Instead, all capital gains, whether short-term or long-term, are taxed as ordinary income at your marginal state income tax rate. This means that a capital gain, regardless of how long you held the asset, will be added to your other income (wages, interest, etc.) and taxed according to California’s progressive income tax brackets.

This is a significant factor, as California boasts some of the highest state income tax rates in the United States, reaching up to 13.3% for the highest earners. When you combine this with federal capital gains tax rates, the total tax burden on a significant capital gain can be substantial. For a high-income earner, a long-term capital gain could be subject to a combined federal rate (e.g., 20% or 23.8% with Net Investment Income Tax) plus the California state rate of up to 13.3%, resulting in a total effective tax rate of over 30% or even higher.

Who Pays Capital Gains Tax in California?

Generally, capital gains tax in California applies to:

- California Residents: If you are a full-time resident of California, all your capital gains, regardless of where the asset is located or where the transaction occurs, are subject to California state income tax.

- Part-Year Residents: Individuals who move into or out of California during the tax year are taxed on gains realized while they were residents of the state.

- Non-Residents with California-Source Income: This is particularly relevant for those investing in California real estate. If you are not a resident of California but sell real property located within the state (e.g., a vacation rental in Big Bear Lake or an investment property in Oakland), the capital gain from that sale is considered California-source income and is subject to California capital gains tax. This rule also applies to gains from the sale of tangible personal property located in California or business interests with a California nexus.

This broad reach means that even if you live outside the state, investing in California’s lucrative markets comes with state tax implications.

The Impact on Real Estate and Property Investments in California

California’s real estate market is notoriously dynamic, characterized by high demand, limited supply, and significant property value appreciation in many areas. For homeowners and investors alike, understanding capital gains tax in the context of real estate is paramount, particularly given the state’s unique tax approach.

California’s Unique Real Estate Landscape

From the luxury condos overlooking the Pacific Ocean in Malibu to the sprawling estates in Silicon Valley, real estate across California has historically seen substantial growth. This appreciation means that when properties are sold, capital gains are almost an expected outcome.

- Primary Residences: Many California homeowners have seen the value of their homes skyrocket over decades, turning their primary residence into a significant asset.

- Investment Properties: The state’s strong tourism industry, bustling urban centers, and attractive lifestyle draw countless visitors and new residents, fueling a robust market for rental properties, vacation homes, and commercial spaces. Investors in popular destinations like Santa Barbara, Lake Tahoe, or even urban hubs like Sacramento often realize considerable gains.

- Commercial Real Estate: From hotels and resorts to office buildings and retail centers, commercial property owners in California frequently face substantial capital gains when divesting.

The sheer volume and value of real estate transactions in California mean that capital gains tax is not merely an obscure tax code detail but a major financial consideration for a vast segment of the population.

Primary Residence Exclusion

One of the most significant tax breaks related to capital gains on real estate applies to the sale of a primary residence. Both federal and state laws allow for an exclusion of a portion of the gain, provided certain criteria are met. Under Section 121 of the Internal Revenue Code, you can exclude up to $250,000 of the capital gain from the sale of your main home if you are single, or up to $500,000 if you are married filing jointly. To qualify, you must have owned and used the home as your main residence for at least two out of the five years preceding the sale. This exclusion applies to both federal and California state capital gains.

For many California homeowners, especially those who purchased their homes decades ago, this exclusion is invaluable, potentially sheltering a significant portion, or even all, of their profit from taxation. However, with skyrocketing property values in areas like Beverly Hills or Palo Alto, it’s not uncommon for gains to exceed these exclusion limits, leaving a taxable portion.

Investment Properties and Vacation Homes

Unlike a primary residence, capital gains from the sale of investment properties (e.g., rental homes, commercial buildings) or vacation homes (secondary residences) are fully taxable under both federal and California law, subject to the standard capital gains rules. There is no $250,000/$500,000 exclusion for these types of properties.

This is a critical point for individuals who own multiple properties in California, perhaps a ski chalet in Mammoth Lakes or a beach house in Laguna Beach, or those who manage short-term rentals through platforms like Airbnb or Vrbo. When these assets are sold, the entire capital gain will be added to their ordinary income for California tax purposes, potentially pushing them into higher income tax brackets.

Furthermore, if depreciation has been taken on an investment property over the years (which is common practice to reduce taxable rental income), a portion of the gain equal to the depreciation taken will be subject to “depreciation recapture.” Federally, this is taxed at a maximum rate of 25%, while in California, it’s treated as ordinary income.

1031 Exchange (Like-Kind Exchange)

For real estate investors, the 1031 Exchange, also known as a like-kind exchange, offers a powerful strategy to defer capital gains tax. This provision of the Internal Revenue Code allows an investor to defer paying capital gains tax on the sale of an investment property if they reinvest the proceeds into a “like-kind” property within a specific timeframe. Both federal and California state tax laws recognize 1031 exchanges.

The rules for a 1031 exchange are strict:

- Like-Kind Property: The new property must be “like-kind” to the old one. This generally means any real estate held for productive use in a trade or business or for investment qualifies as like-kind with other real estate held for investment, regardless of the type (e.g., exchanging a rental home for a commercial building is permissible).

- Identification Period: The investor must identify potential replacement properties within 45 days of selling the original property.

- Exchange Period: The new property must be acquired within 180 days of selling the original property or by the due date of the tax return for the year in which the old property was sold, whichever is earlier.

1031 exchanges are particularly attractive in California’s high-value market, allowing investors to recycle capital into new opportunities without immediate tax erosion. This can be an excellent strategy for those managing a portfolio of hotels, resorts, or apartment complexes, enabling them to upgrade or diversify their holdings while preserving capital. However, it’s a deferral, not an elimination, of tax, and the deferred gain typically remains attached to the basis of the new property.

Navigating Capital Gains Tax: Strategies and Considerations

Given California’s high-tax environment, proactive tax planning is essential for anyone facing a potential capital gain. Understanding various strategies and considerations can significantly mitigate the tax burden.

Tax Planning and Basis Adjustments

Accurate record-keeping is the cornerstone of effective capital gains tax planning. Your cost basis directly impacts the amount of your taxable gain.

- Original Purchase Price: Document the initial cost of acquiring the asset.

- Capital Improvements: Keep meticulous records of any significant improvements made to real estate or other assets. For a property, this could include a new roof, a major remodel, or an addition. These costs increase your basis and thus reduce your taxable gain. Routine repairs and maintenance, however, are not typically added to the basis.

- Transaction Costs: Fees associated with buying and selling the asset (e.g., real estate commissions, legal fees) can often be added to the basis or deducted from the sale price, further reducing the taxable gain.

Without proper documentation, you risk overpaying taxes by understating your basis.

The Role of Depreciation Recapture

For investment properties, depreciation is an annual tax deduction that allows property owners to recover the cost of the property over its useful life. While beneficial during the ownership period, it comes with a caveat: depreciation recapture. When you sell an investment property, any depreciation you claimed (or could have claimed) reduces your basis in the property. Upon sale, this reduction in basis increases your capital gain. The portion of the gain attributable to depreciation is “recaptured” and taxed. Federally, this depreciation recapture is taxed at a maximum rate of 25% (for Section 1250 property). In California, as with other capital gains, it’s added to your ordinary income and taxed at your marginal state income tax rate. This means that depreciation recapture can be particularly costly in California.

State Income Tax Brackets and Capital Gains

California’s progressive income tax system means that the more income you earn, the higher your marginal tax rate. Since capital gains are treated as ordinary income in California, a substantial capital gain can easily push a taxpayer into a much higher state income tax bracket. The top marginal state income tax rate in California is currently 13.3%, which includes a 1% surcharge on incomes over $1 million for mental health services (Prop 63).

Consider an individual with a modest salary who sells a long-held investment property in San Jose for a significant gain. This gain, when added to their salary, could catapult them into one of the highest state tax brackets, resulting in a substantial tax bill. This makes tax timing and planning strategies even more crucial in California.

Estate Planning and Capital Gains

For those planning their estate, understanding the “step-up in basis” rule is vital. When an individual inherits an asset, its cost basis is “stepped up” to its fair market value on the date of the decedent’s death. This means that if heirs later sell the inherited asset, they will only pay capital gains tax on any appreciation that occurred after the original owner’s death.

For example, if a parent bought a home in Pasadena for $200,000, and it’s worth $1.5 million at their passing, the heirs inherit it with a basis of $1.5 million. If they sell it shortly thereafter for $1.5 million, there would be no capital gains tax due, even though the original owner had a $1.3 million unrealized gain. This rule provides a significant benefit for heirs of appreciated assets in California and is a key consideration in estate planning.

Practical Considerations for California Residents and Investors

The complexities of capital gains tax in California demand a strategic approach, especially for those with substantial assets or intricate financial situations.

When to Consult a Professional

Given the high tax rates and unique rules in California, it is almost always advisable to consult with a qualified tax professional, such as a Certified Public Accountant (CPA) or a tax attorney, before undertaking any transaction that could result in a significant capital gain. This is particularly true for:

- Large Real Estate Sales: Selling investment properties, vacation homes, or primary residences with gains exceeding the Section 121 exclusion.

- Complex Investment Portfolios: Managing significant stock sales, especially across different tax years.

- Inherited Assets: Understanding the basis of inherited property and potential tax liabilities.

- 1031 Exchanges: Navigating the strict rules and deadlines for these transactions requires expert guidance.

- Non-Residents with California Property: Understanding reporting requirements and withholding obligations (e.g., FIRPTA for foreign sellers, or California withholding requirements for non-resident sellers).

A professional can help you accurately calculate your basis, identify eligible deductions or deferrals, plan the timing of sales, and ensure compliance with both federal and state regulations, potentially saving you a significant amount in taxes.

Impact on Lifestyle Choices

Capital gains tax can profoundly influence lifestyle decisions for California residents.

- Selling a Second Home: The decision to sell a cherished vacation property, perhaps a beachfront condo in Orange County or a mountain retreat in Tahoe, might be heavily influenced by the anticipated tax bill. Some owners may choose to hold onto the property longer, explore 1031 exchanges, or even convert it into a primary residence for a period to qualify for the Section 121 exclusion.

- Relocation Decisions: For high-net-worth individuals, the cumulative impact of California’s capital gains tax and high income tax rates can be a factor in decisions to relocate to states with lower or no income tax, particularly if they anticipate realizing substantial gains from asset sales.

- Investment Strategy: Investors might adjust their portfolios, perhaps focusing more on tax-advantaged investments or strategies that generate income rather than capital appreciation, or structuring their holdings to optimize tax outcomes.

The Future of Capital Gains Tax in California

The landscape of taxation is never static. California, known for its progressive policies and continuous debates around wealth redistribution, occasionally sees proposals for changes to its capital gains tax structure. While specific proposals vary, discussions sometimes revolve around imposing a wealth tax, adjusting income tax brackets that affect capital gains, or even introducing new surcharges. Staying informed about potential legislative changes is part of prudent financial planning for anyone with significant assets in the state. Monitoring news from the California Franchise Tax Board (FTB) and legislative bodies is advisable.

In conclusion, understanding capital gains tax in California is essential for effective financial management. Unlike the federal system, California taxes all capital gains as ordinary income, often at some of the highest state rates in the nation. This unique approach, combined with the state’s vibrant economy and appreciating asset values, makes proactive planning, accurate record-keeping, and professional guidance indispensable. Whether you are buying a dream home, investing in a thriving business, or simply managing your personal wealth, being well-versed in California’s capital gains tax structure will empower you to make informed decisions and optimize your financial outcomes in this iconic state.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.